Best Crypto Swap Aggregator 2026: Review & Guide

Key Takeaways

- 🧭 A crypto swap aggregator is a service powered by router smart contracts that compose the optimal swap paths through supported liquidity sources that may include DEXs, AMMs, cross-chain bridges, and solvers

- 🧭 Crypto swap aggregators cover a large ground, which makes some of them better optimized for single-chain ecosystems and others for specific use cases like stablecoin swaps

- 🧭 The shortlist of swap aggregators reviewed by the ChangeHero team is: Rubic, 1inch, LI.FI, Jupiter, ODOS, Velora, CoWSwap, and Cetus.

Not financial advice. On-chain execution is irreversible; always verify token contract addresses and approval scopes before confirming a transaction. Quotes displayed by any aggregator can shift between preview and execution due to MEV, price impact, and gas fee volatility.

Where should a DeFi user go for a chain-agnostic experience? “Swap aggregator” in our review means a non-custodial routing layer that queries multiple DEX liquidity sources to find an optimal execution path for a token swap. This is distinct from: (a) a DEX aggregator limited to same-chain DEX routing only, (b) a bridge aggregator focused solely on cross-chain asset transfers, and (c) custodial instant-exchange brokers that hold funds during the process.

Similarly, “best” is not a fixed label here: because liquidity source depth and routing quality vary significantly by network, the guide pairs per-aggregator strengths with scenario-based recommendations covering large trades, stablecoin swaps, cross-chain rebalancing, limit orders, and gasless execution.

Overview: What a Crypto Swap Aggregator Is

Definition

A crypto swap aggregator finds and executes the best token swap route across multiple liquidity sources, comparing quotes from decentralized exchanges, AMMs, order books, and solvers in real time to maximize the output token amount a user receives after accounting for gas fees and slippage.

How does a crypto swap aggregator do that? It queries multiple liquidity sources simultaneously and selects the optimal route based on exchange rate, gas fee cost, and execution failure risk. It then executes the swap on-chain via smart contracts or solvers, remaining non-custodial throughout—the aggregator never holds your funds. Sometimes, when a centralized service that sources liquidity from the best crypto exchanges is involved, if a KYC/AML check is triggered, the funds may get caught in temporary custody; however, this does not happen on the swap aggregator’s side and the service will warn the user.

Such an aggregator does not set the market price (price is determined by the underlying liquidity venues), doesn't eliminate network gas costs, and doesn't guarantee that the quoted price matches the final execution price.

When availing one, a user provides the input token, desired output token, and the amount. Aggregator queries connected liquidity venues and returns competing quotes, and selects the best route based on its objective function: price + gas + failure risk. The swap executes via smart contracts or solvers directly on-chain.

DEX Aggregator vs Swap Aggregator

The terms are often used interchangeably, but they describe meaningfully different tool categories that may or may not avail of a crypto bridge or swap in the process. If you don’t separate them, you end up comparing apples to oranges — and then blaming the wrong thing when execution deviates from the preview quote.

| Dimension | DEX Aggregator | Swap Aggregator (broader) |

|---|---|---|

| Typical venues | AMMs, on-chain order books, solvers | May also include CEX-style instant swap providers and off-chain quote systems |

| Custody model | Non-custodial; settlement fully on-chain | May involve a briefly custodial or semi-custodial leg depending on provider |

| Pricing transparency | Fully transparent; route and price impact visible on-chain | Quote may be opaque if sourced from a private off-chain provider |

| Settlement | On-chain only; transaction is verifiable and reversible only before signing | May involve off-chain legs; settlement confirmation can be delayed |

| Common failure modes | Transaction revert, slippage exceeded, insufficient liquidity in route | Provider timeout, quote expiry before signing, or silent rate degradation |

Not all crypto swap aggregators operate within a single blockchain:

- (a) Same-chain DEX aggregation: The aggregator sources liquidity entirely within one blockchain. Route optimization, gas fee minimization, and slippage management all occur in a single execution environment.

- (b) Cross-chain swap aggregation: The aggregator composes a cross-chain swap by combining a bridge with a destination-chain swap in a single user flow. Example route format: TokenA on Chain1 → Bridge → TokenB on Chain2. The user interacts once, but the execution involves at least two separate on-chain transactions and introduces bridge-specific failure modes.

- (c) Bridge-only tool: Moves the same token across chains without performing a swap. There is no route optimization and no exchange rate applied at the destination.

When to use which:

- Same-chain DEX aggregator: Best when your goal is price optimization on a single chain and you want full on-chain transparency of the route and price impact

- Cross-chain swap aggregator: Best when you need to rebalance assets across chains in a single operation and are willing to accept bridge latency and additional smart contract risk

- Fixed-rate or instant swap provider: Best when predictability and speed matter more than achieving the absolute best exchange rate, and you accept that pricing transparency may be limited

How Crypto Swap Aggregators Work

Routing and Pathfinding

When you submit a swap request, a DEX aggregator kicks off a route construction sequence before a single transaction is signed. The aggregator ingests a fixed set of inputs: the source chain, the input token, the output token, the trade amount, the connected wallet address, allowed slippage tolerance, gas settings (speed preference or a custom gas price), and any user-defined restrictions such as "avoid bridges," "single-hop only," or "exclude specific protocols." Those inputs become the constraints every candidate route must satisfy.

Same-chain routing keeps every leg on one network. The aggregator queries pools, vaults, and order books that share the same EVM (or non-EVM) execution environment, so there is no bridge involved and finality is a single transaction confirmation. Cross-chain routing adds at least one bridge leg: the route is constructed as a sequence of (1) a swap or transfer on the source chain, (2) a bridge transfer, and (3) a swap or transfer on the destination chain.

With the constraints set, the aggregator evaluates four fundamental routing patterns:

- Single-hop: The input token swaps directly to the output token in one pool. Example: USDC → ETH in a single Uniswap v3 pool. Simple and gas-efficient, but only viable when a direct pool exists with adequate depth.

- Multi-hop via intermediate token: No direct pool offers a competitive price, so the route chains two or more swaps through an intermediate token. Example: TOKEN_A → WETH → USDC, where WETH is the intermediate token that bridges liquidity between two thinner markets.

- Split routing across multiple pools or DEXs: The input amount is divided across several pools simultaneously to reduce per-pool price impact. Example: A large WBTC → DAI swap is split 60% through a Curve pool and 40% through a Uniswap v3 pool, so neither pool is hit hard enough to shift its price materially. This is the core mechanism behind route optimization.

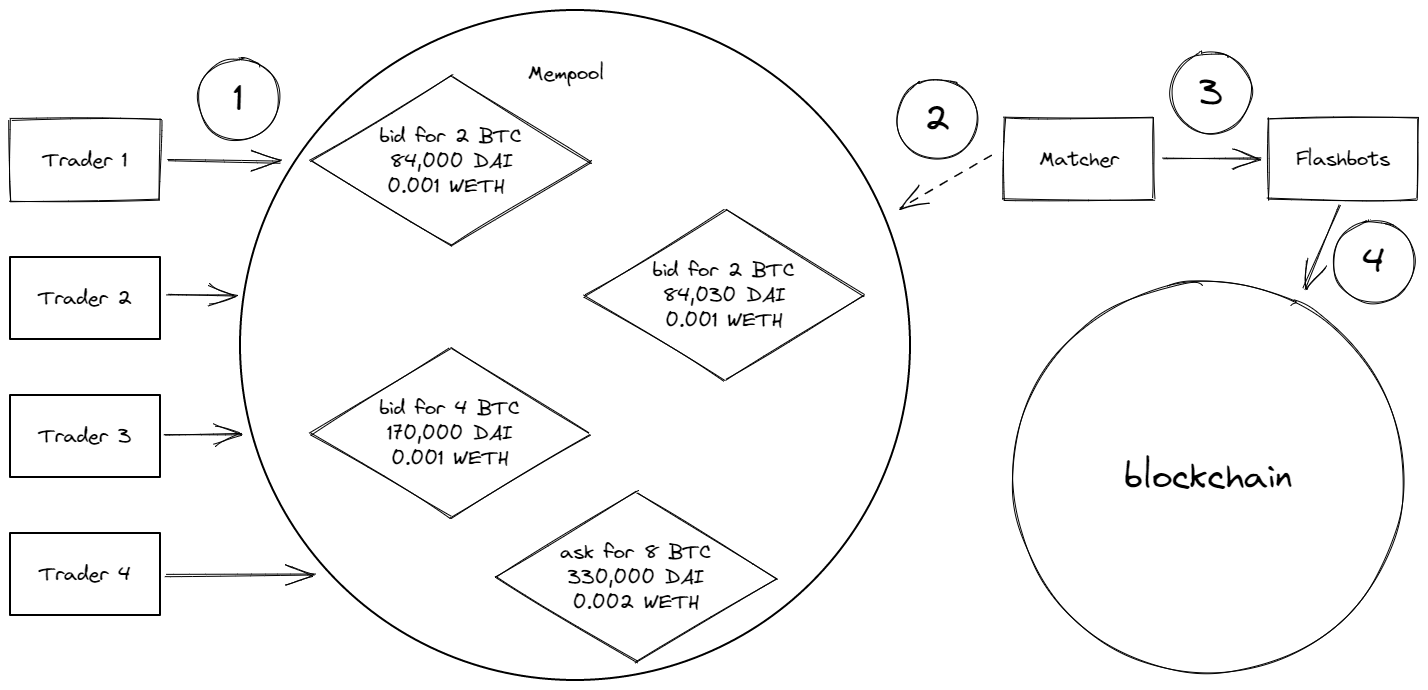

- RFQ/solver/auction-based routing: Instead of querying on-chain pool state, the aggregator broadcasts the swap intent to a solver network or RFQ market makers who respond with firm, off-chain quotes. Example: A 500,000 USDC → USDT trade is sent to competing solvers; the winning solver fills it at a guaranteed rate, bypassing AMM pools entirely and avoiding MEV (Maximal Extractable Value) exposure.

