What Happens When All Bitcoins Are Mined?

Key Takeaways

- 🪫 Bitcoin’s fixed 21 million BTC cap is not a target but a hard ceiling baked into the protocol; every halving event compresses issuance further until the final satoshi is released near 2140, making scarcity a mathematical certainty rather than a policy choice.

- 🪫 Whether on-chain demand or Layer 2 settlement drives transaction volume will determine the size and consistency of the fee market and, by extension, whether fees can realistically replace today’s block subsidy.

- 🪫 Once the block reward hits zero, hash rate becomes a direct function of fee revenue; a thin fee market translates almost immediately into a smaller security budget and a lower cost to mount a network attack.

- 🪫 Users and businesses planning long-term strategies on Bitcoin should account for structurally higher base-layer fees as scarcity intensifies and the subsidy compresses — this is a cost shift, not just a miner problem.

Contents

One of Bitcoin’s most famous features is its hard limit on the total supply of 21 million BTC. New bitcoins are issued through mining at a steadily declining rate, and 90% of all BTC that could exist is already in circulation. Although mathematically it would take over one hundred years to mine the remaining bitcoins, the question is already worth asking: what happens when all bitcoins are mined?

If you need to know how crypto mining works or what Bitcoin halving is, we recommend other guides. This one will dive deep into the Bitcoin block reward mechanics, nuances of supply availability, and most importantly, the fee market. If you care about the long-term prospects of BTC, whether as a user or investor, this one is for you!

Bitcoin Supply Cap and Monetary “Policy”

Bitcoin proponents often contrast it to fiat money for having a protocol-enforced fixed terminal supply of 21 million BTC. After all, one of the challenges it sought to address was inflation that eroded the value of fiat currencies, especially in the aftermath of the 2008-2009 financial crisis.

An important caveat to this rule is Bitcoin’s protocol can be amended through a hard fork if a significant enough portion of the community deems it necessary. However, the scarcity-oriented design introduced in the original proposal by Satoshi Nakamoto is a fundamental feature that justifies the perceived value of BTC in the current market, and for the time being, the very prospect of proposing to change the total supply would be extremely unpopular and unlikely to be adopted even in a minority hard fork.

Total supply cap is not the same as issued or circulating supply. 21 million bitcoins will eventually exist but in a pretty distant future, since the issuance rate is reducing asymptotically until the block subsidy is zero. What matters today is the issued supply, or what has already been mined, and circulating supply, which is issued bitcoins minus the BTC that can no longer be accessed.

Why did we use quotation marks to refer to Bitcoin’s monetary policy? To avoid confusion with governmental policies: despite there being a community that can propose changes to Bitcoin’s protocol, they are not a central authority that has the power to adjust issuance in response to economic conditions. As it stands, all changes to Bitcoin’s issuance happen as dictated by the protocol itself, and the rules were established at the very start without ever changing so far. This makes Bitcoin’s inflation rate entirely predictable years and decades in advance, something no central-bank-issued currency can claim.

Rounding in Bitcoin’s Issuance Schedule

Bitcoin’s block subsidy is denominated in satoshis — the smallest unit of Bitcoin on the Bitcoin blockchain, where one BTC equals 100,000,000 satoshis. Because satoshis are integers, the halving mechanism uses integer division: the subsidy is divided by two and any fractional remainder is simply dropped. Early on, this rounding effect is negligible but as the subsidy shrinks toward tiny satoshi values, it becomes more defined.

Bitcoin’s original block reward was 5,000,000,000 satoshis (50 BTC), a whole number that halves cleanly at first. Every 210,000 blocks, the reward is cut in half using integer division, simply meaning 1 satoshi halved becomes 0 satoshis, not 0.5. Once the subsidy reaches 1 satoshi and is halved again, it cannot be represented as a valid integer reward, so issuance ends entirely. No further BTC can be created after this point.

This rounding behavior means the total Bitcoin supply will settle slightly below 21,000,000 BTC. The satoshi denomination and integer arithmetic together create a hard ceiling that is, in practice, fractionally shy of the round number most sources cite.

