Top 10 Fiat-to-Crypto Payment Providers and Methods

Key Takeaways

- Method choice is a risk choice. Bank transfer and Open Banking reduce chargeback exposure; card rails maximize speed but raise dispute and approval volatility.

- “Lowest fee” is rarely a single number. Your effective cost is processor fee + FX/spread + rail costs, and those layers are bundled differently by each provider.

- Integration path sets your operational scope. API gives control but increases implementation and compliance surface; hosted checkout and plugins reduce scope but limit routing and customization.

- Custody and settlement models are counterparty decisions. You need clarity on who holds fiat/crypto at each stage and what happens during outages, reviews, or bank partner changes.

In practice, vendors in this space range from exchange-led offerings to specialist rails: you may encounter legacy brands like CoinsBank and SpicePay, as well as newer players like Swapin, each positioning differently as a payment service provider for merchants building a fiat to crypto payment gateway or selecting a best crypto payment gateways, with differences in regulatory workflow, support for a local payment method, and whether they offer an embedded on and off ramp widget for fast integration via a crypto onramp.

Fiat-to-crypto payment infrastructure comes in forms that individuals and businesses alike need—no wonder that many providers choose to not limit their services to either and offer comprehensive solutions.

This guide maps the provider landscape to the rails that actually move money, the integration patterns that shape user experience, the fee mechanics that drive effective cost, and the compliance and risk constraints that determine approval rates. Whether you’re using a fiat-to-crypto exchange for an instant purchase or building an embedded flow that can also support crypto-to-fiat conversion for cash out, the goal is the same: understand what is happening at each lifecycle stage—authorization, conversion, delivery, and settlement—and choose accordingly.

Overview

In a general meaning, a fiat-to-crypto on-ramp converts government-issued currency into cryptocurrency through payment infrastructure that connects traditional financial systems to blockchain networks. The practical questions are not whether the conversion happens, but where it happens (custodial account vs self-custody wallet), how fiat moves (bank rails, card networks, Open Banking), and when the provider considers a transaction final enough to release crypto.

On-Ramp Definition

An on-ramp facilitates fiat-to-crypto conversion; an off-ramp, as the name implies, reverses that flow by converting cryptocurrency back to fiat and depositing it into a bank account. “Provider” describes the business entity: exchange, aggregator, widget vendor. “Method” or “payment rail” describes the channel that moves fiat (SEPA, ACH, wire, Visa, Mastercard, Open Banking).

What an on-ramp does not do matters just as much:

- Not a blockchain bridge — bridges move crypto across networks; on-ramps inject fiat liquidity.

- Not DeFi swapping — DEXs swap crypto-to-crypto; on-ramps convert fiat-to-crypto.

- Not guaranteed final pricing until execution — quotes expire, spreads shift, network fees fluctuate.

- Not an approval guarantee — KYC, AML screening, payment validation, and geo restrictions can block completion.

Custody model, i.e. who owns a cryptographic proof of ownership, determines where the purchased cryptocurrency lands. The binary is: Custodial (assets arrive in an account controlled by the provider until the user withdraws) or non-custodial: assets are delivered directly to a user-controlled wallet address.

To keep other terms consistent across the rest of the article, here is the compact glossary used throughout:

- Payment rail — the underlying financial network moving fiat from the user to the provider (SEPA, card network, Open Banking).

- FX/spread — the difference between mid-market rate and provider rate; a core revenue component.

- Quote — a time-limited price offer showing the crypto amount for a given fiat amount, inclusive of fee/spread.

- KYC — identity verification procedures required to confirm the user’s legal identity.

- Settlement — finalization of the fiat payment and corresponding crypto release.

- Chargeback — a card-network dispute mechanism that can reverse the fiat leg after crypto delivery.

Use Cases

Consumer

There are many reasons why a retail user needs one of the fiat-to-crypto providers, even beyond purchasing their first cryptocurrency. Even for that first-time purchase, opting for such a platform instead of, say, a centralized exchange, prioritizes low KYC friction and clear fee disclosure. Other scenarios include:

- Recurring buy (for strategies like dollar-cost averaging): prioritizes predictable pricing and a fee structure that doesn’t punish frequency.

- Funding a self-custody wallet for DeFi or NFTs: prioritizes non-custodial delivery and supported blockchain networks (common targets include Solana).

- Topping up a multi-currency account: prioritizes supported fiat and crypto pairs (support for XRP or Dogecoin varies widely by jurisdiction).

- Cross-border value storage: prioritizes stablecoin availability, geographic access, and restrictions in capital-controlled regions.

Business

Business integrations shift the center of gravity from convenience to workflow alignment, reporting, and liability. The forms a fiat-to-crypto service integration can take range across:

- Embedded on-ramp in a Web3 platform: prioritizes API, SDK, and white label solution options plus documentation quality.

- Marketplace user funding: prioritizes chargeback exposure and settlement flexibility across currencies.

- Merchant checkout where the customer pays crypto but the merchant needs fiat settlement: prioritizes conversion-at-checkout economics and bank payout speed. Some gateways publish distinct service fees for “pay-in only” versus “pay-in with conversion”.

- Payroll or contractor payouts via stablecoin settlement: prioritizes bulk disbursement compliance and stablecoin liquidity.

- Treasury conversion or hedging workflow: prioritizes institutional liquidity, OTC access, and corporate bank settlement.

To summarize, it’s rare for a fist-to-crypto provider to be limited strictly to a widget to embed or a checkout where a user can buy or pay with crypto. They span a long list of scenarios for various business and consumer needs.

Fiat-to-Crypto Payment Methods

Before we look into the crypto side of the deal, let’s review the other half. Traditional finance rails most commonly attached to these services come with their own benefits and drawbacks. As a consumer, you might want to apply different rails to various situations and as a business, it might be useful to know what the user experience will be like for your own customer.

Bank Transfer

Bank transfers are structurally diverse because regional rails define speed and operational complexity:

- SEPA transfers typically settle in one business day.

- UK Faster Payments can confirm within seconds to minutes for domestic GBP.

- ACH transfers follow batch settlement, often same-day or next-day, but some platforms add holds.

- SWIFT transfers can take three to five business days due to correspondent banking.

Best for: Larger purchases where minimizing per-transaction fees matters more than immediate delivery.

Typical speed: Minutes to hours for UK Faster Payments and instant SEPA; one business day for standard SEPA; one to two business days for ACH; three to five business days for SWIFT.

Common fees: 0% to 1.5% processor fees; potential bank fees (€0–€10 SEPA, $25–$35 SWIFT); FX spreads (often 0.5%–2%); typically cheaper than cards for comparable amounts.

Failure and decline reasons: beneficiary name mismatch; missing reference codes; intermediary bank holds (SWIFT); sending-bank compliance holds; incorrect IBAN/account details; insufficient funds and return fees.

Risk and compliance notes: minimal chargeback risk; moderate KYC friction; reconciliation issues when reference IDs are missing.

Debit Card

Debit cards usually run on Visa or Mastercard rails and draw from existing funds in an account, often improving approvals versus credit cards. However, 3D Secure requirements can still introduce friction, and many providers apply risk holds on first-time or large transactions.

Best for: Mid-sized purchases where speed and approval reliability matter more than minimizing fees.

Typical speed: Authorization in seconds; crypto delivery in minutes to hours depending on risk policy.

Common fees: 1.5% to 4.5% processor fees plus interchange; possible issuer FX fees (1%–3%).

Failure and decline reasons: 3D Secure failures; country mismatch; prepaid restrictions; velocity/amount limits; fraud model triggers.

Risk and compliance notes: moderate chargeback exposure; disputes usually 60–120 days; operational costs for dispute handling.

When to avoid: large purchases where fees dominate; situations with unreliable 3DS access; repeated high-value buying that triggers velocity limits.

Credit Card

Credit cards are typically the highest-cost, highest-decline method due to chargeback risk and issuer policies. Some issuers classify crypto purchases as cash-like, triggering cash-advance fees and immediate interest accrual.

Best for: Users who prioritize instant access to crypto and accept higher cost.

Typical speed: Seconds to authorize; minutes to hours for delivery, subject to issuer and platform holds.

Common fees: 2.5%–5.5% processor fees plus FX, interchange, and potentially cash-advance fees (3%–5%) and interest; total often exceeds 5%–8%.

Failure and decline reasons: MCC restrictions; issuer policy blocks; fraud declines; 3D Secure failures; credit limit exhaustion.