Liquidity Sources (and What Can Go Wrong with Each)

A swap aggregator does not hold liquidity itself — it reads and routes through external sources. The major categories, and what the aggregator actually reads from each, are:

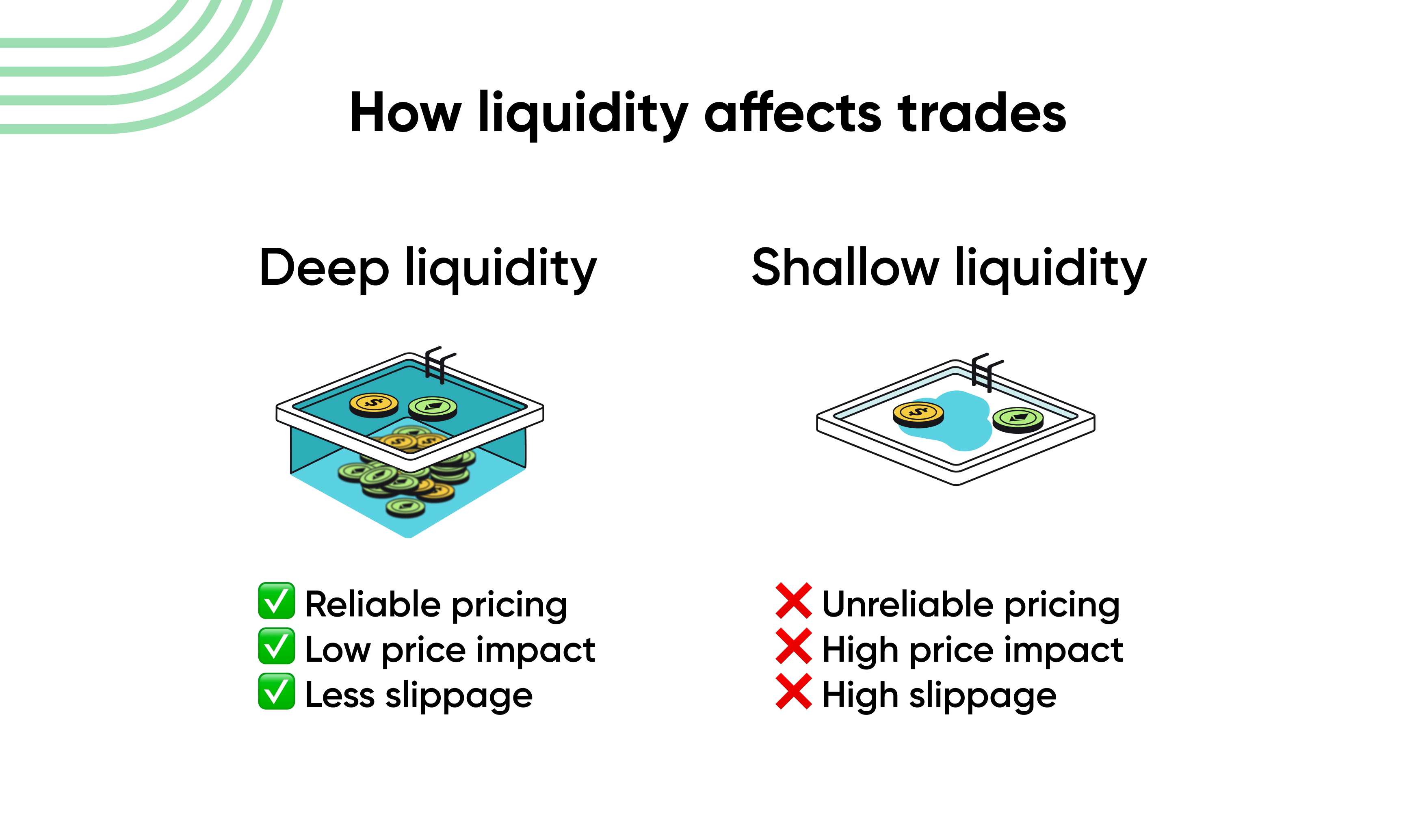

- AMMs (Automated Market Makers): Pool reserves, fee tier, and (for concentrated liquidity protocols) the tick/liquidity distribution across price ranges. Reserve ratios determine the spot price; tick data reveals how much liquidity is available at prices near the current rate. Thin liquidity in a pool creates outsized price impact on larger trades; concentrated liquidity pools can have gaps at certain price ranges.

- Order books (on-chain or hybrid): Bid/ask depth at each price level. The aggregator reads available volume at each price step to estimate fill cost for a given size. Stale quotes on hybrid order books can result in fills at prices worse than displayed if the book hasn't refreshed.

- RFQ market makers: Firm quotes valid for a short window (typically seconds). The aggregator reads quote price, fill size, and expiry timestamp. Unlike AMM prices, RFQ quotes are guaranteed for that window but expire quickly. As a result, quote expiry between the time a quote is fetched and the time the transaction is submitted causes the trade to revert or reprice.

- Cross-chain bridge liquidity: Available liquidity in bridge pools or canonical token reserves on both source and destination chains, plus bridge fee schedules and estimated transfer times. Thin bridge pools cap the maximum size of a cross-chain swap leg. Liquidity caps on bridge pools block trades above a threshold size or introduce significant delay when the pool is temporarily undercollateralized.

Pricing, Quotes, and Execution

Every swap passes through three distinct stages before value moves:

Stage 1 — Indicative quote: The aggregator polls liquidity sources and constructs the best available route using current on-chain state (pool reserves, order book snapshots, RFQ bids). The price shown to the user is an estimate based on this snapshot. Gas estimates are approximate at this stage.

Stage 2 — Final on-chain quote: When the user confirms the trade, the aggregator re-fetches or re-validates the route immediately before transaction submission. Pool state may have shifted since Stage 1 (other trades settled, liquidity was added or removed, an RFQ quote expired, or solver competition resolved differently). The final gas fee is recalculated against current network conditions. If the route has degraded beyond acceptable bounds, some aggregators will warn the user or reroute automatically.

Stage 3 — Execution and settlement: The smart contract executes the route on-chain. At this point, no further repricing is possible. If the actual output falls below the minimum received threshold, the transaction reverts automatically. The final settled amount reflects real-time pool state at the block where the transaction is included.

Slippage and Price Impact

Before discussing slippage, let’s define price impact: it is a function of trade size relative to available liquidity in the pools being used. It is deterministic at the moment of quoting: a $500 swap into a small cap token with a $200,000 pool has a calculable and immediate effect on the pool's price. Price impact is not a user setting — it is a feature of the liquidity source. The aggregator can estimate it before execution, and it should be reflected in the expected output.

Slippage tolerance is the user-defined protection band. Setting 1% slippage tolerance means the smart contract will reject the transaction if the actual output is more than 1% below the expected output. It is a safeguard, not a prediction.

Execution slippage, as the name implies, is the actual deviation between the quoted expected output and the final settled amount. It is only known after the transaction is confirmed. It can be caused by price impact (if the pool moved during block inclusion), by competing transactions in the same block, or by MEV activity such as sandwich attacks that adjust the pool price around your trade.

How aggregators reduce slippage beyond simply sourcing liquidity:

- Splitting routes: Dividing a trade across multiple pools reduces the amount hitting any single pool, which directly lowers per-pool price impact. A trade split three ways affects each pool at one-third the intensity.

- Choosing deeper pools or optimal fee tiers: A concentrated liquidity pool with heavy liquidity in the current price range imposes far less price impact per dollar traded than a sparse pool of the same headline TVL. The aggregator selects fee tiers and pools where tick liquidity is densest near the spot price.

- Selecting higher-liquidity intermediate tokens: Routing through a high-volume intermediate token (e.g., WETH or USDC) rather than a low-volume one reduces slippage at each hop, because the intermediate pools have more depth to absorb the trade without price movement.

