Best Crypto Payment Gateways for Businesses (2026)

Key Takeaways

- 🛍️ Start with settlement strategy, not coin count: Decide upfront whether you need fiat settlement, stablecoin settlement (USDC/USDT), or crypto-to-wallet—this single choice determines volatility exposure, accounting complexity, and which providers even qualify.

- 🛍️ Custodial vs non-custodial is the real risk switch: Custodial buys you smoother refunds, reporting, and compliance posture but adds counterparty risk; non-custodial minimizes custody risk but forces you to own key management, treasury ops, and audit workflows.

- 🛍️ Top picks by use case (2026):

- 🔘 Stripe — best if you’re already on Stripe and want Bitcoin/USDC as an add-on with fiat-only settlement (crypto is not the core rail here).

- 🔘 Coinbase Commerce — best default for non-custodial checkout with direct settlement to merchant-controlled wallets (you handle conversion and compliance surface).

- 🔘 BitPay — best for regulated, licensed processing with crypto + fiat settlement options and strong compliance tooling.

- 🔘 CoinGate — best for plugin-first eCommerce launches (WooCommerce/Shopify/Magento) with flexible fiat or crypto settlement.

- 🔘 NOWPayments — best for maximum altcoin breadth (200+ assets), but it’s crypto-to-crypto only and operationally heavier.

- 🔘 BVNK / CoinsPaid — best for enterprise stablecoin + treasury-grade flows (licensing, OTC/liquidity, higher-volume operations).

Contents

- 1. Crypto Payment Gateways Explained

- 2. Payment Gateway vs Processor vs Payment Solution

- 3. How Crypto Payments Work for Businesses

- 4. Top Crypto Payment Gateways (2026)

- 5. Key Features to Evaluate

- 6. Crypto Payment Processors and Use-Case Fit

- 7. Platform and Integration Options

- 8. Risks and Key Considerations

- 9. Compliance and Legality

- 10. Conclusion

Crypto payment gateways let businesses accept cryptocurrency payments at checkout while offloading the hard parts: settlement, compliance posture, integration, and reliable reporting. In 2026, more merchants are exploring alternatives to traditional payment rails, not as a gimmick, but for lower transaction fees, faster cross-border settlement, and stablecoin-denominated revenue streams in digital currency. This guide breaks down the providers and the decision framework that operational teams actually need to implement crypto payments without surprises.

What this guide covers and doesn't cover: We focus exclusively on B2B merchant acceptance solutions—the gateways and processors that handle cryptocurrency payments at checkout and manage the settlement workflow for seamless payment processing. This is not a consumer wallet review, nor does it cover crypto trading platforms or investment services. It should also be mentioned that this guide does not constitute legal, tax, or compliance advice; availability of specific features and fee structures vary significantly by jurisdiction, and merchants should consult local regulations before implementation.

Crypto Payment Gateways Explained

A crypto payment gateway translates blockchain transactions into checkout experiences, enabling businesses to accept cryptocurrency payments from customers without manually managing wallets, exchange rates, or settlement processes. In practice, it bridges customer wallets and merchant systems by handling address generation, confirmation tracking, and conversion to fiat or stablecoins, so your team gets a plug-and-play option that feels closer to Stripe or PayPal, just for digital assets.

The category is moving fast. The global crypto payment gateway market reached $1.2 billion in 2024 and is projected to grow at 21.3% CAGR through 2034, driven by institutional adoption and stablecoin settlement demand across e-commerce and remittance corridors.

What it Does

- Eliminates manual wallet management: The gateway creates unique deposit addresses or scannable QR codes for each transaction, so merchants avoid exposing a single static wallet that complicates reconciliation and creates privacy risks.

- Protects against volatility during checkout: Most gateways freeze the cryptocurrency-to-fiat conversion rate for 10–15 minutes, ensuring the customer pays the correct amount even if Bitcoin drops 2% while they confirm the transaction on-chain.

- Balances fraud risk vs fulfillment speed: Gateways define how many blockchain confirmations are required before marking a payment "complete," letting merchants choose between instant order processing or waiting for deeper finality.

- Matches treasury strategy with settlement options: Businesses can choose to receive payouts in stablecoins like USDC, convert entirely to fiat currency and receive bank transfers, or split between both—aligning cash flow needs with volatility tolerance to stabilize cash flow.

- Automates refunds without manual intervention: Instead of asking finance teams to manually send crypto back from a wallet, the gateway handles refund transactions through its dashboard, logging the reversal for accounting and customer support.

- Feeds accounting systems: Gateways generate CSV or API-based transaction logs with timestamps, amounts, fees, and settlement data, so finance teams can reconcile crypto revenue alongside card payments without rebuilding spreadsheets from blockchain explorers.

- Triggers order fulfillment: When a payment confirms the blockchain network, the gateway fires a webhook to the merchant's order management system to notify merchant systems, updating inventory and sending shipping notifications without manual intervention.

Where the Gateway Sits in the Stack

The gateway layer acts as the interpreter between decentralized blockchain protocols and centralized business software. Customers still send transactions on Ethereum, Bitcoin, or other networks; the gateway monitors those networks, applies business logic (exchange-rate locks and confirmation thresholds), and pushes structured data into your existing stack. Settlement rails are the final destination: either your bank account (via fiat conversion) or a designated cryptocurrency wallet.

Custodial vs Non-custodial Implications

| Decision Factor | Custodial Gateway | Non-Custodial Gateway |

|---|---|---|

| Who controls private keys | Gateway provider holds keys; merchant never touches them | Merchant controls keys via self-hosted wallet or hardware device |

| KYC/KYB expectations | Provider handles compliance; merchant completes onboarding once | Merchant may need separate KYC for fiat off-ramps; compliance surface distributed |

| Failure modes | Provider outage blocks settlements; regulatory freeze locks funds | Wallet mismanagement (lost keys) = permanent loss; no recovery hotline |

| Refund execution constraints | Provider processes refunds via dashboard; funds always accessible if compliant | Merchant must manually send from controlled wallet; requires liquidity in same asset |

| Accounting evidence | Provider statements treated like bank records; clean audit trail | On-chain transaction hashes are proof; requires blockchain literacy for auditors |

Key Terminology

- Settlement: The moment funds leave the gateway's control and arrive in the merchant's designated destination (bank account or wallet).

- Fiat settlement: Cryptocurrency is converted to traditional currency (USD, EUR) and deposited into the merchant's bank account.

- Crypto-to-fiat conversion: The process of selling received cryptocurrency for fiat currency, either instantly (at time of payment) or on a schedule (daily batch).

- Stablecoin settlement: Payouts are made in USD-pegged tokens like USDC or USDT, avoiding volatility but keeping funds on-chain.

- Destination wallet: The cryptocurrency address where settled funds are sent—either controlled by the merchant (non-custodial) or the gateway (custodial).

- Payment confirmation: The point at which the blockchain network has validated the transaction with enough confirmations (blocks mined after the transaction) to be considered irreversible.

- Exchange-rate spread: The difference between the real-time market price (spot rate) and the rate the gateway charges customers or credits merchants.

- Network fee: The blockchain transaction cost (gas on Ethereum, sat/vB on Bitcoin) paid to miners/validators for processing the payment.

Each term maps to a decision point: settlement speed affects working capital, conversion timing affects margins, and fee structure determines whether crypto payments are cheaper than cards or implicitly more expensive.

Payment Gateway vs Processor vs Payment Solution

Gateways are not the only type of service facilitating payments with digital assets. However, the terms for other types may cause some confusion because judging by name alone does not give enough clarity into what each kind of service does differently. Let’s unpack this.

| Category | Payment Gateway | Payment Processor | Payment Solution (All-in-One) |

|---|---|---|---|

| Primary job | Generates payment addresses, tracks confirmations, sends webhooks | Converts crypto to fiat or executes on-chain settlements | Bundles gateway + custody + conversion + payouts + compliance tools |

| Who holds funds (if anyone) | Custodial models hold temporarily; non-custodial never touch funds | Processes conversions but doesn't store; acts as intermediary | Custodial solutions hold funds through entire lifecycle until payout |

| Typical pricing components | Gateway fee (flat or % per transaction); no conversion spread if crypto-only | Processing fee (% of settled amount) + exchange-rate spread | Gateway fee + processing fee + spread + subscription (dashboard/support) |

| Compliance responsibility surface area | Merchant handles KYC/AML if non-custodial; provider handles if custodial | Split: processor reports conversions; merchant reports sales | Provider shoulders most compliance (KYC, transaction monitoring, reporting) |

| Integration surface | API/SDK for custom checkout; plugins for WooCommerce, Shopify | API focused; requires gateway layer to feed it transactions | Hosted checkout page, plugins, and API; designed for non-technical teams |

| Best-fit business scenarios | Developers building custom flows; businesses with existing crypto treasury | High-volume merchants needing instant fiat conversion at scale | Small-to-midsize businesses wanting turnkey solution with minimal dev work |

A gateway alone won’t normally get fiat into your bank; a processor won’t generate checkout pages. Conversely, a payment solution gives you everything—on paper, but once custody, fees, and supported blockchains start limiting flexibility, the tradeoffs will be more than apparent.