Risk and compliance notes: highest chargeback exposure; chargeback windows can exceed 120 days; losses include principal plus network fees and ratio penalties.

Digital Wallet

Digital wallets often look like one method, but they split into two architectures:

- Wallet-funded card tokens (Apple Pay, Google Pay): tokenized Visa/Mastercard; inherits the underlying card’s fees and chargeback rules.

- Account-to-account wallet rails (PayPal, Venmo in supported regions): debits wallet balance or linked bank account; different economics and risk.

Best for: Mobile-first users who want fast checkout and device-based authentication.

Typical speed: Seconds for card-token rails; minutes to hours for account-to-account rails; delivery depends on platform risk holds.

Common fees: Mirrors underlying card for Apple Pay/Google Pay; typically 0.5%–2.5% for account-to-account wallet debits, plus potential wallet FX spreads.

Failure and decline reasons: same as cards for token rails; insufficient wallet balance; provider risk policies; consent expiry; tokenization errors.

Risk and compliance notes: chargeback exposure depends on the underlying funding source; KYC may be reduced if wallet KYC exists, but platforms can still require independent verification.

Open Banking

Open Banking is consent-based bank payment initiation via regulated APIs. It typically offers faster confirmation than traditional bank transfers, lower fees than cards, and reduced chargeback exposure due to strong customer authentication (SCA).

Best for: Users in supported regions (primarily Europe and the UK as of 2026) seeking low fees and fast confirmation without card networks.

Typical speed: Seconds to minutes once authenticated; delivery often faster due to lower dispute risk, but depends on bank coverage and operating constraints.

Common fees: 0.3% to 1.5%; no interchange; FX/spread still applies when currencies differ.

Failure and decline reasons: bank API downtime/coverage gaps; consent expiry; name mismatches; instant vs batch variability across banks; bank-imposed amount limits.

Risk and compliance notes: materially lower chargeback risk than cards, but not zero; moderate KYC friction; improved reconciliation via structured references.

Comparison Table

| Method | Speed | Cost | Approval Reliability | Chargeback/Dispute Risk | Best Use Case |

|---|---|---|---|---|---|

| Bank Transfer | 1–5 business days | 0%–1.5% + bank fees | High (if details correct) | Very low | Large purchases, cost-sensitive users |

| Debit Card | Minutes to hours | 1.5%–4.5% | Moderate to high | Moderate | Mid-sized, mobile-first buyers |

| Credit Card | Minutes to hours | 2.5%–8%+ | Moderate | High | Instant access, convenience priority |

| Digital Wallet | Seconds to hours | 0.5%–5.5% (varies) | Moderate to high | Moderate (card-backed) to low | Mobile users, existing wallet holders |

| Open Banking | Seconds to minutes | 0.3%–1.5% | High (in supported banks) | Low | Europe/UK, large buys, low fees |

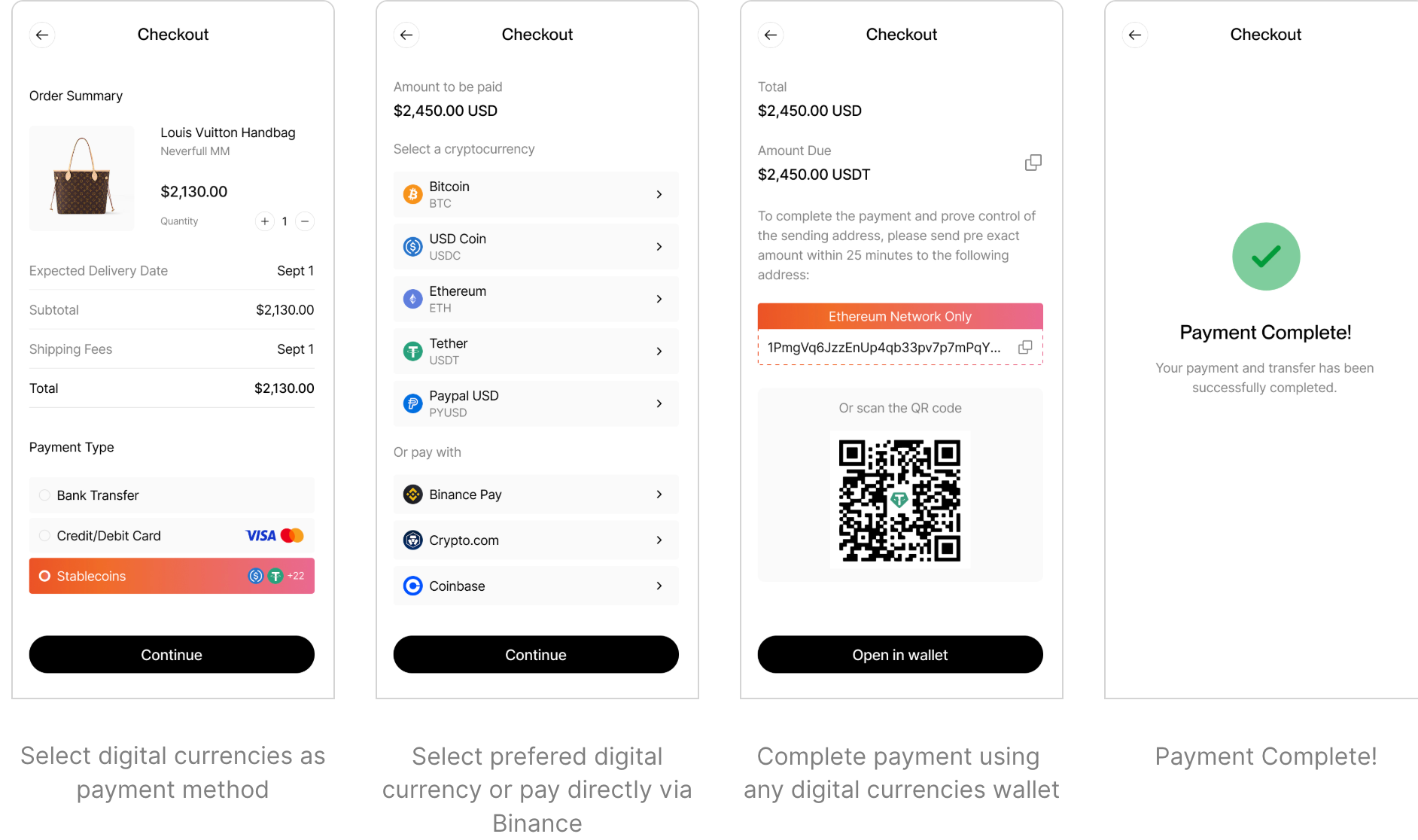

Integration Options

Integration is relevant to the business side of the service and not a purely technical decision; it is a scope decision. The more control you want over UX, routing, and state management, the more infrastructure you inherit: idempotency, webhooks, reconciliation, and support workflows.

API

Direct API integration provides the largest control surface and the highest implementation burden. You orchestrate quote lifecycle, KYC handoff, and retries without creating duplicate charges.

Integration Components Checklist:

- Authentication method patterns — API keys for server-side calls; OAuth for scoped client flows. Treat every request as a secure API call: validate signatures, rotate credentials, enforce least privilege.

- Quote creation + price expiry handling — store quote_id, expires_at, and locked_rate; display expiry countdown; handle refresh/requote logic.

- KYC/KYB handoff approach — redirect vs iframe/SDK; store kyc_session_id or customer_reference_id; do not store identity documents or unredacted PII.

- Webhooks for real-time transaction updates — implement handlers for: quote.expired, kyc.required, payment.authorized, conversion.completed, payout.settled, refund.created, chargeback.initiated, transaction.failed, withdrawal.delayed, fee.adjusted. Log event_id for traceability and handle retries.

- Idempotency keys + retries — use an Idempotency-Key header (UUIDv4) for all state-mutating operations; retry with the same key after timeouts.

- Sandbox environment and testing expectations — run full end-to-end tests: quote → KYC → payment → webhook confirmation → dashboard reconciliation.

Edge Cases Implementers Miss:

- Partial payments/underpayments (bank transfer): handle payment.partial, refund.created, quote.adjusted.

- Duplicate webhook deliveries: maintain a processed_webhook_events table keyed by event_id.

- User abandoning KYC mid-flow: handle kyc.abandoned and session resume links.

- Chargeback notification latency: chargebacks can arrive 60–120 days post-delivery; maintain reserves and automated risk flags.

