RWA Crypto and Tokenization: Beginner’s Guide

Key Takeaways

- 🪩 An RWA token usually isn’t “the asset” — it’s a legal claim (SPV share, note, fund interest) whose enforceability lives in the governing documents, not the blockchain.

- 🪩 Tokenization is a lifecycle, not a mint button: origination → issuance → custody → redemption → settlement. Most blowups happen at the handoffs—especially custody, redemption gates, and reconciliation.

- 🪩 Market size is still small, and the composition matters: ~$3.2B–$4.1B total RWA value in 2026 (stablecoins excluded), with tokenized Treasuries ~70%.

- 🪩 RWAs don’t have “one” risk— they have a stacked risk model: regulatory classification + legal enforceability + counterparty/custodian dependency + smart contract/admin keys + oracle integrity + liquidity/redemption constraints. Any layer can fail independently.

- 🪩 Liquidity is conditional (and can be fake): 24/7 trading doesn’t help if redemption is monthly/quarterly, whitelists narrow your buyer set, or NAV updates lag. Always separate token liquidity from underlying liquidity.

- 🪩 Compliance shape-shifts token design: KYC/AML, transfer restrictions, and regulated venues often make RWAs investable for institutions—but also limit permissionless DeFi composability and fragment secondary markets.

Disclaimer

This article is not a piece of financial advice. When dealing with cryptocurrencies, remember that they are extremely volatile and thus, a high-risk investment. Always make sure to stay informed and be aware of those risks. Consider investing in cryptocurrencies only after careful consideration and analysis and at your own risk.

Real-world asset (RWA) crypto bridges the trillion-dollar traditional finance world and blockchain technology. Still, most confusion comes from one practical question: What, exactly, do you own when you hold an RWA token? After all, it could be a tokenized security, a claim on a custodied asset, or simply price exposure wrapped in crypto rails.

This guide clears that up. We’ll define what counts as an RWA, walk through the asset tokenization lifecycle step by step, and map the compliance, custody, and oracle risks that make RWAs fundamentally different from crypto-native primitives.

RWA Crypto Market Overview (2026)

Real-world asset tokenization, or RWA, creates a measurable on-chain economy anchored to real assets such as bonds, real estate, and credit instruments. As 2026 progresses, the RWA crypto market shows institutional momentum, regulatory maturation, and infrastructure refinement that set it apart from earlier speculative cycles.

RWA Market Size

First things first: the many metrics used to evaluate the RWA market are different for a reason:

- Total RWA Value is the aggregate notional value of traditional assets represented on-chain through tokenization protocols, including Treasuries, real estate, credit, and commodities. Almost always, stablecoins are explicitly excluded from this definition to avoid conflating cash-equivalent instruments with tokenized securities.

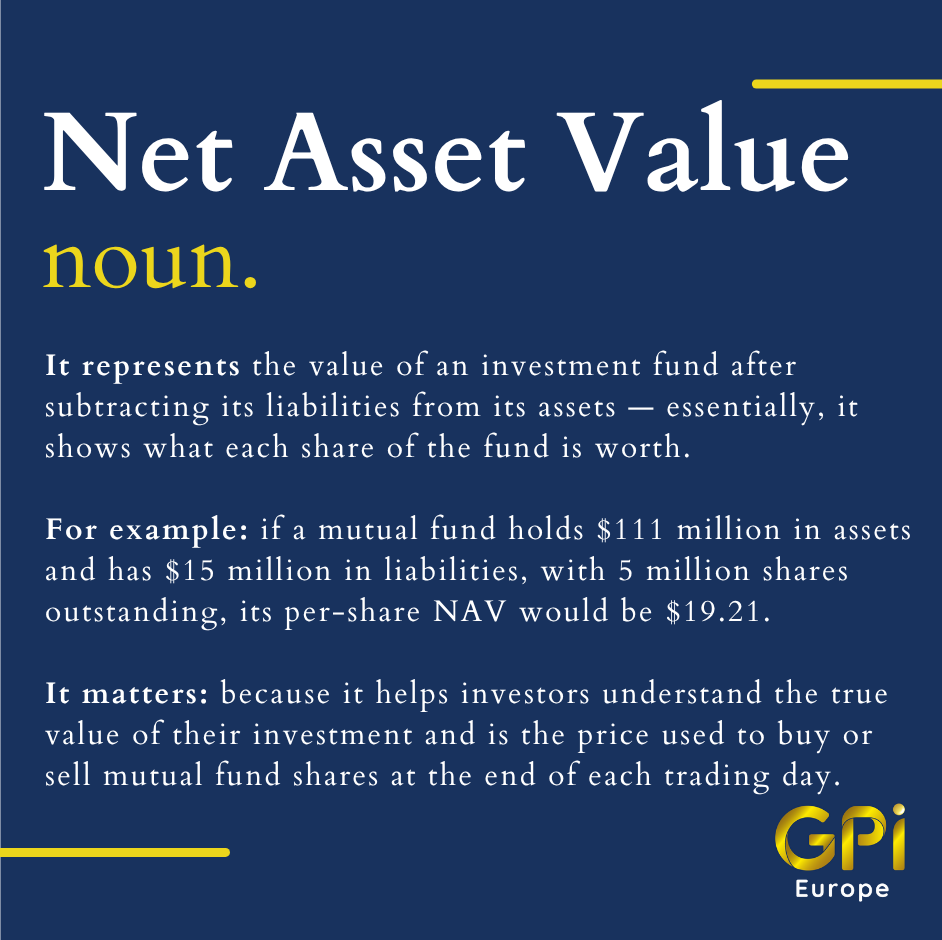

- Represented Asset Value: The underlying off-chain asset value that tokens reference, which may differ from market capitalization when tokens trade at premiums or discounts to net asset value (NAV).

- Market Capitalization: The circulating supply of RWA tokens multiplied by current market price, relevant primarily for exchange-traded RWA tokens rather than fund-like structures.

- Transfer Volume: On-chain transaction activity measuring how frequently RWA tokens change hands, serving as a liquidity and adoption indicator separate from issuance metrics.

- Asset Tokenization: The process of creating blockchain-based representations of real-world assets, distinct from wrapped crypto assets or synthetic derivatives.

Current estimates place total RWA value at approximately $3.2 billion to $4.1 billion in 2026, with tokenized U.S. Treasuries representing roughly 70% of this figure.

RWA totals are easy to quote but surprisingly tricky to measure precisely, for a few reasons that don’t show up in a dashboard headline:

- Fund-like RWA tokens often maintain NAV-based pricing through redemption mechanisms, whereas exchange-traded tokens may trade at premiums or discounts, making direct market cap comparisons misleading.

- Most RWA protocols maintain traditional custody arrangements for underlying assets, with on-chain tokens serving as claim certificates rather than direct ownership, creating measurement ambiguity when custody assets appear in both traditional and blockchain reporting.

- Bridges and wrapped asset protocols can create double-counting scenarios when the same underlying asset appears on multiple chains through different tokenization standards.

- Short-window growth metrics become distorted during large institutional redemptions or issuance events, particularly in tokenized Treasury markets where billion-dollar movements occur within days.

- Whether to count RWA tokens traded exclusively on permissioned, regulated marketplaces versus those accessible through open DeFi protocols affects total addressable market calculations.

Growth Drivers

Seven non-overlapping forces propel RWA market expansion in 2026:

1. Tokenized Treasury Issuance

Traditional finance institutions and mainstream financial service providers launch structured Treasury products directly on blockchain rails, with monthly issuance volumes exceeding $500 million during high-yield periods, signaling institutional appetite for blockchain settlement efficiency.