How Crypto Payments Work for Businesses

Transaction Flow

Crypto payment processing follows a precise lifecycle. If you understand it end-to-end, you can tune confirmation policies, build resilient webhook handling, and reconcile revenue cleanly without turning your finance team into blockchain experts (or vice versa).

1. Pricing and Quote Creation: When a customer reaches checkout, your system requests a payment quote from the crypto payment gateway. The gateway calculates the cryptocurrency amount using exchange rate data and presents payment options across multiple cryptocurrencies and stablecoins, typically with a live crypto-fiat rate displayed for transparency.

2. Exchange-Rate Lock vs Floating Rate Window: Most gateways lock the exchange rate for a time window (typically 10–15 minutes). If the customer pays after expiration, the transaction may be flagged as underpaid due to rate fluctuations. Some merchants prefer floating rates for stablecoin-only checkouts to reduce this risk.

3. Invoice and Wallet Address Generation: The gateway generates a unique wallet address tied to the specific invoice ID. This mapping is essential for automated transaction tracking and reconciliation. The customer sees the exact amount, destination address, and QR code.

4. Customer Broadcast to Blockchain: The customer initiates the transaction from their wallet. The transaction propagates across the appropriate blockchain network, first appearing in the mempool before miners or validators include it in a block.

5. Detection (Mempool vs On-Chain): Advanced gateways detect payments at the mempool stage, updating the dashboard with a "Detected" status. This usually triggers a webhook notification, enabling preliminary order handling while awaiting confirmations.

6. Confirmation Policy and "Paid" Status: The gateway monitors confirmations based on your thresholds. Bitcoin often uses 1–2 confirmations for low-value transactions and 6 for high-value; Ethereum often needs 12; stablecoins on Tron may require 19. Once your threshold is met, the order becomes "Confirmed" or "Paid," and a second webhook fires to authorize fulfillment.

7. Real-Time Merchant Backend Integration: Webhooks deliver structured data to your system: invoice ID, transaction hash, cryptocurrency amount, fiat equivalent, timestamps, network fees, and confirmation count. This powers automated inventory and customer notifications.

8. Settlement Decision (Crypto vs Fiat): Your settlement preference is configured in the gateway. Custodial services can convert to fiat currency upon confirmation, while other setups let you accumulate crypto.

9. Crypto-to-Fiat Conversion and Spread: When fiat settlement is selected, the gateway executes conversion at current rates minus a conversion spread (typically 0.5%–1.5%).

10. Payout Rail Selection: Settlements land via bank transfer (ACH, SEPA, SWIFT), on-chain payouts to merchant-controlled wallets, or balance credits within the gateway dashboard.

11. Reconciliation Artifacts: A complete audit trail links invoice ID, customer wallet address, blockchain transaction hash, confirmation timestamps, fee breakdowns (network fee vs gateway processing fee), exchange rates at payment and settlement, and final deposited amounts.

12. Reporting and Dashboard Tracking: Dashboards and exports power accounting integration and tax compliance.

Network fees fluctuate with congestion, and can be either passed to customers or absorbed by merchants. Gateway processing fees, often 0.5%–1%, go towards infrastructure and compliance. Conversion spreads most often apply for fiat settlement, making the crypto-to-crypto alternative flow beneficial to some businesses.

As for refunds, since blockchain transactions are practically irreversible, crypto refunds are operational, not automatic. In other words, you must collect a customer refund address, calculate the refund amount with exchange-rate differences in mind, and send a new blockchain transaction. Partial refunds demand precision because—again—errors are irreversible.

Custodial Model

And now would be a good time to circle back and discuss custodial and non-custodial models. Custodial crypto payment gateways manage private keys and holdings for merchants, hence “custody”. You get a turnkey implementation and a cleaner “PSP-like” experience—at the cost of reduced control.

| Provider Controls: | Merchant Controls: |

|---|---|

|

|

In these arrangements, a business passes on the operational burden onto the processor, but it does not mean that things can’t and don’t go wrong. Here are a few risks a business can face with a custodial setup and how to mitigate them.

1. Provider Downtime Delaying Settlement:

If the custodial gateway goes down, you can’t access funds or process payouts—especially painful in high-volatility windows.

Mitigation: Keep 7–14 days of working capital in bank reserves. Negotiate SLAs with uptime guarantees and penalties. Define escalation paths. For redundancy, consider splitting volume across two custodial providers.

2. Account Holds Due to Compliance Review:

Automated systems can flag transactions, freezing withdrawals for 24–72 hours.

Mitigation: Provide robust documentation at onboarding. Configure transaction limits under review thresholds. Maintain compliance communication before seasonal spikes. Keep alternative payout rails to survive holds.

3. Counterparty Risk and Provider Insolvency:

Bankruptcy or regulatory seizure can trap funds.

Mitigation: Review financial stability, regulatory licenses, and insurance coverage. Minimize balances via aggressive payout schedules. Ask about fund segregation and custody arrangements. High-volume merchants should negotiate reserve protections or insurance where possible.

Non-Custodial Model

On the other hand, non-custodial systems keep you in control of keys and funds, which is excellent for minimizing counterparty risk. The tradeoff is that operational maturity becomes non-negotiable.

Due to somewhat increased complexity, non-custodial arrangements tend to come in two variations:

Pattern A: Gateway-Generated Addresses with Merchant Custody:

The gateway derives unique addresses per order using your xpub and monitors incoming funds without touching private keys. You must secure the master seed and derivation path records.

Pattern B: Merchant-Generated Addresses with Gateway Monitoring:

You generate addresses yourself and register them with the gateway’s monitoring API. This gives maximum control, but your database becomes the source of truth—and your internal controls must be impeccable.

Once you pass meaningful volume, multi-signature wallets stop being “nice to have” and become basic operational hygiene. For example, in a 2-of-3 multisig setup, two signatures authorize withdrawals, supporting separation of duties and reducing single-point-of-failure risk.

Internal controls should enforce that the person reconciling receipts cannot approve withdrawals. Add withdrawal thresholds (for example, secondary authorization above $10,000) and wallet-level velocity limits to contain compromise events.

How to Choose between Custodial and Non-custodial Setups?

- Fiat Settlement Requirement: Do you need automatic conversion to USD/EUR/GBP within hours of payment? (Yes → Custodial)

- Key Custody Responsibility: Are you prepared to implement enterprise-grade key management with disaster recovery procedures? (No → Custodial)

- Regulatory Exposure: Does your business model require demonstrating that you never take custody of customer cryptocurrency? (Yes → Non-Custodial)

- Stablecoin Settlement Speed: Do you need rapid stablecoin-to-bank settlement (same day) without holding crypto volatility risk? (Yes → Custodial)

- Operational Staffing: Do you have on-call technical staff available 24/7 to respond to wallet incidents, stuck transactions, or security alerts? (No → Custodial)

- Audit and Reporting: Do you require pre-built, audit-ready reporting exports that integrate with accounting software without custom development? (Yes → Custodial)

- Transaction Volume Control: Do you process fewer than 100 crypto transactions monthly where manual treasury operations remain practical? (Yes → Non-Custodial becomes viable)

- Counterparty Risk Tolerance: Is eliminating third-party custody risk worth the operational complexity of self-managed wallets? (Yes → Non-Custodial)

Top Crypto Payment Gateways (2026)

Choosing a crypto payment gateway in general is mostly about matching your operating model to the provider’s strengths. If you want non-custodial checkout with immediate wallet control, Coinbase Commerce or CoinGate are the usual starting points. Enterprise stablecoin settlement with treasury-grade infrastructure points toward BVNK or CoinsPaid. For maximum altcoin breadth across 200+ assets, NOWPayments leads the pack. Regulated operations with established licensing often favor BitPay or BVNK. Plugin-first deployment for WooCommerce, Shopify, or Magento makes CoinGate and NOWPayments a fast route to launch. Stripe, by contrast, fits teams that want crypto as one payment method inside an existing fiat infrastructure—not as the core settlement layer.