Bitcoin Issuance Schedule to 2140

Block Subsidy

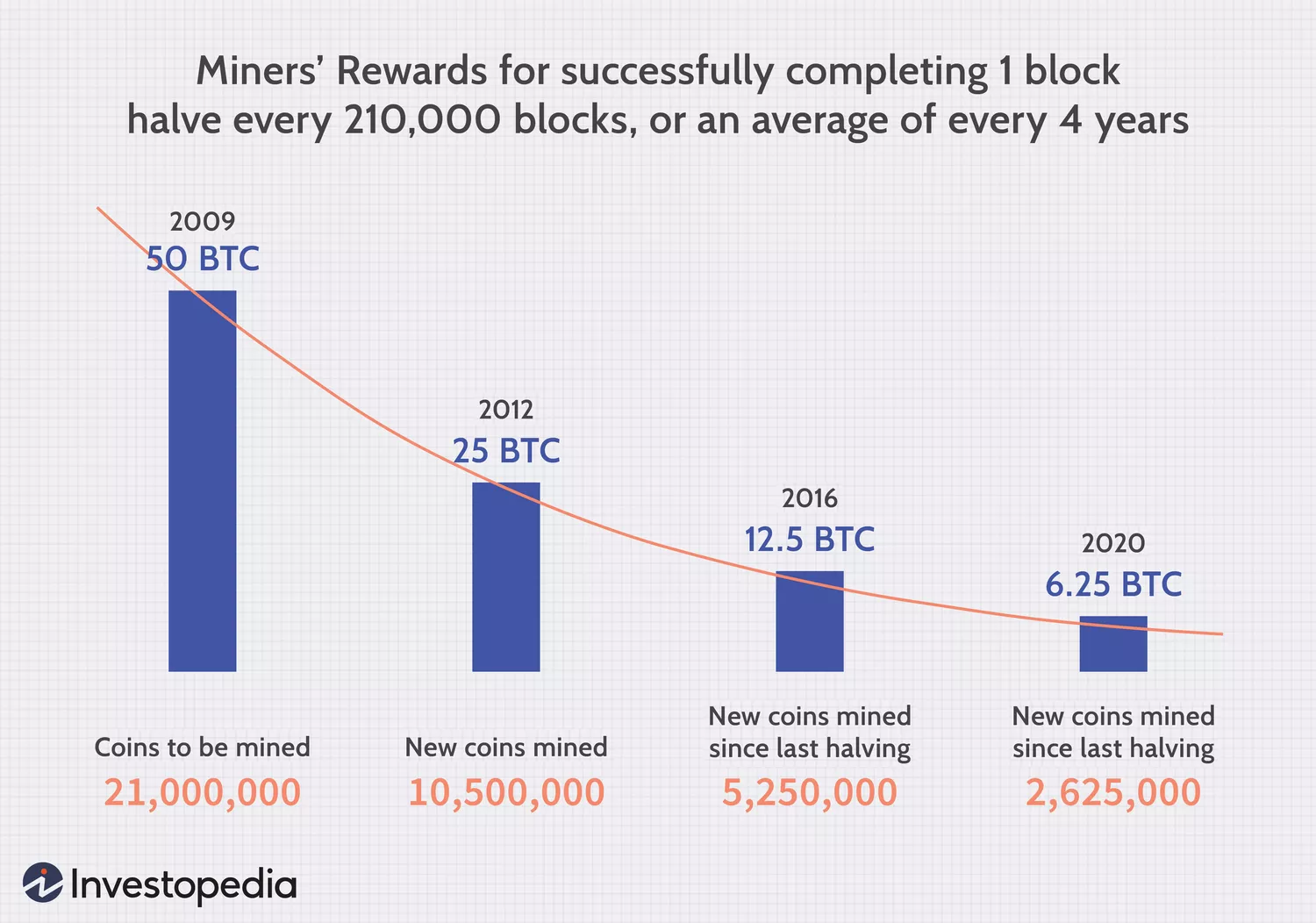

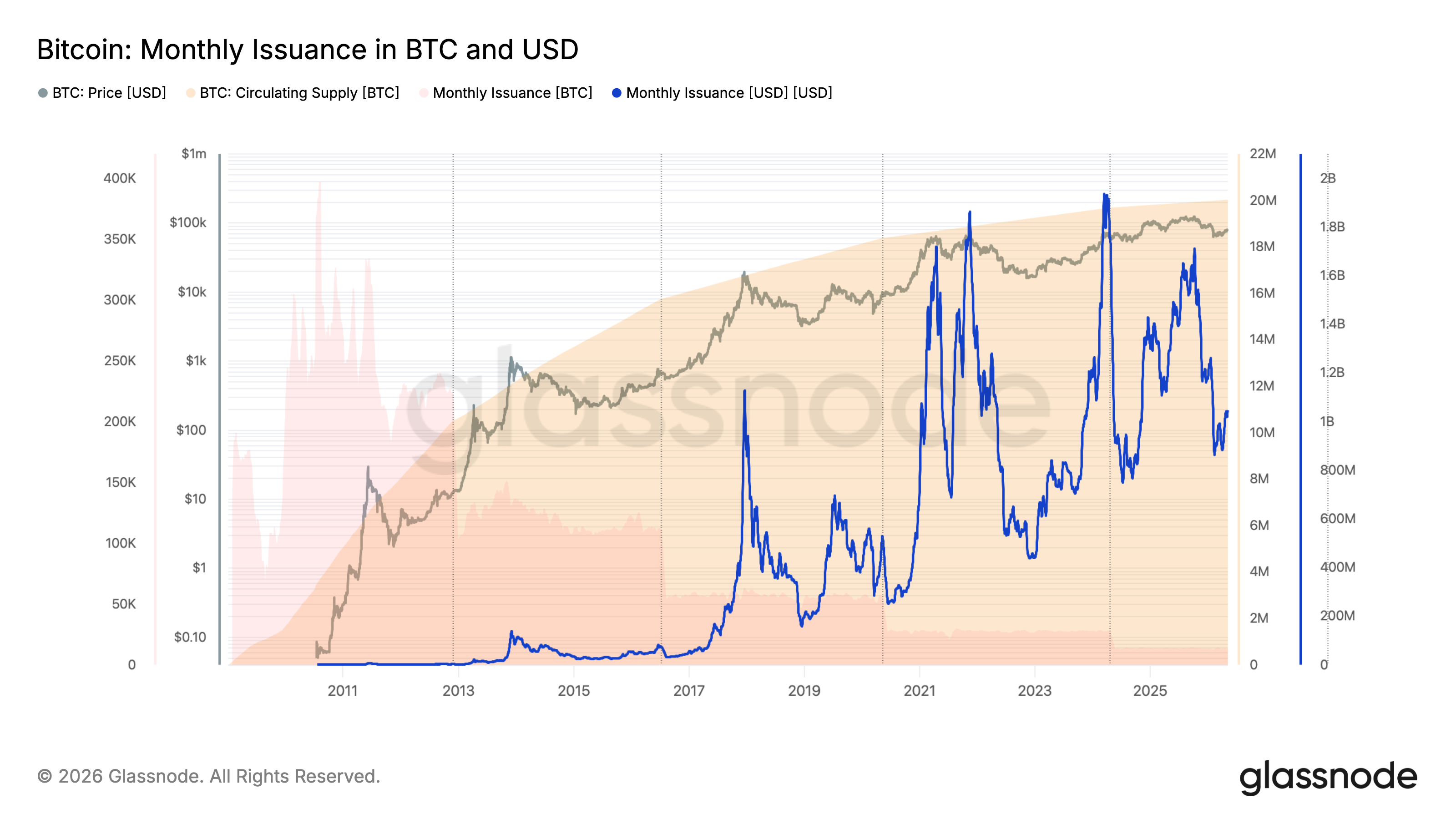

Every time a miner successfully adds a new block to the Bitcoin blockchain, the protocol awards them a fixed number of newly created coins. This award is the block subsidy, and it follows a precise formula: subsidy = 50 ÷ 2n, where n is the current epoch number. An epoch is a 210,000-block interval: the span between two consecutive halvings. The starting subsidy was exactly 50 BTC at genesis (epoch 0), dropping to 25 BTC in epoch 1, 12.5 BTC in epoch 2, and so on.

Blocks on the Bitcoin blockchain are produced roughly every 10 minutes on average, which translates to approximately 144 blocks per day (assuming the standard 10-minute block time). In the current epoch 4, the block subsidy calculation gives 144 × 3.125 = 450 BTC/day, or approximately 164,250 BTC/year.

Halving Events

For a full rundown on what Bitcoin halving is, read our guide! In addition to the definition, we cover the schedule, economic implications, historical impact and more.

By definition, halving is triggered by block height, not by a calendar date. Because real-world block times fluctuate around the 10-minute target, the actual date of each halving drifts. This is why any specific year attached to a future halving should be treated as an approximation tied to a block height, not a fixed event on the calendar.

