What is Ethereum Staking? A Beginner’s Guide

Key Takeaways

- 🏗️ Ethereum staking by definition means posting collateral to secure the network; not “earning interest.” Protocol-level staking means locking ETH as slashable collateral; validators propose blocks and submit attestations—rewards are paid in ETH and are not guaranteed.

- 🏗️ 32 ETH is the hard line for running a validator; it’s not the line for earning rewards. You need exactly 32 ETH to activate a solo validator, but you can stake smaller amounts through pools or liquid staking, trading control for fees and extra risk surface.

- 🏗️ Rewards are variable and come from multiple sources—APY is a moving target. Returns fluctuate with total ETH staked (dilution), validator performance, and execution-layer activity (priority fees and MEV), then get reduced by service fees and any downtime penalties.

Disclaimers:

This article is not financial, tax, or legal advice. Ethereum staking involves volatility risk (ETH price fluctuations), liquidity risk (withdrawal delays or unstaking queues), and operational risk (validator slashing penalties for downtime or protocol violations). Staking rewards are not guaranteed and fluctuate based on network participation, transaction activity, and consensus-layer dynamics. Withdrawal and exit conditions are governed by Ethereum protocol rules, which can change with network upgrades. Always consult qualified professionals for personalized guidance and ensure you understand the custody model, penalty structure, and tax reporting obligations specific to your jurisdiction before staking.

Contents

- 1. Overview of Ethereum Staking

- 2. How Ethereum Staking Works

- 3. Ethereum Staking Requirements

- 4. Ethereum Staking Methods

- 5. Ethereum Staking Rewards and APY

- 6. Liquid Staking Tokens (LSTs)

- 7. Top Ethereum Staking Platforms

- 8. Exchange-Traded Products for Staked Ethereum

- 9. ETH Staking Risks and Key Considerations

- 10. Developments in 2026

- 11. Conclusion

With Ethereum’s transition, Proof-of-Stake has cemented its place as one of the cornerstones of the crypto economy. And yet, it is also often misrepresented or overcomplicated.

In this guide, you’ll find an overview of proof-of-stake consensus fundamentals, how the staking mechanism actually works on Ethereum, the technical and financial requirements for participation, a breakdown of staking methods (solo, pooled, liquid, and custodial), the role and risks of liquid staking tokens (LSTs), platform comparisons, the considerations you must understand before committing capital, and answers to the most common questions new stakers ask.

Overview of Ethereum Staking

Ethereum

Hopefully, by the time you are asking, “how do I stake Ethereum”, you have the questions "what does staking mean" and “what is Ethereum” sorted out but just in case, either read the full version in our guide or a brief recap below.

Ethereum refers to a programmable blockchain network that enables users to execute transactions and deploy smart contracts—self-executing code that powers decentralized applications. At its core, Ethereum is a form of blockchain technology built for global, permissionless coordination and decentralized record-keeping across thousands of independent nodes. ETH (ether) is the native cryptocurrency of the Ethereum protocol, used to pay transaction fees and reward validators.

Some confusion might stem from the fact that ether is more often referred to as Ethereum, despite there being a clear and deliberate distinction: Ethereum is the protocol and infrastructure, ether is ETH, the asset you hold, stake, or trade. Regardless, the phrasing “staking Ethereum” is very common despite being technically incorrect.

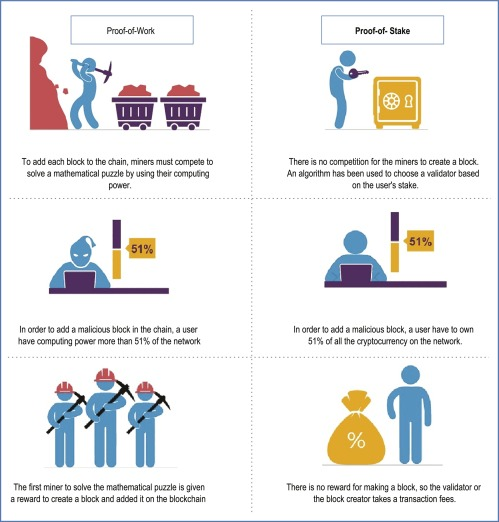

Proof-of-Stake

Speaking of staking, Proof-of-stake (PoS) is Ethereum's consensus mechanism that replaced proof-of-work in September 2022. Now, instead of miners competing with computational power, Ethereum selects validators from a validator set—a pool of participants who have each deposited 32 ETH—to propose new blocks and attest to the validity of others' proposals.

Validators perform two core duties: block proposal (suggesting the next block in the chain) and attestation (voting to confirm that a proposed block is legitimate). When validators execute these duties correctly while remaining online, they earn compensation; when they fail to participate or act maliciously, they face penalties ranging from minor balance reductions to severe slashing events that can forfeit a substantial portion of their stake.

In other words, these validator incentives are the cornerstone of Ethereum’s security model: cooperate or lose capital. This seems a feasible reason the staking threshold is rather steep.

As of May 2026, Ethereum's proof-of-stake network secures over $40 billion in value with over 8 hundred thousand validators actively participating in consensus (per DefiLlama and Beaconcha.in respectively). The scale of participation directly impacts individual staking rewards: as more validators join, the annual percentage yield decreases because the fixed issuance of new ETH is distributed among a larger group. In addition, the penalty mechanisms (minor inactivity leaks and severe slashing for provable malicious actions) create strong economic incentives for validators to maintain high uptime and follow protocol rules precisely.

Cryptocurrency Staking

In general, cryptocurrency staking is the act of posting collateral (i.e.your cryptocurrency holdings) to participate in a blockchain's proof-of-stake consensus process, not a lending arrangement or interest-bearing account. Validators lock their assets to demonstrate economic commitment to honest behavior; in return, they receive newly issued tokens and a portion of transaction fees collected from network users, as is the case with Ethereum.

Cryptocurrency staking operates under fundamentally different mechanics compared to proof-of-work mining, where computational power determines block production rights. Here’s what staking is and is not:

- Is: Collateral for validator participation, earning protocol-level issuance rewards plus transaction-fee-related income tied directly to network activity and validator duties.

- Is not: Proof-of-work mining that requires specialized hardware to solve cryptographic puzzles; staking depends on economic stake and uptime, not computational power races.

- Is not: A guaranteed APY product or fixed-income instrument; rewards vary based on total network participation, validator performance, and penalties for downtime or malicious behavior (slashing).

The idea that staking resembles a savings account with predictable returns is a misunderstanding. Staking functions as a security mechanism with the risks and responsibilities inherent in running a validator node.

Key Definitions:

- Validator: A network participant that proposes and attests to blocks on the Ethereum proof-of-stake beacon chain (consensus layer), earning staking rewards for correct behavior and facing penalties for downtime or rule violations.

- Staking Rewards: Cryptocurrency earned by validators (or delegators in pooled models) for securing the blockchain, sourced from protocol issuance and transaction fees.

- Slashing: A protocol-enforced penalty that destroys a portion of a validator's staked ETH for malicious actions (e.g., double-signing) or prolonged inactivity, designed to maintain network integrity.

- Liquid Staking Token (LST): A tokenized representation of staked ETH (e.g., stETH, rETH) that users receive when depositing into liquid staking protocols, allowing them to trade, lend, or use staked assets in DeFi while still earning staking rewards.

- Custody: The control and safekeeping of private keys; in staking, "self-custody" means you retain full control of your ETH and validator keys, while "custodial" means a third-party service holds and manages those keys on your behalf.

How Ethereum Staking Works

With the definitions out of the way, we can actually dive into how the process works. The validator lifecycle progresses through distinct stages: depositing and locking ETH, activation into the validator set, performing consensus duties (block proposal and attestation), voluntary exit, and finally withdrawal of principal and rewards.

ETH Locking

As mentioned, staking ETH requires depositing 32 ETH into the Ethereum staking contract. "Locking" doesn't simply mean holding ETH in a wallet—it means committing those funds to the protocol as slashable collateral that secures the network economically.

When you deposit ETH for staking, the funds transfer to a protocol-controlled staking contract where they remain locked and non-transferable until you complete the exit and withdrawal process. The stake itself serves three critical functions: besides participation rights and economic security, it creates skin-in-the-game accountability that aligns your interests with network health (hence, the “stake”).

Validator Operations

Running a validator extends beyond simply depositing ETH. Validators must keep their validator keys secure, maintain up-to-date client software to comply with protocol changes, ensure consistent uptime to avoid missing duties, those being: 1) proposing blocks when selected and 2) attesting to the validity of blocks proposed by others.

Every validator is a node (an instance of protocol software) but not every node can validate. In general, a node verifies and relays blockchain data, contributing to network health by maintaining a copy of the chain and broadcasting transactions. A validator, in contrast, actively participates in consensus using cryptographic keys to sign blocks and attestations, earning rewards but also exposing bonded capital to slashing risk.