Stripe

Best for: Businesses with established Stripe fiat infrastructure seeking to add Bitcoin and USDC acceptance without changing payment stack.

Custody & settlement: Stripe retains custody of crypto received and converts it to fiat before settlement. Merchants receive USD (or local currency) deposits to their existing Stripe balance, never handling crypto directly. This eliminates volatility exposure but removes any option for crypto-native treasury management.

Integration surface: Stripe's crypto acceptance integrates through existing Checkout, Payment Links, and API endpoints. The implementation uses the same webhook structure as fiat payments, requiring minimal developer effort for stores already on Stripe. No separate sandbox environment exists for crypto—testing happens in Stripe's standard test mode.

Compliance & risk notes: Stripe performs merchant underwriting through its existing KYB process and restricts crypto acceptance based on business type and jurisdiction. The service is unavailable in multiple U.S. states and internationally restricted countries. Merchants inherit Stripe's regulatory posture but must verify that crypto payments align with their own compliance obligations. Stripe handles sanctions screening and transaction monitoring as part of its payment service provider role, positioning this as a fintech PSP feature rather than a pure gateway. Choose this if you want turnkey compliance within Stripe's ecosystem; not ideal if you require direct control over crypto settlement or multi-gateway redundancy.

Pricing and fees to confirm: Verify the processing fee (typically 2.9% + $0.30 baseline plus crypto surcharge), conversion spread applied during crypto-to-fiat settlement, any additional fees for cross-border transactions, and chargeback handling policies (noting that on-chain Bitcoin transactions cannot be reversed, though Stripe may still process disputes).

Key limitation: Crypto functionality exists as an extension of fiat payment processing, not as a standalone crypto gateway, making it unsuitable for businesses prioritizing crypto-native operations.

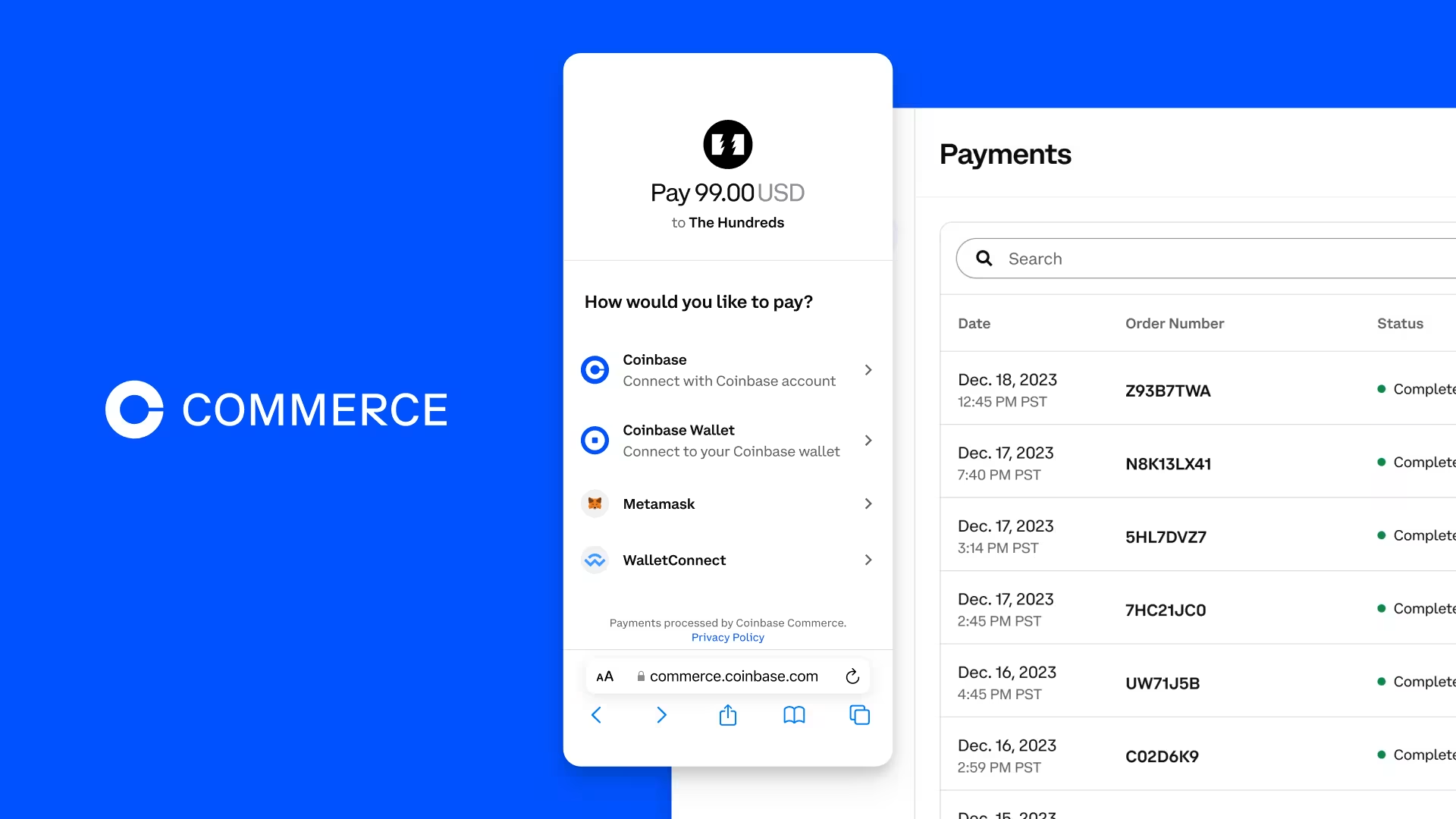

Coinbase Commerce

Best for: Non-custodial checkout for merchants who want immediate Bitcoin, Ethereum, Tether, and USDC settlement to their own wallets.

Custody & settlement: Coinbase Commerce operates as a pure non-custodial service. Customer payments flow directly to merchant-controlled wallets on supported blockchains. Settlement happens on-chain with no intermediary custody period. Merchants choosing this model accept full responsibility for wallet security, private key management, and any subsequent fiat conversion through their own exchange relationships.

Integration surface: Hosted checkout pages, embeddable payment buttons, developer API access with webhook support for real-time transaction updates, and plugins for WooCommerce, Shopify, and Magento. The sandbox environment allows testing without mainnet transactions. Invoice generation works for both one-time and recurring billing structures.

Compliance & risk notes: Since Coinbase Commerce does not hold funds or perform conversion, merchants assume primary regulatory responsibility for receiving crypto. The merchant must implement their own KYC/KYB procedures as required by jurisdiction. Coinbase Commerce provides transaction tracking and reporting exports but does not conduct sanctions screening on the merchant's behalf. Confirm that your business can legally accept direct crypto payments in operating jurisdictions and that you have infrastructure to manage tax reporting for on-chain receipts.

Pricing and fees to confirm: The processing fee (typically 1% of transaction value), whether network fees (gas) are passed to customers or absorbed by the merchant, any charges for API or webhook usage above baseline limits, and how refund handling works given that on-chain transactions are irreversible (requiring new outbound payments).

Key limitation: Merchants must manage their own crypto-to-fiat conversion, creating operational complexity for businesses without treasury infrastructure.

BitPay

Best for: Established merchants requiring licensed, regulated crypto payment processing with proven merchant tooling and long operational tenure.

Custody & settlement: BitPay offers both crypto and fiat settlement options. Merchants can receive Bitcoin, Ethereum, or stablecoins directly to their wallets (non-custodial) or opt for automatic conversion to fiat with ACH or wire settlement (custodial during processing window). The platform supports mixed settlement where a percentage goes to crypto and the remainder converts to fiat, addressing volatility concerns while preserving crypto exposure.

Integration surface: BitPay provides hosted invoicing, embeddable checkout, payment links, developer API access with comprehensive webhook support, and plugins for WooCommerce, Shopify, Magento, and custom eCommerce platforms. The platform includes a dedicated sandbox environment and real-time transaction tracking dashboard. Invoice generation supports both simple and complex billing scenarios.

Compliance & risk notes: BitPay holds money transmitter licenses in multiple U.S. states and operates under regulatory supervision in key jurisdictions. The platform performs merchant KYB during onboarding and conducts ongoing sanctions screening and AML monitoring. BitPay's compliance infrastructure is one of its primary differentiators, but merchants must still verify that BitPay's licenses cover their specific operating regions and that acceptance aligns with their industry regulations. Some high-risk merchant categories face restrictions or additional underwriting requirements.