Execution Speed and Failure Rates

Why can a swap fail? Each failure mode corresponds to user-visible error:

| Failure Mode | User-Visible Outcome |

|---|---|

| Revert due to min-received | Transaction fails on-chain; gas is spent. The actual output fell below the minimum received threshold. Common cause: price moved between quote and confirmation, or slippage tolerance was set too tight. |

| Insufficient allowance / approval missing | Transaction fails before execution. The smart contract cannot pull the input token because the user has not approved (or has revoked) the token allowance for the aggregator's router contract. |

| RPC / timeout | The transaction never reaches the mempool, or the quote fetch times out. The user sees a network error or "transaction not sent" message. No gas is spent. |

| Bridge leg delay | For cross-chain swaps, the source-chain leg completes but the bridge transfer stalls. Funds are in transit and temporarily inaccessible. This is not a revert — it requires monitoring the bridge's status interface. |

| Nonce issues | A pending transaction with the same nonce blocks the swap. The swap transaction queues indefinitely until the conflicting nonce is resolved (replaced or dropped). |

| Out-of-gas | The gas limit set by the aggregator (or overridden by the user) was insufficient for the complexity of the route. The transaction reverts and gas is consumed up to the limit. Common with multi-hop or multi-DEX split routes. |

A cross-chain swap appends two distinct time-related factors after the source-chain confirmation: (1) bridge confirmation, which ranges from minutes to tens of minutes depending on the bridge's security model (optimistic, ZK, or validator-based), and (2) destination execution, the time to submit and confirm the destination-chain transaction after bridge attestation is complete. These are sequential, not parallel, and the total elapsed time is their sum plus the source-chain latency above.

An aggregator controls route selection, quote construction, and transaction parameters but it does not control the base chain itself. Base-layer congestion, validator or sequencer ordering decisions, sudden liquidity withdrawal by LPs between quote and execution, and MEV activity at the block level are all outside the aggregator's reach. The best route at quote time can be a worse route by confirmation time, and no aggregator, regardless of how sophisticated its solver network or smart contract logic, can fully insulate a swap from the underlying chain's state at the moment of inclusion.

With all of these in mind, you might already have a solid grasp on what makes each product click. Before reiterating, let’s jump right into the best examples of currently available swap aggregators on the market.

Top Crypto Swap Aggregators in 2026

Let us address one expectation immediately: there is no single definitive DEX or swap aggregator, and not every one is the right fit for every trader. The best choice would depend on a combination of factors: which chain you're on, how large your trade is, whether you need a cross-chain swap, and how sensitive you are to MEV. The entries below are written to be decision-ready: each one makes explicit what it is good at, what it sacrifices, and who should not use it.

Rubic

Best for (2026): Users who need cross-chain and on-chain swap capability across a broad range of networks without committing to a single bridge or protocol. Rubic Private Mode aggregates multiple privacy providers for users who want to shield their trading activity from market participants.

Supported ecosystems (high level): Multi-chain, spanning EVM chains, L2 networks, and 20+ non-EVM ecosystems—one of the broader cross-chain route aggregators in coverage.

Routing & execution model: Rubic is a cross-chain and on-chain route orchestrator: it composes routes that combine a bridge step and a swap step, pulling from multiple bridge protocols and DEX liquidity sources to find the best combined path. Its model emphasizes aggregating various options such as DEXs, bridges, intent and semi-centralized providers, as well as other aggregators and privacy options, rather than being opinionated about which provider to use, giving users more flexibility in trading off cost, speed, and route reliability. The non-custodial design means assets route through smart contracts without the aggregator holding funds.

Key user controls: Users can compare route options before confirming, including visibility into the cost and estimated gas fee on both source and destination chains. Slippage can be adjusted for the swap leg. Route selection can be influenced by prioritizing speed or cost.

MEV / price-protection: Rubic has in-built MEV protection for Ethereum and BNB chains (the switch-on button appears when you’re performing the trade).

Trade-offs: Cross-chain routes may carry compounded risk: some bridges may have liquidity constraints for unpopular routes, smart contract dependencies across multiple protocols, and route failure scenarios where assets can be delayed. However, Rubic has responsive support service, and can help with refunds or pushing a delayed transaction through.

Who should avoid it: There's no strong avoid case — Rubic covers on-chain, cross-chain, and private swaps; users on a single niche ecosystem with a dominant native aggregator may prefer an ecosystem-native tool.

1inch

Best for (2026): EVM best-price routing for large single-asset swaps where squeezing out every basis point matters.

Supported ecosystems (high level): Primarily EVM—covers a wide range of EVM-compatible networks including mainnet and major L2s (and in practice often includes deployments where liquidity is concentrated on networks like BNB Chain).

Routing & execution model: 1inch uses its Fusion+ mode and Pathfinder algorithm to split orders across multiple liquidity sources simultaneously, including AMM pools, order book venues, and private market makers. What sets it apart is the solver network model under Fusion+, where professional resolvers compete to fill your order—often at better net prices than a single-route swap would produce. Route optimization here is aggressive: it will fragment a trade across many hops if the math favors it.

Key user controls: Slippage tolerance is adjustable per trade. Users can toggle between Classic mode (instant execution) and Fusion+ (solver-based, potentially better price but not instant). Partial fill behavior can be enabled so large orders don't revert if full liquidity isn't available. Token approval handling offers a permit-based flow to reduce on-chain approval transactions.

MEV / price-protection: Fusion+ provides native MEV protection by routing through private solvers rather than the public mempool, which is meaningful for larger trades in fast-moving markets. Classic mode does not carry the same protection.

Trade-offs: The complex multi-hop routing that makes 1inch powerful on large trades also generates higher gas fees—small trades can end up paying more in gas than they save on price impact. Fusion+ introduces auction-style timing, so execution isn't immediate.

Who should avoid it: Avoid if you're trading primarily outside EVM or need guaranteed instant execution without solver delays.

LI.FI

Best for (2026): Cross-chain rebalancing across L2s and EVM networks where you need a single interface to handle both the bridge step and the swap step.

Supported ecosystems (high level): Multi-chain, with emphasis on EVM and L2 ecosystems; not focused on non-EVM (but has Solana and Bitcoin).

Routing & execution model: LI.FI functions as a cross-chain route orchestrator as well as a same-chain DEX aggregator. It composes routes that combine a bridge leg (moving assets between chains) with a swap leg (exchanging tokens on the destination chain), sourcing from multiple bridge protocols and DEX aggregators in sequence. The distinctive mechanism is that it abstracts this multi-step process into a single user action, optimizing across bridge cost, route reliability, and destination-chain liquidity source in combination.

Key user controls: Users can set slippage independently for the swap leg. Bridge selection can be influenced by preference (e.g., prioritizing speed vs. cost). Gas fee estimation is surfaced before confirmation, though the cross-chain nature means final costs include both source-chain gas and bridge fees.

MEV / price-protection: MEV protection is not a primary focus—the cross-chain route structure reduces same-chain MEV exposure naturally, but there is no dedicated solver or private mempool mechanism. The main risk in fast-moving markets is quote-to-execution drift across the bridge step.

Trade-offs: Route failure risk is real: if bridge liquidity is insufficient or a bridge protocol experiences issues mid-route, transactions can stall or require manual recovery. Cross-chain routes also carry cumulative fees (bridge cost + swap fees + gas on both chains), which can erode value on smaller amounts.

Who should avoid it: There's no strong avoid case — Li.Fi (Jumper) covers on-chain, cross-chain, and private swaps; users on a single niche ecosystem with a dominant native aggregator may prefer an ecosystem-native tool. Li.Fi is only an API provider, if you want to use their API, go to jumper.exchange.

Jupiter

Best for (2026): Solana-native traders who want best-execution routing across the full Solana DeFi ecosystem with minimal friction.

Supported ecosystems (high level): Exclusively Solana—deeply integrated with Solana's AMM pools, order book venues, and liquidity programs.

Routing & execution model: Jupiter aggregates liquidity across Solana's AMM protocols and order book DEXs, using route splitting to minimize price impact on larger trades within the Solana ecosystem. Best execution here is defined by speed (Solana's block times), deep local liquidity, and routing that avoids excessive hops that add latency or slippage. Its Metis routing engine continuously recomputes optimal paths in real time.

Key user controls: Slippage is configurable, with an auto-slippage option that adjusts dynamically based on market conditions. Users can enable or disable exact-output swaps. Limit orders are supported natively, allowing traders to set target prices without active monitoring.

MEV / price-protection: MEV on Solana differs structurally from EVM—Jupiter integrates with Solana's transaction priority fee system to help transactions land reliably. Price protection is approached through route optimization and slippage caps rather than a dedicated solver or private mempool model.

Trade-offs: Jupiter is non-custodial and Solana-native, which means it offers no path for assets outside the Solana ecosystem without a separate bridge step. Liquidity depth on long-tail token pairs can vary, and high-traffic periods on Solana may affect transaction confirmation.

Who should avoid it: Avoid if you are not using the Solana ecosystem—Jupiter has no EVM or cross-chain capability.