| Halving (approx. year) | Block height | Subsidy (BTC/block) | Approx. new BTC/day |

|---|---|---|---|

| Genesis era (2009) | 0 | 50 | ~7,200 |

| 1st halving (2012) | 210,000 | 25 | ~3,600 |

| 2nd halving (2016) | 420,000 | 12.5 | ~1,800 |

| 3rd halving (2020) | 630,000 | 6.25 | ~900 |

| 4th halving (2024) | 840,000 | 3.125 | ~450 |

| 5th halving (~2028) | 1,050,000 | 1.5625 | ~225 |

The next expected block reward is 1.5625 BTC per block, projected around 2028 — though, as noted above, the precise date depends entirely on how quickly the Bitcoin blockchain reaches block height 1,050,000.

Timeline to the Final Bitcoin

Bitcoin’s long tail to 2140 is one of the most counterintuitive parts of its monetary design. Because the subsidy halves repeatedly, the inflation rate of new coin creation drops so sharply that the vast majority of all bitcoin will already be mined in the near future. The reward shrinks geometrically, meaning each successive epoch contributes roughly half the coins of the previous one. Eventually, after dozens of halvings, the subsidy in BTC terms becomes incredibly small — and at some point, it rounds down to zero satoshis entirely. That is the functional end of issuance but not the block production.