Pricing and fees to confirm: The processing fee (typically 1% for settlement in crypto), any additional conversion fees for fiat settlement, bank settlement/withdrawal fees for ACH or wire transfers, and how chargebacks or refund requests are handled given the irreversible nature of blockchain transactions.

Key limitation: Enterprise-grade pricing and compliance infrastructure create higher barriers to entry for small merchants compared to developer-first platforms.

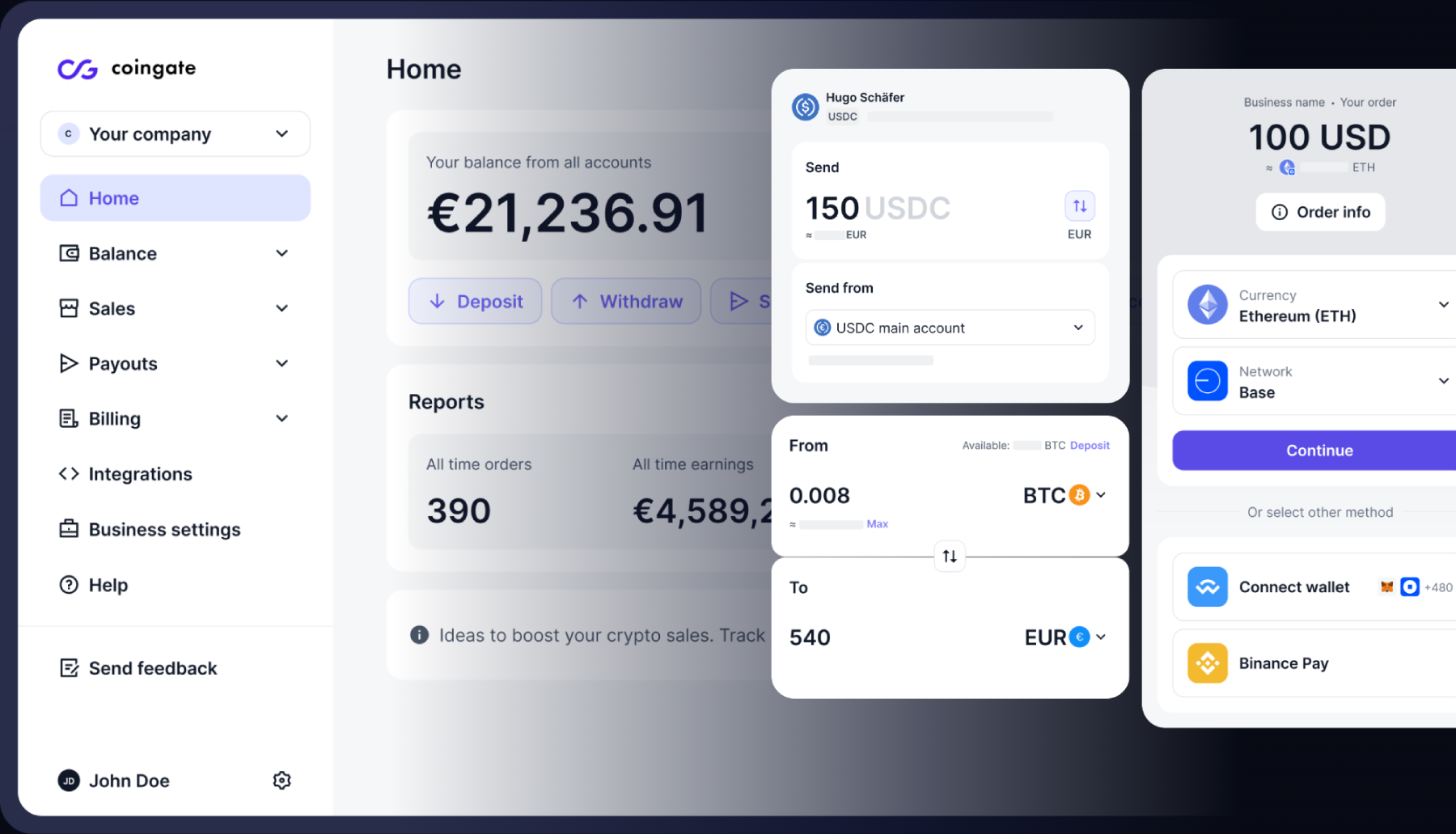

CoinGate

Best for: Plugin-first deployment for small to medium businesses on WooCommerce, Shopify, or Magento seeking fast integration with minimal technical overhead.

Custody & settlement: CoinGate supports both custodial (platform holds crypto and settles in fiat or crypto) and non-custodial modes (direct settlement to merchant wallet). Merchants selecting fiat settlement receive EUR or USD via bank transfer after automatic conversion. The non-custodial option delivers crypto to specified wallet addresses on supported chains. Settlement time varies by method, with crypto settlement occurring after blockchain confirmation and fiat settlement typically within 1-2 business days.

Integration surface: CoinGate excels in plugin support, offering pre-built integrations for over 20 eCommerce platforms including WooCommerce, Shopify, Magento, PrestaShop, and OpenCart. API access and webhook functionality support custom implementations. Hosted payment pages and invoice generation cover standard use cases. The platform provides a test mode for sandbox environment validation.

Compliance & risk notes: CoinGate operates under Lithuanian regulatory supervision and maintains compliance with European Union payment regulations. Merchants undergo KYB verification during account setup. The platform screens transactions but does not publish detailed sanctions screening protocols, so merchants operating in highly regulated industries should request documentation. Verify that CoinGate's EU-based regulatory posture aligns with your business requirements, particularly if you serve customers outside Europe or operate in jurisdictions with specific licensing requirements.

Pricing and fees to confirm: The processing fee (typically 1% for crypto settlement), fiat conversion spread for EUR/USD settlement, bank withdrawal fees, and how refunds are processed (noting that crypto transactions require manual reversal while fiat settlements may support standard refund workflows).

Key limitation: CoinGate has processed over €1 billion in lifetime payments since inception, demonstrating operational tenure, but smaller asset selection compared to specialized providers limits options for merchants seeking broad altcoin support.

NOWPayments

Best for: Merchants requiring the widest altcoin coverage with support for 200+ cryptocurrencies and tokens across multiple blockchain networks.

Custody & settlement: NOWPayments operates as a non-custodial service, with customer payments flowing directly to merchant-specified wallet addresses. The platform supports automatic conversion to preferred crypto assets if merchants want to receive payments in a different cryptocurrency than the customer sends. No fiat settlement option exists—this is a crypto-to-crypto gateway. Merchants handle their own subsequent conversion to fiat if needed. The platform has processed over $1 billion in transactions, providing operational credibility, but the extensive asset coverage creates complexity in wallet management and reconciliation.

Integration surface: API-first architecture with extensive developer API access, webhook support for real-time transaction updates, plugins for WooCommerce, Magento, PrestaShop, and custom implementations, plus hosted payment links and invoice generation. The sandbox environment allows testing across the full asset range. NOWPayments also offers payment buttons and donation widgets for content creators.

Compliance & risk notes: As a non-custodial service, NOWPayments does not perform fiat conversion or custody, shifting regulatory responsibility to merchants. The platform conducts basic transaction monitoring but merchants must implement their own KYC/KYB procedures if required. The wide asset coverage includes many low-liquidity tokens, creating potential tax reporting complexity and requiring merchants to verify that specific cryptocurrencies are legally acceptable in their jurisdictions. Confirm which assets your business can legally receive and ensure you have infrastructure to handle tax reporting across multiple blockchain networks.

Pricing and fees to confirm: The processing fee (typically 0.5% for standard transactions), any fees for automatic crypto-to-crypto conversion, network fees for different blockchain networks (which vary significantly), and how refunds are managed across 200+ supported assets.

Key limitation: Maximum asset breadth creates operational complexity in wallet infrastructure, reconciliation, and tax reporting that may overwhelm merchants without dedicated crypto treasury operations.

BVNK

Best for: Enterprise stablecoin settlement with treasury-grade infrastructure and global licensing footprint for businesses processing significant volume.

Custody & settlement: BVNK provides custodial settlement with a focus on stablecoin infrastructure (Tether, USD Coin) across multiple blockchain networks. Merchants can receive settlement in stablecoins or fiat currency through banking rails. The platform processed over £3 billion in annual volume, providing operational scale credibility. BVNK's settlement infrastructure includes OTC conversion capabilities for large transactions and treasury management features for enterprise clients. This positions BVNK as a payment service provider (PSP) with gateway capabilities rather than a pure gateway. Choose this if you want integrated treasury operations and stablecoin rails; not ideal if you require simple, lightweight API integration without enterprise complexity.