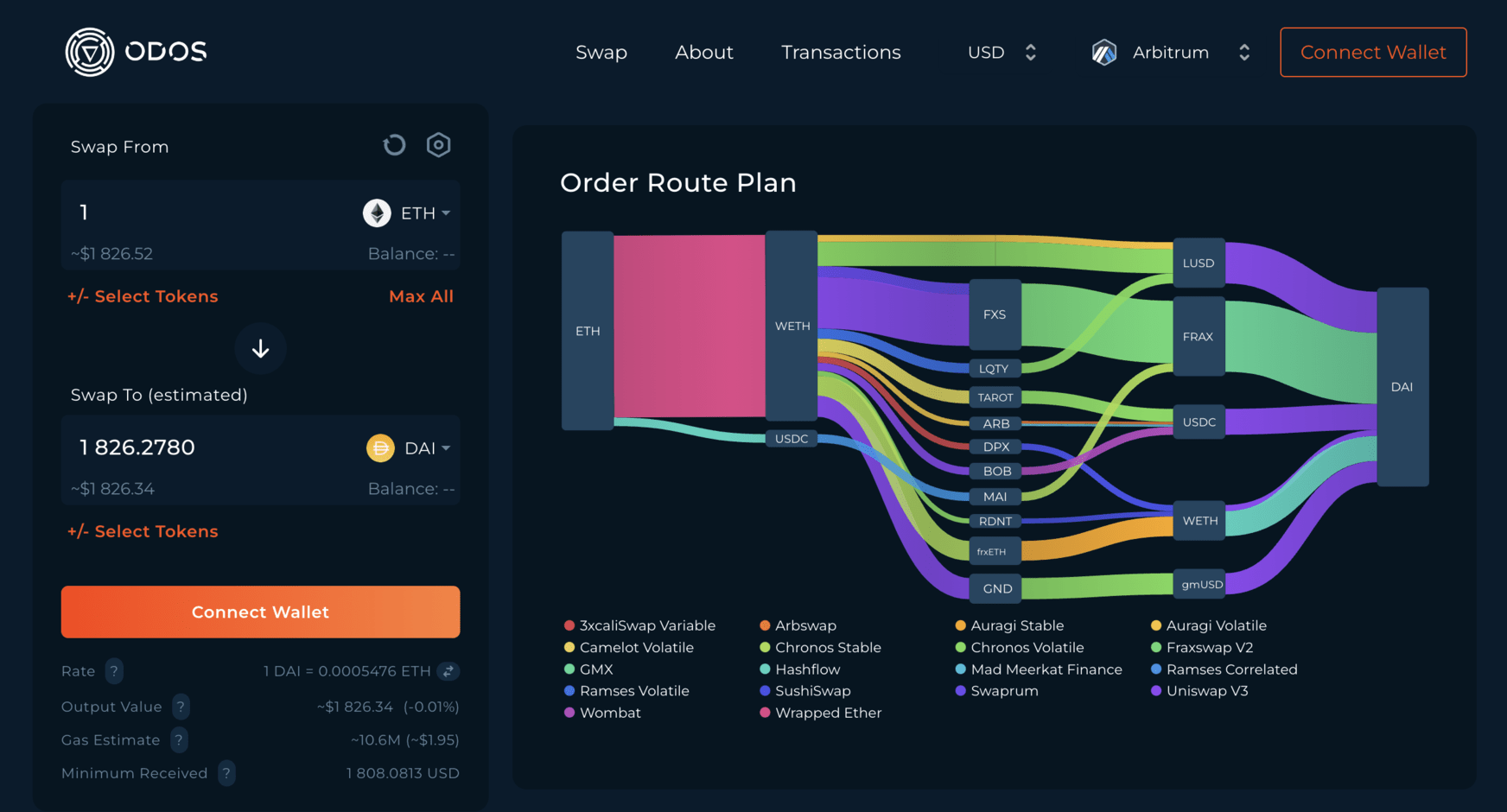

ODOS

Best for (2026): Advanced EVM traders running complex multi-token routes—particularly multi-input swaps where several tokens are consolidated into one in a single transaction.

Supported ecosystems (high level): Primarily EVM, supporting a range of EVM-compatible chains and L2 networks.

Routing & execution model: Odos's distinguishing mechanism is multi-input routing: unlike standard DEX aggregators that swap one token for one other, Odos can accept multiple input tokens and route them simultaneously into a single output (or multiple outputs). This is practically useful for portfolio consolidation or rebalancing without chaining separate transactions. Route optimization accounts for price impact and gas fee efficiency across combined legs.

Key user controls: Slippage can be set per route. The interface surfaces detailed route visualization so users can inspect how each input token is being routed—this is meaningfully more transparent than most aggregators for complex trades. Users can adjust which liquidity sources are included.

MEV / price-protection: MEV protection is not a core differentiator for Odos—execution goes through standard EVM transaction flows. For traders running large consolidation trades, price impact management through smart routing is the primary defense.

Trade-offs: The multi-input capability adds routing complexity that can increase gas fees compared to a simple single-pair swap. On chains with lower liquidity, route quality for less common token pairs may degrade. The tool is less useful if your trades are straightforward single-asset swaps where simpler aggregators are equally effective.

Who should avoid it: Avoid if your trades are simple, single-pair EVM swaps where a lighter aggregator will execute with lower gas overhead.

Velora (previously Paraswap)

Best for (2026): EVM traders and protocols that want competitive route optimization with a strong API layer for programmatic or integrator use cases.

Supported ecosystems (high level): Primarily EVM, with coverage across mainnet and key L2 ecosystems.

Routing & execution model: Velora routes across AMM pools, order book sources, and its own internal Augustus Swapper contract, which batches and optimizes execution. The routing model focuses on finding the best net price after gas fee factored in, splitting across liquidity sources as needed. Where Velora distinguishes itself from 1inch is in its API-first design and flexibility for integrators building on top of it—advanced users tend to choose it when they want programmatic control over routing parameters.

Key user controls: Slippage tolerance is configurable. Users can enable Permit2-style gasless approvals to reduce transaction overhead. Partial fill support is available. The interface and API both expose route details for inspection before execution.

MEV / price-protection: MEV protection is optional rather than native—Velora does not default to a private mempool or solver network. Users who need MEV-resistant execution should consider whether Fusion+-style protection (available via 1inch) is more appropriate for their trade size.

Trade-offs: Velora's strength is breadth of integration and API quality, but for a retail user doing occasional same-chain swaps, the advantage over simpler aggregators may be marginal. Quote-to-execution drift can occur in volatile markets if route computation takes time.

Who should avoid it: Avoid if you need cross-chain swaps or are trading on Solana—Velora is an EVM-only tool.

CoWSwap

Best for (2026): EVM traders prioritizing MEV protection and who can tolerate batch auction timing rather than needing instant execution.

Supported ecosystems (high level): Primarily EVM, focused on Ethereum mainnet and select EVM-compatible networks.

Routing & execution model: CoWSwap's mechanism is fundamentally different from standard DEX aggregators. It does not execute trades directly against AMM pools at submission time. Instead, it submits orders into a batch auction, where a solver network competes to find the optimal fill—including peer-to-peer coincidence-of-wants matches (where two traders' opposing orders are matched directly, bypassing AMM liquidity entirely). This batch/solver execution model is the centerpiece of what CoW Swap offers and is what makes it meaningfully different from route-splitting aggregators.

Key user controls: Slippage tolerance is set at order submission. Orders can be set as limit-style (fill at this price or better, or not at all). Gasless order submission is supported—users sign an intent, and solvers handle execution, meaning no gas is paid if the order fails. Token approvals use a dedicated contract to limit exposure.

MEV / price-protection: MEV protection is native and structural. Because orders are submitted off-chain and filled by solvers in batches, they never enter the public mempool in the traditional sense—front-running and sandwich attacks are substantially mitigated. This is CoWSwap's primary value proposition for large or sensitive trades.

Trade-offs: Batch auction timing means execution is not instant—if the market moves sharply between order submission and batch settlement, your order may not fill at the expected price, or may not fill at all. CoW Swap can underperform in fast-moving markets where urgency matters more than MEV protection. It is also less suited to very small trades where the overhead of auction participation adds unnecessary complexity.

Who should avoid it: Avoid if you need immediate execution or are trading in highly volatile conditions where batch settlement timing creates unacceptable slippage risk.

Cetus

Best for (2026): Traders operating on Sui or Aptos-style ecosystems who want native DEX aggregation with concentrated liquidity and deep local routing.

Supported ecosystems (high level): Primarily Sui/Aptos-style chains—Cetus is a native protocol on Sui and has presence on Aptos, not an EVM or Solana tool.

Routing & execution model: Cetus operates as a concentrated liquidity AMM and aggregator within its native ecosystem. Best execution in this context means routing across Sui's on-chain liquidity sources efficiently, leveraging concentrated liquidity positions to reduce price impact on larger trades. The routing model is tightly integrated with Sui's architecture—transaction speed and low gas fee costs are structural advantages of the underlying chain, not features Cetus adds independently.

Key user controls: Slippage tolerance is configurable. Liquidity provision and swap interfaces are combined in the same protocol, so users who also provide liquidity can manage positions alongside trading. Route details are surfaced before confirmation.

MEV / price-protection: MEV dynamics on Sui differ from EVM—the architecture reduces certain front-running vectors by design. Cetus does not add a dedicated MEV protection layer, but the chain-level properties provide some structural defense compared to EVM public mempool exposure.

