Is Staking Crypto Worth It?

Key Takeaways

- 🕰️ Time horizon decides the trade. If you’ll hold 6–24 months, staking usually works; if you need the funds within 30 days, avoid it; if you might need cash within weeks, stake only what you can leave locked without stress.

- 🕰️ Liquidity constraints are a stack, not one rule. Separate lockup (can’t move tokens while staked), unbonding/unstaking (days to weeks after you request exit), and withdrawal queues (delays during mass exits). Many networks stop rewards during unbonding, so the “exit” period can be dead time.

- 🕰️ Custody is the hidden risk switch. Self-custodial/native staking lets you exit unilaterally (protocol rules only). Exchange/custodial staking turns your position into a platform IOU, adding insolvency, withdrawal freezes, policy changes, and regulatory holds on top of protocol risk.

Disclaimer: Nothing on this page constitutes financial advice or tax advice. Staking terms — including APY, lockup periods, slashing conditions, and platform fees — vary significantly by network and by the platform or validator you choose. The examples used throughout this guide are illustrative and reflect conditions that can change at any time. Always verify current rates, lockup terms, fee structures, and slashing policies on the specific platform or network you intend to use before committing funds.

Crypto staking is often advertised as a passive income method; even if you are well aware of the actual purpose and goals of staking, you might still want to ask: is staking worth it?

This guide evaluates these three dimensions—net yield, liquidity/lockup & exit time, and price risk relative to reward—so you can estimate whether your expected investment return is realistic.

How We Research and Verify: The analysis in this guide is based on a review of proof-of-stake network documentation, exchange and staking pool fee schedules, available as of June 2026. Before acting on any recommendation or example, you should independently verify the current APY, lockup duration, validator performance, and fee structure on the exact platform or network you plan to use. Staking terms are not static, and relying on outdated information can result in unexpected costs or missed opportunities.

What Is Crypto Staking?

Definitions

What does staking mean? In one sentence: Staking includes committing tokens to a blockchain network’s security mechanism in exchange for the right to validate transactions and earn rewards.

In more detail, crypto staking locks tokens to secure a proof-of-stake network by making holders participate in transaction validation; it does not require mining hardware and earns usually protocol-issued rewards. Unlike lending interest, which derives from borrower demand, staking rewards come from network issuance and sometimes transaction fees paid by other network users. Unlike proof-of-work mining, staking is comparatively energy efficient because it relies on economic commitment—validators risk their own capital rather than electricity.

How does staking contribute to security? Network and economic security are accomplished by requiring validators to lock collateral that can be destroyed if they behave dishonestly, and by granting staking participants the authority to propose and attest to new blocks, keeping the network running. Additionally, it:

- Grants participation or governance power in networks where voting weight correlates with staked amount

- Distributes rewards as new token issuance, transaction fees, or both, depending on chain architecture

It should also be mentioned that staking does not provide guaranteed returns, is not risk-free and more often than not illiquid. Those are not incidental drawbacks but intentional design choices.

Proof of Stake (PoS)

Proof-of-stake distributed networks select validators through weighted randomness: the more tokens a participant stakes, the higher their probability of selection to propose the next block, though exact algorithms vary. Once chosen, validators propose new blocks containing transaction batches, while other validators attest to those proposals’ validity thus ensuring the accuracy of transaction ordering and state transitions.

Rewards that compensate validators’ work originate from two sources depending on chain design: newly minted tokens, which contribute to asset’s supply inflation, and transaction fees paid by users, which some networks burn partially while distributing the remainder to validators (e.g. Ethereum).

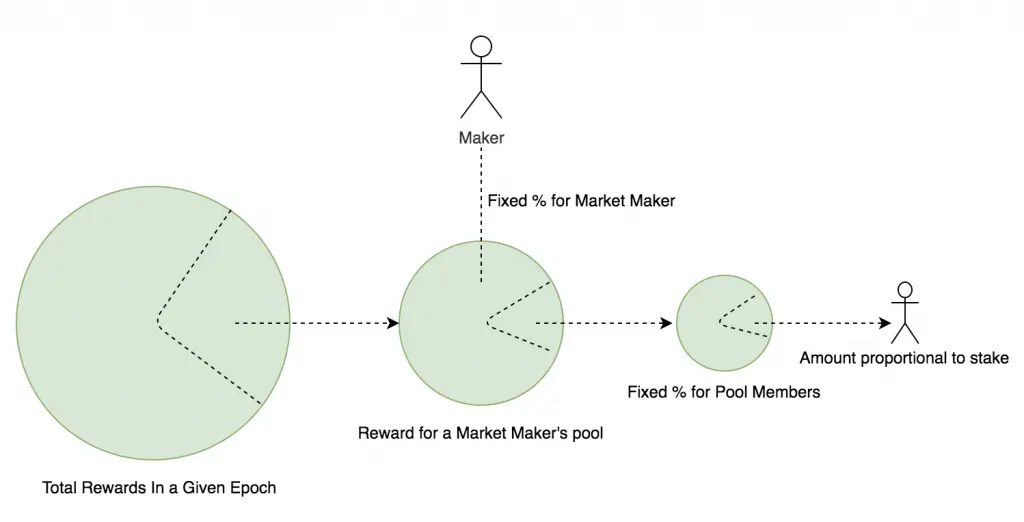

In some implementations, delegation operates as a trust relationship without custody transfer: token holders assign their stake’s validation weight to a professional validator while retaining ownership in their own wallet. The validator operates node infrastructure—maintaining uptime, signing attestations, proposing blocks—and typically charges a commission between 5% and 15% of earned rewards. This structure allows participants who lack technical expertise or capital to still earn staking yield. Delegators share both rewards and risks: if their chosen validator suffers slashing penalties for downtime or malicious behavior, delegated stake absorbs proportional losses.