- Chain/asset mismatch: validate destination address format against selected network; require explicit confirmation.

Hosted Checkout

Hosted checkout is the fastest path to production because you avoid handling raw card data and identity documents. You create a session, redirect the user, and rely on webhooks for completion.

What You Can/Can't Control Without Code:

- Branding: typically logo, primary color, limited copy.

- Payment method availability: largely constrained by provider coverage and account approval; not always toggleable per-session.

- Fee disclosure: depends on provider transparency policy.

- Settlement mode: often account-level, not per-session.

Compliance Boundary:

PCI scope shrinks because card data never touches your servers. Identity documents are uploaded to the provider. What you store is order metadata, customer reference IDs, status updates, and settlement reports.

Minimal Implementation Recipe:

- Create a checkout session (amount, fiat_currency, asset, success_url, cancel_url, merchant_reference)

- Lock or allow asset choice

- Return URLs must be asynchronous-safe (“Processing your transaction”)

- Confirm via webhook, not redirect

Payment Links

Payment links are session-less URLs distributed via email, SMS, QR code, or support chat. They excel for asynchronous invoices, low-technical merchants and high-value, low-frequency payments; high-volume in-app conversions and multi-SKU carts are a couple of use cases when they fall short.

Security Mini-Checklist:

- Link signing (HMAC/JWT)

- Anti-tamper parameters

- Phishing/forwarding risk mitigation (single-use links for high-value)

- Payer identity verification where needed

Plugins

Plugins package common integration patterns for WooCommerce/Shopify/Magento/Joomla and reduce setup to API keys and webhooks—but you inherit platform constraints and plugin maintenance risk.

When Plugins Break:

- Caching/CDN conflicts (Cloudflare, Varnish)

- Webhook endpoints without signature validation

- Theme overrides that break checkout assumptions

- Provider API changes outrunning plugin updates

Preflight Checklist for Merchants:

- Confirm fiat currencies and crypto assets

- Test in staging with sandbox keys

- Validate webhook delivery and order status transitions

- Simulate refund/chargeback events if supported

- Confirm accounting export fields exist (transaction_id, order_id, fiat_amount, crypto_amount, exchange_rate, provider_fee, network_fee, settlement_currency, timestamp)

Risks and Key Considerations

Fiat-to-crypto is a conversion business layered on top of reversible rails. Your job is to identify where reversibility exists, where custody exists, and where your liability window opens.

Approval Rate and High-Risk Category Constraints

Approval rates determine whether your product scales or stalls. Four constraint categories dominate:

- Merchant-category restrictions (MCC-like risk tiers): negotiate 30-day notice for policy changes and a documented appeal workflow.

- Jurisdictional restrictions (hard geofences / soft restrictions): require a supported-country schedule and 60-day notice before removals.

- User-level KYC thresholds: prioritize KYC processing SLA and tier fallback options.

- Velocity and limit controls: demand transparent limit schedules and a process for increases.

Approval-rate measurement protocol: Define approval rate as (successful authorizations ÷ total authorization attempts) × 100 and segment by rail, geography, and cohort. Separate declines into provider decline, issuer/bank decline, and compliance decline to identify what you can negotiate, what you can message, and what you must screen.

Custody, Settlement, and Counterparty Risk

Risk profiles vary between:

- Custodial on-ramp: provider holds fiat and crypto until delivery; insolvency/hack/regulatory seizure becomes your counterparty risk.

- Non-custodial service: provider orchestrates without holding; reduces custody risk but can reduce visibility into where value is at each moment.

- Merchant-of-record (MOR) vs agent model: MOR shifts disputes to provider but reduces control; agent model increases your liability and control.

Settlement finality and reconciliation: Demand clarity on settlement currency (fiat vs stablecoin), settlement cadence (daily/weekly/rolling T+X), cut-off times and batching rules, partial settlements vs all-or-nothing, reconciliation artifacts (payout ID, transaction IDs, fee breakdowns, CSV/API export mapping).

Control list: daily payout matching, an exception queue for held/disputed items, and reserve/hold monitoring against contractual caps.

Chargeback, Refund, and Dispute Exposure

Crypto delivery is irreversible; fiat rails are not. That mismatch defines the dispute surface.

| Scenario | Who is debited | Timeline | Evidence required | Operational steps |

|---|---|---|---|---|

| Refund (customer requests return before delivery) | Merchant or provider, depending on MOR model | Immediate to 3 business days | Proof transaction was not completed; no crypto delivery occurred | Halt delivery if still pending; reverse fiat authorization; issue refund via original payment method; log refund ID and transaction ID for reconciliation |

| Chargeback (customer disputes card charge post-delivery) | Merchant if agent model; provider if MOR model | 30–120 days after transaction | Proof of delivery (tx hash + timestamp + destination address), customer consent artifacts, KYC match, IP geolocation log | Freeze further transactions from the same user; submit representment package; trigger re-verification; send dispute-resolution communication |

| Crypto sent but card later disputed | Merchant or provider, depending on contract liability clause | 30–180 days (Visa/Mastercard dispute window) | All of the above, plus proof customer confirmed destination address and quote acceptance | Mark account high-risk; reserve/chargeback accounting; update fraud model; consider blocklist or enhanced verification |

Dispute prevention controls (specific to fiat-to-crypto):

- Strong consent capture: quote acceptance + separate wallet address confirmation

- Proof-of-delivery artifacts: tx hash + timestamp + destination address

- High-risk flags surfaced in real time: mismatched country/KYC, rapid retries, address reuse

Data Privacy and Operational Resilience

Data privacy is a compliance risk; resilience is a continuity risk. Treat both as integration requirements, not afterthoughts.

| Data category | Who processes it | Retention expectations | Transfer mechanism |

|---|---|---|---|

| PII (name, email, phone) | Merchant and provider; subprocessors if hosted KYC | Provider: per-jurisdiction regulation (e.g., MiCA, GDPR); Merchant: per your privacy policy | API (if merchant collects) or hosted checkout (if provider collects) |

| KYC documents (passport, driver's license, selfie) | Provider and KYC subprocessor (e.g., Onfido, Jumio) | Typically 5–7 years for AML compliance; confirm with provider's DPA | Hosted KYC widget (provider-controlled) or API upload (merchant-controlled) |

| Payment data (card number, bank account) | Provider and payment processor (e.g., Stripe, Adyen); merchant never touches raw card data | PCI DSS standards apply; provider must be PCI Level 1 certified; Merchant should not store card data | Hosted checkout or tokenized API (merchant receives token, not raw PAN) |

| Wallet addresses | Merchant and provider; potentially on-chain analytics subprocessors | Indefinite (on-chain record is permanent); provider may retain address in transaction logs per AML retention | API (merchant sends destination address) or hosted widget (provider collects address from customer) |

| Device fingerprints | Provider and fraud-prevention subprocessor (e.g., Sift, Forter) | Typically 12–24 months; confirm with provider's fraud vendor DPA | Hosted checkout (provider collects via JavaScript) or API (merchant collects via SDK) |

Fiat-to-Crypto Provider Reviews

The providers below span three categories—consumer exchanges, business payment gateways, and infrastructure/embedded on-ramps—and are evaluated across: supported purchase rails, settlement and custody options, integration tooling, fee structure, and geographic/compliance constraints.

Availability, pricing, and onboarding requirements vary by jurisdiction, merchant category, and risk profile. Use these as decision-ready starting points, then confirm your corridor-specific details in the vendor’s documentation.