Trade-offs: Cetus's value is concentrated in the Sui/Aptos ecosystem—liquidity depth and route quality outside that environment are not relevant, but within it, coverage of non-native or cross-chain assets depends on bridge availability. Users expecting EVM-level tooling or cross-chain route composition will not find it here.

Who should avoid it: Avoid if you are not actively trading within the Sui or Aptos ecosystem—Cetus has no practical utility for EVM or Solana traders.

Selection Criteria: How to Choose the Best Swap Aggregator

Let’s suppose you would like to review more options than we have highlighted. Alternatively, you would like to go beyond our summaries and evaluate our picks for yourself. In any case, feel free to use our criteria described right below.

Network Coverage

Not all "multi-chain" aggregators are made equal. Chain & asset support varies enormously beneath the headline claim, and you need to verify three measurable dimensions before trusting an aggregator with your funds.

Three dimensions to check:

- Chain family support — Does it cover EVM-compatible chains only, or does it also support non-EVM environments like Solana, Cosmos, or Tron? An EVM-only aggregator is a hard blocker if you need to move assets on Solana, and niche ecosystems (for example Aleo or Filecoin) are typically served by separate, ecosystem-native tooling rather than mainstream swap routing.

- L2 coverage depth — Arbitrum and Optimism are fairly regular at this point. Check whether it covers newer L2s and L3s (Base, zkSync Era, Scroll, Linea) and whether those chains have meaningful liquidity source depth or are just cosmetically listed.

- Token and DEX coverage within a chain — A chain can be "supported" with only three AMM pools indexed. Verify that the specific token you want to swap is actually routed through real liquidity.

How exactly do you verify? Open the aggregator's chain selector, switch to the target chain, and paste the token's contract address directly into the input field rather than searching by name. If support is real, you should see: (1) the token resolves correctly with its symbol and logo, and (2) available routes appear with liquidity source labels. If the token doesn't resolve or routes show zero liquidity, the chain is listed but not meaningfully supported for that asset.

Cross-Chain Support

Cross-chain swap support and bridge aggregation are often bundled together in marketing, but they're functionally different—and conflating them leads to costly surprises.

- Cross-chain swap UX refers to the end-to-end flow where you input one asset on Chain A and receive a different asset on Chain B, with the aggregator handling routing, bridging, and destination swap in a single interface.

- Bridge aggregation is a narrower function: the aggregator finds the best bridge for a specific asset transfer, but may not handle the destination-chain swap or gas.

Three things to test at quote time:

- Does the route show an explicit bridge leg? A transparent aggregator will label which bridge is being used (e.g., Stargate, Across, Hop) within the route breakdown. If you see a cross-chain route with no bridge name, treat that as a red flag.

- Is estimated time-to-finality displayed? Cross-chain swaps can take seconds or hours depending on the bridge. The UI should show an expected completion window before you confirm.

- Does the app show destination-chain gas requirements? Some bridges require you to hold native gas on the destination chain to receive or claim funds. If the aggregator doesn't surface this requirement pre-confirmation, you may arrive on the destination chain unable to move your assets.

Before you confirm a cross-chain route, verify that the bridge name is explicitly shown, expected completion time is displayed, refund or failure handling (what happens if the bridge fails mid-route?) is documented, and last but not least, whether you must hold destination gas before initiating.

Wallet Support

Wallet compatibility is more nuanced than a list of supported wallet names. Before assuming your setup works, check three criteria that aggregators frequently handle inconsistently:

- Mobile vs. extension parity — Some aggregators offer full route optimization and advanced settings on desktop browser extensions but serve a stripped-down experience on mobile. If you trade on mobile, verify that slippage controls, route details, and transaction previews are available—not just the swap button.

- Hardware wallet flow support — Using a Ledger or Trezor introduces additional signing steps. Confirm the aggregator supports hardware wallet connections natively and that the transaction data displayed on the device is human-readable, not just a raw hex blob.

- Permit-based approval signing — Some modern token approvals use EIP-2612 permit signatures (gasless approvals). Verify whether your non-custodial wallet can sign permit-based approvals if the aggregator uses them, as some wallet/aggregator combinations fail silently on this.

Treat any prominent in-app wallet warning seriously: if the aggregator at any point asks you to enter your seed phrase, requests signing on a domain you don't recognize, or redirects you to an unknown page during the transaction flow—stop immediately. Legitimate aggregators never require seed phrase entry; it’s a known pretense for crypto wallet scams.

Fees

Gas fee, LP fee, aggregator fee, bridge cost—these are four distinct cost layers that users routinely conflate into a single "fee." If you don’t separate them, you can’t compare routes in a way that survives execution.

| Fee Layer | What It Is | Who Charges It |

|---|---|---|

| Aggregator fee | A cut taken by the aggregator platform on the swap output | The aggregator |

| DEX LP fee(s) | Trading fees paid to liquidity providers on each AMM or order book hop in the route | Liquidity providers |

| Gas | Network transaction cost for on-chain execution | The blockchain network |

| Bridge/relayer fee (cross-chain only) | Fee charged by the bridge protocol for moving assets across chains | The bridge |

| Destination gas (cross-chain only) | Gas required on the destination chain to complete or claim the swap | The destination network |

Some aggregators charge zero aggregator fees but route through higher-fee liquidity sources. Others charge a small aggregator fee but find routes with better price impact that more than compensate.

To compare two aggregators fairly, use: identical input token and amount, identical slippage setting, and compare the expected received amount after all fees—not the displayed exchange rate or headline price. Run this check for the same pair at the same time. The aggregator showing a higher final received amount is offering better net route optimization for that trade.

Transaction Controls

The swap button is the last step. What matters is what the aggregator lets you control before you click it:

- Slippage controls (auto vs. manual) — Does the aggregator set slippage automatically, and if so, can you override it? Auto-slippage is convenient but may be set too high on volatile or low-liquidity pairs, increasing exposure to price impact. Look for the ability to set a manual maximum slippage percentage.

- Route pinning / avoid sources — Some aggregators let you pin a specific route or exclude certain liquidity sources. This matters if you want to avoid a DEX with known front-running issues or prefer a specific AMM for routing reliability.

- Partial fill behavior and order types — Standard market execution fills your full order at the best available price. Some aggregators offer limit-order-like execution or split orders over time (TWAP). Understand which mode is active for your trade.

- Approval management — When approving a token for the first time, check whether the aggregator defaults to unlimited approval or exact-amount approval. Exact spend approvals are safer; unlimited approvals expose your full balance to the contract's risk surface.

Contract address is shown and matches the aggregator's documented router address? Calldata summary is provided (where available), so you can verify what the transaction is actually executing? Token approval scope is explicitly labeled (exact amount vs. unlimited)? Then consider the transaction control test passed.

MEV Protection

Maximal Extractable Value is not just a theoretical concern—it's a measurable cost on high-value trades in public mempools. When evaluating an aggregator, look for user-visible MEV defenses rather than marketing language.

Which criteria matter here:

- Private vs. public mempool handling — Does the aggregator route transactions through a private mempool or RPC (like Flashbots Protect or similar) by default, or are transactions broadcast publicly? Public mempool exposure means bots can see and front-run your transaction before it confirms.

- Intent/solver or batch auction execution — Some aggregators use an intent-based or solver architecture where your trade is filled by competing solvers off-chain before settlement, reducing on-chain MEV exposure. Others use batch auctions where trades are bundled and settled at a uniform price. Both approaches reduce sandwich attack risk compared to naive AMM routing.

- UI labeling of protected mode — Does the interface clearly indicate when MEV protection is active? If it's buried in settings or undocumented, you can't confirm you're protected.

Large trade size + illiquid pair + public mempool = materially higher MEV risk. If your trade checks all three boxes, enable protected mode or private routing if the aggregator offers it. If it doesn't offer any mempool protection for that combination, factor that into your aggregator choice.

Audits, Reputation, and Support

Don’t be hasty to assume "audited" is a binary property. Before trusting an aggregator with significant funds, run a three-part due diligence check:

1. Smart contract audit verification

Find the aggregator's publicly linked audit reports. Verify: (a) the scope of the audit covers the contracts you're actually interacting with (router, approval contracts, bridge adapters), and (b) the audit date is recent enough to cover the current version of those contracts. A two-year-old audit on a contract that's been upgraded multiple times since is not meaningful coverage.

2. Incident history

Search for prior exploits, emergency pauses, or outages. Check the aggregator's official channels, post-mortem documentation, and third-party sources like DeFiLlama's hack tracker or Rekt News. A clean history matters; so does how the team responded to past incidents—transparent post-mortems and fast remediation are positive signals.

3. Support responsiveness

Identify the active support channels (Discord, Twitter/X, email). For time-sensitive issues like a failed cross-chain swap with funds in transit, you need to know the realistic response window before you're in that situation, not during it. Some aggregators have active community Discord channels with fast mod response; others are effectively asynchronous with multi-day email queues.