Validators

Finally, validators bear three core responsibilities: maintaining continuous node uptime to participate in each consensus round, accurately validating transaction data and state transitions within proposed blocks, and signing attestations or votes according to protocol timing requirements. For example, in Ethereum, in addition to adding block by block, validators also vote on the chain state in general, which are two separate duties.

Failure modes trigger penalties of varying severity. Minor infractions like missing a single attestation typically result in small reward forfeiture. Prolonged downtime or critical violations—proposing conflicting blocks, attesting to invalid state—trigger slashing, where a percentage of the validator’s staked tokens is permanently destroyed. Ethereum’s slashing rules, for example, can destroy up to 100% of a validator’s 32 ETH stake for the most severe infractions.

Validator operation imposes certain requirements depending on the network. Ethereum requires exactly 32 ETH per validator instance; other networks like Solana set lower barriers around 1 SOL but recommend higher amounts for competitive selection. Additionally, hardware and technical competency are basically implicit requirements to run a validator node.

Some networks facilitate pooled or delegated participation as an alternative: users combine funds to meet minimum thresholds collectively or assign stake to established operators, reducing individual capital requirements in exchange for commission fees and trust in third-party competence.

How Crypto Staking Works

Process

The end-to-end staking sequence involves both system-level protocol actions and user-facing decisions, with a clear separation between what the delegator initiates and what the validator executes:

- User deposits stake: The delegator transfers tokens from their wallet to a staking smart contract or validator’s designated address, signaling intent to participate in network consensus.

- Protocol registers stake: The blockchain’s consensus client records the delegated amount and associates it with the selected validator’s public key, increasing that validator’s voting power proportionally.

- Validator enters active set: Once the validator meets the minimum stake threshold, the protocol promotes it into the active validator set during the next epoch or slot transition.

- Block proposal and attestation: Active validators propose new blocks when selected by the protocol’s pseudorandom algorithm and attest to the validity of proposed blocks from other validators.

- Protocol calculates rewards: At the end of each epoch or slot cycle, the network measures validator uptime, correctness, and participation, then allocates base rewards proportional to stake weight.

- Validator deducts commission: Before distributing rewards to delegators, the validator subtracts its pre-disclosed commission percentage as operational compensation.

- Rewards credited to delegators: Remaining rewards are distributed to all delegators in proportion to their individual stake within that validator’s total pool.

- Unstaking request initiated: When a delegator wants to exit, they submit an unstaking transaction, triggering the protocol’s unbonding or cooldown period before tokens become liquid again.

Ethereum and Cosmos ecosystems refer to reward calculation windows as epochs, typically spanning hundreds of blocks and lasting minutes to hours, while Solana and Avalanche use slots, representing individual block production opportunities measured in seconds. Despite naming differences, proof-of-stake chains implement discrete intervals for tallying validator performance and distributing rewards.

Asset Custody

Self-custodial staking and custodial staking represent fundamentally different ownership models, distinguished by who controls private keys, who can impose withdrawal restrictions, and what the staker actually holds during the staking period. It boils down to a practical question: can you exit unilaterally, or are you asking permission?

In self-custodial staking and wallet delegation, the staker retains full control of their private keys throughout the staking lifecycle. When you delegate from a digital wallet like MetaMask, Ledger, or Phantom, the staking transaction writes your delegation intent directly to the blockchain, and the protocol itself enforces reward accrual and unstaking rules—no intermediary holds your tokens. What you own is an on-chain staked position: your tokens remain registered to your public address, visible on any block explorer, and recoverable only with your private key.

Custodial staking (exchange/platform) involves a centralized cryptocurrency exchange or staking provider, relinquishing private key control in exchange for simplified user experience. The exchange aggregates customer deposits, operates validators on your behalf, and credits rewards to your account balance as an internal ledger entry, not an on-chain transaction. What you own in this model is an IOU or claim: a contractual right to withdraw staked tokens, subject to the platform’s terms of service, regulatory compliance obligations, and operational solvency. The exchange can impose withdrawal restrictions beyond protocol rules, including account-level holds, jurisdiction-based freezes, or platform-wide liquidity constraints during stress events.

In other words, a wallet provider (e.g., Trust Wallet, Exodus) facilitates your interaction with the blockchain but never holds your keys, while a digital asset exchange (e.g., Coinbase, Kraken) takes full custody and operates as your counterparty.