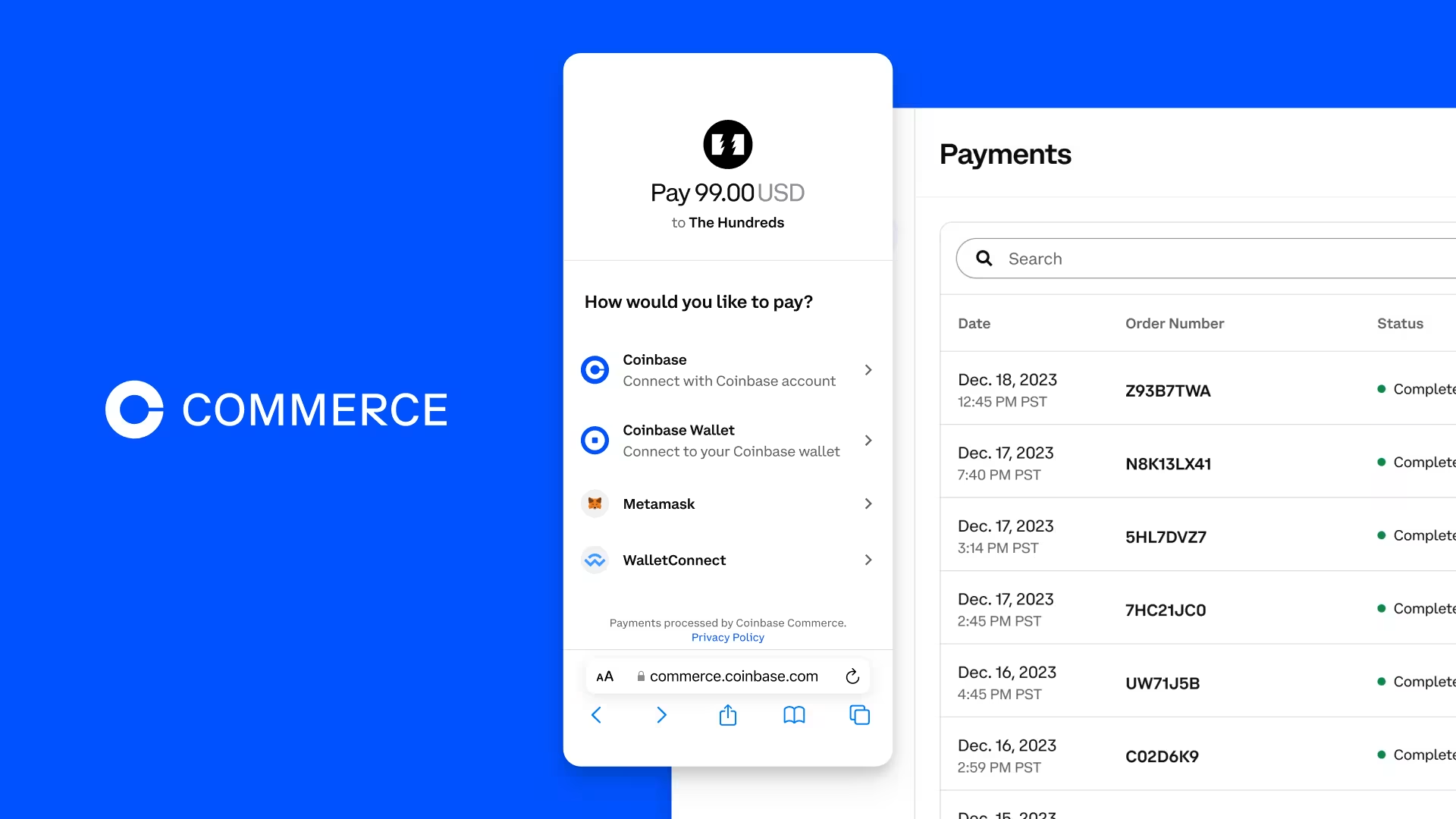

Coinbase

Best for: US-based businesses and retail consumers seeking a simple fiat-to-crypto on-ramp with bank account settlement and familiar brand trust.

What it is: Coinbase operates as both a consumer cryptocurrency exchange and, through Coinbase Commerce, a business payment gateway for merchants accepting digital assets.

Supported purchase rails: Bank transfer (ACH for US customers, SEPA for Europe), debit card (Visa and Mastercard), wire transfer, and PayPal (US only); Apple Pay and Google Pay are supported on mobile for eligible customers.

Settlement & custody: Merchants using Coinbase Commerce receive payments directly to a self-custody wallet or can opt to settle to their Coinbase account, where they control whether to convert to fiat and transfer to a bank account or hold in stablecoin; consumer exchange flows are custodial until user initiates withdrawal to external wallet.

Integration options: API access with comprehensive documentation, hosted checkout pages that require minimal integration effort, payment links for invoicing, and plugins for WooCommerce and Shopify; developer sandbox environment is available for testing.

Fees (headline): Consumer exchange spread ranges from 0.5% to 2% depending on order size and funding method; debit card purchases carry an additional 3.99% fee; ACH bank transfers typically incur a 1.49% fee; Coinbase Commerce charges merchants 1% per transaction with no monthly fees.

Coverage constraints: Available in over 100 countries, with US, UK, and EU markets receiving the broadest rail and settlement support; KYC is mandatory for all consumer accounts, and KYB verification applies to business accounts; high-risk merchant categories (gambling, adult content) face restrictive policies or outright rejection during onboarding.

Notable strengths:

- Local bank account settlement in multiple fiat currencies (USD, EUR, GBP) with SEPA and ACH support

- Developer-friendly API with extensive event webhooks and reconciliation exports for automated bookkeeping

Watch-outs:

- Card-funded purchases carry chargeback exposure, and Coinbase's dispute resolution process can freeze account access during investigations

- Pricing opacity for high-volume merchants—standard published rates do not reflect negotiated enterprise pricing, and FX spreads are not disclosed separately from transaction fees

Implementation notes: Webhook delivery for payment confirmations is real-time, but on-chain settlement (when merchant chooses non-custodial flow) depends on network congestion; test API keys in sandbox mode replicate production behavior except for actual blockchain writes; transaction exports for reconciliation are available in CSV format with filterable date ranges.

Binance

Best for: International merchants and consumers requiring broad cryptocurrency selection, low-fee trading, and access to local payment rails in emerging markets.

What it is: Binance functions primarily as a global consumer cryptocurrency exchange with Binance Pay as its merchant-facing payment gateway for point-of-sale and e-commerce acceptance.

Supported purchase rails: Bank transfer (local rails vary by region—SEPA in Europe, PIX in Brazil, UPI in India), debit and credit card (Visa, Mastercard), peer-to-peer marketplace for cash and bank-based trades, third-party payment processors (Adyen, Simplex, Paxos), and Apple Pay/Google Pay in supported regions.

Settlement & custody: Binance Pay allows merchants to settle in the original cryptocurrency received (Bitcoin, Ethereum, stablecoin) or convert to fiat and withdraw to a linked bank account; all funds remain in Binance's custodial infrastructure until withdrawal is initiated; no non-custodial settlement option exists for merchant accounts.

Integration options: Binance Pay API with REST and WebSocket endpoints, QR code-based checkout for physical retail, payment links for invoicing, hosted checkout widget for websites, and plugins for WooCommerce; sandbox environment is provided with test API credentials.

Fees (headline): Consumer spot trading fees start at 0.1% maker/taker and decrease with volume; debit/credit card purchases incur processor fees ranging from 3% to 5% depending on issuer and region; Binance Pay charges merchants 0% transaction fees, but currency conversion spreads apply when settling to fiat (typically 0.5% to 1%).

Coverage constraints: Operates in over 180 countries, but regulatory restrictions limit or prohibit service in the US, UK (partial restrictions on derivatives), Canada, and several other jurisdictions; KYC is mandatory for accounts exceeding basic withdrawal limits; certain merchant categories (unregulated securities, high-risk goods) are excluded from Binance Pay onboarding.

Notable strengths:

- Zero-fee merchant acceptance through Binance Pay when settling in cryptocurrency, making it cost-effective for businesses willing to hold digital assets

- Extensive local payment rail coverage in Asia, Africa, and Latin America, including mobile money and regional banking networks that other providers do not support

Watch-outs:

- Regulatory uncertainty and historical enforcement actions create compliance risk for merchants relying on Binance as a sole settlement provider—account freezes and withdrawal delays have been reported during regulatory investigations

- Card-funded transactions carry elevated chargeback risk, and Binance's dispute resolution process can delay access to funds during investigation periods

Implementation notes: Webhook notifications for payment status updates deliver within seconds under normal network conditions, but on-chain confirmation times vary by cryptocurrency and network congestion; reconciliation reports export in CSV format with transaction ID, timestamp, asset type, and settlement currency; test environment replicates production API behavior but does not execute real blockchain transactions.

Crypto.com

Best for: Retail-focused businesses and consumers seeking integrated crypto payment acceptance alongside a feature-rich consumer exchange with rewards programs and card funding options.

What it is: Crypto.com operates as a consumer exchange with an associated merchant payment gateway (Crypto.com Pay) that allows businesses to accept cryptocurrency at checkout while benefiting from promotional integration with the platform's user base.

Supported purchase rails: Bank transfer (SEPA for Europe, ACH for US where available), debit and credit card (Visa, Mastercard), Apple Pay and Google Pay on mobile, and peer-to-peer transfers between Crypto.com users.