Confirm whether the aggregator is fully non-custodial at every step of the route. For same-chain swaps through an AMM, most aggregators are non-custodial—your funds go directly from your wallet to the smart contract and back. For cross-chain swaps, the bridge or relayer layer may introduce temporary custody of your assets. This is a meaningful risk distinction. Before confirming a cross-chain route, check the route details screen to identify which bridge is handling the transfer and research that bridge's custody model. If the aggregator's route detail doesn't disclose which bridge is being used, that is itself a trust signal worth weighing.

Use Cases: Best Scenarios for Swap Aggregators in 2026

Large Trades

If one source dominates (90%+) and price impact is still low, a single deep liquidity pool is sufficient — don't override it. However, if the quote screen shows the order being filled from three or more sources with roughly equal allocations, split routing is working in your favor.

Best when…

- Your quote shows meaningful price impact — typically a sign the trade size is large relative to pool depth at your primary liquidity source.

- The DEX aggregator suggests multiple hops or splits across more than one AMM, signaling that no single pool can absorb the order without slippage.

- You're moving an amount where even a 0.1–0.2% difference in execution price represents a cost worth optimizing.

Why an aggregator helps:

Route optimization is the most helpful core mechanism here. A crypto aggregator runs pathfinding across many liquidity sources simultaneously, then splits the order across multiple pools — or routes it through a single deep pool if that produces a better net price. The split-routing approach reduces price impact by not exhausting any one pool's liquidity. Without this, a large transaction sent directly to a single AMM can move the price against you mid-fill.

What to configure:

- Slippage tolerance: Set it tight enough to protect you (0.5–1% for most large trades), then confirm the displayed "minimum received" figure reflects that threshold before signing.

- Route preference: Enable "multi-route" or "split routing" if the UI offers a toggle; disable "single source" modes.

- MEV / private transaction mode: Large trades are high-value targets for sandwich attacks — enable private or MEV-protection mode where available.

- Route reliability: Some aggregators display estimated transaction failure rates per route; prefer routes with lower failure likelihood, especially under volatile conditions.

Trade-offs:

- Fragmented liquidity risk: Split routes execute as a single transaction, but if one liquidity source in the bundle has moved significantly between quote and execution, the whole route can fail or partial-fill at a worse price than shown.

- Overconfidence in displayed price impact: Price impact shown at quote time assumes static liquidity. In fast-moving markets, the actual impact at execution can be worse.

- Approval surface: Large trades often require interacting with contracts you haven't approved before. Verify token contract addresses before signing — a copied address error on a large trade is unrecoverable.

Stablecoin Swaps

For same-peg swaps (USDC↔USDT on the same chain), the primary variables are protocol fee, spread, and gas fee — not price impact. For cross-chain stable swaps, add bridge cost and finality time to the comparison. A quote that looks "tight" on a same-chain swap can still be net-worse than a competing route once gas is included.

Best when…

- You're swapping between same-peg stablecoins (e.g., USDC↔USDT, USDC↔DAI) where spread and fees matter more than price direction.

- You need to move stablecoins across chains and bridge cost is a meaningful variable.

- Gas fee relative to swap size makes direct DEX interaction inefficient, and aggregator routing through a stablecoin-optimized AMM (like a Curve-style pool) would reduce total cost.

Why an aggregator helps:

Stablecoin liquidity is highly fragmented across AMMs, order books, and cross-chain bridges. An aggregator can identify the specific liquidity source with the tightest spread and lowest price impact for a given stablecoin pair — something that isn't obvious from looking at any single venue. For cross-chain stablecoin moves, the aggregator handles bridge selection and can compare bridge cost against swap cost to find the cheapest net route.

What to configure:

- Slippage tolerance: Set to 0.1% or lower for same-peg stablecoin pairs. These pools are designed for minimal slippage; a higher setting unnecessarily exposes you to worse execution.

- Quote comparison step: Before confirming, isolate the three cost components on screen: gas fee, protocol fee, and bridge cost (if cross-chain). Add them manually and compare to alternative quotes.

- Bridge preference: For cross-chain routes, if the aggregator allows bridge selection, prefer bridges with audited canonical asset output over those producing wrapped representations.

- Route inspection: Expand the route diagram and verify every intermediate token. If the path passes through a non-stable intermediate asset, your exposure changes momentarily — relevant for large amounts and thin intermediate liquidity.

Trade-offs:

- Depeg risk in intermediate tokens: Some aggregators route USDC→USDT through an intermediate token (e.g., ETH or a liquidity pool token) to access deeper liquidity. If that intermediate asset depegs or drops sharply between the first and second leg of the transaction, you receive less than expected. Always verify intermediate tokens in the route before signing.

- Gas cost inversion: For small stablecoin swaps, the gas fee can exceed the benefit of optimized routing. Calculate net outcome (output minus gas) before executing.

- Bridge finality delay: Cross-chain stablecoin swaps via bridge routes can take minutes to hours to finalize depending on the bridge; factor this into time-sensitive rebalancing plans.

Cross-Chain Rebalancing

Best when…

- You need to move assets to hit target allocations across two or more chains — for example, shifting 30% of a position from Ethereum mainnet to an L2 to reduce gas fees on future transactions.

- You're managing a cross-chain portfolio and a single position drift (e.g., ETH heavy on one chain, stablecoin heavy on another) needs correcting without opening multiple manual bridging steps.

- Speed of rebalance matters less than cost certainty and receiving canonical assets on the destination chain.

Why an aggregator helps:

Cross-chain rebalancing requires coordinating a bridge leg and often a swap leg — two separate operations that most users handle manually and inefficiently. A cross-chain swap aggregator bundles these, selects the optimal bridge based on cost and finality, and executes the swap leg at the destination in the same flow. The pathfinding covers both DEX liquidity on the destination chain and bridge cost, producing a single net-outcome quote.

- Plan target amounts: Decide exactly how much of which asset you need on which chain before getting a quote. Vague rebalancing targets lead to multiple small transactions, each incurring bridge cost.

- Get a cross-chain quote: Enter the source asset/chain and destination asset/chain in the aggregator. Review the full route — identify which legs are bridge operations and which are DEX swaps.

- Verify bridge and DEX legs separately: Before signing, check the bridge leg (which bridge, estimated time, bridge cost) and the swap leg (which AMM, price impact, liquidity source) independently.

Bridge legs introduce finality delay — the transaction appears pending on the destination chain until the bridge reaches consensus or a relayer confirms it. DEX swap legs on the destination chain execute only after the bridge leg completes. Failures most commonly occur at the bridge leg (congestion, liquidity limits on the bridge, finality delays). The swap leg on the destination can also fail if market conditions changed during bridge transit.

What to configure:

- Bridge preference: Select bridges that produce canonical assets (e.g., native USDC via CCTP) over those producing wrapped representations where possible.

- Slippage on destination swap leg: Set conservatively, since bridge transit time creates uncertainty about destination chain prices at execution.

- Gas option on destination: Ensure you have sufficient native gas token on the destination chain to receive and interact with assets, or use an aggregator that handles destination gas.

- Route reliability: Prefer bridge/DEX combinations with higher historical success rates if the aggregator surfaces this data.

Trade-offs:

- Canonical vs. wrapped asset risk: A route that looks cheaper may deliver a wrapped or third-party bridged token instead of the canonical asset. Wrapped assets carry additional smart contract risk and may have lower liquidity on the destination chain.

- Bridge finality delay during volatility: If the bridge takes 20 minutes and markets move, you'll receive the destination asset at a worse net rate than quoted.

- Stuck funds: Some bridge routes have recovery mechanisms; others don't. If the bridge leg completes but the destination swap fails (e.g., slippage exceeded), funds may require manual recovery from the bridge contract.

Limit Orders

Best when…

- Liquidity for your target pair is thin and market-swapping now would produce unacceptable price impact.

- You're operating in volatile conditions and want to avoid slippage spikes by setting an exact minimum execution price.

- You have a target entry or exit price and execution timing is less important than execution quality.

Why an aggregator helps:

Here, "limit order" typically refers to on-chain limit orders or solver/auction-based intent systems (such as Fusion-style execution) — not the traditional order book model. Instead of routing against AMM liquidity immediately, your order is placed as an intent that a solver network watches. When market price reaches your target, a solver fills it — often at or better than your limit price because solvers can batch, offset, or route creatively. This mechanism beats market swapping in thin-liquidity or high-volatility scenarios because you're not forced to accept the current AMM quote.

What to configure:

- Limit price: Set based on your target rate, not the current market price. Most UIs show the current rate as a reference; adjust from there.

- Expiry: Set an expiry that matches your intent — hours for short-term tactical orders, days for longer-horizon targets. Orders that expire unfilled simply return the approval state; nothing is executed.

- Partial fill behavior: If supported, decide whether a partial fill is acceptable (useful for large orders in thin markets) or whether you require full execution only.

- Cancellation cost: Understand that canceling an on-chain limit order before expiry requires a transaction and gas fee. Factor this into the decision to place the order.

Trade-offs:

- Price never hits: If the market doesn't reach your limit price before expiry, the order expires unfilled. You've lost nothing except the opportunity cost and any gas paid for placement (varies by implementation).