2. DeFi Collateral Integration

Protocols like Aave and Compound enable users to borrow against tokenized assets, with TVL growth in RWA-accepting pools indicating whether digital assets achieve DeFi composability or remain isolated in walled gardens.

3. Regulated Marketplace Launches

The proliferation of regulated marketplaces in jurisdictions like Singapore, Switzerland, and the UAE provides institutional-grade infrastructure, with exchange registration counts and daily trading volumes serving as adoption proxies.

4. KYC/AML Infrastructure Maturity

On-chain identity protocols enable transfer restrictions and compliance automation, with the number of verified addresses across major RWA protocols indicating whether regulatory requirements facilitate or hinder adoption.

5. Institutional Custody Integrations

Traditional custodians like State Street and Copper deploy RWA-compatible custody solutions, with assets under management in these specialized services revealing institutional commitment beyond pilot programs.

6. Oracle and Data Provider Expansion

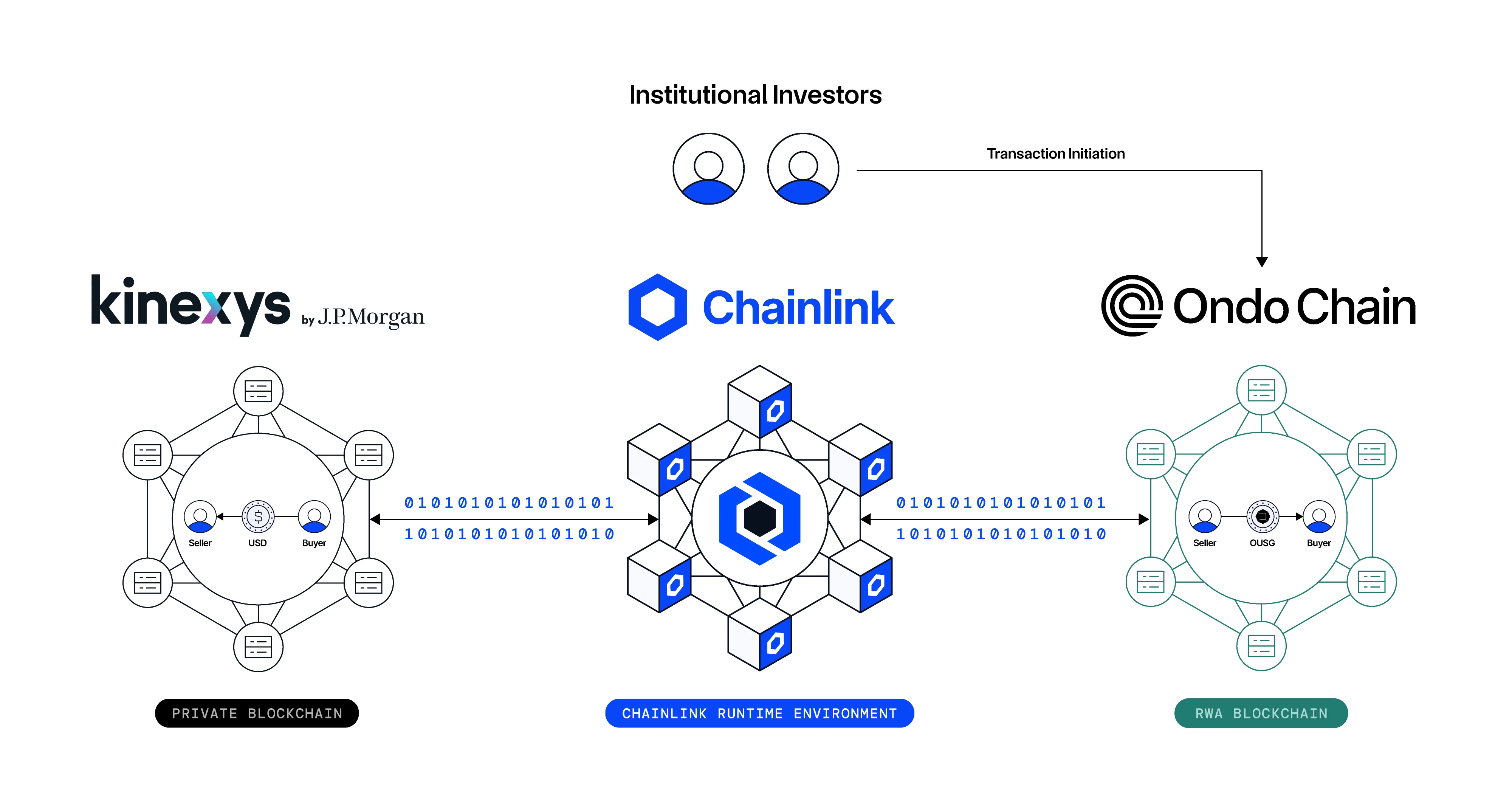

Real-time pricing and verification infrastructure from providers like Chainlink enables transparent valuation, with feed deployment counts and update frequencies indicating market infrastructure maturation.

7. Cross-Border Payment Efficiency

Blockchain-based asset transfers eliminate correspondent banking delays, with measurable improvements in settlement speed (T+0 vs T+2) and cost reduction (basis points saved) driving corporate adoption for high-frequency transfers.

Stablecoin Growth vs RWA Growth

Let’s address it early on: stablecoins and RWA tokens can both represent traditional assets on-chain, but they do not do the same job. Stablecoins are digital cash equivalents—payment rails and value transfer mechanisms without yield or underlying asset diversity. In contrast, RWA tokens represent income-producing securities, real estate, or credit instruments with distinct risk-return profiles.

Furthermore, stablecoin infrastructure supports RWA adoption through three channels: settlement (instant delivery-versus-payment), collateral (Treasury-backed stablecoins funding leveraged RWA positions), and distribution (digital dollar rails enabling global investor access). Consequently, stablecoin growth builds plumbing for RWA markets without counting toward RWA market size—a critical distinction for accurate analysis.

Institutional Participation

Institutions show up in the RWA ecosystem in very specific roles; they are not the same as a retail investor but with a heftier bag.

Traditional asset managers or corporations tokenizing their own securities, requiring disclosures equivalent to traditional offerings (prospectuses, audited financials) and regulatory registration under securities frameworks act as issuers or originators of RWA tokens.

Licensed intermediaries facilitating investor access to RWA tokens, demanding auditability of all transactions for anti-money laundering compliance and investor suitability verification become distributors or broker-dealers in this ecosystem.

Market makers or liquidity providers quote bid-ask spreads and maintain secondary market depth to necessitate transfer restrictions that prevent inadvertent sales to non-accredited or unsophisticated investors. Infrastructural roles extend to custodians holding private keys or underlying assets, requiring institutional-grade security infrastructure, insurance coverage, and segregated account structures to prevent commingling of client assets and oracle/data providers, who supply off-chain asset valuations and verification data.

But of course, institutions can and do act as investors and allocators. Pension funds, endowments, and asset managers purchase RWA tokens, demanding risk management mandates aligned with traditional investment guidelines (concentration limits, liquidity thresholds, credit quality minimums).

Ethereum Share in 2026 RWA Market

In 2026, Ethereum dominates RWA tokenization across two primary dimensions: total RWA value (share of aggregate asset value represented on-chain) and transfer volume (share of secondary market trading activity). According to RWA.xyz data, Ethereum hosts approximately 54% of total RWA value and 62% of daily transfer volume, positioning it as the primary settlement layer for institutional tokenization despite growing competition.