Settlement & custody: Merchants using Crypto.com Pay receive payments in cryptocurrency to a custodial Crypto.com merchant account; fiat settlement is available by converting received assets and withdrawing to a linked bank account; no direct non-custodial option exists—funds remain in Crypto.com's custody until withdrawal.

Integration options: API access with RESTful endpoints, QR code checkout for in-store payments, payment links for invoicing, hosted checkout pages requiring minimal technical integration, and plugins for Shopify; sandbox environment is available for testing payment flows.

Fees (headline): Consumer exchange trading fees range from 0.075% to 0.4% depending on volume tier and account level; card purchases incur a 2.99% fee; Crypto.com Pay charges merchants 0% transaction fees when settling in cryptocurrency, but fiat conversion carries a spread typically around 0.5% to 1%, and bank withdrawal fees vary by region and currency.

Coverage constraints: Available in over 90 countries, with strongest support in Europe, Asia-Pacific, and select Latin American markets; US availability is limited and varies by state due to regulatory restrictions; KYC is mandatory for all accounts, and KYB applies to merchant accounts; high-risk merchant categories face restrictions or exclusion during onboarding.

Notable strengths:

- Native integration with Crypto.com's consumer user base, allowing merchants to tap into an existing pool of crypto-ready customers and benefit from promotional visibility

- Zero-fee merchant acceptance when settling in crypto, combined with a streamlined onboarding process for small to mid-sized businesses

Watch-outs:

- Limited fiat settlement options compared to dedicated payment gateways—conversion to fiat and bank withdrawal require multiple steps and incur combined fees that reduce net proceeds

- Pricing for card-funded transactions is not fully transparent—published consumer card fees do not always reflect the final cost when combined with FX spreads and network fees

Implementation notes: Webhook notifications for payment confirmation deliver in near real-time, but merchants should implement retry logic for webhook failures; transaction reconciliation exports are available in CSV format with filterable date ranges and asset breakdowns; test API keys in sandbox mode replicate production behavior except for actual on-chain settlement.

Coinbase Business

Best for: US-based enterprises and institutional clients requiring fiat settlement, dedicated account management, and compliance-ready infrastructure for high-volume cryptocurrency payment acceptance.

What it is: Coinbase Business (formerly Coinbase Commerce for larger enterprises) is a business payment gateway built on Coinbase's exchange infrastructure, offering custodial payment acceptance with institutional-grade tooling and support.

Supported purchase rails: Bank transfer (ACH for US, SEPA for Europe), wire transfer for large transactions, debit and credit card (Visa, Mastercard) with interchange-plus pricing for qualifying accounts, and crypto-to-crypto transfers for existing Coinbase users.

Settlement & custody: Merchants receive payments to a custodial Coinbase account and can settle to a linked US bank account in USD or European bank account in EUR; stablecoin settlement (USDC) is available as a treasury option, allowing businesses to hold funds on-chain or within Coinbase's custody; no non-custodial flow exists—Coinbase retains custody until withdrawal.

Integration options: Comprehensive REST API with webhook support for payment status updates, hosted checkout pages with white-label branding options, payment links for invoicing, plugins for Shopify and WooCommerce, and custom integration support for enterprise clients; sandbox environment includes test transactions and reconciliation tools.

Fees (headline): Transaction fees are volume-tiered and negotiated per client—published rates start at 1% for standard accounts, but enterprise pricing can drop below 0.5% for high-volume merchants; card-funded transactions incur interchange-plus fees ranging from 2.5% to 3.5% depending on card type and issuer; ACH and wire transfers carry lower processing fees, typically under 1%.

Coverage constraints: Primarily serves US-based businesses, with limited availability in Europe and select international markets; KYB verification is mandatory, and onboarding includes enhanced due diligence for high-risk industries; certain merchant categories (gambling, adult content, unregulated financial services) are excluded or subject to additional compliance review.

Notable strengths:

- Dedicated account management and priority support for enterprise clients, including assistance with compliance reporting and regulatory filings

- Seamless fiat settlement to US bank accounts with ACH or wire transfer, and USDC stablecoin settlement for businesses seeking to hold reserves on-chain without immediate conversion

Watch-outs:

- Pricing is opaque for mid-market businesses—standard published rates do not reflect negotiated volume discounts, and FX spreads on currency conversion are not disclosed separately from transaction fees

- Account freezes and compliance holds can occur without advance notice during regulatory reviews, delaying access to funds and requiring extensive documentation to resolve

Implementation notes: Webhook delivery for payment confirmations is near-instantaneous, but merchants should implement idempotency keys to handle duplicate events; reconciliation exports include transaction ID, payment status, settlement currency, and net proceeds, available in CSV and JSON formats; API rate limits apply—consult documentation for throttling thresholds and retry strategies.

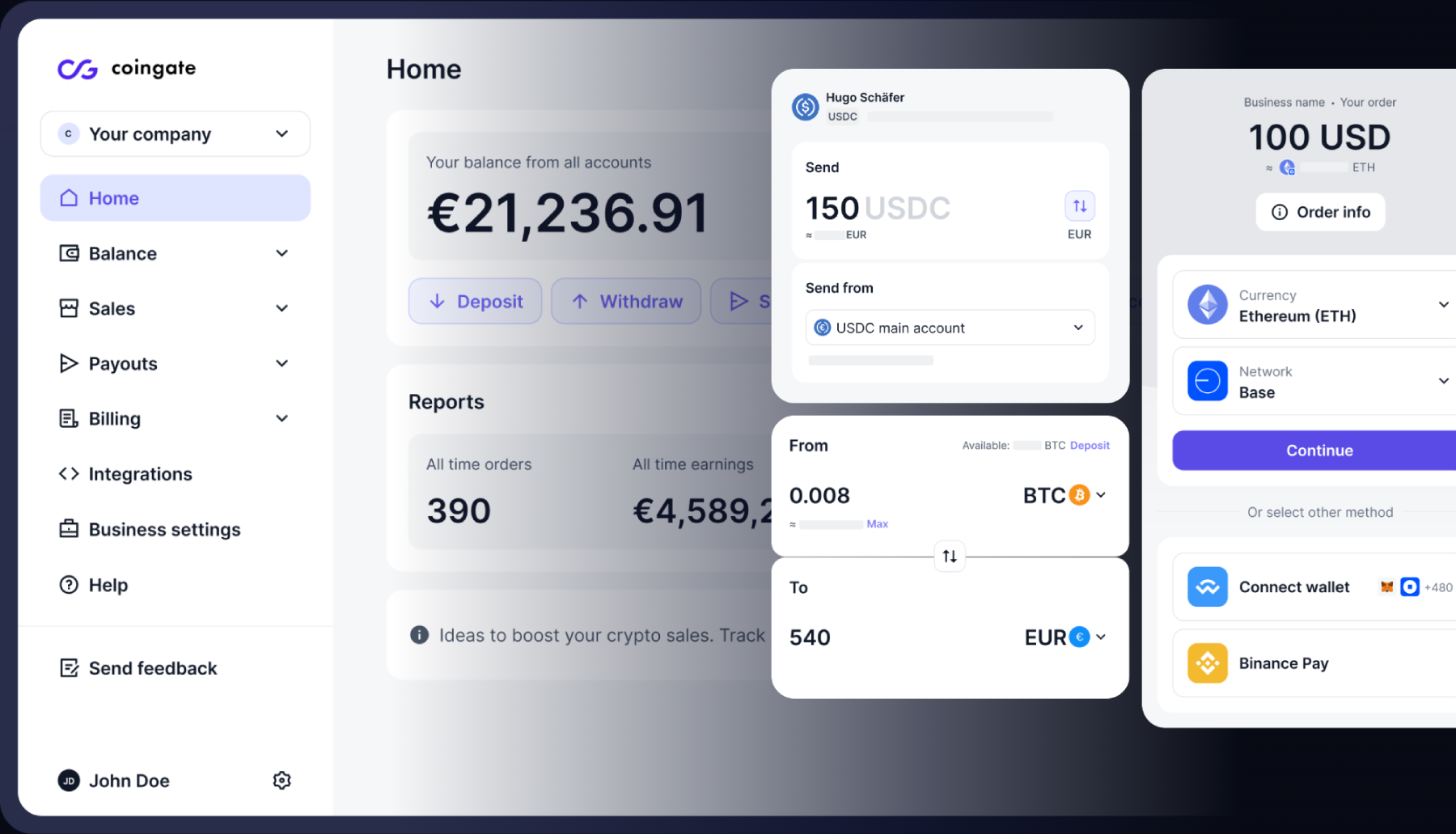

CoinGate

Best for: European small to mid-sized businesses seeking a straightforward cryptocurrency payment gateway with stablecoin and fiat settlement options and transparent pricing.