Validator operations demand reliability because downtime directly impacts earnings. Missing attestations reduces your rewards incrementally, while missing a block proposal when selected results in lost block rewards and transaction fees. Prolonged offline periods can trigger inactivity penalties that further gradually reduce your staked ETH balance, creating economic pressure to maintain consistent participation.

Transaction Validation

Validators don't individually "approve" each transaction the way a bank approves a wire transfer but validate blocks and the transactions they contain according to protocol rules: blocks follow consensus rules, included transactions are properly signed and formatted, and the state transitions proposed by the block are valid according to the Ethereum Virtual Machine's execution rules.

The validation process happens at two levels. When a validator proposes a block, they assemble transactions from the mempool (a queue for transactions just submitted), confirm their validity, and include them in a candidate block. When validators attest, they're voting that the proposed block they've seen is valid and should be added to the chain, contributing to the network's collective decision about which version of history becomes canonical.

Another distinction of PoS from previous security models is it can guarantee transaction finalization by having validators with at least two-thirds of the total staked ETH attest to a block and its ancestors. That portion of the chain becomes considered irreversible under normal conditions.

Validator Activation

When you deposit 32 ETH to the staking contract, your validator doesn't immediately start earning rewards. Instead, it enters a pending state, waiting in the activation queue until the protocol allows it to join the active validator set.

First, it moves from "Deposited" to "Pending" once the protocol recognizes your deposit, then transitions to "Active" when your position in the queue reaches the front and the protocol formally adds you to the active validator set. Then, you're now eligible for selection as a block proposer and expected to submit attestations every epoch, with both duties carrying rewards and penalties.

The activation queue exists because the protocol limits how many validators can join or leave per epoch to maintain network stability. During periods of high staking demand, thousands of validators might be queued, creating wait times that range from hours to weeks depending on network conditions. This intentional throttling prevents sudden mass changes to the validator set that could destabilize consensus.

Validator Selection

And now, for something more validators see more often. The protocol selects validators for specific duties using two distinct randomness-based mechanisms. For block proposals, one validator per slot receives selection as the proposer with the responsibility to build and broadcast a new block. For attestations, validators are organized into committees—groups of validators assigned to attest during specific slots within each epoch.

Both slots and epochs are cadence setters: a slot lasts for 12 seconds and each epoch is 32 slots long. The former is effectively the same as block time in other blockchains, i.e. how long does each block take to be formed and included in the ledger. Epochs are a longer unit of time, usually reserved for more drastic adjustments, such as problem difficulty in Bitcoin or voting on the state of the entire network in Ethereum.

The Ethereum Consensus Specification uses a verifiable random function that produces random selections based on chain state, making it computationally infeasible to determine which validators will be selected as proposers or which committees they'll join until shortly before their duties begin. The lack of predictability prevents validators from gaming the system by selectively coming online only when profitable duties are guaranteed.

Block Proposal

The Ethereum network expects one new block to be proposed and validated every slot or a dozen seconds. When a validator is selected as the proposer for a given slot, they assemble a candidate block by collecting pending transactions from the mempool, ordering them according to priority (typically by transaction fee), executing the state transitions, and packaging everything into a properly formatted block.

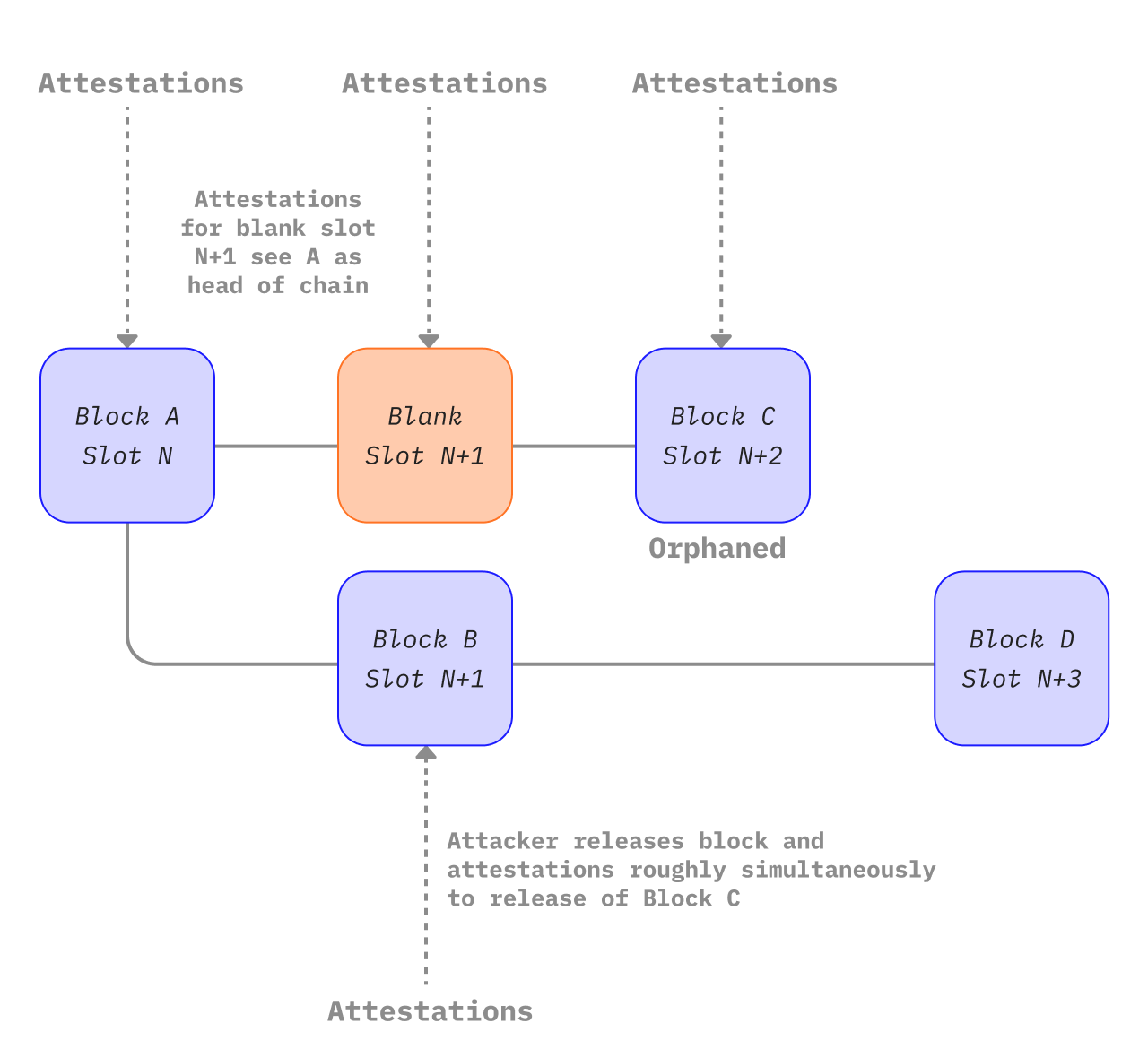

The selected proposer builds the block during the early portion of their assigned slot, broadcasts it to the network through peer-to-peer gossip, and then relies on other validators to attest to its validity. The block doesn't become "accepted" simply because the proposer published it—acceptance depends on enough validators in the assigned committee seeing the block, verifying it, and including positive attestations in their votes.

Slots are rigid windows, and if a proposer is offline, experiences network delays, or fails to broadcast their block quickly enough, that slot passes empty. The chain continues forward regardless, with the next slot's proposer building atop the most recent valid block. This keeps Ethereum's block production steady and predictable, maintaining the network's consistent throughput.

Attestation

Validators also create attestations that serve as votes on two critical pieces of information: the current head of the chain (which block they believe should be the latest canonical block) and the justification and finalization progress of previous blocks. These attestations aggregate across the validator set to build consensus about the true state of the blockchain.

Every active validator produces exactly one attestation per epoch. The protocol assigns each validator to a specific slot within the epoch and organizes them into committees, ensuring that each slot receives attestations from a statistically significant portion of the validator set. This distribution balances security (enough validators voting on each block to prevent attacks) with efficiency (avoiding network congestion from simultaneous messages).

To be clear, proposal creates a candidate block with new transactions and state transitions, while attestation validates and votes for blocks that proposers have already created. A validator might go weeks without proposing a block due to random selection, but they attest every single epoch, making attestation the primary continuous duty that generates the majority of staking rewards.

Exit

Any validator is free to stop participating in consensus duties and begin the process of retrieving their staked ETH at any time. When a validator initiates an exit request, they're signaling to the protocol their intention to transition out of active duties, which triggers a state change that removes them from future proposer and attester selections.

Validators might choose to exit because they want to upgrade their hardware, restructure their staking setup, manage risk by reducing exposure during uncertain periods, or simply because they no longer wish to operate the necessary infrastructure. Exit provides a protocol-defined path for gracefully leaving the validator set without penalties.

This step is separate from withdrawal: exiting stops you from participating in consensus and accumulating new rewards, but it doesn't immediately return your funds. Your principal plus any earned rewards remain locked in the staking contract until withdrawal conditions are met and the protocol processes it. Before you exit, the protocol needs time to verify no slashable offenses occurred during your active period before releasing bonded collateral.