- Open approvals risk: Placing a limit order typically requires a token approval to a contract. If the order expires or you forget about it, the approval remains active. Periodically audit and revoke stale approvals using a token approval manager.

- Solver non-execution at target: In solver/auction-based systems, solvers are incentivized but not guaranteed to fill orders exactly at the limit price at the moment price crosses. In extremely fast-moving markets, fill timing can lag by one or more blocks.

Gasless Execution

One critical distinction from the get-go: "gasless for user" does not mean "no cost." It may be worth it to get the gasless quote (output amount), then get a standard swap quote for the same pair and size. If the gasless route delivers materially less output, paying gas directly is cheaper.

Best when…

- You hold assets on a chain but have insufficient native gas token to pay for a transaction directly.

- You want to batch or simplify UX for non-technical users who shouldn't need to manage gas across multiple L2s.

- The gasless quote produces a net outcome (output received minus embedded cost) that is at least as good as a standard swap quote.

Why an aggregator helps:

Gasless execution in this particular case means the user does not pay gas in the native token — but gas is not free. It is either embedded in the swap spread, deducted from the output amount, or sponsored by a relayer/solver. A solver network or relayer submits the transaction on your behalf and recovers gas cost from the trade economics. The mechanism typically uses meta-transactions, ERC-4337 account abstraction, or Fusion-style execution. The aggregator's value here is making this process invisible to the user while (ideally) still delivering a competitive route.

Before relying on gasless execution, verify:

- Wallet compatibility: Gasless routes typically require smart contract wallets, ERC-4337-compatible wallets, or specific router integrations. Standard EOA wallets may not be supported on all aggregators.

- Chain availability: Gasless execution is often limited to specific chains (commonly major L2s). Confirm the feature is live for your chain before building a workflow around it.

- Volatility constraints: High volatility can cause relayers to reject or delay submission if gas prices spike beyond the embedded gas budget. Gasless transactions may fail more frequently during congested periods.

- Token support: Not all tokens are eligible for gasless routes; check the aggregator's documentation or UI indicator before assuming it's available for your specific asset.

What to configure:

- Net outcome comparison: Enable "gasless" mode and note the quoted output. Then disable it and requote with standard gas payment. Choose based on net received, not UX convenience alone.

- Slippage tolerance: Set as you would for any swap — the relayer/solver still executes against AMM or solver liquidity, and slippage limits still apply.

- Minimum received: Verify this figure explicitly. In gasless flows, the gas cost deduction may reduce the minimum received below what you'd expect — confirm it's acceptable before signing.

- Relayer/solver identity: If the aggregator discloses which relayer or solver network is handling submission, note it. Reputable, audited solver networks reduce — but don't eliminate — execution risk.

Trade-offs:

- Embedded cost opacity: The gas cost embedded in spread or output deduction is not always clearly labeled. If the UI only shows "output amount" without itemizing the gas deduction, calculate it manually by comparing to a standard quote.

- Relayer failure under load: If the relayer goes offline or rejects the transaction due to gas price spikes, your transaction may silently fail or be delayed. Unlike a self-submitted transaction, you have less direct control over resubmission.

- Approval and trust surface: You are signing a message or transaction that authorizes a third-party relayer or solver to execute on your behalf. Before signing, verify: token approval scope (what contract, how much), minimum received, and the full route. Treat this with the same scrutiny as any contract interaction.

Risks and Key Considerations

When using swap aggregators, every transaction is non-custodial: you authorize actions via wallet signatures, and once confirmed on-chain, swaps are generally irreversible. The practical discipline is to treat each risk category as a separate layer — and to verify the layer that actually applies to your route.

Smart Contract Risk

A vulnerability or malicious behavior in the aggregator contract, the underlying AMM/DEX contract, or the token contract itself can cause funds to be lost, locked, or misdirected during a swap. It can show up when the swap completes but you receive far fewer tokens than quoted (fee-on-transfer or rebase token behavior quietly adjusting output); a sell transaction succeeds but a buy of the same token always fails (classic honeypot pattern). Your wallet can preview an unexpected sequence—approve + swap + an additional arbitrary call—that you didn't initiate, or a token balance becomes frozen mid-hold because the token contract has a blacklist or pause function.

Mitigations:

- Differentiate contract layers before trading. Aggregator contract risk (the router logic routing your swap) is separate from DEX/AMM contract risk (the pool executing it) and token contract risk (the asset itself). Verify each independently.

- Pre-flight token check: Confirm the token contract address against at least two authoritative sources (the project's official site and a reputable on-chain explorer). Mismatched addresses are the first sign of a scam token.

- Check for transfer restrictions: Fee-on-transfer tokens reduce output on every hop; rebase tokens change balances automatically; blacklist/pause tokens can freeze your position. Look for these flags on token analytics platforms before swapping.

- Check audit and reputation signals: Prefer tokens and aggregators with published, recent audits from recognized firms. Absence of any audit is itself a signal for smaller or newer tokens.

- Simulate or preview the transaction: If your EVM-compatible wallet supports transaction simulation (many do via built-in or extension features), use it. A simulation that fails or shows unexpected state changes is a hard warning.

- Inspect all function calls: Reject any transaction that bundles unfamiliar permissions alongside the swap—particularly approve calls to unknown spenders or arbitrary external contract calls. If you see more calls than expected, stop and investigate.

Avoid the trade if the token contract address cannot be independently verified against the project's official channels or the transaction preview includes function calls you did not initiate or cannot identify.

Route Risk

The route selected by the aggregator may fail to deliver the expected output due to stale quotes, illiquid intermediate tokens, or pool-level issues that appear only at execution time.

How it shows up:

- Slippage tolerance is exceeded repeatedly and the transaction reverts.

- The estimated output differs significantly from the final received amount even within your slippage setting.

- A multi-hop route fails midway because an intermediate liquidity source dried up between quote and execution.

- Gas fee estimates on L2 networks come in far higher than shown, causing unexpected transaction failures.

Mitigations:

- Compare 2–3 aggregator quotes before trading. A single quote is a snapshot; comparing across liquidity sources reveals whether one router has a genuinely better route or is quoting stale data.

- Inspect intermediate tokens on multi-hop routes. Any intermediate token with thin volume or a small market cap adds fragility. A route through a low-liquidity AMM pool can collapse between quote and fill.

- Prefer fewer hops when price difference is marginal. Route reliability decreases with each additional hop. If a two-hop route offers only a fractionally better price than a direct swap, the simpler route is lower risk.

- Set slippage relative to volatility and liquidity depth. High-volatility pairs and low-liquidity pools require wider slippage tolerance, but wider slippage also increases price impact exposure—calibrate, don't default.

- For large trades, split size across multiple transactions. A single large swap through a thin pool will move the price against you. Partial fills executed over time or via limit/auction-style execution, where available, reduce that price impact.

- Avoid thin liquidity pairs even when the quote looks best. A great-looking quote on a pool with almost no depth is a stale quote waiting to fail or a high-price-impact trade waiting to happen.

If the route includes an intermediate token you cannot independently verify or that has near-zero trading volume or the aggregator's quote is significantly better than all competitors without an obvious reason—stale data or a misconfigured pool fee tier is the likely culprit.

MEV Risk

Miners and validators (or searcher bots in a mempool) can observe your pending transaction and insert their own trades around it—sandwiching, backrunning, or exploiting liquidation-adjacent volatility—to extract value at your expense. In the sandwiching case, a bot buys before your swap and sells immediately after, pushing the price against you by the maximum your slippage allows. Backrunning can happen when your large swap moves the price, and a bot immediately arbitrages the resulting imbalance—you don't lose directly, but you “subsidize” the arbitrage. On top of that, during high-stress market moments, bots racing to trigger liquidations create sharp price spikes that hit your pending swap's slippage limit.

MEV red flags:

- Your transaction fails repeatedly, then finally succeeds—but at a noticeably worse price than the original quote.

- Significant price movement occurs between the moment you sign and the moment your transaction is included in a block.

- You observe unusually high gas fees on transactions immediately before and after yours in the same block.

Mitigations:

- Use a private RPC or MEV-protected submission endpoint when your wallet or the aggregator UI supports it. These routes bypass the public mempool, eliminating the window during which bots can front-run your transaction.

- Tighten slippage on large or high-value swaps. Wider slippage is a larger MEV extraction window. Set it as tight as the pair's volatility and liquidity depth allow.

- Avoid broadcasting during volatile market conditions. High-volatility periods attract more MEV searchers and increase the probability of sandwiching.

- Prefer batch-auction or intent-based execution when the aggregator supports it (some newer aggregators route via intent systems that settle off-chain before broadcasting). These architectures structurally reduce sandwich exposure.

- Avoid predictable, easily copied transactions. Large round-number swaps on frequently monitored pairs are higher-profile MEV targets.

Avoid or at the very least be careful with the combination that maximizes MEV extraction potential: no access to a private RPC and the pair is high-value, high-volatility, and thinly traded. Retrying when a transaction has already failed multiple times at the same price, without changing execution conditions will produce the same result.