What it is: CoinGate is a business payment gateway specializing in merchant acceptance of over 70 cryptocurrencies, with automatic conversion to fiat or stablecoin settlement based on merchant preference.

Supported purchase rails: Direct cryptocurrency transfer from customer wallet (on-chain payment), Lightning Network for Bitcoin, and limited debit/credit card support through third-party integrations; no direct bank transfer or Apple Pay/Google Pay rails—customers must already hold cryptocurrency.

Settlement & custody: Merchants can settle in fiat (EUR, USD, GBP) to a linked bank account via SEPA or SWIFT, or settle in stablecoin (USDT, USDC) for treasury management; custodial flow requires funds to remain with CoinGate until withdrawal is processed; minimum withdrawal threshold is 50 EUR or equivalent, and payouts occur on a rolling schedule (daily, weekly, or monthly based on account settings).

Integration options: REST API with comprehensive documentation, hosted payment pages with customizable branding, payment links for invoicing, and plugins for WooCommerce, Shopify, Magento, and PrestaShop; sandbox environment is available for testing payment flows and webhook delivery.

Fees (headline): CoinGate charges a flat 1% transaction fee on all payments, with no setup or monthly fees; fiat settlement incurs an additional withdrawal fee (typically 1 EUR for SEPA transfers, higher for SWIFT), and currency conversion spreads apply when settling in a non-native currency; the minimum withdrawal amount is 50 EUR, which can create cash flow delays for merchants processing small transactions.

Coverage constraints: CoinGate serves more than 100 countries, with strongest support in Europe and growing availability in Asia and Latin America; KYB verification is required for business accounts, and enhanced due diligence applies to high-volume merchants; certain high-risk merchant categories (gambling, unregulated financial products) face restrictions or exclusion during onboarding.

Notable strengths:

- Transparent, flat-rate pricing with no hidden fees—1% transaction fee is clearly stated and applies uniformly across payment methods

- Support for over 70 cryptocurrencies with automatic conversion to merchant's preferred settlement currency (fiat or stablecoin), reducing treasury management complexity

Watch-outs:

- Minimum withdrawal threshold of 50 EUR can create cash flow delays for merchants processing low-value or infrequent transactions—funds remain in CoinGate custody until the threshold is met

- Limited dispute resolution tooling for on-chain payments—cryptocurrency transactions are irreversible, and CoinGate provides minimal support for refund or chargeback scenarios compared to card-based gateways

Implementation notes: Webhook notifications for payment status updates (pending, confirmed, expired) deliver within seconds, but on-chain confirmation times vary by cryptocurrency and network congestion; reconciliation exports are available in CSV format with transaction ID, payment amount, settlement currency, and net proceeds; test API keys in sandbox mode replicate production behavior without executing real blockchain transactions.

BitPay

Best for: US and international businesses requiring enterprise-grade cryptocurrency payment acceptance with fiat settlement, invoicing tools, and compliance-ready reporting for tax and accounting.

What it is: BitPay is a long-established business payment gateway that enables merchants to accept Bitcoin, Ethereum, and stablecoin payments with automatic conversion to fiat or crypto settlement.

Supported purchase rails: Direct cryptocurrency transfer from customer wallet (on-chain payment), Apple Pay and Google Pay through BitPay's wallet app, and limited debit/credit card support via third-party card-to-crypto services; no direct bank transfer rail—customers must fund with existing cryptocurrency.

Settlement & custody: Merchants can settle in fiat (USD, EUR, GBP) to a linked bank account via ACH, SEPA, or SWIFT, or settle in cryptocurrency (Bitcoin, Ethereum, USDC) for treasury management; custodial flow with BitPay holding funds until settlement; no non-custodial option exists.

Integration options: REST API with extensive documentation, hosted checkout pages with white-label branding, payment links for invoicing, and plugins for WooCommerce, Shopify, Magento, BigCommerce, and Salesforce Commerce Cloud; sandbox environment is available with test payment flows and webhook simulation.

Fees (headline): Transaction fees are volume-tiered—1% for standard accounts, with negotiated rates dropping to 0.5% or lower for high-volume merchants; fiat settlement carries an additional 1% conversion fee, and bank withdrawal fees vary by method (ACH is typically free, SWIFT incurs $25 fee); no monthly or setup fees.

Coverage constraints: Available in over 200 countries, with strongest support in North America and Europe; KYB verification is mandatory, and enhanced due diligence applies to high-volume or high-risk merchants; certain merchant categories (gambling, adult content, unregulated securities) face restrictions or exclusion.

Notable strengths:

- Robust invoicing and billing tools, including recurring payment support for subscription models and automated invoicing with customizable templates

- Comprehensive compliance and tax reporting, with built-in transaction exports formatted for accounting software (QuickBooks, Xero) and IRS Form 1099-K generation for US merchants

Watch-outs:

- Fiat settlement fees compound—1% transaction fee plus 1% conversion fee results in a 2% effective cost when settling to USD, which is higher than some competitors offering combined rates

- Account freezes and compliance holds can occur without advance notice during risk reviews, delaying access to funds and requiring extensive documentation to resolve

Implementation notes: Webhook delivery for payment confirmations is near-instantaneous, but merchants should implement retry logic for webhook failures and validate signatures to prevent spoofing; reconciliation exports include transaction ID, payment amount, settlement currency, and net proceeds, available in CSV and JSON formats; test API keys in sandbox mode replicate production behavior except for actual bank transfers.

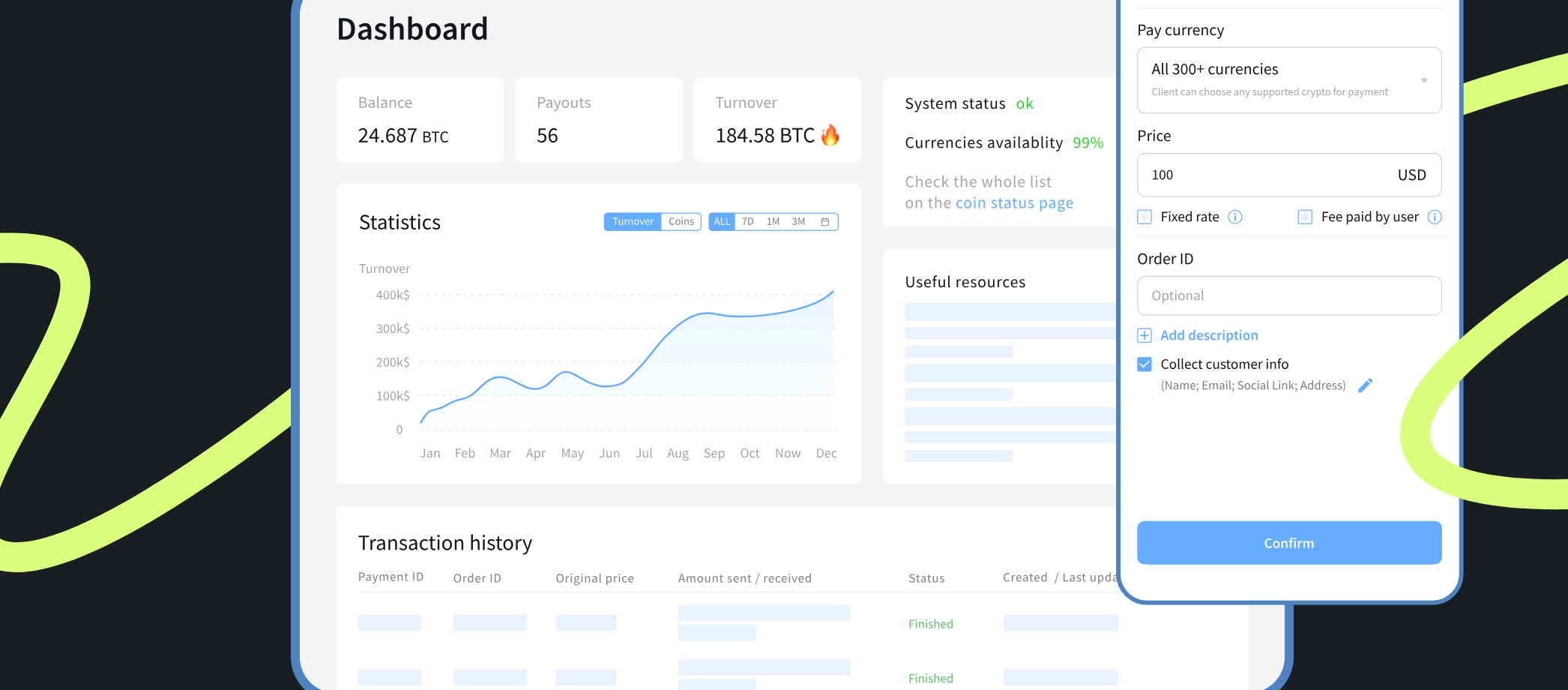

NOWPayments

Best for: Global businesses seeking broad cryptocurrency support, low-fee processing, and flexible settlement options including mass payout capabilities for affiliates and contractors.