Withdrawal

Should you so choose, the successful validator lifecycle concludes with withdrawing both your original principal and any rewards accumulated during your time as an active validator. This process is the actual transfer of funds from the staking contract back to your specified withdrawal address.

The protocol distinguishes between withdrawal eligibility and withdrawal execution. Eligibility means your validator has completed the exit process and satisfied any waiting periods the protocol imposes to ensure finality and slashing accountability. Execution is the actual processing of your withdrawal, which happens automatically once you become eligible through the protocol's sweep mechanism that processes withdrawals in queue order.

Withdrawals became significantly simpler after Ethereum's Shanghai/Capella upgrade enabled both partial withdrawals (rewards only) and full withdrawals (entire stake). Before this upgrade, staked ETH remained locked indefinitely, creating uncertainty that deterred many potential stakers. Luckily, the current system ensures you can always access your funds after completing the proper exit procedure.

Ethereum Staking Requirements

So far we have established it takes a lot to prove you are willing to have some “stake” in Ethereum’s operations: at the very minimum, a whopping 32 ETH to lock up and the resources to maintain your node while it does a responsible job. Naturally, that is not all, so let’s take a more inquisitive look into requirements in particular.

Minimum Stake Amount

The 32 ETH required for activation are not a minimum, they are an exact amount to register a new validator on the network. This staking threshold is intentional to balance network security with validator decentralization: too low, and the network risks becoming bloated with validators; too high, and participation becomes exclusive. Once activated, that 32 ETH cannot be withdrawn or transferred until a validator exit is processed, which introduces a lock-up consideration beyond the pure capital requirement.

From there, adding balance to an existing validator operates under different rules. If your validator's effective balance falls below 32 ETH due to penalties, you can top it up through additional deposits to the staking contract without activating a new validator. However, the effective balance that counts toward rewards caps at 32 ETH regardless of how much you deposit. Depositing 40 ETH to one validator provides no additional reward compared to 32 ETH.

However, staking via pools or centralized exchanges removes the barrier entirely. Services like Lido, Rocket Pool, or Coinbase allow staking with any amount by pooling user deposits to meet validator thresholds collectively. Your capital becomes a share in a larger validator operation, and you may receive derivative tokens representing your stake. This drastically lowers the entry point but introduces third-party trust and smart contract dependencies.

Hardware and Software

Running a validator node also demands infrastructure that meets simultaneous availability, security, and performance thresholds. The architecture requires two distinct client software layers working in tandem: an execution client (like Geth or Nethermind) that maintains Ethereum's state and processes transactions, and a consensus client (like Prysm or Lighthouse) that handles validator duties and block finalization. Both clients must run continuously on the same machine or network segment with synchronized block data.

Minimum Viable Validator Architecture Checklist:

- CPU: 4+ cores (preferably modern architecture with AES-NI support for cryptographic operations)

- RAM: 16 GB minimum (32 GB recommended to handle state growth and client overhead)

- Storage: 2 TB NVMe SSD (avoid SATA SSDs or HDDs—sync times suffer, and IOPS bottlenecks cause missed attestations)

- Network: Stable broadband with 10+ Mbps upload/download (25+ Mbps recommended); avoid metered connections due to ~1-2 TB monthly data transfer

- Time Synchronization: NTP client configured with sub-second accuracy (Validator attestations are slot-specific; clock drift causes missed duties)

- Power: Uninterruptible power supply (UPS) to survive brief outages without triggering downtime penalties

Operational Security Baseline

Think again if you thought all this hardware and software do not require operational security. Validator keys used for signing attestations and blocks must remain accessible on the validator machine since they're required for real-time duties. These keys are distinct from withdrawal credentials, which control access to staked ETH and should be generated offline and stored securely—ideally on hardware wallets or air-gapped systems. In practice, you should treat your withdrawal credentials like a long-term crypto wallet key that is never exposed to internet-connected devices.

Backups follow a dual-track approach: export validator keystores immediately after generation and store encrypted copies in geographically separate locations (fire, theft, or hardware failure can otherwise eliminate your ability to exit gracefully). Simultaneously, document your mnemonic seed phrase in a secure manner. Regardless of the chosen method to secure the seed phrase, never store plaintext keys or mnemonics in cloud storage, password managers, or email.

Client software updates are best checked weekly, monitoring for critical patches and planned hard forks that mandate coordinated upgrades across the network. Running outdated clients during a fork can cause your validator to attest on the wrong chain, triggering slashing penalties.

Uptime

Ethereum's validator economics tie directly to continuous availability, with an explicit uptime target of 99%+ considered baseline for profitable operation. Translated into allowable downtime, it permits roughly 7.2 hours offline per month. Each missed attestation costs you the equivalent of what you would have earned, plus a small additional penalty. At 99% uptime, you lose approximately 1% of potential annual rewards; drop below 95%, and you risk breaking even or operating at a loss.

Beyond missed attestations, extended downtime triggers Ethereum's inactivity leak mechanism—a protocol feature designed to finalize the chain even when large portions of validators go offline simultaneously. If your validator remains inactive during an inactivity leak, which begins after the network fails to finalize for 4 epochs, penalties accelerate quadratically, potentially consuming several percent of your stake over weeks. This doomsday scenario is engineered for catastrophic network events but indiscriminately punishes all offline validators during such periods.

Slashing, the harshest penalty Ethereum can impose, destroys a minimum of 1 ETH from your validator balance and forcibly exits you from the network. However, slashing occurs only for provable malicious behavior: double-signing conflicting attestations or blocks, which typically results from running duplicate validator instances with the same keys (a configuration error during failover setups). Simple offline status, even for months, never triggers slashing. Uptime failures cost opportunity and gradual penalties, while key management failures cost chunks of capital instantly.

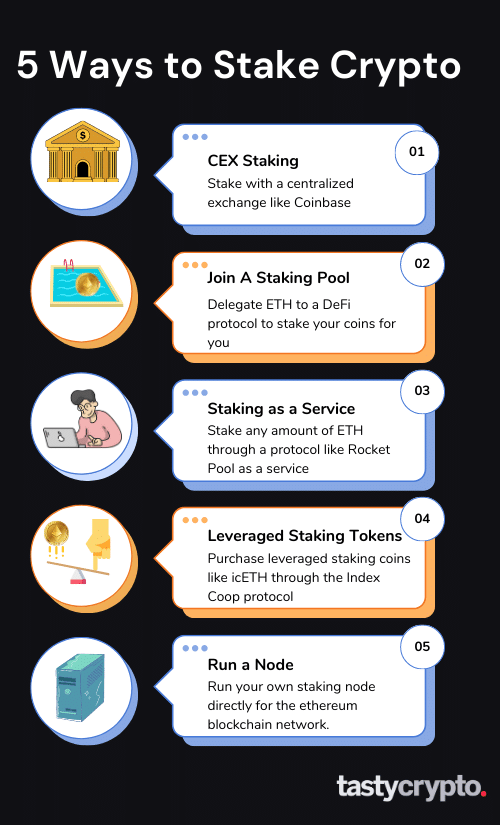

Ethereum Staking Methods

Before choosing your staking path, evaluate these decision-critical criteria that appear consistently across all methods:

- Minimum ETH requirement — the capital threshold needed to participate

- Custody & control — who holds your private keys and withdrawal credentials

- Operational responsibility — hardware setup, uptime monitoring, and maintenance burden

- Liquidity & exit path — how quickly you can access your staked ETH and accumulated rewards

- Fees & commissions — what you pay and to whom (protocol, operator, or platform)

- Primary risks — method-specific vulnerabilities beyond general staking risks

Solo Staking

Solo or home staking implies running your own validator node by depositing 32 ETH and maintaining the infrastructure that validates transactions and proposes blocks on the Ethereum Consensus Specification.

Who it's best for:

- Technical users comfortable with command-line interfaces and system administration

- Those prioritizing maximum decentralization and protocol contribution

- Holders with 32+ ETH willing to manage ongoing operational demands

Minimum stake & access: Exactly 32 ETH per validator node. This threshold is hardcoded into the Ethereum protocol and cannot be split—you must commit the full amount to activate a validator. If you can afford it, you can run multiple validators in 32 ETH increments.

How rewards are received: Native ETH accrues directly to your validator balance on the Beacon Chain. Rewards compound automatically as your effective balance increases (up to the 32 ETH cap), with excess skimmed to your withdrawal address. After the Shanghai upgrade, you can perform partial withdrawals to access accumulated rewards while keeping your validator active, or full exits to reclaim your entire stake.

Fees & what you're paying for: No third-party commissions—you keep 100% of consensus rewards (attestations, block proposals, sync committee participation). However, you absorb all infrastructure costs: hardware depreciation, electricity, internet bandwidth, and your own time for maintenance and monitoring.

Liquidity & exiting: Zero immediate liquidity. Waiting time to exit depends on how many other validators are exiting simultaneously, and during high-congestion periods, exits can take days.