Ethereum’s edge is less about raw throughput and more about institutional-grade surface area:

- Liquidity Depth: The largest pools of on-chain capital exist on Ethereum, enabling RWA tokens to achieve price discovery and exit liquidity that smaller chains cannot replicate.

- DeFi Composability: Established lending protocols, automated market makers, and derivative platforms integrate seamlessly with RWA tokens, creating network effects that lock in institutional issuers.

- Infrastructure Maturity: Custody solutions, compliance tooling, and oracle networks have been battle-tested on Ethereum longer than on alternative chains, reducing operational risk for regulated entities.

- Institutional Integrations: Partnerships with traditional finance incumbents (State Street, Franklin Templeton, Siemens) concentrate on Ethereum, creating path dependency for subsequent issuers seeking similar credibility.

At the same time, competing networks take share by solving specific operational constraints: Polygon PoS hosts approximately 12% of total RWA value through partnerships with real estate tokenization platforms thanks to its carbon-neutral positioning appeal to ESG-focused asset managers, among other things. Other notable alternatives include:

- Solana: High throughput and sub-cent transaction costs enable frequent rebalancing and high-frequency trading strategies, attracting algorithmic market makers and programmatic Treasury products that represent 8% of RWA transfer volume.

- Stellar, Hedera, and XRP Ledger: Permissioned network features and built-in compliance frameworks serve institutions requiring granular transfer controls, with combined market share around 7% concentrated in cross-border payment-related RWA products.

- Arbitrum and Avalanche C-Chain: Layer-2 cost advantages and Ethereum compatibility attract issuers seeking lower operational expenses without sacrificing access to Ethereum’s DeFi ecosystem, collectively holding 11% of RWA value.

- ZKsync Era: Zero-knowledge rollup settlement and lower fees attract pilots where issuers want Ethereum security with more scalable secondary transfers for permissioned RWA tokens, particularly for high-frequency treasury management flows.

- Aptos, Algorand: Non-EVM L1 networks that periodically win niche institutional tokenization proofs-of-concept based on throughput and developer tooling, though liquidity depth and standardized DeFi integration typically lag Ethereum.

RWA Asset Types

Real World Assets tokenized on blockchain networks span six primary categories, each with its own cashflow mechanics, custody dependencies, and composability limits.

U.S. Treasuries

What is tokenized: Token holders typically receive either shares in a regulated fund that purchases U.S. Treasury securities, or debt claims backed by Treasury repos and short-term bills. The legal structure matters: fund-based products grant beneficial ownership of the underlying portfolio, while note structures create creditor claims against the issuer. Cash-equivalent tokens often represent shares in money market funds holding T-bills, creating one additional layer of abstraction from the sovereign debt itself.

Typical on-chain structure: Most implementations issue ERC-20 or similar fungible tokens on Ethereum representing fractional interests in fund shares or notes. These tokens track net asset value (NAV) computed daily based on underlying Treasury holdings, though some models attempt continuous pricing through synthetic order books.

Primary return drivers: Yield originates from Treasury coupon payments and short-term bill rollover strategies. Returns typically match or slightly trail direct Treasury rates after accounting for fund management fees, custody costs, and on-chain operational overhead. Some structures add staking rewards or protocol incentives, creating composite yields.

Liquidity reality: Primary issuance occurs through subscription windows with KYC/AML checks and accreditation requirements. Secondary trading faces friction—redemptions follow fund-specific windows (often T+1 or T+2), NAV pricing creates discontinuities versus 24/7 crypto markets, and whitelisting requirements prevent permissionless transfers. Continuous trading exists only within closed ecosystems where buyers accept delayed settlement and price discovery lag. Cutoff times for subscriptions (typically 4 PM ET to align with Treasury market hours) mean DeFi protocols cannot execute instant arbitrage when spreads emerge.

Key risks & constraints:

- NAV calculation lag creates temporary mispricing during volatile Treasury markets

- Regulatory changes to fund structures or tokenization frameworks could force redemptions

- Whitelisting requirements prevent true permissionless composability with DeFi protocols

- Operational dependencies on traditional financial infrastructure (custodians, fund administrators) introduce single points of failure

Best-fit DeFi use cases: Collateral for overcollateralized stablecoin protocols seeking yield-bearing reserves, treasury management for DAOs requiring capital preservation with modest returns, liquidity provision in stablecoin pairs where predictable NAV reduces impermanent loss risk.

Private Credit

What is tokenized: The underlying collateral typically consists of claims on SME loan portfolios, trade finance receivables, specialty finance contracts (equipment leasing, invoice factoring), or consumer credit tranches. Tokenization creates fractional interests in the cashflows these debt instruments generate, not direct claims on the borrowing entities themselves.

Typical on-chain structure: Most tokenized credit products structure as tokenized notes or fund shares with explicit waterfalls determining distribution priority. Senior tranches receive first claim on principal and interest payments, junior tranches absorb initial losses but capture excess spread, and first-loss capital (often retained by the originator) provides overcollateralization buffers. A typical structure might feature 70% senior notes, 20% junior notes, and 10% first-loss equity, with overcollateralization ratios of 120-150% protecting senior holders.

Primary return drivers: Interest spread between what borrowers pay and what the fund costs to operate drives returns. Senior tranches typically target 6-10% yields, junior tranches 12-18%, and equity 20%+ depending on portfolio risk. Yield sustainability depends entirely on loan performance and default rates staying within underwritten assumptions.

Liquidity reality: Primary issuance follows traditional private credit fundraising—due diligence periods, capital calls, and lock-up commitments. Secondary trading remains limited due to investor accreditation requirements, transfer restrictions in fund documents, and the need for buyers to undergo full KYC. Most structures impose 12-24 month lock-ups with quarterly redemption windows subject to liquidity gates.

Key risks & constraints:

- Servicer performance directly affects collection efficiency and default management outcomes

- Reporting cadence (typically monthly or quarterly) creates information asymmetry versus real-time DeFi data

- Borrower concentration risk—single large default can disproportionately impact small portfolios

- Legal enforceability of claims varies by jurisdiction, affecting recovery rates in default scenarios

Best-fit DeFi use cases: Yield optimization vaults seeking uncorrelated returns to crypto-native assets, collateral for stablecoin protocols requiring diversified backing beyond crypto volatility, structured products offering differentiated risk/return profiles for sophisticated LPs.

Real Estate

What is tokenized: Real estate tokenization splits into two core paths—equity-like structures tokenize ownership interests in special purpose vehicles (SPVs) or funds that hold property titles, while debt-like structures tokenize mortgage notes, bridge loans, or mezzanine financing.

Equity tokenization grants holders fractional ownership in properties through SPV shares, entitling them to rental income distributions and appreciation upon sale. Debt tokenization creates claims on interest payments from real estate-backed loans, with the property serving as collateral but ownership remaining with the borrower.

Typical on-chain structure: Equity tokens typically implement ERC-20 standards representing membership units in LLCs or similar entities holding property deeds. Debt structures issue notes as tokens with embedded terms for interest payment schedules, maturity dates, and foreclosure triggers.

Primary return drivers: Equity structures generate returns through rental yields (typically 4-8% net after property management costs) plus property appreciation upon exit events (sales or refinancing). Geographic location, property class (multifamily, office, retail, industrial), and management quality drive performance variance significantly. Debt structures produce predictable coupon payments (8-15% for bridge loans, 5-8% for senior mortgages) with principal repayment at maturity, but offer no upside exposure to property value increases.