Reward Distribution

If you have ever wondered why an advertised APY doesn’t match what you actually received, the explanation usually lies in protocol-defined payout mechanics: timing, net yield, and variance.

(1) Protocol schedule determines reward timing: In this case, rewards are not credited continuously or immediately after validation work. Instead, the blockchain allocates rewards on a fixed schedule aligned with its consensus interval—epoch, block, or daily snapshots on centralized platforms mirroring protocol behavior. This means your reward balance updates in discrete increments, not real-time accrual, and any dashboard showing a “live” reward counter is extrapolating from the last settled epoch, not reflecting finalized protocol state.

(2) Validator commission deducted before delegation: When the protocol calculates rewards for a validator’s total stake pool, it credits the full base reward amount to the validator’s account first. The validator then retains its commission percentage and distributes the remainder proportionally among delegators. If you delegated to a validator charging 10% commission, you never see that 10% in your balance—it is deducted upstream, before your share is calculated. Advertised APY figures on dashboards and aggregators typically reflect gross protocol rewards before commission, requiring manual adjustment to estimate your net return; many wallets now include a built-in staking calculator to estimate net outcomes.

(3) Realized yield varies with performance and network conditions: Reward rates fluctuate based on validator uptime (missed attestations reduce payout), total network stake (higher participation dilutes individual share), and transaction fee activity (priority fees on Ethereum can boost returns but are unpredictable). A validator experiencing downtime earns reduced rewards or none during offline epochs, directly impacting delegator payouts. Network-wide stake increases dilute the per-token reward rate because the fixed issuance pool is divided among more participants. During periods of high on-chain activity, validators earn additional revenue from transaction priority fees, which may or may not be shared with delegators depending on the validator’s fee structure.

Lockups and Unstaking

Staking imposes two separate liquidity constraints that users frequently conflate: lockup refers to the inability to move or trade your tokens while they remain staked, and unbonding/unstaking period refers to the delay between requesting exit and receiving liquid tokens. Some protocols enforce both, others mainly enforce exit delays, and liquid staking protocols attempt to sidestep the problem by issuing a tradable derivative.

When you stake tokens, they are committed to the protocol’s staking contract or validator assignment and sometimes cannot be spent, transferred, or traded until you initiate unstaking. Your tokens remain locked as long as they carry a “staked” designation on-chain, which could be indefinite if you never request withdrawal. Ethereum staking operated under a strict lockup from the Merge (September 2022) until the Shanghai upgrade (April 2023), during which no withdrawal mechanism existed at all.

Once you submit an unstaking request, usually the protocol does not return your tokens immediately. Instead, it places them in an unbonding queue for a predefined cooldown window, during which the tokens remain locked and non-transferable but are no longer earning rewards. This delay exists as a security buffer: it prevents validators from rapidly exiting during network attacks or coordination failures, and it gives the protocol time to finalize any pending slashing penalties before releasing the stake.

Some staking systems, particularly liquid staking protocols, do not impose an upfront lockup—you receive a derivative token (e.g., stETH, rETH) representing your staked position, which you can trade or use as collateral immediately. However, redeeming that derivative for the underlying staked asset still triggers the protocol’s native unbonding period. The liquidity is synthetic: you can exit the position via secondary market sale, but canonical withdrawal from the staking contract remains subject to the same delays as direct staking.

Staking Methods Compared

When evaluating staking and weighing the risk against the reward, the method plays a big part in the thought process. You may find solo (native) staking to be not worth the capital risk but still see some benefit going for its alternative.

| Method | Who holds the keys (custody) | Typical setup effort | Fees/commission types | Key risks (non-overlapping) | Best for | Deal-breakers |

|---|---|---|---|---|---|---|

| Native Staking | User retains custody; keys never leave user's digital wallet | Medium to high; requires wallet setup, validator research, delegation transaction | Validator commission (typically 5–20% of earned rewards) | Validator underperformance, slashing events if validator misbehaves, unbonding delays | Users prioritizing self-custody and willing to research validators | Lack of technical comfort; inability to evaluate validator performance |

| Staking Pools | Varies by pool type; some pools custody keys (shared validator), others route delegation while user keeps keys | Low to medium; often simplified through web interfaces | Management fee (2–5% of rewards) or performance-based cuts | Smart contract bugs in pool infrastructure, liquidity mismatches in liquid staking derivatives | Users seeking lower minimums or simplified delegation without exchange counterparty risk | Need for instant unstaking; unwillingness to interact with pool smart contracts |

| Centralized Exchanges | Exchange holds custody; user has no private keys | Very low; sign up, deposit, enable staking via dashboard | Variable reward share set by exchange policy; often undisclosed or discretionary | Exchange insolvency, withdrawal freezes, policy changes, KYC/regulatory exposure | Beginners wanting maximum convenience and already holding assets on an exchange | Strong preference for self-custody; concern about exchange transparency or solvency |

| Running a Validator | Full custody with user; validator operator controls all keys | Very high; requires hardware procurement, network configuration, continuous monitoring | No third-party fees; operator keeps full rewards minus network inflation dilution | Slashing for downtime or protocol violations, operational complexity, capital lockup, security breach risk from key exposure | Technical users with capital, infrastructure, and operational discipline | Inability to maintain 24/7 uptime; lack of redundancy; discomfort with on-call responsibilities |

Native staking refers to delegating crypto directly to a validator node through your own digital wallet while retaining full custody of your private keys. No intermediary holds your tokens; you maintain control throughout the lock-up period, though unbonding (withdrawal) timelines vary by network and can range from days to weeks.