Key risks specific to this method:

- Slashing risk from operational errors: Signing conflicting attestations or being offline during critical duties can result in ETH penalties

- Hardware failure: Power outages, network drops, or drive corruption can cause missed attestations and gradual balance leaks

- Client bugs: Running outdated or minority clients increases vulnerability to consensus failures

- Key management catastrophe: Losing your validator keys or mnemonic means permanent loss of access

Solo staking represents the purest form of participation in Ethereum's proof-of-stake mechanism, where you directly secure the network without intermediaries. However, "self-custody via a node operator" services exist where you retain withdrawal credentials but delegate infrastructure to specialists—this hybrid is closer to Staking-as-a-Service than true solo staking, even though you control the keys.

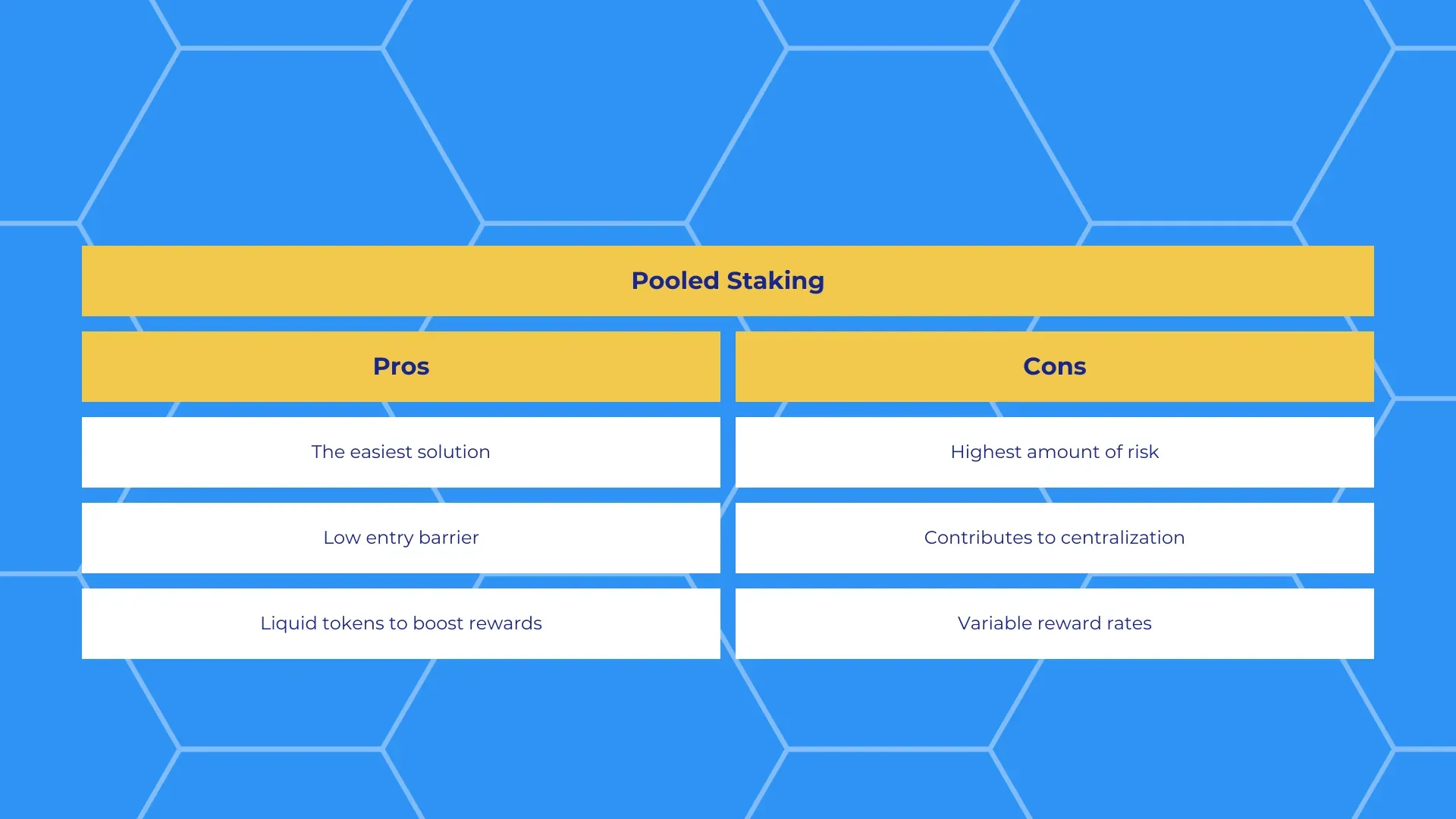

Staking Pools

Pools let you deposit any amount of ETH into a smart contract that aggregates funds from multiple users to reach the 32 ETH validator threshold, distributing proportional rewards to all participants.

Who it's best for:

- Holders with less than 32 ETH seeking staking yield

- Users wanting exposure without technical infrastructure management

- Those comfortable with smart contract risk in exchange for accessibility

Staking pool entry barriers are dramatically lower than solo staking; practical minimums typically range from 0.01 to 1 ETH depending on the provider.

In a pooled validator staking, your ETH joins a shared pool managed by the protocol's validator set, with rewards distributed proportionally based on your deposit share. You don't choose operators—the protocol handles validator duties across its fleet. Some pools let you pick specific node operators from a marketplace, creating a more direct relationship but introducing operator reputation as a selection factor. Both consolidate capital to meet the 32 ETH requirement, but governance and operator accountability differ significantly.

Most staking pools issue a receipt token representing your staked position (e.g., rETH from Rocket Pool). Rewards accrue either through token price appreciation relative to ETH (each receipt token becomes redeemable for more ETH over time) or through rebasing mechanisms that increase your token balance. Some pools distribute rewards as separate ETH deposits to your account, which you can claim periodically.

Validator commission in staking pools typically ranges from 5-15% of staking rewards, covering validator infrastructure, smart contract maintenance, protocol development, and insurance funds. Some pools charge deposit or withdrawal fees (0.1-0.5%) on top of commission. You're paying for convenience, capital aggregation, and the pool's operational expertise.

Liquidity & exiting varies by pool design. Non-liquid pools require you to wait for validator exits and protocol withdrawal queues (similar to solo staking timelines). Liquid staking pools issue tradeable receipt tokens that you can sell on DEXs immediately, providing instant liquidity—though this introduces depegging risk.

Key risks specific to this method:

- Smart contract vulnerabilities: Bugs in pooling contracts can lock funds or enable exploits

- Pool size and operator concentration: Large pools may control significant validator shares, potentially centralizing consensus power if operators are geographically or infrastructurally concentrated

- Withdrawal queue congestion: If many pool participants exit simultaneously, you may face delays even if the pool itself has no technical issues

Liquid Staking

What is liquid staking? It’s staking ETH through a protocol that issues a liquid staking token (LST) representing your staked position, allowing you to use that token in DeFi while your underlying ETH remains staked and earning rewards.

Who it's best for:

- DeFi-active users who want to maintain capital efficiency while staking

- Those prioritizing liquidity and flexibility over maximum yield

- Holders comfortable with receipt token mechanics and smart contract complexity

Similar to staking pools, liquid staking protocols typically accept deposits from 0.01 ETH upward. The primary difference is the tradeable receipt token that unlocks additional utility.

Each LST is a claim on the underlying staked ETH plus accrued rewards. For example, 1 stETH represents your proportional share of the Lido staking pool.

- Rebasing tokens: Your balance increases daily as rewards accumulate (e.g., stETH increases from 1.0000 to 1.0001 stETH as rewards compound)

- Reward-bearing tokens: The token's redemption rate increases while your balance stays constant (e.g., 1 rETH becomes redeemable for more ETH over time)

LSTs should trade at or near the value of the underlying staked ETH plus rewards. However, market conditions—liquidity crunches, smart contract fears, or mass exits—can cause the LST's market price to deviate from its redemption value. This creates arbitrage opportunities but also means selling your LST during depeg events may realize losses even if the underlying stake is healthy. LSTs are not all benefits with no overhead: you must monitor both the intrinsic redemption value and the market trading price when planning exits or using LSTs as collateral.

The receipt token is freely transferable and composable in DeFi—you can supply it as collateral, provide liquidity in DEXs, or use it in lending protocols while continuing to earn staking yield.

Protocol fees typically range from 8-10% of staking rewards, funding validator operators, protocol development, insurance reserves, and DAO treasuries. Some protocols add small deposit/withdrawal spreads (0.05-0.3%) to cover operational costs. You're paying for liquidity provision, smart contract infrastructure, and the ability to unlock capital efficiency through DeFi composability.

Liquidity & exiting: Immediate liquidity via secondary markets—you can sell your LST on decentralized exchanges anytime without waiting for protocol exits. Alternatively, some protocols offer direct redemption by burning LSTs to reclaim underlying ETH, subject to validator exit queues. The choice between instant sale and protocol redemption depends on LST market pricing relative to intrinsic value.