Liquidity reality: Both structures are illiquid. Equity tokens can only transfer among accredited investors passing issuer KYC processes, and finding buyers requires either secondary platforms or bilateral negotiation. Property sales that enable redemptions occur on multi-year timelines dictated by market conditions and fund lifecycle. Debt tokens offer slightly better liquidity since they mature at predetermined dates, but early exit still requires secondary buyers willing to accept yield and credit risk.

Valuation frequency: Properties receive appraisals quarterly or semi-annually at best, creating long gaps where token valuations rely on stale data. Unlike securities with continuous pricing, real estate tokens fluctuate based on assumptions rather than market discovery, making real-time collateralization calculations unreliable. Liquidation mechanics suffer accordingly—forced sales during defaults often realize 20-40% discounts to appraised values due to urgency and market illiquidity.

Key risks & constraints:

- Property-level risks (tenant defaults, maintenance costs, environmental liabilities) directly impact token value

- Geographic concentration—local market downturns can devastate portfolio values

- Leverage at property or fund level amplifies losses during price declines

- Exit timing uncertainty—forced sales in down markets destroy value

Best-fit DeFi use cases: Long-term collateral for lending protocols with patient capital, real estate-focused index products offering diversified property exposure, treasury diversification for protocols seeking inflation-hedged reserves.

Commodities

What is tokenized: The key split is allocated physical commodity backing versus unallocated or derivative exposure. Allocated gold tokens grant claims on specific, segregated bullion bars held in vaults, with serial numbers recorded on-chain linking tokens to physical metal. Unallocated structures pool holdings, giving token holders a claim on the issuer’s general commodity inventory without specific bar assignment. Derivative structures don’t involve physical commodities at all—they track price exposure through futures, swaps, or other financial instruments.

Typical on-chain structure: Physical-backed tokens typically use ERC-20 implementations where each token represents a fixed weight unit (e.g., one gram of gold, one barrel of oil equivalent). Warehouse receipts or custody certificates are digitized and mapped to token IDs, creating verifiable links between on-chain records and off-chain physical assets.

Primary return drivers: Commodities themselves generate no cashflow—they’re non-productive assets. Returns derive entirely from price appreciation (or depreciation). Some tokenized commodity products add yield by lending physical holdings to industrial users or deploying financial strategies like covered call writing, but the underlying commodity remains yield-free.

Liquidity reality: Token trading can occur 24/7 on decentralized exchanges, but that can create price discovery disconnected from commodity spot markets that operate on specific hours. True arbitrage requires physical redemption capability, which introduces significant friction.

Key risks & constraints:

- Custodian counterparty risk—tokens become worthless if physical backing disappears

- Audit frequency and quality directly affect confidence in backing ratios

- Storage costs and insurance fees reduce net returns versus spot commodity exposure

- Cross-border legal complications affect ownership clarity during disputes

Best-fit DeFi use cases: Inflation hedges within crypto portfolios seeking non-correlated assets, collateral for stablecoins requiring commodity backing diversity, synthetic commodity exposure products enabling leverage or options strategies.

Art and Collectibles

What is tokenized: Fractional ownership in individual artworks, vintage cars, rare wines, or other unique collectibles through SPVs or trust structures that hold legal title. Unlike fungible commodities, each asset has distinct characteristics making valuation subjective and contentious.

Typical on-chain structure: ERC-20 tokens representing fractional beneficial ownership in the SPV, or ERC-721 NFTs representing whole-asset ownership that gets fractionalized through smart contracts. Governance rights regarding insurance, storage location, loan-out decisions, and eventual sale typically attach to tokens based on ownership percentage thresholds.

Primary return drivers: Appreciation in collector markets drives returns, as art and collectibles generate no cashflows. Some structures add revenue by loaning pieces to museums or exhibitions, licensing images, or offering fractional owners visitation rights, but these remain secondary to price appreciation.

Key risks & constraints:

- Authentication failures can emerge years after tokenization, destroying value instantly

- Illiquidity far exceeds traditional real estate—finding buyers for fractional rare collectible interests is exceptionally difficult

- Storage and insurance costs compound over holding periods, eroding net returns

- Legal frameworks for fractional collectible ownership remain underdeveloped in most jurisdictions

Best-fit DeFi use cases: Extremely limited—mostly novelty governance experiments or speculative trading among collectors.

Securities

What is tokenized: Traditional securities (stocks, bonds, fund shares) can be tokenized by representing ownership on distributed ledgers instead of centralized securities depositories. Tokenized securities as regulated instruments mean newly-issued equity or debt complying with securities laws but using blockchain infrastructure for issuance, trading, and settlement. Synthetic price exposure tokens avoid security classification by creating derivative claims tracking asset prices without granting ownership rights or legal claims.

Typical on-chain structure: Tokenized securities typically deploy permissioned blockchain architectures where transfer validation occurs before settlement. Smart contracts enforce transfer restrictions (holding period locks, investor accreditation checks, jurisdiction blocks) and automatically distribute dividends, interest payments, or corporate action proceeds. Security token standards like ERC-1400 add compliance capabilities beyond basic ERC-20 functionality.

Primary return drivers: Dividends, interest coupons, and capital appreciation mirror traditional securities. Tokenization itself doesn’t change cashflow economics—a tokenized bond pays the same coupon as a traditional bond with identical terms.

Liquidity reality: Secondary trading is constrained by transfer restrictions embedded in security documentation. Regulated marketplace requirements mean security tokens can only trade on Alternative Trading Systems (ATS) or registered exchanges that enforce compliance checks.

Key risks & constraints:

- Regulatory classification uncertainty—tokens designed as non-securities may be reclassified

- Limited secondary market liquidity due to transfer restrictions and marketplace fragmentation

- Custodial complexity—security tokens require qualified custodians meeting financial services regulations

- Cross-border complications—securities laws vary by jurisdiction

Best-fit DeFi use cases: Minimal integration with permissionless DeFi due to compliance incompatibilities; mostly confined to regulated walled gardens.