Integration surface: Developer API access with REST and webhook architecture, hosted checkout pages, payment links, and custom integration support for enterprise clients. BVNK's integration surface prioritizes enterprise use cases over plugin-based deployment, making it less suitable for small eCommerce stores. Sandbox environment and staging infrastructure support complex testing scenarios.

Compliance & risk notes: BVNK holds multiple regulatory licenses including FCA registration in the United Kingdom and money transmitter licenses in several jurisdictions. The platform conducts comprehensive KYB during merchant onboarding and maintains ongoing AML monitoring and sanctions screening aligned with PCI-DSS standards. The licensing footprint creates strong compliance positioning, but merchants must confirm which licenses apply to their specific operating regions—regulatory coverage varies by jurisdiction. Verify that BVNK's licenses align with your business's geographic and industry requirements.

Pricing and fees to confirm: Verify processing fees (typically negotiated for enterprise accounts), conversion spread for crypto-to-fiat or stablecoin-to-fiat settlement, withdrawal fees for bank settlement, and how the platform handles refund workflows for both on-chain and off-chain settlement.

Key limitation: Enterprise-first positioning and pricing create barriers for small to medium businesses seeking simple plugin-based crypto acceptance.

CoinsPaid

Best for: High-volume merchants and digital businesses requiring both payment processing and OTC desk liquidity for large cryptocurrency transactions.

Custody & settlement: CoinsPaid offers custodial settlement with options for crypto or fiat (EUR/GBP) delivery. The platform serves approximately 800 merchants and processes around €100 million in monthly volume, demonstrating operational scale. For transactions exceeding €100,000, merchants can access the integrated OTC desk for better liquidity and reduced slippage during conversion. This combined gateway-plus-liquidity model benefits high-ticket businesses that need predictable conversion rates on large amounts. Settlement timing varies by method, with crypto settlement after confirmation and fiat settlement typically within 2-3 business days.

Integration surface: API-first architecture with comprehensive developer API access, webhook support, hosted payment pages, and custom integration assistance for enterprise implementations. Plugin support exists for major eCommerce platforms but is not the primary focus. Invoice generation and payment link functionality support both B2C and B2B scenarios.

Compliance & risk notes: CoinsPaid conducts merchant KYB during onboarding and maintains transaction monitoring and AML screening. The platform's regulatory positioning focuses on European operations, though specific licensing details vary by service line. Merchants processing high volumes or operating in regulated industries should verify that CoinsPaid's compliance infrastructure meets their jurisdictional requirements. The OTC desk component introduces additional regulatory considerations for large transactions—confirm how these are handled in your operating regions.

Pricing and fees to confirm: Confirm processing fees (typically volume-tiered), OTC conversion spread for large transactions, fiat settlement/withdrawal fees, and how the platform structures pricing for the combined gateway and liquidity services.

Key limitation: Combined payment processing and OTC services create complexity that benefits high-volume merchants but introduces unnecessary overhead for businesses processing smaller transaction values.

CoinRemitter

Best for: Developer-focused businesses seeking straightforward API implementation with non-custodial settlement and minimal platform overhead.

Custody & settlement: CoinRemitter operates as a non-custodial gateway where customer payments flow directly to merchant-controlled wallet addresses on supported blockchain networks (Bitcoin, Ethereum, Tether, USD Coin, and additional assets). No fiat settlement option exists—merchants receive cryptocurrency only. The platform provides a lightweight layer for transaction tracking and notification without taking custody, keeping the merchant in full control of private keys and settlement timing.

Integration surface: REST API with webhook support for real-time transaction updates, hosted payment pages, invoice generation, and basic plugins for WooCommerce and custom platforms. The developer experience prioritizes API simplicity over extensive pre-built integrations. Sandbox environment allows testing without mainnet transactions. The platform focuses on core gateway functionality without extended features like recurring billing or complex subscription management.

Compliance & risk notes: As a non-custodial service, CoinRemitter does not perform conversion or custody, placing regulatory responsibility on merchants. The platform provides transaction data but merchants must implement their own KYC/KYB procedures if required by jurisdiction. No published information exists about the platform's AML screening or sanctions monitoring capabilities—merchants in regulated industries should request documentation. Verify that your business can legally accept direct crypto payments and that you have infrastructure for tax reporting on self-custodied receipts.

Pricing and fees to confirm: Verify processing fees (typically percentage-based on transaction value), whether the platform charges for API calls or webhook delivery above certain thresholds, how network fees (blockchain gas) are calculated and passed through, and the cost structure for using hosted payment pages versus API-only integration.

Key limitation: Minimal feature set beyond core payment processing makes CoinRemitter unsuitable for merchants requiring complex invoicing, subscription management, or extensive eCommerce platform integrations.

Key Features to Evaluate

Choosing one of the above? Trying to see which criteria set would let you find a gateway for your own needs? Regardless, let’s go through the key features that you should always consider when shopping for a crypto PSP.

First and foremost, it’s about testing the mechanics that decide whether you get elegant simplicity or a slow-moving operational mess. Use the checklist below to compare providers systematically and not fall for the SEO-friendly marketing pages.

Settlement Currency

It dictates what you can actually spend, where volatility lives, and how predictable accounting becomes.

What to verify:

- Crypto-settlement vs. fiat settlement vs. stablecoin settlement: Determine whether the gateway delivers your funds in the original cryptocurrency (Bitcoin, Ethereum), converts automatically to fiat (USD, EUR, GBP), or settles in stablecoins (Tether, USDC). Each option shifts where volatility risk lives—crypto settlement leaves it entirely with you, fiat settlement transfers it to the provider during conversion, and stablecoin settlement minimizes it through pegged assets.

- Manual conversion vs. auto-conversion: Check if the gateway requires you to convert manually or runs automated conversion upon payment confirmation. Auto-conversion reduces exposure windows but may lock you into the provider's exchange rate and timing.

- Rate-setting modes: Clarify when the conversion rate locks—spot at authorization (when the customer initiates payment), spot at confirmation (after blockchain validation), or within a locked quote window (a fixed rate valid for a set duration, typically 5-15 minutes). Locked quote windows protect both parties from slippage but require faster customer action.

- Supports real-time crypto-to-fiat conversion with transparent spread disclosure: Verify that the gateway publishes its conversion spread separately from processing fees, so you can calculate true settlement value and eliminate volatility where needed.

- Offers configurable confirmation thresholds before marking transactions as paid: Higher confirmation counts reduce double-spend risk but delay settlement finality, impacting your cash flow.

If predictable revenue recognition is the goal, fiat settlement with instant conversion is typically the cleanest. However, instant conversion can widen spreads during volatility, so request historical spread behavior during evaluation.

Supported Assets

This sounds simple until you run into network mismatches, memo/tag requirements, and inconsistent finality across chains.

What to verify:

- On-chain vs. internal ledger settlement: Determine if payments settle directly on public blockchains or through the provider's internal accounting system. On-chain settlement offers transparency and irreversibility; ledger-based systems may enable faster transactions but introduce custodial risk.

- Token + network pairing clarity: Confirm that the gateway specifies both the token (e.g., USDT) and the network (Ethereum, Polygon, Solana). Wrong-network deposits are one of the fastest ways to create support tickets and unrecoverable funds.

- Confirmation reliability across assets: Ask how the gateway calibrates confirmation thresholds per asset and whether you can tune them to your risk tolerance.

- Memo/tag support for assets requiring it: Coins like XRP and certain stablecoins require destination tags or memos. Missing tags can break attribution even if funds arrive.

Integration

Technical quality separates “accepting crypto” (air quotes included) from having a state-of-the-art payment system that won’t break during traffic spikes.

What to verify:

- Integration modes offered: API access, hosted checkout pages, plugins (WooCommerce, Shopify, Magento).

- API surface area completeness: Invoice creation, status checks, refunds, customer records, and transaction history.

- Webhook completeness and reliability: Events for invoice created, payment initiated, payment confirmed, payment failed, refund issued.

- Idempotency key support: Prevent duplicates during retries.

- Webhook signature verification mechanism: Authenticate event payloads.

- Sandbox environment availability with test funds: Simulate full flows without risking production logs.

- SDK maturity and language coverage: Reduce build time and maintenance burden.

- Documentation quality signals: Runnable examples, Postman collections, changelog transparency, public status page.