Key risks specific to this method:

- Depegging events: Market price can diverge from redemption value during stress, forcing you to choose between selling at a discount or waiting for protocol redemption

- Smart contract complexity: LSTs introduce additional layers of code (staking contract, token contract, DeFi integrations), each a potential vulnerability surface

- Composability risk: Using LSTs in DeFi protocols adds liquidation risk if the LST's value fluctuates or depegs while serving as collateral

- Provider concentration: Dominant liquid staking protocols controlling large shares of staked ETH can create systemic centralization risks for Ethereum consensus

Staking-as-a-Service

In this case, you supply the 32 ETH and retain withdrawal credentials (control of your funds), while a professional infrastructure provider runs and maintains the validator hardware and software on your behalf.

Who it's best for:

- Holders with 32+ ETH who want solo staking benefits without operational burden

- Those willing to pay for infrastructure expertise while maintaining custody

- Users seeking uptime guarantees through service-level agreements

The key difference from solo staking is outsourcing the technical responsibility rather than running infrastructure yourself. Staking-as-a-Service differs from pools or exchanges because you control the withdrawal keys—your ETH never leaves your custody. You also control the withdrawal address, so rewards flow to you without intermediary claims.

Service fees typically range from 5-15% of staking rewards or flat monthly costs ($20-100 per validator depending on service tier). You're paying for hardware provisioning, monitoring, client updates, slashing protection, 24/7 incident response, and guaranteed uptime levels. Some providers offer tiered pricing with premium SLAs guaranteeing 99.9%+ attestation effectiveness.

As is the case with solo staking, you face the same protocol exit queues. After exiting, withdrawals follow the standard sweep schedule, with funds flowing to your withdrawal address.

Key risks specific to this method:

- Provider dependency: Your rewards rely on the provider's operational excellence; poor maintenance or bankruptcy can lead to missed attestations

- Custodial ambiguity: Ensure the provider cannot access withdrawal credentials; some lower-tier services may request key access, which defeats the custody benefit

- Centralization through provider consolidation: If many users choose the same Staking-as-a-Service provider, that single operator's infrastructure risks can affect a large portion of staked ETH

Exchange Staking

Depositing ETH into a centralized exchange account where the platform stakes on your behalf is a popular option, crediting rewards to your account balance without requiring you to run infrastructure or manage keys.

Who it's best for:

- Users already holding ETH on exchanges who want convenient yield without transfers

- Beginners seeking the simplest onboarding with zero technical knowledge required

- Those prioritizing ease of use over custody or maximum returns

Exchanges impose widely varying minimums—some as low as 0.01 ETH, others requiring 1 ETH or more. Entry thresholds often correlate with the exchange's reward structure and internal pooling mechanisms.

Exchange staking is an account-based claim, not on-chain control. You don't hold private keys or withdrawal credentials—your stake is a balance entry on the exchange's internal ledger. This means:

- The exchange technically controls the underlying staked ETH

- Your legal claim is contractual (terms of service) rather than cryptographic

- Rewards are platform credits that the exchange can modify terms for (fee changes, reward rate adjustments)

- Withdrawal limitations may apply (lock-up periods, daily limits, verification requirements)

This structure introduces a distinct security threat class: platform and legal counterparty risk.

Ethereum Staking Rewards and APY

It’s important to know Ethereum staking rewards are variable payments, with Annual Percentage Yield (APY) fluctuating based on validator performance, network participation rates, execution-layer fee activity, and operational costs. Unlike traditional fixed-income products, realized staking returns depend on a combination of protocol-level issuance, transaction fees, MEV opportunities, and the specific staking method you choose.

Reward Components

- Consensus-layer issuance reward for attestations and block proposals: The Ethereum protocol mints new ETH as base rewards for validators who correctly attest to blockchain state and propose blocks when assigned. This component is predictable and scales inversely with total staked ETH—currently the largest share of staking income.

- Execution-layer tips and priority fees: Users include priority transaction fees in transactions to expedite being included in a block during congestion. Validators proposing blocks collect these tips directly, creating variable income that spikes during network stress but can fall near zero during quiet periods.

- MEV (Maximal Extractable Value): Validators running MEV-boost software can accept bids from specialized builders who reorder transactions for profit, sharing a portion with the validator. MEV income is highly concentrated in DeFi-heavy blocks and requires specific infrastructure to capture, meaning not all validators participate equally.

- Penalties and opportunity cost from missed duties.

- Net-of-fee outcome after operator, pool, or exchange commissions.

APY Components

There is a large variety of moving parts that affect the annual percentage yield (APY) of staking on Ethereum. Incidentally, note that the term “APY” is used as a practical shorthand, not a promise of returns.

Staking participation rate acts as a dilution mechanism. When fewer validators participate, the Ethereum protocol distributes the same base issuance reward among a smaller pool, increasing individual validator rewards; conversely, as more ETH enters staking, yields compress.

Validator performance and uptime likewise directly impact your share of rewards. Missing even a small percentage of attestation duties reduces your effective yield.

MEV and priority fee variability introduces execution-layer unpredictability. During high-demand periods—NFT mints, token launches, liquidation cascades—validators proposing blocks can capture substantial transaction fees and MEV bundles, temporarily spiking returns well above baseline. However, these spikes are episodic and concentrated among block proposers, making execution-layer income inherently lumpy.

Service fees from pools, operators, or exchanges directly reduce net APY through validator commission. A liquid staking protocol charging 10% of gross rewards transforms a 4% headline APY into a 3.6% realized yield.

By the way, APY assumes automatic reinvestment of rewards and compounds them, while APR presents a simple annualized rate without compounding. Realized return is what you actually earn after accounting for downtime, penalties, fees, and timing of withdrawals. Many staking dashboards display APR-like rates (non-compounding base issuance) while marketing materials advertise APY, creating a ~0.3-0.5 percentage point perception gap that compounds over multi-year positions.

To eyeball your realized annualized return, multiply the ETH rewards earned over a period, divided by average ETH staked, by 365 divided by the number of days. Tools like Beaconcha.in provide granular breakdowns, allowing you to isolate each component and understand whether underperformance stems from missed duties or lower network activity.

Liquid Staking Tokens (LSTs)

Token Design

Liquid staking tokens (LSTs) represent a tokenized claim on staked ETH plus accumulated rewards, issued when you deposit ETH into a liquid staking protocol. The underlying staked ETH remains locked in Ethereum's validator set, while the LST circulates freely, tradable, transferable, and usable across decentralized finance applications. Your exit path depends on protocol mechanics: some LSTs allow on-chain redemption (burning the token to reclaim your staked ETH plus rewards), while others require selling on decentralized or centralized exchanges to exit your position immediately.

Two dominant reward-accrual models exist. Rebasing tokens like Lido's stETH increase your wallet balance automatically—your token count grows daily to reflect staking rewards. Non-rebasing tokens like Rocket Pool's rETH or Lido's wstETH maintain a constant token count but appreciate in value relative to ETH—the exchange rate between the LST and ETH rises as rewards accumulate. For holders, rebasing means your balance changes continuously (which can complicate DeFi integrations), while non-rebasing means the price-per-token increases but your balance stays fixed. Each model suits different use cases: rebasing tokens feel intuitive for passive holders, while non-rebasing tokens integrate more cleanly into lending protocols and accounting systems.

The fee stack naturally erodes your net return. Most liquid staking protocols charge a protocol fee (typically 5-10% of staking rewards), a node-operator or validator commission (another 5-10%), and occasionally withdrawal or exit fees when you redeem. Fees are almost always taken from rewards, not principal—so your initial deposit stays whole, but your reward stream shrinks.

Depegging

Therefore, the "peg" for liquid staking tokens is not a hard peg—it's an expected relationship between the LST's market price and its underlying redeemable value (the staked ETH plus accrued rewards you could theoretically claim by burning the token). Both discounts and premiums are normal in healthy markets: the former reflect liquidity imbalances or friction in redemption, while the latter signal high demand for DeFi collateral or staking exposure without needing to lock ETH directly.

What to check before buying or selling an LST:

- On-chain liquidity depth: Inspect the size of the primary DEX pools (Curve, Uniswap) and order-book depth on CEXs—shallow liquidity means high slippage risk.

- Current discount or premium vs. redeemable value: Calculate the gap between market price and the protocol's stated redemption rate; a widening discount without clear cause signals trouble.

- Holder and LP concentration: If a few wallets control most circulating supply or liquidity, sudden selling can destabilize the peg quickly.

- Audit history and bug bounty posture: Review public audits, active bug bounty programs, and whether the protocol has suffered past exploits or near-misses.

- Redemption functionality: Confirm whether on-chain redemption is currently operational—check for paused withdrawals, queue backlogs, or protocol announcements.

- Validator performance metrics: Monitor the protocol's validator uptime, slashing incidents, and MEV smoothing (if applicable) to assess underlying collateral quality.