Staking pools aggregate capital from multiple users to meet minimum staking thresholds or simplify delegation logistics. However, “staking pool” is not a single product category; users participate through pooled delegation, liquid staking protocols, or shared validator models. Custody profile varies between all three: they are self-custodial, custodial and pool custody respectively.

- If you need: Full custody and transparency → Choose pooled delegation (on-chain delegation remains visible; you keep keys).

- If you need: Liquidity and flexibility to use staked assets elsewhere → Choose liquid staking (accept smart contract risk and derivative price tracking risk).

- If you need: Simplified access without technical setup → Choose shared validator (sacrifice individual control for lower entry barriers).

Staking pools typically charge a management fee ranging from 2% to 5% of earned rewards. This fee is deducted before rewards are distributed to participants, reducing your effective annual percentage yield (APY). Fee structures vary: some pools take a flat percentage of rewards, while others apply performance-based cuts only when rewards exceed a baseline threshold.

Centralized crypto exchanges offer staking products that prioritize convenience over custody and transparency. When you enable staking on an exchange, you are not delegating tokens on-chain in most cases; instead, the exchange credits your account with a yield product derived from its own staking operations or liquidity lending.

Running a validator node means operating the infrastructure that validates transactions and secures the proof-of-stake network. Validators earn rewards directly from the protocol without intermediaries, but they also assume full responsibility for uptime, security, and protocol compliance. This method is not delegation; it is active and direct participation in network consensus.

Staking Returns and Yield Drivers

Advertised rates tell only part of the story; the full picture emerges when you subtract inflation, account for commission layers, and acknowledge that rewards fluctuate epoch to epoch based on network conditions you cannot control. Real return is what remains after inflation eats into nominal gains, fees carve out their share, and variability introduces uncertainty into any single-period estimate.

APY

Annual Percentage Yield (APY) differs from Annual Percentage Rate (APR) in one critical assumption: compounding. APR treats rewards as static—you earn X% and never reinvest. APY assumes you compound those rewards back into the staking position at regular intervals, which increases the effective return over time. Platforms display projected APY based on this reinvestment assumption, but realized yield depends on whether you actually claim and restake rewards or let them sit idle in your wallet.

Not all advertised APY figures represent the same yield sources. Protocol base staking rewards—emissions distributed by the blockchain itself—form the foundation. In some proof-of-stake networks, particularly Ethereum post-merge, validators can capture additional revenue streams such as maximal extractable value (MEV) or priority fees paid by users seeking faster transaction inclusion.

Inflation

Real yield for staking equals nominal staking yield minus token inflation—do your rewards actually increase your economic share or merely keep pace with supply expansion? Consider a protocol offering 15% APY on staked tokens but issuing new tokens at 12% annual inflation. Your nominal yield is 15%, but if the entire token supply grows by 12% over the same period, your real yield—the increase in your proportional ownership of the network—is only 3%. If inflation exceeds your staking yield, you are losing ground in real terms despite accumulating more tokens, because the denominator in your ownership fraction is growing faster than your numerator.

Inflation likewise affects holders who do not stake through dilution: their percentage of total supply shrinks as new tokens are issued and distributed to stakers. Stakers, on the other hand, receive those newly minted tokens as rewards, which can partially or fully offset the dilution depending on their share of total staked supply.

Protocols with high issuance rates create an inflation sensitivity dynamic: staking participation becomes a defensive necessity rather than an optional yield strategy. When a network emits 20% new tokens annually, sitting idle means accepting a 20% dilution of your ownership stake. Staking simply to offset that dilution is not “earning” yield in the traditional sense; it is paying the cost of maintaining your proportional claim on the network.

Fees

Staking fees appear in several distinct forms, and each carves out a slice of your gross yield before you see the net return in your wallet. Validator commission is the percentage a validator node operator charges for running infrastructure and maintaining uptime. Pool or service fees apply when you stake through a third-party platform or liquid staking protocol and are typically taken from rewards. Exchange cuts emerge when you stake directly through a centralized exchange and may be discretionary or only partially disclosed. Network transaction fees for staking, unstaking, or claiming rewards can also erode net yield, particularly on networks where gas costs fluctuate; while these fees are typically paid in the network’s native token (not the staked asset), they still represent a real cost in dollar terms when you convert to calculate total return.

Some platforms advertise gross yield—what the protocol pays before any deductions—while quietly charging fees in the background. To identify these hidden costs, scan the platform’s documentation or settings page for terms like "validator commission," "service fee," "reward share," or "performance fee." If the platform displays a single APY number without a breakdown, assume it is gross and subtract estimated fees manually. Liquid staking protocols, which issue derivative tokens representing staked positions, often embed fees in the exchange rate between the derivative and the underlying asset rather than taking an explicit percentage cut, making the fee structure less transparent but no less real.