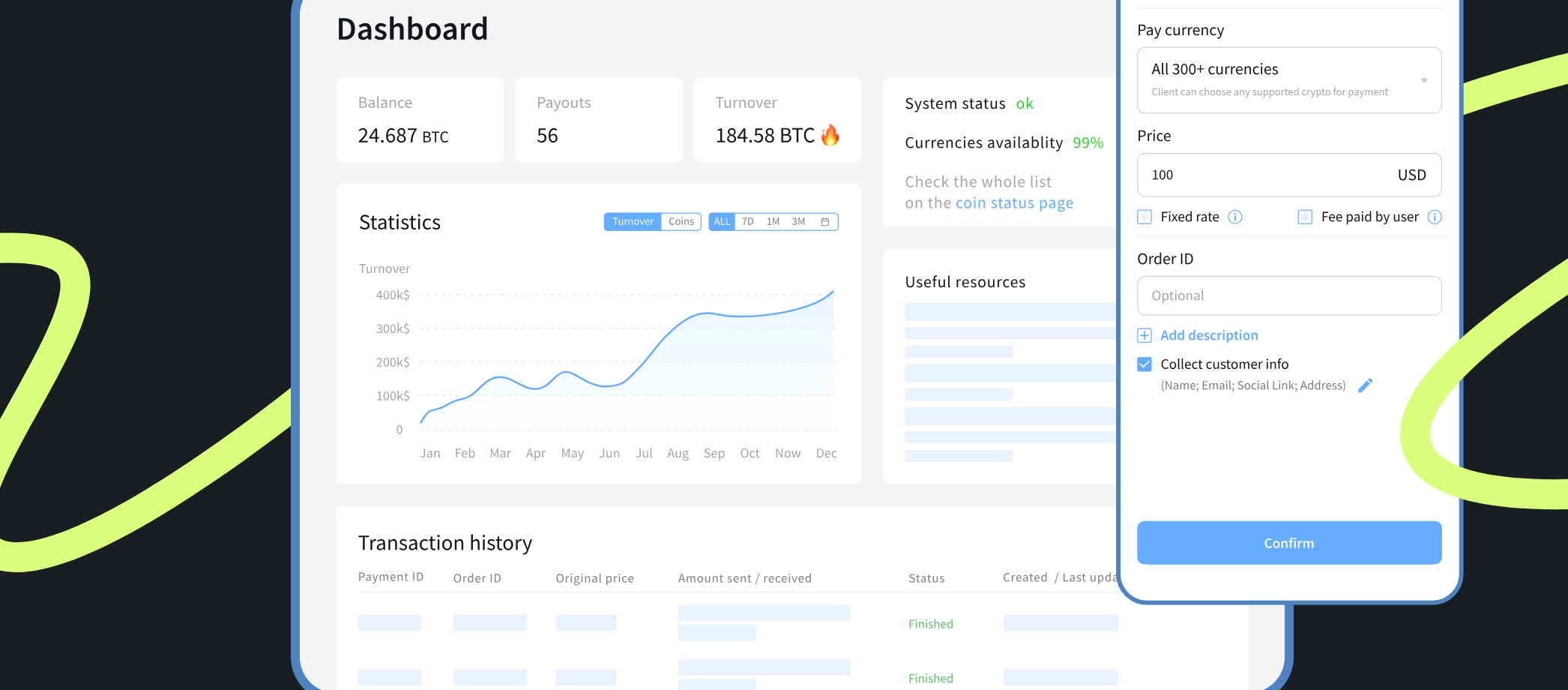

Fees

And how can we forget about costs? They’re a stack rather than a line: gateway fee, network fees, conversion spread, withdrawal fees, and edge-case costs.

What to verify:

- Gateway/processing percentage: 0.5% to 1.5% of transaction value is the usual.

- Network fees (blockchain transaction costs): Passed to customers, absorbed by you, or split.

- Conversion spread: Applied when settling in fiat or stablecoins.

- Withdrawal fees: Bank or wallet withdrawals.

- Chargeback/dispute handling fees: Some providers charge administrative fees even without on-chain reversals.

- Refunds processing fees: Who pays the network fee for returning funds?

- Minimum payout thresholds: Minimum balances before release.

A $100 sale processed at 1% gateway fee, 0.75% conversion spread, $3 network fee, and $15 withdrawal fee is $19.50 in total cost—nearly 20% of gross revenue. Fee transparency is not optional.

Compliance

Adhering to regulations is especially tricky due to changing shape depending on custody, conversion, and jurisdiction.

What to verify:

- KYB (Know Your Business) onboarding requirements

- Transaction monitoring and sanctions screening: OFAC, EU, UN lists.

- Licensing posture by region: Confirm coverage for your corridors.

- Record retention and audit readiness: Typically 5–7 years.

- Compliance obligation shifts between custodial vs. non-custodial flows

PCI-DSS is irrelevant for pure crypto flows but becomes relevant if the provider also processes cards or stores payment details.

Security

Security needs concrete controls, not marketing slogans.

What to verify:

- Key custody model: Custodial vs non-custodial.

- Multi-sig support for high-value accounts

- Role-based access control (RBAC) and team permissions

- API key scopes and expiration policies

- IP allowlisting for API access

- Webhook signature verification enforced

- Incident history transparency

- Operational safeguards: Manual withdrawal approvals, velocity limits, 2FA enforcement.

Payouts

Withdrawing your revenue decides cash flow speed and treasury flexibility.

What to verify:

- Payout methods supported: On-chain payouts, SEPA, UK Faster Payments, ACH, wire.

- Payout scheduling options: Fixed, on-demand, threshold-based.

- Batch payout support

- Supported payout currencies

- Payout cutoff times

- Reconciliation export formats: Link payout batches to transactions.

Refunds

Refunds are not simple reversals and require clear, tested procedures.

What to verify:

- Full vs. partial refund support

- Same-asset vs. different-asset refunds

- Network fee responsibility

- Refund address collection and validation

- Refunds when customer paid on wrong network

- Accounting trail requirements: Refunds linked to original invoice/transaction IDs.

Chargebacks

No on-chain chargebacks does not mean no disputes. It means you need better pre-fulfillment controls.

What to verify:

- Confirmation policy enforcement

- Fraud screening integration

- Proof-of-payment artifact generation: tx hashes, block explorer links

- Invoice expiry policies

- Under/overpayment handling workflows

- Customer support workflows for disputes

Crypto Payment Processors and Use-Case Fit

A gateway can be “good” overall but still wrong for your workflow. Before you shortlist, match requirements to capabilities.

E-commerce and Retail

Primary objective: Accept cryptocurrency payments at checkout with minimal customer friction while maintaining full order-to-ledger reconciliation for accounting.

Non-negotiable requirements:

- Checkout page UX and conversion impact: Hosted checkout or plugin support that mirrors fiat payment flows; a custom payment button can be useful for optimized storefront placement. Customers should see familiar cart-to-payment handoffs; unexpected wallet redirects increase abandonment.

- Real-time transaction updates via webhook: Order management systems need instant transaction status callbacks (pending, confirmed, failed) to trigger fulfillment or restock logic.

- Refund workflow including partial refunds and restocking: The gateway must handle partial crypto refunds and tie them to original transaction IDs for accounting reconciliation. Returns represent 8–15% of retail volume.

- Reconciliation outputs for accounting: CSV or API exports that map cryptocurrency transaction hashes to order IDs, timestamps, amounts (both crypto and fiat equivalent at settlement), and fees.

Nice-to-haves:

- Multi-currency pricing display (show prices in customer's local fiat while accepting crypto)

- Checkout abandonment recovery via payment reminders

- Integration with inventory management platforms for real-time stock syncing

Best fit if: You process over 100 orders per month, handle frequent returns, and need tight integration with existing e-commerce platforms like Shopify or WooCommerce.

Avoid if: Your order volume is under 50 per month or you lack technical resources to manage webhook infrastructure and reconciliation workflows.

Global Enterprise and Stablecoins

Primary objective: Facilitate cross-border treasury operations and stablecoin settlement with enterprise-grade controls, audit trails, and fiat payout rails.

Non-negotiable requirements:

- Stablecoin settlement vs fiat settlement: Determine whether you need to hold stablecoins (USDT, USDC) on-balance-sheet or auto-convert to fiat.

- Geo coverage and supported country constraints: Verify that the gateway supports both inbound payments and outbound payouts.

- Bank-transfer payout options (SEPA, UK Faster Payments, SWIFT): Without direct bank payouts, you're forced to use third-party exchanges, adding settlement risk and delays.

- Role-based permissions and audit trail for finance teams: Multi-user dashboards with role restrictions and immutable transaction logs.

Nice-to-haves:

- FX hedging tools to lock exchange rates before settlement

- API access for programmatic treasury management

- White-glove onboarding with dedicated account managers

Best fit if: You handle cross-border payments exceeding $500,000 per month, require stablecoin settlement, and operate in multiple regulatory jurisdictions with strict audit requirements.