What it is: NOWPayments is a business payment gateway offering acceptance of over 350 cryptocurrencies with automatic conversion to merchant's preferred settlement currency, including stablecoin and fiat options.

Supported purchase rails: Direct cryptocurrency transfer from customer wallet (on-chain payment), with support for over 350 cryptocurrencies and 75+ fiat currencies; no direct bank transfer or card funding—customers must already hold cryptocurrency; Lightning Network support for Bitcoin.

Settlement & custody: Merchants can settle in the original cryptocurrency received (no conversion), convert to stablecoin (USDT, USDC) for treasury management, or settle to fiat via SEPA, SWIFT, or local banking rails depending on region; custodial flow with NOWPayments holding funds until withdrawal; mass payout feature allows batch transfers to multiple recipients.

Integration options: REST API with detailed documentation, hosted payment pages, payment links for invoicing, donation widgets for non-profits, and plugins for WooCommerce, Shopify, Magento, PrestaShop, and OpenCart; sandbox environment is available for testing.

Fees (headline): NOWPayments charges a service fee split: 0.5% for mono-currency transactions (no conversion) or 1% for transactions with currency conversion; no setup or monthly fees; fiat withdrawal fees vary by method and region, typically ranging from 1 EUR for SEPA to higher SWIFT charges; minimum withdrawal thresholds apply per currency.

Coverage constraints: Operates globally with support for over 100 countries and 75+ fiat currencies, with strongest coverage in Europe, Asia, and Latin America; KYC/KYB requirements depend on transaction volume—basic accounts have lower thresholds, while high-volume merchants undergo enhanced verification; certain high-risk merchant categories face restrictions.

Notable strengths:

- Exceptionally broad cryptocurrency support (350+ assets) allows merchants to accept niche tokens and emerging assets that other gateways do not support

- Mass payout feature enables businesses to distribute payments to multiple recipients (affiliates, contractors, suppliers) in cryptocurrency or fiat, reducing treasury management overhead

Watch-outs:

- Limited dispute resolution tooling for on-chain payments—cryptocurrency transactions are irreversible, and NOWPayments provides minimal support for refund scenarios compared to card-based gateways

- Minimum withdrawal thresholds vary by currency and can create cash flow delays for merchants processing low-value transactions or accepting less-liquid cryptocurrencies

Implementation notes: Webhook notifications for payment status updates (waiting, confirming, finished, failed) deliver within seconds, but on-chain confirmation times vary by cryptocurrency; reconciliation exports are available in CSV format with transaction ID, payment amount, settlement currency, and net proceeds; test API keys in sandbox mode replicate production behavior without executing real blockchain transactions.

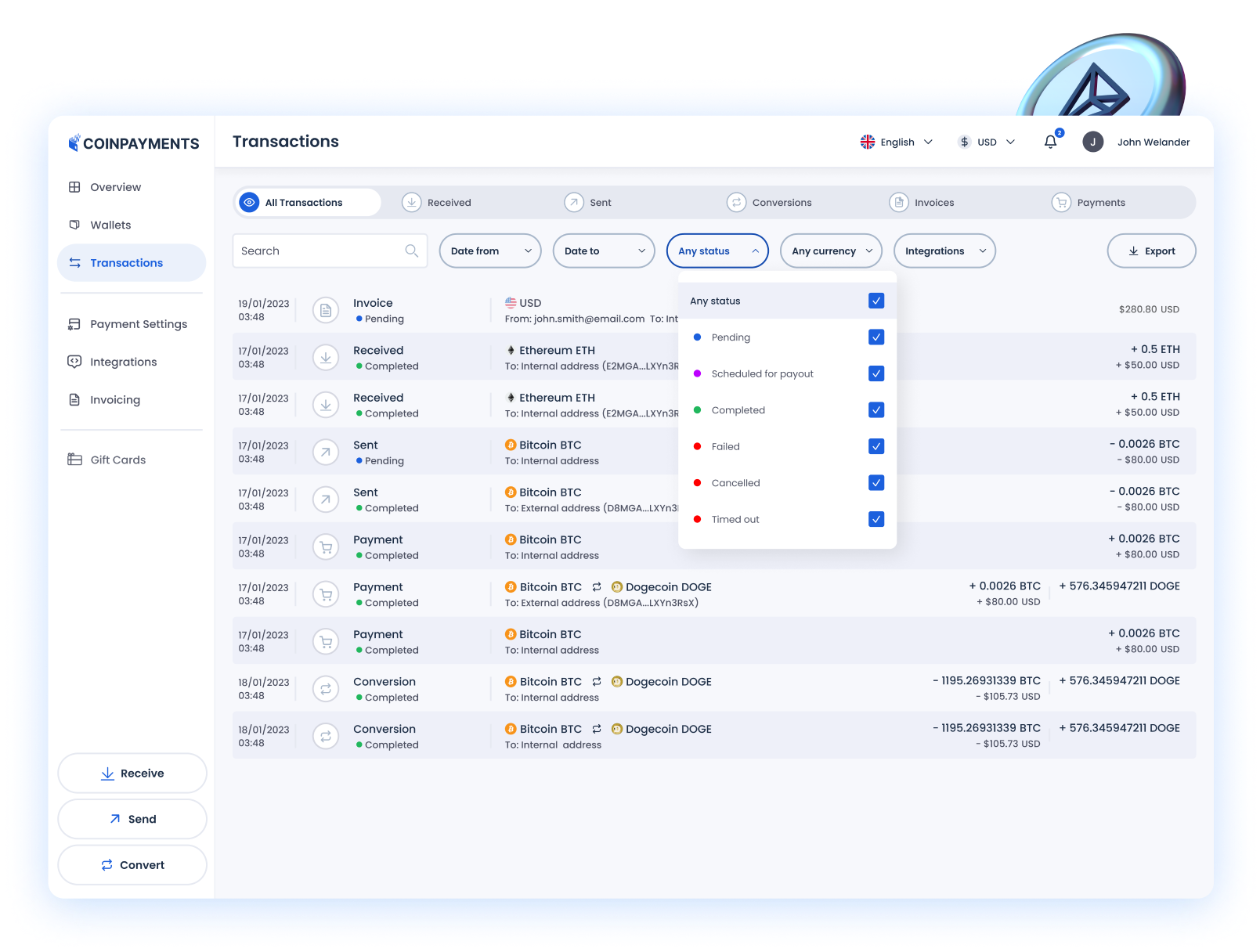

CoinPayments

Best for: International businesses requiring multi-currency cryptocurrency acceptance, auto-conversion to preferred settlement asset, and built-in wallet functionality for treasury management.

What it is: CoinPayments is a veteran business payment gateway supporting over 2,000 cryptocurrencies, with automatic conversion, wallet infrastructure, and merchant point-of-sale tools.

Supported purchase rails: Direct cryptocurrency transfer from customer wallet (on-chain payment), with support for over 2,000 cryptocurrencies; no direct bank transfer, card, or Apple Pay/Google Pay rails—customers must already hold cryptocurrency.

Settlement & custody: Merchants can settle in the original cryptocurrency received, convert to a preferred cryptocurrency or stablecoin (USDT, USDC), or settle to fiat via supported third-party exchanges; custodial wallet is provided for holding funds until withdrawal; auto-conversion feature allows instant swap to merchant's preferred asset at payment time.