Reward Variability

Staking rewards fluctuate day to day and epoch to epoch due to three primary drivers, each operating independently but compounding in effect. Validator uptime and performance is the first one, which we have already covered. Network participation rate—the percentage of total token supply actively staked—affects your individual yield because most protocols distribute a fixed or algorithmically determined reward pool across all active stakers; when participation increases, the same reward pool is divided among more recipients, reducing per-staker yield, and when participation drops, yields rise as rewards concentrate among fewer participants. Protocol-level reward schedule changes represent the third driver: some networks reduce issuance over time (diminishing inflation), others adjust rewards based on security budgets or governance votes, and a few tie emission rates to on-chain activity levels, meaning your yield can shift not due to your actions or your validator’s performance but due to macroeconomic protocol design changes you have no control over.

A range, not a point estimate approach to yield management acknowledges that any single day’s or week’s reward figure is a sample, not a constant.

Benefits of Staking Crypto

Passive Income

Viewing staking just as a source of passive income is not entirely correct due to the reasons outlined above: it bears inherent risks, its primary goal is compensating validators for real work, and a good portion of it does not even translate to real economic gain. However, fee-derived rewards represent real economic yield extracted from network activity, meaning your reward comes from users paying to transact, not from printing new tokens.

It may be true that delegating to a validator requires minimal ongoing effort—you monitor performance and occasionally switch validators if your chosen one underperforms or suffers slashing penalties. In practice, the commissions eat into the supposed yield and the real rates are not high enough to outpace the inflation. Running your own validator node, by contrast, demands 24/7 uptime, software updates, security hardening, and active monitoring to avoid downtime penalties.

Last but not least, typical proof-of-stake yields in 2026 range from 3% to 12% in nominal token terms—meaning the percentage increase in the number of tokens you hold, not your total return in fiat or purchasing power; it is not a savings account or bank deposit product, and it definitely does not behave like a guaranteed savings account rate.

Network Security

Validator incentive alignment works because validators earn rewards for honest behavior and lose capital for dishonest behavior. This lays the foundation of economic security, which is a necessary component of healthy tokenomics. Fraud deterrence operates through slashing—validators who misbehave have a portion of their stake permanently burned. Together, these mechanisms shift the security model to economic commitment, making attacks expensive and self-destructive.

That being said, staking can hurt security under specific conditions. If stake concentration funnels through a small number of large validators or centralized exchanges, the system becomes vulnerable to coordinated censorship, regulatory pressure, or correlated outages. Similarly, if validators run identical software configurations or rely on the same cloud infrastructure provider, a single bug or infrastructure failure can knock multiple validators offline simultaneously, risking chain liveness or temporary network halts. The security benefit of staking is real but conditional on stake being distributed broadly across independent operators.

Portfolio Strategy

Long-term position enhancement applies when an investor already intends to hold a token through volatility cycles; staking converts idle holdings into multiplying assets, increasing token-unit accumulation over time without requiring active trading. Inflation-offsetting matters on networks with high emission rates—staking can help maintain proportional ownership rather than being diluted by new issuance.

If you may need liquidity on short notice, the long-term-oriented benefit is weaker because lockup periods or unstaking delays can trap capital during drawdowns. Even high APYs can be overwhelmed by price drawdowns, which is why staking belongs in a risk framework, not in a headline-number mindset.

Risks and Key Considerations

Staking crypto generates rewards, but those rewards are paid in the same volatile asset you staked—so your unit count may grow while your portfolio’s dollar value falls. The real question is not whether staking produces yield but whether that yield survives the drawdown in price, the friction of liquidity constraints, and the operational risks embedded in the method you choose.

Price Volatility

Price exposure is the dominant risk in crypto staking because rewards compound your position in an asset that can drop faster than your yield accrues. Consider a 12-month scenario: you stake a token offering 18% APY, expecting to grow your holdings from 1,000 tokens to 1,180 by year-end. During the first two months, the token price drops 40%—from $1.00 to $0.60. The volatility dominates the yield when the percentage price swing in a short window exceeds the annualized staking return.

Liquidity Constraints

Liquidity in staking is a whole stack of overlapping constraints that readers frequently conflate. Lock-ups, unbonding or unstaking, withdrawal queues, cooldown periods all considerably restrict the movement of your capital.

“Cannot sell while staked” applies to tokens locked in native delegation, but “can sell a liquid staking token” introduces a different risk: the liquid token may trade at a discount to the underlying asset or lose its peg during market stress.

Before staking, check the staking UI or protocol documentation for these parameters: exact unstaking time, whether rewards auto-compound or require manual claiming, whether any early-exit mechanism exists with or without penalty.

Slashing

Slashing is protocol-level penalization applied to validators for misbehavior or prolonged downtime, and as a delegator, your staked tokens can be partially destroyed if your chosen validator is penalized. This is distinct from missed rewards, which occur when a validator experiences temporary downtime or raises commission fees—you lose potential earnings but your principal remains intact.