- Market stress indicators: Watch ETH price volatility, DeFi leverage ratios, and cross-protocol liquidation cascades that could spill over into LST markets.

LST depegging risk is separate from ETH price risk, but they can stack. If Ethereum drops 20% and your LST simultaneously depegs by 5%, you've absorbed a compounded loss. A stable LST peg does not protect you from ETH price volatility, and a rising ETH price does not immunize you from LST-specific smart contract or liquidity failures.

Top Ethereum Staking Platforms

Exchanges, liquid staking protocols, and decentralized node pools each trade off control, liquidity, and complexity in fundamentally different ways. For the purposes of this guide, let’s review a top example of each.

| Platform | Staking Type | Custody Model | Token Received | Minimum to Start | Fee/Commission Model | Withdrawal/Liquidity Path | Key Risks | Best For |

|---|---|---|---|---|---|---|---|---|

| Coinbase | Exchange staking | Platform holds validator keys & withdrawal credentials | No | Often as low as 0.00001 ETH; varies by account tier | Platform commission (percentage of rewards); spreads on deposits/withdrawals | Withdrawal subject to platform queue + regulatory processing; no instant liquidity token | Custody/rehypothecation, platform insolvency, account freeze/regulatory hold | Users prioritizing simplicity, tax reporting integration, and tolerance for custody trade-offs |

| Lido | Liquid staking | Node operators hold validator keys; protocol smart contract manages withdrawal credentials | Yes (stETH, rebasing) | No protocol minimum; practical minimum driven by gas cost of wrap/unwrap | Protocol fee (shared between node operators and DAO treasury); DEX swap spread if selling stETH | Instant liquidity via secondary market (DEX/CEX trading); protocol unstake queue as fallback | Smart contract exploit, stETH depeg during stress, node operator slashing, protocol governance capture | Users needing self-custody + liquidity who accept smart contract and depeg surface |

| Rocket Pool | Decentralized node pool | Node operators run mini-pools with bonded collateral; protocol smart contract manages withdrawal credentials | Yes (rETH, appreciation model) | No protocol minimum; practical minimum driven by gas cost | Node operator commission (set per mini-pool); protocol commission to treasury; swap spread if selling rETH | Instant liquidity via secondary market; protocol unstake queue as fallback | Smart contract exploit, rETH depeg, node operator misconduct/mini-pool failure, protocol complexity | Users wanting decentralization without 32 ETH, willing to navigate higher complexity and smaller liquidity depth |

Coinbase

Coinbase staking credits your account with staked ETH and accrues rewards as a separate balance entry, not a liquid token. Rewards appear as incremental ETH in your Coinbase account, typically compounded and displayed daily. This means you cannot move your staked ETH to an external wallet until you initiate an exit.

Coinbase holds both the validator keys and the withdrawal credentials; you control only your Coinbase account login credentials and any two-factor authentication mechanisms tied to that account. The validator nodes themselves—where your staked ETH secures the network—are operated by Coinbase infrastructure, meaning the platform can, in theory, move, upgrade, or shut down validators without your explicit transaction-by-transaction consent. Regulatory holds, account freezes, or platform insolvency scenarios leave you dependent on Coinbase's legal and operational status to recover funds.

A withdrawal enters two queues: Ethereum's protocol-level exit queue, which delays based on how many validators are exiting network-wide, typically days to weeks, and Coinbase's internal processing queue, which can add additional wait time depending on platform liquidity and operational batch cycles. Secondary market liquidity does not exist for this model—your only exit is through Coinbase itself.

As the model implies, Coinbase charges a commission on staking rewards (historically in the 25-35% range). This commission is deducted before rewards are credited to your balance, so the displayed APY is post-fee. Additionally, watch for withdrawal fees if moving unstaked ETH off the platform (flat fee or percentage-based depending on network conditions and account tier), and deposit spreads if purchasing ETH on Coinbase to stake (the buy price includes a bid-ask spread that can exceed the advertised trading fee). If your jurisdiction treats staking rewards as taxable events, Coinbase provides tax forms that may simplify reporting but do not eliminate the liability.

Lido

Lido commands a dominant share of the liquid staking market—often controlling 25-30% of all staked ETH as of 2026—raising centralization concerns that mirror the validator concentration risks Ethereum itself aims to avoid; this market position makes Lido both highly liquid and a potential single point of failure for protocol-level governance influence.

Lido staking issues stETH, a liquid staking token that rebases daily to reflect accrued rewards. When you deposit ETH into Lido's smart contract, you receive stETH at a 1:1 ratio initially; as validators earn rewards, the stETH balance in your wallet increases automatically (rebasing mechanism). You hold stETH in your own wallet, and you can transfer, trade, or use it in DeFi protocols (e.g., collateral in lending markets, liquidity provision in AMM pools). The stETH token itself represents a claim on the underlying staked ETH plus accrued rewards, redeemable via Lido's unstaking queue or tradable on secondary markets.

Lido's node operators hold validator keys, but the protocol's smart contracts control withdrawal credentials. You, as the stETH holder, control the token in your wallet; you decide when to sell, unstake, or deploy it in DeFi. The protocol cannot freeze your stETH or prevent you from transferring it—your custody is self-sovereign at the wallet level. However, the validator keys are managed by a curated set of professional node operators (e.g., infrastructure providers vetted by the Lido DAO), meaning you do not control validator-level decisions like exits or fee recipient addresses.

Exiting Lido staking offers two primary paths: instant liquidity via secondary markets or protocol unstaking. The instant route involves selling stETH on an exchange. The protocol unstaking path queues your stETH for redemption through Lido's withdrawal queue, which adds Ethereum protocol exit delays plus Lido's internal processing.

Lido charges a protocol fee—historically 10% of staking rewards—split between node operators (who earn the majority) and the Lido DAO treasury (which funds development and insurance). This fee is invisible at the wallet level; you see only the net staking yield reflected in your rebasing stETH balance.

Rocket Pool

Similarly to Lido, Rocket Pool staking issues rETH, a liquid staking token that, unlike the competitor, appreciates in value relative to ETH rather than rebasing. When you deposit ETH into Rocket Pool's smart contract, you receive rETH at an exchange rate that increases over time as validators earn rewards. Your rETH token count stays constant, but each rETH becomes redeemable for more ETH. You are expected to hold rETH in your wallet, and you can trade it or use it as collateral in DeFi protocols.

Rocket Pool's architecture distributes validator keys across independent node operators who run mini-pools. You, as the rETH holder, control the token in your wallet; the protocol's smart contracts manage withdrawal credentials, ensuring that when you burn rETH to unstake, the ETH flows back to your address. Node operators cannot access your funds beyond the validator-level mechanics.

Exiting Rocket Pool staking mirrors Lido's dual-path model: instant liquidity via secondary markets or protocol unstaking. A detail worth mentioning is rETH liquidity is typically shallower than stETH's—expect higher slippage for large exits. The protocol unstaking route involves burning rETH through Rocket Pool's smart contract, which queues your redemption against available mini-pool liquidity. If mini-pools have excess capacity, you may receive ETH in days; if not, you wait for validators to exit on the Ethereum protocol level, adding weeks.

Rocket Pool charges node operators a commission set at the mini-pool level, plus the practical costs of trading (swap spread and gas) if you exit via secondary markets.

Exchange-Traded Products for Staked Ethereum

In 2026, a guide to Ethereum staking would be incomplete without mentioning that these instruments exist. An exchange-traded staked-ETH product (ETP) is a regulated financial wrapper that holds Ethereum and delegates its staking operations to validators, allowing investors to gain exposure through traditional brokerage accounts. Importantly, these products combine two distinct return sources: ETH price exposure (the spot value of the underlying cryptocurrency) and staking yield passthrough or retention (the validator rewards, net of fees, which may or may not flow to investors depending on product structure).

That structure ranges from grantor trusts and closed-end trust vehicles without redemption mechanisms to ETF wrappers that keep share prices tightly aligned with net asset value (NAV) and notes that represent issuer’s debt rather than Ether directly. In most products, the issuer contracts with specialized institutional validator operators rather than running nodes directly. ETH itself typically resides with a qualified custodian—often a regulated entity like Coinbase Custody or BitGo—under segregated accounts that prevent commingling with the sponsor's operational assets.

Choosing between these ETPs or direct participation comes down to a whole laundry list of criteria. Do you have the brokerage access or do you prefer the on-chain approach and full sovereignty? How complicated can you let your tax history become vs. how many DeFi opportunities you wish to take advantage of? Are you comfortable with custodial and counterparty risks weighted against operational complexity and security? Ultimately, starting off here is largely the same question as choosing between crypto vs stocks.

ETH Staking Risks and Key Considerations

Although so far we have covered a lot of ground when it comes to the good and the bad of ETH staking, it would not hurt to reiterate the risks in a standalone section so you can build a risk management tactic along with your strategy.