Integration options: REST API with extensive documentation, hosted payment pages, payment buttons for websites, point-of-sale app for in-store transactions, and plugins for WooCommerce, Shopify, Magento, PrestaShop, and WHMCS; sandbox environment is available for testing.

Fees (headline): Transaction fees are tiered by account level—0.5% for basic accounts, with volume discounts available; auto-conversion incurs an additional 0.5% fee; fiat withdrawal via third-party exchanges carries exchange-specific fees (typically 1% to 3%); no setup or monthly fees for standard accounts, but premium features require subscription.

Coverage constraints: Operates globally with support for over 100 countries; KYB verification is required for business accounts processing above basic thresholds, and enhanced due diligence applies to high-volume merchants; certain high-risk merchant categories face restrictions.

Notable strengths:

- Exceptionally broad cryptocurrency support (2,000+ assets) provides maximum flexibility for merchants serving niche crypto communities

- Built-in wallet infrastructure with vault storage and multi-signature security options for merchants requiring treasury management without third-party custody

Watch-outs:

- Fiat settlement is indirect—merchants must use third-party exchange integrations to convert cryptocurrency to fiat and withdraw to bank accounts, adding complexity and compounding fees

- Limited customer support for free-tier accounts—priority support requires paid subscription, and response times for troubleshooting can be slow during high-volume periods

Implementation notes: Webhook notifications for payment status updates (pending, confirmed, timeout) deliver within seconds, but on-chain confirmation times vary by cryptocurrency; Instant Payment Notifications (IPN) require HTTPS endpoint and signature validation to prevent spoofing; reconciliation exports are available in CSV format with transaction ID, payment amount, settlement currency, and net proceeds.

Cryptomus

Best for: Small to mid-sized businesses seeking low-cost cryptocurrency payment acceptance with flexible settlement options and minimal technical integration requirements.

What it is: Cryptomus is a business payment gateway offering acceptance of multiple cryptocurrencies with automatic conversion to merchant's preferred settlement currency, targeting cost-conscious merchants.

Supported purchase rails: Direct cryptocurrency transfer from customer wallet (on-chain payment), with support for Bitcoin, Ethereum, Litecoin, Tether (USDT), and select altcoins; no direct bank transfer, card, or mobile wallet funding—customers must already hold cryptocurrency.

Settlement & custody: Merchants can settle in the original cryptocurrency received, convert to stablecoin (USDT, USDC), or settle to fiat via SEPA or SWIFT; custodial flow with Cryptomus holding funds until withdrawal; no non-custodial option exists.

Integration options: REST API with basic documentation, hosted payment pages, payment links for invoicing, and plugins for WooCommerce and Shopify; sandbox environment is available for testing payment flows.

Fees (headline): Cryptomus charges transaction fees starting at 0.8%, with volume discounts available for high-volume merchants; fiat settlement carries an additional 1% conversion fee; no setup or monthly fees; withdrawal fees vary by method (typically 1 EUR for SEPA, higher for SWIFT).

Coverage constraints: Operates in over 80 countries, with strongest support in Europe and Asia; KYB verification is required for business accounts, and enhanced due diligence applies to high-volume merchants; certain high-risk merchant categories face restrictions.

Notable strengths:

- Competitive transaction fees (0.8%) undercut many established gateways, making Cryptomus attractive for cost-conscious merchants processing moderate volumes

- Straightforward onboarding process with minimal documentation requirements for low-volume accounts, enabling faster activation

Watch-outs:

- Limited cryptocurrency support compared to competitors—accepts only the most liquid assets, which may restrict merchants serving niche crypto communities

- Minimal dispute resolution tooling—on-chain payments are irreversible, and Cryptomus provides basic support for refund scenarios without dedicated chargeback handling

Implementation notes: Webhook notifications for payment status updates deliver within seconds, but merchants should implement retry logic for webhook failures; reconciliation exports are available in CSV format with transaction ID, payment amount, settlement currency, and net proceeds; test API keys in sandbox mode replicate production behavior without executing real blockchain transactions.

Triple-A

Best for: Asia-Pacific businesses requiring cryptocurrency payment acceptance with strong local banking rail support, regulatory-compliant settlement, and licensed operation in multiple jurisdictions.

What it is: Triple-A is a regulated business payment gateway licensed in Singapore and other jurisdictions, offering cryptocurrency acceptance with fiat settlement and compliance-ready infrastructure.

Supported purchase rails: Direct cryptocurrency transfer from customer wallet (on-chain payment), with support for Bitcoin, Ethereum, stablecoin (USDT, USDC), and select altcoins; limited card support via third-party integrations; no direct bank transfer or mobile wallet funding—customers must already hold cryptocurrency.

Settlement & custody: Merchants can settle in fiat (USD, EUR, SGD) to a linked bank account via local banking rails (SEPA, SWIFT, local transfers), or settle in stablecoin for treasury management; custodial flow with Triple-A holding funds until settlement; licensed custody ensures regulatory compliance in supported jurisdictions.

Integration options: REST API with comprehensive documentation, hosted payment pages with white-label branding, payment links for invoicing, and plugins for WooCommerce, Shopify, and Magento; sandbox environment is available with test payment flows.

Fees (headline): Transaction fees are volume-tiered, starting at 1% for standard accounts with negotiated rates for high-volume merchants; fiat settlement carries an additional conversion fee (typically 0.5% to 1%); no setup fees, but monthly fees may apply for premium support; withdrawal fees vary by banking rail and currency.

Coverage constraints: Operates in Asia-Pacific, Europe, and select international markets, with strongest support in Singapore, Hong Kong, and Australia; KYB verification is mandatory, and regulatory licensing requirements apply to high-volume merchants; certain merchant categories (gambling, unregulated financial products) face enhanced scrutiny or exclusion.

Notable strengths:

- Licensed and regulated operation in multiple jurisdictions (Singapore, other regions) provides compliance-ready infrastructure for merchants requiring legal certainty

- Strong local banking rail support in Asia-Pacific, including SGD settlement and faster payout timelines compared to international gateways relying on SWIFT

Watch-outs:

- Limited geographic coverage outside Asia-Pacific—merchants in North America or Latin America may face higher fees or slower settlement times due to reliance on international banking rails

- Pricing is not fully transparent for mid-market businesses—standard published rates do not reflect negotiated volume discounts, and currency conversion spreads are not disclosed separately

Implementation notes: Webhook notifications for payment confirmations deliver in near real-time, but merchants should implement idempotency keys to handle duplicate events; reconciliation exports include transaction ID, payment status, settlement currency, and net proceeds, available in CSV and JSON formats; test API keys in sandbox mode replicate production behavior except for actual bank transfers.

Comparison and Selection Criteria

Checkout Experience

Its components can be verified in sandbox: hosted checkout vs embedded iframe/SDK, step count (under four is a useful target), SCA/3DS behavior and biometric support, local payment methods (SEPA, iDEAL, local cards) rendering by geography, error messaging quality and retry flows, mobile responsiveness, and even branding controls.

Conversion and Settlement Options

Resolve four branches:

- Customer rail: fiat (card/bank/Open Banking) vs crypto (wallet-to-wallet)

- Merchant settlement currency: crypto, stablecoin, fiat, or selectable

- Conversion timing: authorization vs capture vs settlement

- Conversion counterparty: internal pricing vs external routing

Service fees often change when conversion is required. One multi-currency processor charges 0.5% when no conversion happens, but 1% when conversion is triggered, illustrating the cost of bridging rails.

Treat settlement as a pipeline: authorization time — conversion time — payout initiation — payout delivery. Log timestamps for each stage and measure stage-by-stage latency. “Instant settlement” often refers only to authorization and conversion, not bank delivery via SEPA/ACH.

Conclusion

Fiat-to-crypto infrastructure in 2026 is defined by how providers bundle three cost layers—processing fees, FX/spread, and settlement rail costs—and by how they manage reversibility risk when crypto delivery is final but fiat rails are not. If you want a reliable shortlist, model your decision around approval rate, settlement mechanics, and custody exposure first, then optimize fees.

If you only remember three things:

- Total cost drivers: Effective fee = FX/spread + processing percentage + settlement rail costs. Do not compare headline rates in isolation.

- Approval rate and risk constraints: A low advertised fee with a 70% approval rate can cost more than a higher-fee provider with a 95% approval rate.

- Settlement and custody preference: Fiat settlement minimizes crypto exposure; stablecoin settlement can reduce cost and speed up delivery if your treasury workflow supports it.