To reduce slashing risk as a delegator, verify validator hygiene signals before staking: consistent uptime history over multiple months, stable commission rates without frequent changes, and evidence of infrastructure redundancy or professional operation. Diversify your stake across multiple validators rather than concentrating all tokens with a single operator, and avoid validators with unusually low commission if their infrastructure track record is unproven.

Opportunity Cost

Speaking of missed rewards, opportunity cost in staking extends beyond “you can’t use funds elsewhere” into three comparisons that determine whether staking is worth it relative to your alternatives. First, compare the staking APY to the token’s inflation rate to calculate real yield. Second, evaluate alternative returns available with liquid capital, including selling into rallies or deploying into other yield sources where appropriate. Third, assess the value of maintaining dry powder for dips, taxes, and rotation opportunities.

Counterparty Risk

Delivery or counterparty risk materializes differently depending on where custody of your staked tokens actually sits. Centralized exchanges hold your tokens in pooled, exchange-controlled wallets, exposing you to insolvency risk if the platform collapses or imposes withdrawal freezes during liquidity crises. Staking pools and third-party validator operators introduce operational risk. Self-custodial staking eliminates third-party trust but shifts the risk inward: if you lose your private key or seed phrase, no authority can recover your funds.

To reduce counterparty exposure, diversify custody across providers and methods rather than concentrating everything on a single exchange or pool; test withdrawals on a small scale before committing large amounts; set internal concentration limits; and read the platform’s terms on reward rate changes and withdrawal policies.

When there is technically no counterparty, smart contract risk applies specifically to DeFi staking protocols, liquid staking platforms, and restaking mechanisms. Four failure modes dominate this category: contract bugs or exploits, oracle manipulation, admin key compromise or governance attacks, and depegging/discount risk in liquid staking tokens during stress events. Audits by reputable firms reduce but do not eliminate these risks.

So, Is Staking Worth It? Making the Decision

Before committing tokens to a staking arrangement, run through this decision checklist:

- If you will hold for 6+ months → stake most; if under 30 days → avoid entirely. Lock-up mechanics and unstaking delays mean short-horizon holders pay more in opportunity cost than they earn in rewards.

- If you need emergency liquidity within weeks → partial stake at most. Full staking exposure leaves no buffer when unstaking windows stretch days or epochs.

- If a 30–50% drawdown would force you to sell → reduce exposure first, stake second. Rewards never compensate for being overleveraged into a volatile asset.

- If you cannot verify validator uptime, inflation rate, and governance risk → do not stake that token. Conviction requires data, not narrative.

Time Horizon

Staking rewards compound slowly, and that compounding only begins to offset typical price movement and transaction friction when your holding period extends beyond short-term noise.

See for yourself: unstaking delay + gas fees + potential price slippage erase any yield; rewards have no time to accumulate in under 30 days. For a time window this short, it might be best to avoid it entirely.

Rewards begin to cover fees once 1 to 6 months pass, but only consider it if you can exit without multi-day delays; monitor for planned liquidity events.

6–24 month-long staking plan is a strong fit for most networks. That’s enough runway for rewards to compound through one or two market cycles; unstaking friction becomes minor relative to total gain. Longer than that is even more than enough to ride through drawdowns and benefit from compounding; suits conviction-driven holders treating tokens as protocol equity.

Ethereum’s current 3.6% annual staking yield becomes meaningful at the 12-month mark, when compounding begins to offset typical intra-year drawdowns and transaction costs; shorter windows leave you chasing pennies while risking dollars. If you are holding specifically to trade a catalyst event within weeks, those rewards will not move your P&L—liquidity and timing flexibility will.

Liquidity Needs

Your staking posture must map directly to how quickly you need access to capital:

| Scenario | Staking Posture | Rationale (Access + Unstaking Delay) |

|---|---|---|

| (a) Emergency cash needs | No stake | If you might need to liquidate within 72 hours, unstaking delays (7–21 days for most PoS networks) eliminate staking as an option; keep funds in a wallet or yield-bearing account with instant withdrawal. |

| (b) Planned large expenses | Partial stake (under 50%) | If a known expenditure falls 3–6 months out, stake only the portion you will not touch; unstake the target amount one full epoch before the deadline to avoid last-minute liquidity gaps. |

| (c) Trading/rotation strategy | No stake or liquid staking only | Frequent portfolio rebalancing and entry/exit timing require same-block liquidity; native staking lockups conflict directly with tactical positioning—use liquid staking derivatives if you must capture yield. |

| (d) Long-term cold storage | Fully stake | If the tokens sit untouched for 12+ months, unstaking delay becomes irrelevant; staking turns idle holdings into compounding positions without added operational overhead. |

Some staking pools charge 2%–5% of rewards as their commission. If you are operating in scenario (b) or (c), where your holding window is marginal, subtract that fee drag from your gross APY before deciding whether the net return justifies the liquidity trade-off.

Risk Tolerance

Staking rewards do not insulate you from price exposure; they add a small income layer on top of full directional risk. If a 30–50% drawdown would force you to sell at a loss, staking rewards will not change that outcome—reduce your position size first, then stake only what you can afford to hold through volatility.