Approval Risk

Granting token approvals—especially unlimited ones—gives a spender contract permanent permission to transfer your tokens, expanding the blast radius of any future exploit or malicious interaction with that contract.

How it shows up:

- A prompt asks you to approve an unlimited token amount to a contract address you haven't verified.

- A spender address in the approval request differs from the aggregator's documented router contract.

- You are asked to sign an approval for a token you are not actively trading in the current session.

- A two-step approval flow appears when you try to change an existing allowance (some EVM tokens require resetting to zero first).

Mitigations:

- Approve exact amounts when possible. Approving only the amount required for the current swap limits exposure. If the aggregator's UI offers an "exact approval" option, use it.

- Use separate approvals per token per session. Bundling approvals increases the attack surface. Approve each token independently and only when you are actively trading it.

- Revoke allowances after trades. Persistent approvals are persistent risk. Use your wallet's allowance management settings or a dedicated allowance manager tool to revoke permissions for contracts you are no longer actively using.

- Verify the spender address before approving. The spender in an approval request should match the aggregator's published router contract address. A mismatch is a hard stop—do not approve.

- Avoid approvals requested by unknown spenders. Any approval prompt that originates outside the aggregator's own UI (e.g., from a pop-up, a DM link, or an unfamiliar site) should be rejected immediately.

- Expect and handle the two-step reset: Some tokens require the allowance to be set to zero before it can be changed to a new value. If you encounter a two-step approval process and higher gas fee, this is expected behavior for those token contracts—not an error.

The aforementioned red flags apply here. It may be for the best to dip if the spender address in the approval request cannot be verified against the aggregator's official documentation or you are prompted to approve an asset that is not part of the current swap.

Bridge Risk

Cross-chain swaps route funds through bridge contracts and messaging/relayer layers, each of which introduces distinct failure modes—smart contract exploits, relayer downtime, or liquidity shortfalls—that can delay, strand, or permanently lose your funds.

How it shows up:

- Funds leave the source chain but do not arrive on the destination chain within the estimated time window.

- A wrapped or bridged asset is received instead of the native token you expected (token mapping mismatch).

- The bridge UI shows a "pending" status indefinitely, with no clear recovery path.

- The bridge cost shown at quote time differs materially from the actual gas fee deducted on the destination chain.

Bridges roll up three kinds of risks into one: smart contract risk, messaging/relayer risk (the destination chain is not notified of a bridging transaction and funds are stuck), and liquidity risk (insufficient funds for minting on the destination chain).

Take some extra steps to ensure a transaction is successful whenever a bridge is involved:

- Confirm the source chain and destination chain match your intent before signing.

- Verify the recipient address on the destination chain—address formats differ across EVM and non-EVM networks.

- Confirm the token mapping: know whether you will receive a canonical asset, a wrapped asset, or a liquidity pool receipt token.

- Note the estimated arrival time and set a calendar reminder to check status if the bridge cost or complexity is significant.

- Understand the partial failure path before you send: does the bridge refund to source automatically, or do you need to manually claim on the destination?

If your cross-chain swap does not arrive as expected, do not retry immediately. Save the originating transaction hash, then check the bridge's own status page and the block explorer on both the source and destination chains. Confirm the source transaction finalized before assuming the bridge failed. Retrying without this verification risks a duplicate send.

Things to verify the lack of risk are the bridge contract address, ideally, its audit status, and the status on the project’s page or block explorer. Can’t do it, don’t do it.

Phishing Risk

Attackers use fake aggregator interfaces, malicious permit signatures, and social engineering to trick users into granting wallet access or sending funds to attacker-controlled addresses—without any on-chain vulnerability needed.

How it shows up:

- A browser search for a popular aggregator returns a sponsored result with a lookalike domain (one character off, or a different TLD).

- A token airdrop appears in your wallet; interacting with it triggers an approval or permit signature.

- A "support" account in Discord or Telegram DMs offers to help resolve a swap issue and asks you to connect your wallet to a link they provide.

- A malicious browser extension intercepts transaction data and replaces the destination address or modifies approval parameters.

- A "permit" signature request (EIP-2612) grants a spender permission to transfer your tokens without requiring a separate on-chain approval transaction—making it silent and fast to exploit.

Signature hygiene checklist:

- Verify the domain in your browser's address bar before connecting your wallet. Bookmark legitimate aggregator URLs and use bookmarks, not search results.

- Inspect every requested permission in the signature prompt. Permit signatures will show a spender address, an amount, and an expiry—scrutinize all three.

- Reject blind signatures. If your wallet cannot decode and display what a signature authorizes in plain language, do not sign it.

- Use a hardware wallet for large swaps. Hardware wallets provide an additional confirmation layer and make it significantly harder for malicious software to silently approve transactions.

- Never share your seed phrase or private key—with anyone, in any context, including "official support."

If compromised, immediately revoke all approvals from the affected wallet using an allowance manager. Prioritize high-value tokens first. Move remaining funds to a fresh wallet that was generated on a clean device—do not reuse any wallet associated with the compromised seed phrase. Rotate compromised devices and extensions: Uninstall all browser extensions on the affected device, run a full security scan, and consider the device untrusted for future high-value transactions.

Unless the aggregator URL exactly matches the official domain you have used before or verified from the project's official social channels, and no signature request appears outside the expected swap flow, or includes permissions you did not explicitly initiate, do not treat a transaction as risk-free.

Conclusion

Choosing the right aggregator comes down to matching your trade type to the tool built for it. "Best price" is not the number shown in the quote box; true execution quality is the all-in outcome: quoted amount minus gas fee, minus bridge cost, adjusted for failure probability and any revert cost if the transaction fails mid-route. Evaluate every swap on this composite figure — quote + gas + bridge cost + failure probability—not on the headline rate alone.

Frequently Asked Questions

Are crypto swap aggregators safe?

Crypto swap aggregators are generally non-custodial—they never hold your private key or funds—but they introduce several distinct risk layers you should evaluate before signing any transaction, including the fact that many aggregator front-ends are browser-based DApp interfaces that can be impersonated.

Check the front-end and URLs, smart contract addresses (routers, bridges etc.), token approvals and wallet signatures every time you make a swap.

An unexpected or unsolicited token approval request, a token contract address that doesn't match the official source, a dramatic price impact warning (e.g., >5–10%), an unfamiliar or newly deployed DEX appearing in the route, or a forced chain-switch prompt you didn't initiate are the red flags you should watch out for.

Do swap aggregators always get the best price?

Not always—"best price" is better understood as the best expected execution outcome, which folds in protocol fees, aggregator fees, LP fees, gas cost, MEV exposure, price impact, and any failure or retry costs, not just the quoted swap rate.

How do gas fees affect swap results?

Gas fees directly reduce your net received amount and, when underpriced, increase the likelihood that a transaction fails entirely—leaving you with a fee paid and no swap completed.

What slippage should I set?

Slippage tolerance is your instruction to the smart contract to reject the trade if execution price moves beyond a set threshold—it is not the same as price impact, which is the market effect your trade size has on the pool price.

If price impact is already high (e.g., >2%), lowering slippage tolerance only increases failure rate—address the root cause by reducing trade size or splitting the order instead.

Higher slippage tolerance also widens the window for sandwich attacks, where a bot front-runs and back-runs your trade. When MEV-protected modes or private solvers are available in the aggregator UI, enable them. If no MEV protection is available, use the minimum slippage that still allows the trade to execute rather than the maximum you'd tolerate.

If you adjust trade size or the aggregator recalculates the route, revisit your slippage setting—liquidity source composition can shift the optimal value.

How do aggregators choose routes?

A DEX or crypto swap aggregator evaluates available liquidity sources—AMMs, order books, and private market makers—alongside gas cost estimates, hop count, intermediate tokens, split-routing options, and estimated probability of success to construct the path that maximizes your output.

What's the difference between cross-chain swaps and bridges?

A standard same-chain swap settles entirely on one blockchain in a single state transition; a cross-chain swap requires a bridge or cross-chain messaging step to move value between chains, followed by a destination swap—introducing extra settlement time, additional fees, and a mid-route failure scenario that doesn't exist in single-chain swaps.

Which swap aggregator is best for beginners?

Rather than pointing to a single brand, the right aggregator for a beginner depends on chain, cross-chain need, MEV protection preference, and UI complexity tolerance—and the safer starting point is a set of beginner-safe defaults, not just a name.

- On Solana? Use an aggregator native to Solana's liquidity layer with integrated MEV protection and clear route disclosure.

- On EVM chains (Ethereum, Arbitrum, Base, etc.)? Choose an aggregator that shows full route transparency, supports EIP-1559 gas controls, and offers MEV-protected execution modes.

- Need cross-chain? Add a cross-chain-capable aggregator, but only after you're comfortable with same-chain swaps—cross-chain introduces the additional bridge cost and failure-mode complexity described above.

- Want a simple UI? Prioritize aggregators with one-click conservative defaults over those that surface advanced controls by default.

- Want advanced controls? Look for full route customization, adjustable slippage, gas settings, and split-routing visibility.