First come the protocol-level risks: slashing and penalties. After all, they are risks baked directly into the mechanism to complement the incentives for staking. Slashing is the more severe penalty but unless you somehow double-sign while proposing, cast contradictory votes during attestation, or run duplicate validators, this should not be a concern. Liveness faults are a lot more common and likely to sink your returns, not even through balance leakage but missed opportunity costs. Follow the best practices during setup and throughout maintenance, and you should be fine.

Now, when you are staking through a pool or further integrating your staked positions via LSTs, smart contract risk becomes a major concern, compounded by the fact that it is often outside of your control. What you can do is due diligence: Review audit recency and whether audits covered the current contract version; verify active bug bounty programs with meaningful reward caps; understand the upgradeability model (including timelocks); examine admin key controls; research historical incidents; and understand redemption mechanics (including queue delays and secondary market dependencies).

Thirdly, custody inevitably introduces risks, whether with a third-party custodian or in self-custody. Risk management here comes down to evaluating the tradeoff of what you can tolerate or mitigate. In self-custody arrangements, validator signing keys and withdrawal credentials are unrecoverable if lost, and incorrect setup can lock you out of access or even end up in slashing. Third-party custody shifts risk from operational burden to counterparty trust.

Liquidity risk for staking manifests in lock-ups and exit conditions. During market drawdowns or sudden capital needs, this liquidity constraint means you cannot quickly exit positions. LSTs and liquid staking do not remove it entirely, and like was mentioned earlier, introduce smart contract risks and the risk of depegging.

Speaking of which, ETH staking should not be understood as yield bearing for the reason that even if your ETH holdings grow, the market volatility can erode the stake’s economic value. Simply put, if you had staked 32 ETH a year ago, you could have about 33.3 ETH today but because Ether was traded for $2,550 back then and today changes hands for $2,110, your stake in dollar denomination went from $81,600 to $70,263. In this scenario, staking can be seen as hedging against price depreciation, since instead of losing 17% over a year, the position is down by 13.9%; nevertheless, a negative is a negative.

Developments in 2026

Ethereum's consensus mechanism evolved measurably from prior years through several protocol-level adjustments that directly impact validator operations and staking returns. Unlike 2023–2024, when the Ethereum protocol focused on stabilizing post-Merge infrastructure, 2026 developments concentrate on optimizing validator lifecycle efficiency, refining reward distribution mechanics, and addressing queue congestion as the validator set scales.

The Ethereum Consensus Specification introduced adjustments for stakers in 2026. Validator activation and exit queue algorithms received optimization to handle increased network scale; consensus clients implemented stricter uptime expectations; reward calculation mechanics adjusted to account for higher staking participation; slashing penalties underwent recalibration to distinguish between minor operational errors and malicious behavior more granularly; and client diversity expectations became more explicit in community guidance and client recommendations.

Liquid staking protocols and node-operator consolidation create measurable centralization vectors that affect network security and individual staker outcomes. When liquid staking is dominated by a small number of providers, Ethereum faces governance optics challenges and practical concentration risk: a major protocol incident can propagate quickly across DeFi, while operator consolidation can increase correlated failure modes. Splitting capital between major providers and more decentralized alternatives reduces single-protocol exposure and supports validator client diversity.

Ethereum's staking participation rate reached 35% of total ETH supply by early 2026, up from 15% in early 2023—a clear trajectory of growing validator adoption driven by liquid staking accessibility and rising institutional involvement. Rising participation produces directional effects on yields and network congestion: as more ETH enters staking, individual APRs compress, and activation/exit queues can extend during high-demand periods.

Conclusion

Ethereum staking transforms ETH holdings into network security tools while generating passive income, but choosing the right method requires matching your technical comfort, capital size, and liquidity needs to one of five distinct approaches. Entry points range from very small deposits in some pools to the full 32 ETH solo requirement, and understanding the trade-offs—custody, liquidity, fee drag, and operational risk—matters more than accessibility.

Check out ChangeHero blog for even more insightful articles on all things crypto. To stay in touch with news and updates, subscribe to ChangeHero on Telegram, X (Twitter), and Facebook.

Frequently Asked Questions

How long does it take to unstake ETH from a validator?

The complete unstaking timeline typically spans 1-5 days depending on network conditions. When you initiate a voluntary exit, your validator first enters the activation queue—this stage can take anywhere from minutes to several days based on how many other validators are exiting simultaneously. Ethereum processes exits in discrete intervals because the network operates on 12-second time slots organized into epochs of 32 slots (~6.4 minutes each), meaning exit events aren't continuous but batched. After your validator successfully exits, withdrawals become available within roughly 1-5 days as the protocol processes withdrawal sweeps across all validators.

What's the difference between starting an exit and actually receiving my ETH?

Starting an exit means submitting a voluntary exit message to remove your validator from active duties, but this doesn't immediately return your funds. The exit itself requires waiting in the activation queue—during peak periods, thousands of validators might queue ahead of you. Once your validator completes its exit and enters the "exited" status, a separate withdrawal process begins where the protocol sweeps through validators to process withdrawals, adding another layer of timing that's protocol-driven rather than user-controlled. Think of it like submitting a resignation versus receiving your final paycheck—there's a structured settlement period between the two.

Can I speed up the unstaking process?

You cannot accelerate the protocol-level timing for native Ethereum staking—the exit queue, epoch processing, and withdrawal sweeps operate on fixed schedules determined by network rules. For liquid staking tokens (LSTs) like stETH or rETH, you can bypass the withdrawal queue entirely by selling or redeeming your tokens on secondary markets or through protocol redemption pools, though this option carries depegging risk during market stress when many holders attempt to exit simultaneously. The protocol's timing granularity exists to maintain network stability, preventing sudden mass exits from destabilizing consensus.

What can delay my unstake beyond the normal timeline?

Several factors create delays beyond typical withdrawal windows, and understanding which you can control matters for planning. Network-level delays include large exit queue sizes (uncontrollable), while operator-specific delays involve custodian batching practices—exchanges often batch withdrawal requests to optimize gas costs, adding hours or days to your wait. Smart-contract redemption mechanics for LSTs introduce their own timing constraints based on available liquidity and redemption caps. You control your choice of provider and whether to use liquid alternatives, but you cannot control protocol timing, queue congestion, or how quickly the Ethereum Consensus Specification processes validator state changes tracked on tools like Beaconcha.in.

How do liquid staking redemptions differ from native withdrawals?

Liquid staking tokens allow instant liquidity by trading or redeeming your receipt token (like stETH) rather than waiting for full protocol withdrawals to complete. When you redeem an LST through the protocol, you're accessing pooled liquidity or triggering validator exits on your behalf—this can be faster than solo staking but introduces smart contract vulnerability and liquidity constraint challenges. During periods of market stress or network congestion, LSTs can depeg from their underlying ETH value because redemption demand exceeds available liquidity, potentially forcing you to accept a discount or wait for the protocol's standard withdrawal process anyway.

What are my main staking options if I don't have 32 ETH?

Four primary alternatives exist, each with distinct custody and risk profiles that shape where control and risk reside. Staking pools aggregate small deposits from multiple users to run validators collectively—you contribute any amount but the pool operator controls the validator keys and you share slashing risk with other staking pool members. Liquid staking tokens (LSTs) give you a receipt token representing your staked ETH, which you can trade or use in DeFi while the protocol operator manages validators; here, smart contract vulnerability and operator centralization become your primary concerns. Staking-as-a-service platforms let you maintain key control while outsourcing technical operations, blending self-custody with managed infrastructure. Exchange staking offers maximum simplicity—you receive account credits rather than tokens—but sacrifice key control entirely since the exchange holds your ETH and validator keys.

What's the smallest amount I can stake?

Minimum deposits vary dramatically by provider, with some staking pools accepting as little as 0.0001 ETH to maximize accessibility for beginners. Platforms like Lido and Rocket Pool allow contributions starting around 0.01 ETH, though these minimums are UX decisions rather than protocol requirements—the underlying Ethereum network doesn't enforce deposit floors for pooled staking. Be aware that extremely small deposits may face proportionally higher fee impacts, and platform minimums can change based on operational costs or gas fee economics, so verify current thresholds before depositing.

Can I run a validator with less than 32 ETH?

Running your own validator node on the Ethereum Consensus Specification requires exactly 32 ETH as the validator activation minimum—this is a hard protocol rule you cannot bypass through any technical means. However, you can contribute capital to pooled validators operated by staking services, effectively "renting" a share of validator economics without meeting the 32 ETH threshold yourself. Returns and fee structures differ significantly: solo validators earn the full consensus-layer rewards minus hardware/electricity costs, while pooled contributors pay validator commission (typically 5-10%) plus potential protocol fees, reducing net APY but eliminating hardware responsibilities.

How do I choose between alternatives if I'm new to staking?

The decision hinges on balancing three competing priorities: custody control, operational simplicity, and risk tolerance. If maintaining key control matters most and you're comfortable with technical complexity, consider staking-as-a-service or pooled staking with non-custodial options. For maximum simplicity without hardware requirements, exchange staking or liquid staking protocols work best, though you're trusting the exchange or smart contracts respectively. LSTs add composability—using your staked ETH in DeFi—but introduce smart contract vulnerability and liquidity risk during redemptions. Start by honestly assessing whether you value control over convenience, then map that priority to the custody model that matches.