How RWA Tokenization Works

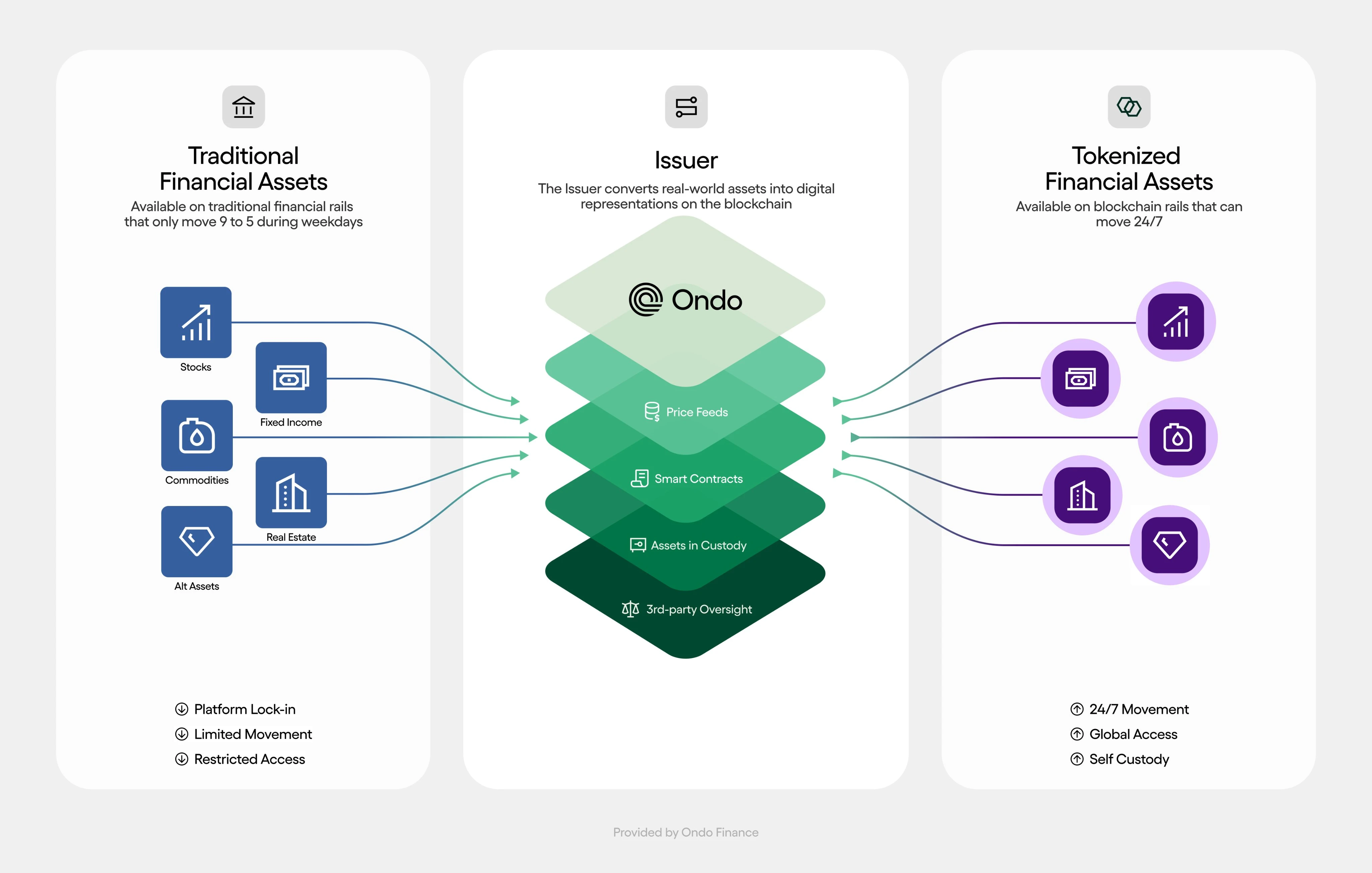

On a high level, RWA tokenization converts ownership rights in physical or financial assets into digital tokens that exist on blockchain infrastructure. The process bridges traditional asset custody, legal frameworks, and blockchain-based settlement systems through a structured lifecycle that involves issuers, custodians, administrators, and technology operators. Once you understand each stage—from on-chain representation to legal record updates—you’ll see exactly where efficiency comes from, and where the failure points hide.

On-Chain Representation

On-chain representation defines how the token relates to the underlying asset both legally and operationally. The token can function as a claim or receipt that references off-chain records, or as the native record of title where blockchain entries constitute legal proof of ownership. In a claim model, the token holder possesses rights against a custodian or issuer who controls the underlying asset; legal ownership remains tied to traditional registers. In a native title model, the token itself represents ownership, and the blockchain state determines who holds enforceable rights—a structure rarely achieved outside of digital-native assets due to regulatory and legal constraints.

Fungible tokens (ERC-20 on Ethereum, SPL tokens on Solana) represent fractional, interchangeable shares in asset pools like real estate funds or Treasury portfolios, where each token unit carries identical rights. Non-fungible tokens (ERC-721, ERC-1155 on Ethereum, Polygon, or Arbitrum) represent discrete, unique assets—individual properties, fine art pieces, or specific loan agreements—where each token carries distinct metadata, valuation, and ownership history. Permissioned transfer constraints differentiate most tokenized security structures from open cryptocurrencies: whitelists restrict transfers to KYC-verified investors in regulated marketplace environments, transfer agents enforce lock-up periods, and smart contract-level freeze or burn functions allow issuers to respond to regulatory demands or covenant breaches. Permissionless transfers, while technically possible, conflict with securities laws in most jurisdictions and remain rare outside of stablecoin structures.

Oracle dependency arises when on-chain logic requires off-chain data. If a token’s value or redemption rights depend on NAV calculations, interest accruals, or asset appraisals, an oracle or administrator must feed that data onto the blockchain technology stack. Tokens representing fixed-income instruments or real estate funds rely heavily on oracle inputs; equity-like tokens with static cap tables may not.

Common architectures:

- Fully on-chain transfer with permissioning: Tokens execute transfers directly on Ethereum, Avalanche C-Chain, or Polygon with smart contract-enforced whitelist checks and transfer restrictions. Operationally, this maximizes transparency and composability but requires continuous oracle feeds for complex financial instrument logic.

- Wrapper token representing shares in an off-chain vehicle: The token functions as a digital certificate for shares held in a traditional SPV, trust, or fund. Asset tokenization occurs at the share level, not the underlying asset level. Operationally, this minimizes legal complexity but creates reconciliation dependencies between on-chain balances and off-chain registries.

- Marketplace-issued tokens with transfer-agent style controls: A regulated marketplace or platform issues tokens and maintains the authoritative cap table off-chain, using blockchain primarily for settlement and custody. Transfers require platform approval. Operationally, this mirrors traditional securities infrastructure while leveraging blockchain for faster settlement.

Issuance

Issuance follows a gated, multi-step workflow that synchronizes legal structuring, investor eligibility, and token minting:

- Asset Sourcing: The originator (real estate developer, fund manager, corporate treasurer) identifies and acquires the underlying asset: property title, loan portfolio, commodity reserves, or securities holdings.

- Legal Structuring: The asset transfers into a bankruptcy-remote SPV, trust, or regulated fund vehicle designed to isolate the asset from the issuer’s balance sheet and satisfy securities law requirements.

- Onboarding and KYC Gates: Prospective investors complete identity verification, accreditation checks, and jurisdiction-specific compliance screens through the issuer’s platform or a third-party administrator.

- Minting: Once subscription funds clear and eligibility is confirmed, the issuer or designated smart contract operator mints tokens and assigns them to the investor’s whitelisted wallet address.

- Initial Allocation and Distribution: Tokens transfer to investors’ self-custody wallets or qualified custodian accounts, and the cap table or holder registry updates to reflect ownership.

Primary actors: The SPV or originator structures the asset; the issuer (often the SPV itself or a platform operator) executes minting; the transfer agent or administrator manages investor onboarding, compliance screening, and cap table updates; broker-dealers may facilitate distribution in certain securities offerings.

On-chain, minting functions create new token supply at specified addresses, constrained by token standard rules (ERC-20 for fungible shares, ERC-721/ERC-1155 for unique assets). Smart contracts enforce permissions—only addresses with minter roles can create tokens. Transfer rules activate immediately: newly minted tokens inherit whitelist requirements, lock-up periods, and transfer restrictions encoded in the contract.

Off-chain, subscription agreements, purchase confirmations, and custody account setup occur through traditional legal and banking channels. The issuer’s treasury receives fiat payments or confirms stablecoin settlement before triggering on-chain minting. The transfer agent records beneficial ownership in a parallel registry that serves as the legal system of record in most jurisdictions.