Avoid if: Your transaction volumes are under $100,000 per month or you lack internal processes to manage stablecoin accounting and multi-user approval workflows.

High-Volume Altcoin Payments

Primary objective: Accept payments across a broad spectrum of cryptocurrencies (50+ assets) while managing conversion complexity and liquidity exposure for long-tail coins.

High-volume here means high order count (500+ transactions per month) or supporting many assets (30+ cryptocurrencies). Either way, you’re dealing with diverse block times, confirmation rules, and slippage.

Non-negotiable requirements:

- Supported cryptocurrency breadth and network selection: Verify not just coin count but chain diversity.

- Transaction tracking at scale: Each blockchain has different block times and confirmation requirements.

- Confirmation policies before fulfillment: Define thresholds per asset.

- Auto-conversion settings and liquidity management: Decide per asset whether to hold, auto-convert to stablecoin, or auto-convert to fiat.

Nice-to-haves:

- Conversion rate locks to protect against slippage during settlement

- Real-time blockchain monitoring dashboards with per-coin confirmation status

- Automated alerts for stuck or low-fee transactions

Best fit if: You serve niche communities requiring specific altcoin acceptance, process over 500 transactions per month across 30+ assets, and have treasury workflows to manage conversion slippage.

Avoid if: You process fewer than 200 transactions per month, lack tools to monitor blockchain confirmations, or cannot absorb liquidity risk on long-tail coins.

Subscriptions

Primary objective: Collect recurring cryptocurrency payments with minimal involuntary churn, accounting for wallet changes and variable exchange rates.

Recurring billing in crypto is different from fiat. Most gateways require customer-initiated payments each cycle rather than stored authorizations—simpler in one sense, more fragile in another.

Non-negotiable requirements:

- Variable exchange rate handling: A $50/month subscription priced in Bitcoin fluctuates daily.

- Invoice generation and payment reminders: Each billing cycle generates a new invoice with a unique crypto payment address.

- Recurring payment mechanics: Clarify what "recurring" means.

- Payment failure detection and dunning workflows: Without webhook events for "invoice expired," you’ll build it yourself.

Nice-to-haves:

- Flexible billing intervals (weekly, monthly, annual) with prorated adjustments

- Integration with subscription management platforms (Chargebee, Recurly) via API

- Grace periods for late payments before service suspension

Best fit if: You have an established subscriber base willing to manage manual payments each cycle, can tolerate 5–10% higher involuntary churn than fiat, and process over 200 renewals per month.

Avoid if: Your pricing model requires seamless auto-renewal without customer action, you lack dunning infrastructure, or your margins can't absorb exchange rate volatility.

Digital Goods

Primary objective: Deliver instant digital fulfillment (licenses, downloads, in-game items) while mitigating fraud and irreversible payment risk.

Digital goods demand speed, but crypto’s irreversibility means you must tune confirmation policy like a risk dial.

Non-negotiable requirements:

- Confirmation policy tradeoffs (speed vs risk)

- Receipt and proof-of-payment handling

- Customer support artifacts (transaction ID, timestamps)

- Fraud/scam mitigation via delayed delivery thresholds

Common failure modes:

- Irreversible payments and dispute escalation

- Delayed delivery breaks UX

- No delivery confirmation proof

- Fraud via zero-confirmation exploitation

Best fit if: You sell digital goods under $100, can tolerate occasional fraud losses as a cost of speed, and process over 500 transactions per month where instant delivery drives conversion.

Avoid if: You sell high-value software or licenses where fraud exposure exceeds 2%, lack infrastructure to track delivery confirmations, or cannot absorb irreversible payment disputes.

Marketplaces

Primary objective: Accept cryptocurrency payments from buyers while splitting fees and routing payouts to multiple sellers, maintaining clean sub-ledgering and audit trails per seller.

Marketplaces separate receiving from paying out. That means splits, fee capture, sub-ledgers, and multi-party compliance.

Non-negotiable requirements:

- Split payments and fee capture model

- KYC/KYB responsibilities

- Payout batching via Payouts API or CSV

- Reconciliation per seller (sub-ledgering)

Nice-to-haves:

- Seller-facing dashboards for earnings and payouts

- Escrow features

- Multi-currency payout support

Best fit if: You operate a marketplace with over 50 active sellers, process more than 1,000 transactions per month, and have engineering resources to integrate Payouts API and maintain sub-ledgering.

Avoid if: You have fewer than 20 sellers, lack API integration capabilities, or cannot manage reconciliation complexity across multiple payout recipients.

Platform and Integration Options

| Integration Type | Implementation Effort | Checkout UX Control | PCI/SAQ Impact | Typical Buyer Channel | Best For | Main Risk |

|---|---|---|---|---|---|---|

| API | 2-4 weeks | Full control | Low (crypto-only flow) | Web checkout, mobile app | Enterprise, marketplaces | Webhook failures, reconciliation gaps |

| Hosted Checkout | 2-5 days | Limited (provider's UI) | Minimal (redirect) | Web checkout | SMBs, fast launches | Redirect drop-off, conversion tracking loss |

| Plugins | 1-2 hours | Moderate (theme-dependent) | Minimal (managed by plugin) | E-commerce storefronts | WooCommerce, Shopify merchants | Breaking updates, theme conflicts |

| Invoicing | 1-3 days | Full (email/manual) | None (off-session) | B2B sales, net terms | High-AOV, enterprise | Partial payment confusion, rate lock disputes |

| Payment Links | Minutes | None (fixed template) | None (one-time use) | Social, DM, support tickets | Creators, support teams | Link leakage, fraud via shared links |

API

A real API integration is not one endpoint but a workflow spanning engineering, finance, and risk controls.

API Integration Checklist:

- Create quote/payment intent – Reserves an exchange rate and wallet address before the customer sees payment details.

- Address generation and chain selection – Dynamically generates deposit addresses per order and lets customers choose BTC, ETH, or other chains.

- Exchange-rate lock/expiry behavior – Locks the fiat-to-crypto rate for 10-30 minutes and expires the payment window.

- Webhook signature verification – Validates that incoming event payloads are signed by the gateway's private key.

- Idempotency keys for retries – Attaches unique identifiers to API calls so network timeouts don't duplicate payments.

- Confirmation policy (0/1/N conf) and reorg handling – Defines how many blockchain confirmations trigger "paid" status and monitors for chain reorganizations.

- Reconciliation identifiers (invoice_id/order_id mapping) – Embeds your internal order ID in payment metadata so transaction reports map directly to your ERP.

- Sandbox environment/testing expectations – Provides a testnet or mock API for rehearsing the full payment lifecycle without real funds.

CoinGate's scale—processing billions in transaction volume—demonstrates why mature API integrations prioritize webhook reliability and sandbox testing; providers serving high-volume merchants cannot afford event delivery failures that break order fulfillment pipelines.

NOWPayments' support for dozens of blockchains highlights why robust API implementations must handle chain/asset selection dynamically and track transaction states across vastly different confirmation speeds and finality models.

Hosted Checkout

This type of PSP redirects customers to the gateway's payment page, then returns them to your site after completion. Three details decide whether it feels seamless or breaks conversion: redirect vs embedded iframe, passing metadata for reconciliation, return URL + server-side verification.

When Hosted Checkout is the wrong choice: Complex marketplaces requiring split settlement cannot route funds through a single hosted checkout session.

Plugins

Plugins turn API complexity into a settings screen, but updates and theme interactions can introduce fragile points.

Platform-Specific Integration Notes:

| Platform | Configuration Fields | Common Breakage Points | Quick Test Procedure |

|---|---|---|---|

| WooCommerce | API key, webhook URL, confirmation threshold (0-6 confirmations), sandbox toggle | Custom checkout blocks override plugin hooks; some themes inject JavaScript that hides payment instructions | Place test order → verify webhook hits your gateway Dashboard → confirm WooCommerce order status updates from "Pending" to "Processing" → check tx hash stored in order meta |

| Shopify | API key (read/write scopes), webhook URL, auto-fulfill toggle, supported currencies | Shopify's checkout.liquid cannot be edited on lower plans, breaking custom instruction displays; app conflicts when multiple payment apps use the same webhook endpoint | Create draft order → customer pays → confirm Shopify receives webhook → verify order tag includes blockchain network and tx hash → test storefront purchase end-to-end |

| Magento | API key, secret key, webhook URL, IPN fallback URL, multi-store currency mapping | Magento's event-observer pattern means plugin updates can miss new checkout events; custom payment method renderers in themes override plugin templates | Configure plugin → place order as guest → verify Magento invoice creation → confirm tx hash appears in order comments → test logged-in customer flow separately |

Invoicing

Invoices trade checkout speed for clean B2B workflows and audit-ready trails—perfect when buyers demand invoice numbers and approvals.