Do pooled staking rewards differ from solo validator returns?

Gross staking rewards remain identical at the protocol level—both solo and pooled validators earn the same base APY from Ethereum network issuance. The difference emerges in net returns after fees: solo stakers keep 100% of rewards minus only operational costs (electricity, hardware, internet), while pooled stakers pay validator commission to operators (often 5-15%) and sometimes additional protocol fees. For example, if gross APY is 4% and your staking pool charges a 10% commission on rewards, your net return becomes roughly 3.6%. MEV splitting also varies—solo stakers can capture more MEV through proposer-builder separation, whereas pooled staking distributes MEV across all participants after operator cuts.

When are staking rewards withdrawable?

Consensus-layer rewards become withdrawable immediately after the Shapella (Shanghai + Capella) upgrade enabled withdrawals in April 2023, but actual availability depends on your staking method. For solo validators, partial withdrawals (rewards exceeding 32 ETH) sweep automatically to your designated withdrawal address within days as the protocol cycles through all validators. Platform-specific withdrawal windows add another layer—exchanges often impose internal settlement periods or maintenance windows before transferring funds to your account. LST holders bypass protocol withdrawals entirely by selling tokens on secondary markets like Uniswap, accessing immediate liquidity albeit potentially at a discount during market stress when liquidity constraints tighten.

Why does my platform show 'available' but I can't transfer yet?

Several operational holds can freeze withdrawals even after your balance updates, and understanding these internal processes prevents frustration. Compliance and custody checks require platforms to verify identity, source of funds, or sanctions screening before releasing large withdrawals—regulatory requirements that can delay transfers by hours or days. Batching practices group multiple withdrawal requests to optimize gas fees, meaning your withdrawal waits for the next scheduled batch rather than processing immediately. Network congestion assumptions lead some platforms to pre-emptively delay user-initiated withdrawals during high-traffic periods, even if blockchain capacity exists. Internal settlement processes at exchanges can also hold funds while reconciling their hot/cold wallet balances and validator accounting.

Do I need a specific withdrawal address setup?

You must configure a compatible Ethereum execution-layer address (0x...) that can receive ETH before initiating withdrawals—this withdrawal credential must be set during validator setup or updated through a one-time credentials change process. The most common mistake involves attempting to withdraw to unsupported addresses on centralized exchanges that lack proper Ethereum deposit infrastructure or routing, causing funds to be rejected or lost. For solo stakers using the Ethereum Foundation's deposit tooling, your withdrawal address is specified in the initial deposit data and cannot be changed easily without validator exit. Double-check your destination wallet supports native ETH transfers and isn't a smart contract address unless you control its logic.

Can I withdraw partial amounts or must I exit completely?

Partial withdrawals automatically sweep any validator balance exceeding 32 ETH to your withdrawal address without requiring full validator exit—this typically happens within 4-5 days as the protocol's withdrawal sweep cycles through all active validators. Full withdrawals require initiating a voluntary exit, entering the exit queue, and waiting for complete validator shutdown before receiving your entire 32 ETH stake plus accumulated rewards. If you're staking through a pool or exchange, partial withdrawal availability depends entirely on the platform's liquidity and withdrawal policies—some allow flexible redemptions while others require minimum periods or batch processing schedules.

How do exchange withdrawal policies differ from protocol timing?

How do exchange withdrawal policies differ from protocol timing?

Ethereum's protocol-level withdrawal timing follows predictable, transparent rules based on epoch processing and validator sweeps tracked publicly on Beaconcha.in. Exchange withdrawal policies overlay additional restrictions driven by business operations: minimum withdrawal amounts to discourage small transactions, maximum daily limits for security and liquidity management, and scheduled maintenance windows that temporarily disable withdrawals. These platform-specific constraints can extend your effective waiting time by days beyond protocol requirements, particularly during peak demand when exchange liquidity buffers drain and they must wait for validator withdrawals to replenish reserves.Does staking ETH have fees?

Fee structures span multiple layers, and understanding each component prevents surprises in your net returns. Validator commission represents the operator fee charged by staking services (typically 5-15%) for running validator infrastructure and maintaining uptime. Pool protocol fees apply to decentralized staking platforms like Lido or Rocket Pool (usually 5-10%) to fund protocol development and DAO operations. MEV boost splits determine how maximal extractable value from block proposals is divided between you and infrastructure providers—this can add 0.5-2% to returns but often requires separate configuration. Exchange service fees or spreads manifest as the difference between advertised staking APY and what you actually receive after platform cuts. On-chain transaction costs hit when depositing ETH to staking contracts or withdrawing from pools, varying with Ethereum gas prices from $2 to $50+ per transaction during network congestion.

How do fees affect my net staking APY?

Fees directly reduce your net annual percentage yield by taking a cut of your gross staking rewards before distribution. For example, if Ethereum's base staking APY is 4% and your chosen platform charges a 10% commission on rewards, your calculation becomes: 4% gross × (100% - 10% fee) = 3.6% net APY. This percentage-on-rewards model means the fee impact scales with your stake size. Combined fees compound this effect: if you pay both an operator commission and a protocol fee, your calculation becomes multiplicative rather than additive.

Are there hidden costs beyond advertised fees?

Three hidden costs frequently catch stakers off-guard and should factor into your decision-making. Slippage when selling LSTs occurs when you exit liquid staking positions during market stress—depegging events can cost 1-5% of your principal as you sell stETH or similar tokens at a discount to underlying ETH value. Tax lots and recordkeeping overhead emerge because every staking reward and LST price fluctuation potentially creates a taxable event, requiring meticulous tracking. Opportunity cost from withdrawal delays manifests when you cannot access funds for weeks during volatile markets—missing a large price move while locked in unstaking queues represents real economic loss even though no direct fee was charged.

Do different staking methods have different fee structures?

Fee architectures vary dramatically by method, shaping long-term cost efficiency. Solo validators pay only operational costs (electricity, hardware depreciation, internet) without any commission. Pooled staking through decentralized protocols splits fees between node operators and protocol treasuries. Centralized exchanges typically charge higher implicit fees by advertising lower APYs than the network's base rate and pocketing the difference. Liquid staking protocols add smart-contract interaction costs for minting/redeeming tokens, making frequent small transactions proportionally expensive.

Can I negotiate or reduce staking fees?

Fee reduction opportunities depend entirely on your staking path and scale. Solo validators minimize fees by nature—running your own infrastructure eliminates all commission layers, leaving only electricity and hardware costs you can optimize. Large institutional stakers can negotiate custom fee arrangements with staking-as-a-service providers. For retail users in pooled or exchange staking, fees are generally non-negotiable and fixed by protocol governance or platform policy.

What's the safest way to stake for beginners?

Safety in staking represents a trade-off triangle between self-custody control, operational simplicity, and smart-contract exposure—no method eliminates all risks simultaneously. Centralized exchange staking maximizes simplicity but concentrates custody risk entirely with the platform. Liquid staking protocols reduce custody risk through self-custody but introduce smart contract vulnerability. Solo staking offers maximum control and eliminates third-party risks but demands technical competence to avoid self-inflicted slashing from misconfiguration. For true beginners, starting with a small allocation via a reputable liquid staking protocol can balance accessibility with reasonable risk distribution, allowing you to learn mechanics before committing larger sums or attempting solo operation.

How do I reduce slashing and penalty risk?

Slashing mitigation strategies differ fundamentally by staking method, and applying the right controls to your setup is essential. For solo validators, implement redundancy, ensure active monitoring via alerting tools, and practice client diversity to avoid correlated failures. For pooled staking, evaluate operator reputation metrics on platforms like Rated.network or Beaconcha.in validator leaderboards, checking their historical slashing incidents and uptime statistics before delegating. For exchange staking, assess platform risk limits by diversifying across multiple exchanges rather than concentrating all stakes with one provider.

What is concentration risk and how do I manage it?

Concentration risk emerges when too much of Ethereum's staked supply consolidates under few providers, threatening network censorship resistance and creating systemic vulnerability. Your practical mitigation checklist includes: diversifying across multiple staking providers rather than maximizing convenience with one platform, limiting exposure to any single LST to prevent correlated depegging risk during stress events, understanding governance and upgrade key controls, and monitoring market-share metrics quarterly to rebalance as concentration levels shift.

Can I lose more than my staked ETH?

Under normal circumstances, your maximum loss is capped at your staked principal—you cannot incur debt or lose additional funds beyond what you deposited. Slashing penalties for severe infractions can destroy a portion of your stake. For LST holders, smart-contract exploits theoretically could drain pools to zero, though protocols may employ safeguards and insurance mechanisms that reduce—but do not eliminate—tail risk. The closest scenario to "losing more" involves opportunity cost: large ETH price drawdowns during periods when you cannot exit due to queues or depegging can create losses in purchasing power beyond what the staking yield can offset.