Minting triggers vary by structure. In subscription-based models, minting occurs only after fiat cash clears settlement accounts; in asset-backed structures, minting follows confirmation of asset purchase or deposit into custody. Supply elasticity depends on the asset type: open-ended funds allow continuous issuance as subscriptions arrive, while fixed-supply structures (tokenized bond issuances, closed-end real estate trusts) mint once and prohibit further creation.

Manual vs. automated minting: High-value or complex assets often require multi-signature approval from the issuer, legal counsel, and auditor before tokens are created. Automated minting through smart contracts is feasible only when subscription payments arrive via stablecoins or blockchain rails and compliance checks integrate programmatically with the minting function.

Primary failure modes:

- If subscription funds fail to clear after mint intent (payment reversal, sanctions hit, bank reject), the issuer must either hold the tokens in escrow until re-payment or burn them and reverse the allocation.

- Minting to non-whitelisted addresses due to operational error creates tokens that cannot legally transfer, requiring manual burn and re-mint.

- Insufficient multi-sig coordination delays minting beyond investor subscription deadlines, creating regulatory or contractual breaches.

Evidence and audit artifacts: Minting events are permanently recorded on-chain with transaction hashes and timestamps. Off-chain, the issuer maintains subscription documents, payment confirmations, compliance reports, and audited cap tables. Third-party administrators may issue attestation letters confirming the reconciliation between on-chain supply and subscribed capital.

Custody

Custody, or responsibility over storage and management, in RWA tokenization spans three distinct layers, each with separate service providers and risk profiles:

- Custody of the Underlying Asset: Banks, prime brokers, or specialized custodians (e.g., institutional real estate trustees) hold physical title, securities accounts, or commodity reserves. The custodian’s role is governed by custody agreements that specify segregation, audit rights, and claim priority in insolvency.

- Custody of Token Holder Keys: Investors choose self-custody (controlling private keys directly) or qualified custodian solutions (Fireblocks, Anchorage, BitGo) that provide institutional-grade key management, insurance, and regulatory reporting. For institutional investors, qualified custody is often mandatory under fiduciary standards.

- Custody and Administration of Cap Table or Holder Registry: When tokens are transfer-restricted, a transfer agent or administrator maintains the authoritative registry of eligible holders, maps wallet addresses to legal identities, and enforces transfer rules. This registry reconciles on-chain balances with off-chain compliance records.

What happens on-chain: Token balances reside in wallet addresses controlled by private keys. Smart contracts may implement emergency pause or freeze functions that prevent transfers from specific addresses. Whitelist contracts check holder eligibility before allowing transfers. On-chain activity is transparent and auditable via block explorers.

What happens off-chain: Custody agreements define legal ownership, liability, and operational controls for the underlying asset. Key management systems (HSMs, multi-party computation) secure private keys within qualified custodian infrastructure. The transfer agent maintains a legal registry that reconciles wallet addresses with investor identities, tracks beneficial ownership for regulatory reporting, and manages corporate actions.

Custody control checklist:

- Are underlying assets held in separate accounts or commingled with issuer or custodian assets?

- Does the legal structure shield token holders from issuer insolvency, and does the custodian provide claim priority?

- Are third-party audits or attestations conducted quarterly, annually, or ad-hoc, and are reserve proofs published?

- Who holds authority to pause transfers, freeze wallets, or burn tokens in response to regulatory orders, fraud, or sanctions? Are these powers exercised through multi-signature governance or centralized admin keys?

Primary failure modes:

- Custodian insolvency or fraud places underlying assets at risk despite valid token holdings.

- Loss of private keys in self-custody eliminates access to tokens; qualified custodian failures (hack, operational error) similarly strand assets.

- Misalignment between on-chain token balances and off-chain cap table records creates legal disputes over beneficial ownership.

Redemption

Redemption converts tokens back into underlying value through one of two primary paths, each with distinct mechanics and gating conditions:

(a) Token Burn for Off-Chain Cash Payout. The investor initiates redemption by sending tokens to a designated burn address or smart contract. The issuer or administrator verifies eligibility (minimum holding period, redemption window compliance, whitelist status), calculates the payout (NAV, spot price, or contractual formula), and initiates a fiat transfer to the investor’s linked bank account or stablecoin payment to their wallet. The token supply decreases by the burned amount.

(b) Token Burn for Delivery or Transfer of the Underlying Asset. Where applicable (fractional real estate, commodity-backed tokens, NFT-wrapped physical assets), the investor redeems tokens in exchange for title transfer or physical delivery of the underlying asset. This path requires legal documentation (deed transfer, bill of sale) and coordination with custodians or originators. Minimum redemption sizes often apply to make the operational burden economical.

What happens on-chain: Tokens are sent to a burn address or a smart contract that locks and destroys them, reducing total supply. The redemption transaction is recorded permanently on-chain. Smart contracts may automate eligibility checks (holding period, minimum balance) and trigger stablecoin payouts atomically.

What happens off-chain: The administrator confirms the redemption request against compliance records, initiates fiat wire transfers through banking partners, and coordinates with custodians for asset delivery when applicable. Legal documentation is executed for title transfers. The transfer agent removes the redeemed tokens from the cap table and updates beneficial ownership records.

Primary failure modes:

- If the underlying asset lacks liquidity (illiquid real estate, distressed debt), the issuer cannot fulfill redemptions without selling the asset—potentially at a loss.

- Sanctions against the investor’s jurisdiction or entity post-redemption request create legal holds.

- Transfer restrictions triggered by covenant breaches can freeze redemptions until the breach is cured. Tokens remain valid but non-redeemable, creating a secondary market discount or forcing distressed sales.

Settlement

Settlement in RWAs is layered, and it’s rarely “instant” end-to-end. The token leg can finalize in seconds, while the cash leg and legal record can lag behind.

- On-Chain Token Transfer Finality

Once a transaction is confirmed on Ethereum, Polygon, or Avalanche C-Chain, the token transfer is cryptographically final and irreversible. Block times range from seconds (Solana, Arbitrum) to minutes (Ethereum during congestion). This layer achieves immediate settlement of the token leg. - Off-Chain Cash Leg and Reconciliation

When payment occurs via bank wire or ACH, settlement depends on banking hours, correspondent bank intermediaries, and manual reconciliation by the issuer’s treasury or administrator. Stablecoin payments (USDC, USDT) settle near-instantly on-chain but require issuer redemption into fiat if the underlying asset or obligations are denominated in dollars. Reconciliation—matching on-chain token transfers with off-chain cash receipts—remains manual or semi-automated and prone to timing mismatches. - Final Legal Settlement and Record Updates

The transfer agent or administrator updates the cap table, shareholder registry, or beneficial ownership records to reflect the new holder. In jurisdictions requiring notarized documentation or regulatory filings (real estate, certain securities), this step can lag days or weeks behind on-chain settlement. Only after this step does the buyer possess enforceable legal rights against the issuer or underlying asset.

Primary failure modes:

- Timing mismatch between on-chain token transfer and off-chain cash settlement creates delivery-versus-payment risk.

- Banking intermediaries reject or delay transfers due to compliance holds, incorrect routing, or sanctions screening.

- Reconciliation errors—mismatched wallet addresses, duplicate payments, incorrect amounts—require manual investigation and correction.