Your staking method determines your counterparty and slashing exposure:

- Risk-averse posture: Prefer self-custody delegation to a validator with transparent uptime history (99%+ over trailing 90 days), published fee structure, and clear withdrawal terms. Avoid centralized platforms that co-mingle funds or obscure slashing accountability.

- Due-diligence signal to look for: Check the validator’s historical slashing record on-chain (zero slashing events), confirm their staked amount is large enough to signal skin in the game but not so dominant that they approach centralization risk (avoid validators holding more than 5% of total network stake).

- What to avoid: High-leverage yield products that combine staking with lending or derivatives; these layer additional smart contract risk and liquidation mechanics on top of base staking risk.

If you cannot locate a validator’s uptime percentage or withdrawal policy within five minutes of searching, that opacity is itself a risk signal—move to a validator or pool with published operational metrics.

Project Conviction

Staking requires you to hold a token, so staking a project you would not hold unstaked is a decision error, not a diversification strategy. Ask yourself these questions to verify whether a network merits allocation before locking funds:

- Token inflation/issuance rate: What percentage of new tokens enter circulation annually? Good answer: Inflation is explicitly capped (e.g., Ethereum post-merge trending toward deflation) or predictably declining on a published schedule. Red flag: Inflation is variable, governance-adjustable without notice, or exceeds 15% annually.

- Validator decentralization: How many active validators secure the network, and what is the Nakamoto coefficient (minimum validators needed to control 33% of stake)? Good answer: Nakamoto coefficient above 5; validator set distributed across multiple jurisdictions and entities. Red flag: Fewer than 100 validators, or top 10 validators control over 50% of stake.

- Roadmap/shipping cadence: Has the team delivered major upgrades on schedule over the past 12 months? Good answer: At least two significant mainnet upgrades or feature launches in trailing year, with transparent Github commit activity. Red flag: Roadmap is vague; last major update occurred over a year ago; repeated delays with no post-mortem explanation.

- Ecosystem usage: Are developers building on the network, and are users transacting? Good answer: Rising or stable active addresses, non-zero DeFi TVL, and at least three live applications with real usage (not testnets). Red flag: Declining active addresses quarter-over-quarter; ecosystem page lists only partnerships, not live products.

- Governance/upgrade risk: Who controls protocol changes, and how transparent is the process? Good answer: On-chain governance with published proposals and voting records; upgrade proposals require multi-week discussion periods. Red flag: Core team holds unilateral upgrade keys; governance process is informal or happens off-chain in private channels.

- Audits and security posture: Has the staking contract or protocol been audited by a reputable third party? Good answer: At least two independent audits by firms like Trail of Bits, Certora, or OpenZeppelin; audit reports published and findings addressed. Red flag: No audits, or audits conducted by unknown entities with no track record.

- Validator/node operator transparency: Can you verify validator performance metrics (uptime, commission, slashing history) on-chain or via a public dashboard? Good answer: Network provides a public explorer or validator leaderboard with real-time uptime and commission data. Red flag: No validator transparency; performance metrics are self-reported or absent.

Conclusion

At the end of the day, crypto staking is not a one-size-fits-all magic risk-free yield generator: it’s only really worth it when your time horizon exceeds two years and you hold conviction in the underlying network. Staking is not worth it when you require liquidity within six months or maintain low tolerance for principal volatility. Typical yields vary by network and are heavily influenced by inflation schedules, validator participation, and fee layers; returns are variable, and staking involves both technical and market risk.

Frequently Asked Questions

Is staking crypto safe?

Staking carries distinct risk categories, each with a corresponding mitigation action you can implement before committing funds. Price volatility represents the largest real-world exposure: your staked tokens can appreciate or depreciate regardless of yield earned, so position sizing and a multi-year time horizon are non-negotiable if you want to absorb drawdowns without forced exits. Liquidity and unstaking delays lock your capital for days to weeks depending on the network (Ethereum’s unstaking queue can extend beyond 7 days during high-exit periods, Solana typically 2–3 days), meaning you should never stake emergency funds or capital you might need on short notice. Slashing risk applies to proof-of-stake networks that penalize validators for downtime or malicious behavior: reduce this by choosing validators with documented uptime above 99% and diversifying across multiple validators if the protocol allows. Counterparty risk separates self-custody delegation (you control the wallet, the validator only processes blocks) from exchange staking (the exchange controls the keys), with exchange custody introducing insolvency and regulatory seizure vectors. Smart-contract risk enters the picture exclusively when you use liquid staking derivatives (like Lido’s stETH) or DeFi yield products that wrap your staked position in additional contracts, each of which can contain exploitable code.

Safer setups include native delegation from a self-custodial wallet like Ledger or Trezor, where you retain private-key control and select a well-capitalized validator with public track records, or staking through large, audited pools operated by established entities (Coinbase Cloud, Kraken, Figment). Higher-risk setups involve newly launched DeFi protocols offering double-digit yields through unaudited contracts, unknown validators with no performance history, or structured yield products that layer leverage or derivatives on top of the base staking position. None of these configurations make staking “principal protected”—you remain fully exposed to the asset’s price movement, and a 50% token decline will outweigh any single-digit APY you earned during the holding period.