Integration with reconciliation/reporting: Invoice generation creates a receivable in your accounting system. When the invoice webhook fires payment_confirmed, your system must credit Accounts Receivable and debit your crypto settlement account, using the stored exchange rate to maintain consistent fiat valuations.

Invoices outperform checkout flows for net terms, high AOV, off-platform sales, and B2B payment requirements where buyers need invoice numbers and approver-friendly audit trails

Payment Links

Finally, links are fast, flexible, and dangerously easy to misuse without controls.

Use-Case Segmentation:

| Use Case | Link Controls Required |

|---|---|

| Social/DM sales | Link expiry (24-72 hours), amount locking, single-use enforcement, Instagram/Telegram preview compatibility |

| Customer support payments | Multi-use links, internal notes field, email receipt trigger, support agent permissions audit |

| Deposits | Customer-entered amount, multi-use for single customer, no expiry (or very long), webhook tied to customer account ID |

| Off-session payments | Single-use, amount locked, 30-60 min expiry, SMS/email delivery with one-time code |

Fraud/Scam Guardrails:

- Restrict who can generate links

- Require internal notes/customer reference

- Rate-limit link creation

- Dashboard shows link-to-settlement mapping

Risks and Key Considerations

Crypto payment acceptance introduces risks that look different from card and bank processing. The good news is that most of them are controllable—if you design for them up front.

Volatility and Settlement Risk

Volatility risk is mostly time risk: the gap between price display, customer broadcast, blockchain confirmation, and conversion/settlement. Keep your team aligned on three layers: 1) pricing currency (what you display), 2) payment currency (what the customer sends), and 3) settlement currency (what you receive).

Your controls for settlements are rate lock window, confirmation policy, and conversion trigger. Ask every gateway:

- What is the maximum rate lock duration you support, and does it vary by payment asset or invoice size?

- Do you offer zero-confirmation acceptance for stablecoins or low-value transactions, and what fraud liability does that shift to us?

- Is conversion triggered per-transaction in real time, or do you batch conversions at fixed intervals (hourly, daily)?

- If I choose deferred settlement, can I override the conversion trigger manually or set conditional rules (e.g., convert only if BTC drops below $X)?

Custody and Counterparty Risk

Custody risk shows up at three failure points:

- Custodial gateway balance risk (funds pooled in gateway-controlled wallets)

- Custodial exchange/treasury conversion risk (third-party exchange outages or seizures)

- Banking partner payout risk (the final-mile fiat payout stalls)

Request a due-diligence packet with: (1) contractual fund segregation language, (2) SOC 2 Type II or ISO 27001 reports if available, (3) incident history, (4) withdrawal controls (multi-signature requirements, cold wallet thresholds, manual review triggers), and (5) payout SLAs and escalation paths.

Custody choices define your operational blast radius. Choose accordingly.

Fraud, Scams, and Dispute Limitations

No chargebacks can be great—until it forces you to be your own chargeback system. Screen before fulfillment, not after. Build a refund SOP for wrong-chain deposits, under/overpayments, duplicate payments, and phishing scenarios.

Before you process a “refund” (which is just “sending funds back yourself”): verify deposit on-chain, check its settlement status, assess the return path, calculate net amount, and only then document and execute. It’s a lot more busywork but some may find this less prone to fat-thumb mistakes.

Compliance, Tax, and Reporting Exposure

Compliance responsibility fragments across merchant and provider. A RACI mapping is the only sane way to define ownership. To stay audit-ready, your exports should include at least ten fields per transaction (and realistically 15–20 for complex flows).

Treasury policy must be executable from day one: approval thresholds, separation of duties, multi-signature or RBAC, and daily reconciliation. Monitoring and incident response need named owners and triggers—no “someone should watch this” policies.

Compliance and Legality

Crypto payment gateways operate under strict regulations designed to prevent financial crimes and protect customer data. While the gateway handles certain checks and controls, the merchant retains ultimate responsibility for regulatory adherence, recordkeeping, and reporting in most jurisdictions. Note: This is not legal or tax advice; consult qualified professionals for your specific situation.

Licensing

A "licensed" or "regulated" crypto payment gateway can mean vastly different things depending on the entity structure and operating footprint.

When conducting vendor due diligence, ask for the legal entity name operating the service, the specific registration or license IDs, and which entity serves which region. Request documentation showing the license covers the services you intend to use: payment acceptance, settlement, custody if applicable, and fiat conversion.

KYC and KYB

Know Your Business (KYB) processes determine what information a gateway collects from you as a merchant before enabling payment acceptance and payouts. Verify the gateway's KYB data requirements align with your onboarding timeline and document availability.

From an implementation reality perspective, KYB directly affects your time-to-live and conversion. Plus, certain business models face additional scrutiny.

AML and Sanctions Screening

An Anti-Money Laundering (AML) program touches your business in several ways, even when the gateway performs transaction monitoring.

Many gateways allow you to configure controls that reduce laundering risk and align with your business model. Ask what transaction monitoring tools are in place and what actions you must take when alerts arise.

Related to it, sanctions screening checks wallet addresses, counterparties, geolocation or IP data, and names in invoices or fiat payment rails against government-issued sanctions lists.

Operationally, a sanctions hit triggers a defined workflow. Review it and confirm you can respond to compliance holds within required timelines.

Data Privacy

Crypto payment gateways process multiple categories of data, each with different retention purposes. Blockchain privacy introduces a unique reality: on-chain data is public and immutable.

Review the DPA, data residency options, sub-processor list, and breach notification procedures before signing an agreement with a provider.

Conclusion

In practice, many merchants shortlist additional providers beyond the ones profiled above—such as Cryptomus, CoinsBank, SpicePay, and CoinPayments—then evaluate them against the same rubric for custody, reporting, and operational controls; in blended checkouts, some also confirm whether the broader payment stack supports Apple Pay, Google Pay, Visa, and Mastercard alongside crypto, and whether settlement is routed to a multi-currency account where applicable.

Frequently Asked Questions

What fees does a crypto gateway usually charge?

Crypto gateways layer multiple fees: a processing fee (percentage of transaction value, typically 0.5–2%), blockchain network fees, FX spread, and payout fees.

Who pays the network fee—merchant or customer?

Network fee allocation depends on your invoice configuration.

Are there hidden costs beyond headline %?

Beyond the advertised processing rate, watch for minimum monthly fees, per-transaction minimums, auto-conversion fees distinct from FX spread, plugin or integration licensing costs, and refund handling charges.

Is accepting crypto legal for a business?

Accepting cryptocurrency is generally legal in most jurisdictions but subject to financial regulations, anti-money laundering (AML) rules, and tax obligations.

What compliance steps do gateways require?

Reputable gateways perform Know Your Business (KYB) checks during onboarding.

What records should we keep for audits/tax?

Maintain a complete trail: invoice details, transaction hash, cryptocurrency amount received, fiat value at time of sale, settlement receipt showing conversion and payout, and customer identification where legally required.

Can we receive payouts in USD/EUR instead of crypto?

Most gateways offer auto-conversion.

How does crypto-to-fiat conversion pricing work?

Gateways source exchange rates from aggregated market data or partner exchanges, then apply a spread.

What payout rails are supported?

Settlement methods vary by gateway and region.

What's the practical difference between custodial and non-custodial for a business?

Custodial gateways hold your private keys; non-custodial solutions give you the keys.

Can crypto payments be refunded?

Yes, but unlike credit card reversals, crypto refunds require sending a new outbound transaction.

Is refund in crypto or fiat value?

Policy choice depends on volatility tolerance and customer expectations.

How do refunds work if the customer used the wrong network?

Wrong-network deposits are usually unrecoverable.

When is a payment considered complete?

A payment is complete once the blockchain network confirms the transaction a sufficient number of times.

How long until funds are spendable/withdrawable?

Beyond blockchain finality, gateways may impose internal risk holds.

What makes settlement slow?

Congestion on popular networks delays confirmations.

What does 'supports a coin' actually mean?

Coin support requires both the asset and the specific network it runs on.

How do we avoid wrong-network deposits?

Wrong-network errors are the leading cause of lost customer funds and support tickets. Use double-labeling to communicate both asset and chain to the customer.

Does supporting many chains increase risk?

Broad chain support expands customer choice but multiplies operational complexity.