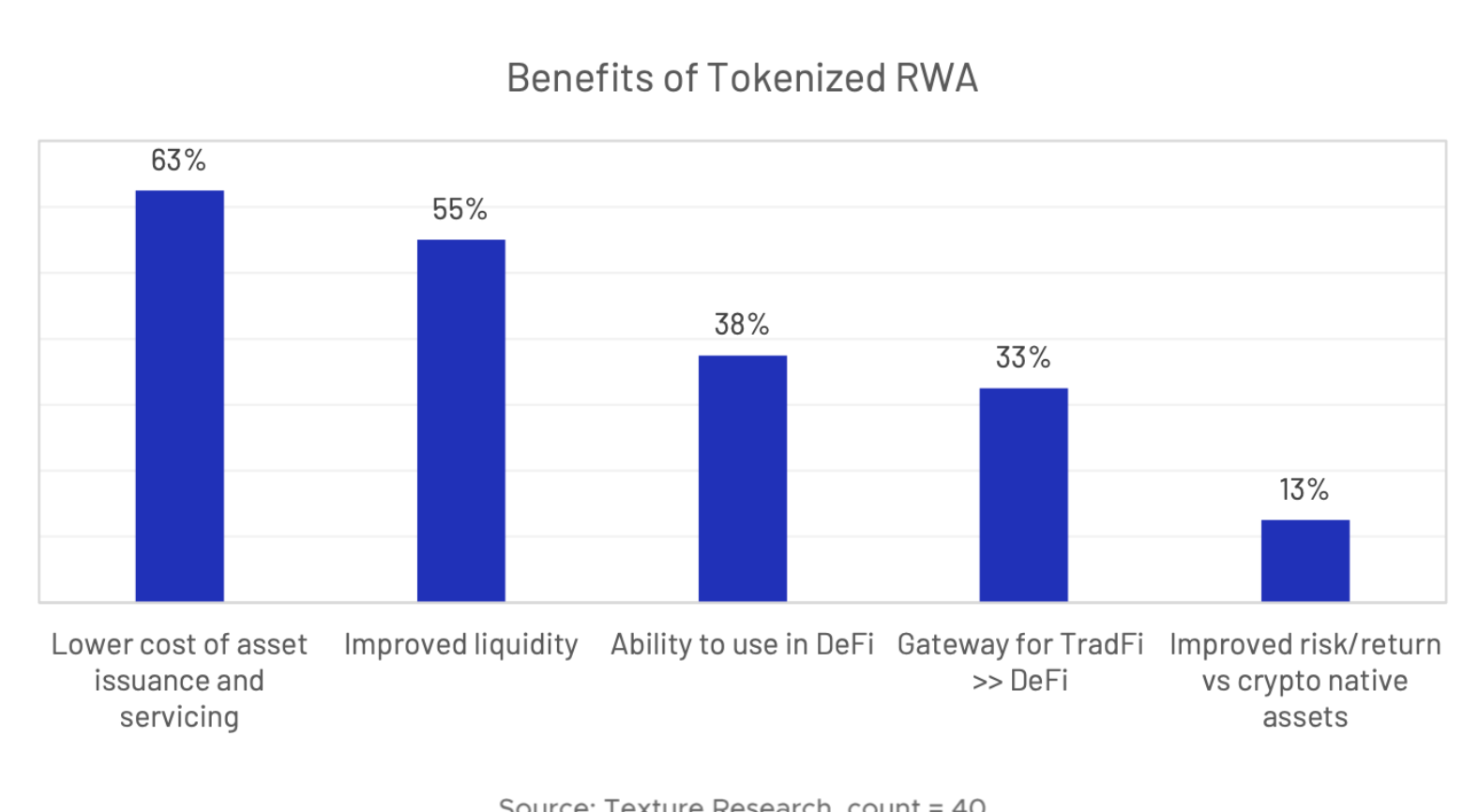

Main Benefits of RWA Crypto

Tokenization can offer real efficiencies, but the payoff depends heavily on the asset type and whether the market is permissionless or permissioned.

Liquidity

Liquidity in tokenized RWAs operates on two distinct levels: On-chain liquidity translates to how easily the token wrapper can be traded on secondary markets. Underlying liquidity, in turn, means whether the real-world asset can be redeemed or liquidated fast enough to support that token price.

Several levers decide whether liquidity improves in practice:

- Standardized token terms for cross-platform compatibility

- Continuous quoting by market makers

- Permissioning and KYC constraints that may increase institutional participation but fragment liquidity

- Redemption mechanisms that anchor price to intrinsic value

- Use as collateral in decentralized finance lending protocols

Tokenization can also create illusory liquidity. If redemption is quarterly, whitelists are narrow, or issuer discretion is high, “24/7 trading” can vanish exactly when you need it most.

Fractional Ownership

For clarity’s sake, fractional ownership usually means fractional economic exposure, not fractional legal title. ERC-20 decimals make it easy to divide exposure, but legal and operational constraints still impose minimums and transfer rules.

Fractionalization is most useful for high-ticket assets where traditional minimums are six figures; diversified baskets that bundle assets into a single tokenized security; alternatively, cross-border participation where blockchain rails reduce distribution friction.

That being said, it adds complexity when servicing overhead is heavy, governance is messy, or the underlying instrument requires strict consent rules.

Market Access

Tokenization changes access across:

- Geography: broader reach, until KYC/AML and jurisdiction blocks reintroduce borders

- Time: 24/7 transferability, even if redemption still depends on business hours

- Product: smaller minimums for traditionally gated assets

The tricky part is that permissioned access can both widen and narrow investors’ reach. It can make institutional participation possible, while still excluding most retail buyers by design.

Settlement Efficiency

Tokenization can reduce settlement friction through:

- Programmable settlement logic (including delivery-versus-payment in fully on-chain flows)

- Reduced reconciliation burden by using a shared ledger

- Fewer intermediaries in the settlement chain

- Automated corporate actions (interest, dividends, redemptions)

- Improved audit trails for compliance and forensics

The ceiling is still set by off-chain legs: banking hours, custodian operations, and legal record updates often dominate real-world settlement time.

Transparency

On-chain transparency is strong for token balances, transfers, and supply. Off-chain transparency depends on disclosures, audits, and attestation design.

Meaningful transparency usually requires:

- Proof of reserves and attestations

- Asset registers and collateral detail

- Valuation methodology clarity

- Delinquency and impairment metrics for credit products

- Redemption terms that are explicit and enforceable

- Smart contract addresses and audit reports

Permissioned chains can reduce transparency, and “on-chain activity” alone can become a transparency illusion if collateral reporting is weak.

Cost Structure

Tokenization shifts costs rather than eliminating them. You may see lower settlement and reconciliation costs, but higher legal, compliance, oracle, and smart contract audit costs. Smart contract audits can run $50,000-$200,000+ per engagement, and continuous compliance monitoring adds ongoing overhead.

Who captures savings matters. In early markets, issuers may retain efficiency gains rather than pass them through to token holders, especially when competition is limited.

Top RWA Crypto Protocols and Tokens

To help you navigate this expanding landscape, we’ve developed a consistent evaluation framework that applies across every protocol reviewed below:

- RWA Primitive/Type Supported – What real-world exposure does the protocol enable? (treasuries, corporate credit, real estate, commodities, infrastructure data)

- Product Surface – Does the platform focus on issuance (creating tokenized securities), marketplace functions (trading/discovery), or lending (collateralized credit)?

- Compliance & KYC Posture – Are operations permissioned (whitelist-only), permissionless (open access), or hybrid? What verification layers exist?

- Collateral Quality & Verification Method – How is underlying asset quality assured? (third-party audits, on-chain proof, custodian attestations, oracle feeds)

- Liquidity & Redemption Mechanics – Can tokens be redeemed for underlying assets? What are withdrawal timeframes and liquidity depth?