How much can you earn from staking?

Typical staking yields in 2026 range from 1.2% to 7.2% annually depending on the network, with large-cap proof-of-stake chains clustering in the lower half of that band and mid-cap or high-inflation networks pushing toward the upper bound. Ethereum validator rewards sit around 3.6% annual yield according to Chainalysis data, while Solana delivers approximately 7.19%, Avalanche 1.16%, and BNB Chain 2.21% based on Grand View Research benchmarks. High-yield outliers like Cosmos (ATOM) have touched 18.5% as of April 2026 according to Revolut reporting, but these elevated rates frequently coincide with higher token inflation or smaller validator sets, which introduce additional risk vectors. Remember: all these figures represent APY paid in the staked token, not guaranteed fiat returns—if the token loses 40% of its value in two months, an 18% APY will not offset the principal erosion.

Which assets are best to stake?

Which coins to stake? Selecting a staking asset begins with criteria, not coin lists, because the “best” token depends on your specific goals and risk tolerance rather than a universal ranking. Apply these six selection filters in sequence: (1) Long-term conviction—only stake tokens you would hold through a 50% drawdown, because staking does not insulate you from price risk; (2) Liquidity and unstaking terms—confirm the unlock period fits your capital availability and that secondary markets exist if you choose liquid staking derivatives; (3) Slashing history and operational maturity—prioritize networks with established validator infrastructure and minimal historical slashing events; (4) Inflation versus real yield—distinguish between nominal APY (new tokens printed) and real yield (value captured from network fees or external revenue); (5) Validator and pool decentralization—avoid networks where a single entity controls more than 33% of stake, as this introduces centralization and censorship risk; (6) Ecosystem and custody support—ensure your preferred wallet or exchange supports native staking for that asset, because third-party bridges introduce additional attack surface.

What you should not inform your opinion by: never choose an asset solely by headline APY—a 20% yield on a token that drops 60% in six months leaves you down 40% net, while a 4% yield on a stable asset that appreciates 10% delivers 14% total return. Always compare inflation-adjusted outcomes and stress-test the scenario where the token loses half its value during your staking period.

What are good beginner-friendly staking options?

Beginner paths to staking exist on a spectrum from maximum convenience to maximum control, with each step requiring additional operational knowledge and accepting new tradeoffs. Here are the four primary entry points ranked by accessibility:

1) Exchange staking represents the fastest route: deposit your tokens on Crypto.com, Uphold, or Robinhood, navigate to the staking section, click a button, and earn yield within 24 hours. The platform handles validator selection, unstaking queues, and tax reporting automatically. The tradeoff: you cede custody to the exchange (counterparty risk), pay a platform fee that can range from 15% to 25% of gross rewards according to exchange disclosures, and remain vulnerable to withdrawal freezes during regulatory actions or liquidity crises. Suitable for users who prioritize simplicity and trust their chosen exchange’s solvency.

2) Wallet-based delegation to a validator grants you more control: download a self-custodial wallet that supports staking (Ledger Live, Phantom, Keplr), transfer your tokens, select a validator from the in-wallet list, and delegate directly on-chain. You retain private-key custody throughout, which eliminates exchange counterparty risk, and you typically pay only the validator’s commission (often 5–10%) rather than layered platform fees. The tradeoff: you must research and choose a validator yourself, monitoring their uptime and commission changes manually, and you handle your own wallet security and backup procedures. Suitable for users comfortable managing private keys who want to avoid centralized intermediaries.

3) Staking pools lower the barrier to entry for networks with high minimum requirements: instead of needing 32 ETH to run an Ethereum validator (worth approximately $64,000 at $2,000 per ETH as of 2026), you contribute any amount to a pooled staking service like Lido or Rocket Pool, which aggregates capital from many users and distributes proportional rewards. The tradeoff: pool operators charge a fee (2–5% of rewards per Aqru), and you accept smart-contract risk from the pool’s code—if the contract is exploited, your stake can be drained. Suitable for users with capital below the solo validator minimum who accept DeFi risk in exchange for access.

4) Running a validator represents the advanced path: stake the network’s minimum (32 ETH for Ethereum, 1,000 AVAX for Avalanche, amounts vary by chain), configure and maintain server infrastructure, ensure 99%+ uptime, and monitor slashing conditions continuously. You earn the full yield without paying validator commission or pool fees, but you assume operational burden—downtime penalties, hardware costs, and the technical expertise required to troubleshoot node software. Suitable only for users with technical background, capital reserves, and time to manage infrastructure.

Which coins can you stake?

Whether you can stake a coin depends on its consensus model and how your chosen platform implements yield products. Proof-of-stake networks commonly support native staking—Cardano is a canonical example—while proof-of-work assets generally do not offer protocol staking; if you see “staking” on a proof-of-work coin like Litecoin or a meme token like Shiba Inu, it is typically an exchange-run rewards program or a DeFi-style incentive mechanism rather than true consensus staking secured by validator collateral.

If you’re evaluating specific network mechanics, start with chain-specific resources for ETH staking and SOL staking.