- Smart Contract/Oracle Dependencies – Which chains host the protocol? What oracle infrastructure ensures off-chain data integrity?

- Chain/Network Coverage – Single-chain or multi-chain deployment?

- Primary Risks – Top two risk vectors tied to asset tokenization challenges

| Protocol | RWA Type | Product Surface | Compliance Model | Collateral Verification | Liquidity | Chain Coverage | Primary Risks |

|---|---|---|---|---|---|---|---|

| Chainlink | Oracle infra | Data feeds | Permissionless | Decentralized oracle network | N/A (infrastructure) | Multi-chain | Oracle manipulation, data source quality |

| Ondo Finance | Tokenized treasuries | Issuance + marketplace | Permissioned (KYC) | Third-party audits, custodian attestation | Medium (institutional LPs) | Ethereum, Polygon, Solana | Legal enforceability, custodian counterparty |

| XDC Network | Trade finance, settlement | Infrastructure layer | Hybrid (permissioned nodes) | Notary/validator consensus | High (network native) | XDC mainnet | Network adoption risk, validator centralization |

| Quant | Interoperability | Cross-chain messaging | Permissionless | Multi-ledger attestation | N/A (infrastructure) | Multi-chain (via Overledger) | Interop protocol risk, licensing model |

| Maple Finance | Corporate credit | Lending pools | Permissioned (accredited) | Credit assessment by pool delegates | Low-Medium (lockup periods) | Ethereum, Solana | Credit default, delegate diligence |

| Pendle | Yield tokenization | Trading (yield derivatives) | Permissionless | Smart contract logic | Medium-High (AMM pools) | Ethereum, Arbitrum, Polygon | Smart contract complexity, impermanent loss |

| Centrifuge | Diversified credit | Issuance + lending | Hybrid (issuer verification) | Asset originators + on-chain data | Low (RWA illiquidity) | Ethereum (Centrifuge Chain bridge) | Asset underwriting quality, bridge risk |

| MANTRA | Regulated marketplace | Issuance + marketplace | Permissioned (regulated) | Regulatory compliance framework | Medium (regulated venue) | MANTRA Chain (Cosmos SDK) | Regulatory jurisdiction, platform adoption |

| TrueFi | Uncollateralized credit | Lending pools | Permissioned (credit assessment) | Credit model + staking | Medium (portfolio liquidity) | Ethereum, Optimism | Unsecured default, credit model accuracy |

Key Considerations, Risks, and Drawbacks

Unlike native crypto assets where the token is the asset, RWA crypto depends on legal enforceability, operational counterparties, smart contract correctness, and oracle data integrity, among other risks in the stack.

To safeguard against potential legal action against the tokenized asset of your choice, before committing, verify its security status, offering exemption posture, transfer restrictions, KYC/AML enforcement points, and marketplace type. These are not abstract; they directly determine whether you can hold, transfer, and exit.

Remember, the token is not the claim—the legal agreement is. Identify the issuer/SPV, locate the governing agreement, confirm your capital stack position, and understand insolvency outcomes. The issuer, custodian, originator/servicer, trustee, market makers, and oracle providers can break your redemption or cashflow path.

Separate custody of the off-chain asset from custody of the on-chain token. Also watch for mismatched settlement cycles where a token burns before fiat payout finalizes. Moreover, smart contract risks and its components: upgradeability, admin keys, permissioning logic, mint/burn/redeem correctness, and DeFi integration behavior—all matter. Look for audits, bug bounties, timelocks, and clear emergency procedures.

Where applicable, and RWA crypto mostly falls into this category, oracle correctness is not the same as oracle uptime. Check multi-source aggregation, update frequency, fallback procedures, and on-chain provenance logging.

Finally, measure bid-ask spread, depth, transfer volume, redemption gates, minimum sizes, and whether liquidity is incentive-dependent. Also remember the liquidity-legal interaction: a willing buyer who cannot pass whitelisting is not a buyer in practice.

Conclusion

RWA crypto enables institutional-grade assets—U.S. Treasuries, private credit, real estate, commodities—to circulate on blockchain rails with programmable liquidity and fractional ownership. For this model to deliver real value (and not just a token wrapper), three conditions must hold: legal enforceability of the underlying rights, compliant issuance and custody structures, and reliable redemption mechanisms.

More crypto projects and categories are covered in detail in ChangeHero blog. For bite-sized content and updates, feel free to follow our pages on social media: X, Facebook, and Telegram.

Frequently Asked Questions

What exactly qualifies as RWA crypto?

RWA crypto refers to blockchain tokens that represent legal claims on or economic exposure to real-world assets—such as Treasury bills, corporate bonds, real estate equity, or commodities—rather than purely digital assets like Bitcoin. These tokens bridge traditional finance and blockchain infrastructure by tokenizing ownership rights, yield streams, or fractional interests in physical or financial assets.

How is RWA crypto different from protocol governance tokens or stablecoins?

Tokenized RWAs represent economic exposure to specific underlying assets. Governance tokens derive value from platform usage and governance rights. Stablecoins are RWA-adjacent: backed by reserves, but designed for price stability rather than yield generation.

Does owning an RWA token mean I own the underlying asset itself?

Usually, no. In most cases you own a claim, not the asset directly. The enforceability of that claim depends on the legal structure, custody, and redemption process.

Is RWA crypto the same as tokenized security?

Often, but not always. Many RWAs are securities; some may be commodities or other non-security structures depending on design.

What is the difference between "on-chain representation" and the actual off-chain asset?

The token lives on-chain; the asset remains off-chain. Redemption works only if issuer processing, KYC/whitelisting, and the legal wrapper all align.

Can I transfer my RWA tokens freely to anyone like I can with Bitcoin?

Not usually. Whitelists, lockups, and regulated venue requirements often restrict transfers.

How big could asset tokenization realistically get?

A BCG forecast cited by industry reports projects $16 trillion by 2030, but the 2026 market is still in the billions. Track current market data via platforms like RWA.xyz.

What are the key risks specific to RWA crypto to watch for?

Counterparty risk, regulatory risk, smart contract risk, oracle risk, and liquidity risk—often compounding together.

What does a "tokenized Treasury" token actually represent?

Typically, a fractional claim on U.S. Treasury bills or notes held in custody via an SPV/trust structure, with yield distributed via rebasing, NAV appreciation, or stablecoin payouts.

What operational constraints do buyers typically hit with tokenized Treasuries?

Whitelisting/KYC, transfer restrictions, redemption windows, and minimum investment thresholds.

Are tokenized Treasury products true "cash equivalents" like money market funds?

Sometimes, with caveats: redemption friction, thin liquidity, and wrapper risk can break cash-equivalent behavior under stress.

Are tokenized Treasuries "risk-free" because they are backed by U.S. government debt?

No. The underlying credit risk may be minimal, but the wrapper introduces issuer, custodian, smart contract, and chain risks.

What is the difference between senior and junior exposure in tokenized private credit?

Senior has first claim and lower yield; junior absorbs first losses and targets higher yield.

What happens if the borrower defaults on a tokenized private credit loan?

A servicer enforces the loan. Recoveries depend on collateral, jurisdiction, and servicing quality, and can take months or years.

Can I redeem my private credit tokens anytime like a savings account?

No. Private credit is inherently illiquid; assume lockups until maturity unless a real secondary market exists.

Do I own the asset or a claim on the asset when I hold an RWA token?

You own a claim on the asset, not the asset itself. The structure defines how strong that claim is, and what you can enforce in stress.