However, before that milestone is reached:

- By ~2036 (roughly epoch 7), the subsidy will be approximately 0.39 BTC/block, and annual issuance will represent less than 0.1% of the total 21 million supply. At that point you can already say that mining would produce less than one coin per block but daily issuance will still come up to 56.1 BTC per day.

- By ~2048 (approximately epoch 10), the subsidy falls to around 0.049 BTC/block — annual issuance at that point is a negligible fraction of total supply, well under 0.01%.

- By ~2100, the subsidy will have halved more than 40 times, shrinking to a level measured in dozens of satoshis per block. At this stage, the inflation rate of Bitcoin approaches zero in any practical sense, with only a sliver of the total cap remaining to be issued over the following four decades.

How Much Bitcoin Is Already Mined

At the moment of writing, Bitcoin has mined 20,025,953 BTC out of its 21 million hard cap — roughly 95.4% of total supply. Even that mined figure does not equal what can realistically trade hands, because circulating supply strips out provably unspendable and likely lost coins. Estimates suggest up to 1,456,158 of all issued BTC may be permanently inaccessible, meaning effective supply is meaningfully lower than the on-chain issued total.

For clarity, current supply from here on will refer to issued bitcoins and circulating supply will be used for current supply without the “lost” coins.

Lost Bitcoins

Bitcoins that can no longer, well, circulate come in three categories:

- Provably unspendable: Coins sent to addresses constructed from invalid or burn scripts (e.g., OP_RETURN outputs or known burn addresses). These are cryptographically guaranteed to be unspendable and are sometimes excluded from supply counts entirely.

- Inaccessible: Coins whose private keys existed at some point but are no longer recoverable — for instance, keys on a destroyed hard drive or with a forgotten passphrase. The coins sit in a valid address but no one can sign a transaction to move them.

- Lost: A broader, informal term covering both inaccessible coins and coins whose owners are simply unknown or unreachable. In practice, analysts use “lost” to cover anything that has not moved in years and shows behavioral signals of abandonment.

According to River, up to approximately 20% of all issued BTC may fall into lost or inaccessible categories, which would place genuinely effective circulating supply well below the issued figure.

Why do these losses happen?

- Lost private key or seed phrase: The most frequent cause. A user neglects to keep their 12- or 24-word seed phrase secure or fails to back it up, and the phrase is later irretrievable.

- Deceased owner without an inheritance plan: No seed phrase handoff means heirs have no access, even if the wallet balance is publicly visible on-chain.

- Accidental burn addresses: Coins sent to addresses that are technically valid in format but belong to no one — sometimes due to typos or malformed address generation.

- Early wallet and key management mistakes: Bitcoin’s early years predated robust wallet standards. Many keys generated between 2009 and 2012 were stored in informal formats and subsequently lost.

- Forgotten passphrases: A BIP39 passphrase (sometimes called the “25th word”) added on top of a seed phrase creates a completely separate wallet. Forgetting it locks the coins just as effectively as losing the seed entirely.

- Destroyed storage media: Hard drives, USB sticks, and paper wallets have finite lifespans. Physical destruction or data corruption eliminates access permanently.

Lost coins reduce effective Bitcoin supply and may amplify scarcity effects as demand grows but they do not alter the 21 million protocol cap in any way.

“The Final Block” and the Post-Subsidy Era

It’s worth reiterating: what is commonly referred to as “the final block”, expected sometime in 2140, is not actually the last block the Bitcoin blockchain will see produced but the last one that will issue the block subsidy. By the 2030s and 2040s, the amount of newly minted BTC per block will be so small as to be economically negligible long before the protocol reaches its hard stop.

End of New Supply

What exactly stops and doesn’t stop at the final block?

- No new BTC minted via block subsidy. The coinbase transaction, which is the special first transaction in every block that creates new coins and assigns them to the Bitcoin miner, simply stops carrying a subsidy output. The coinbase transaction itself still exists — it just no longer generates fresh satoshis from protocol issuance.

- Miners can still collect fees via the coinbase transaction. Transaction fees accumulate from every included transaction and are claimed through that same coinbase mechanism. The collection infrastructure remains intact, only the subsidy component disappears.

- The 21 million BTC supply cap continues to be enforced by full nodes. Every node on the network independently validates consensus rules on every block. No single party can override the cap — it is a rule embedded in the code that every participant in the network has chosen to run.

In the post-subsidy era, miner compensation comes exclusively from fees, although it would already be a century since the subsidy had been a primary source of miner income. Without a subsidy cushion, users competing for block space will see the direct cost of transaction processing reflected in real time, without any subsidy-driven masking of the true market rate. The total value paid to Bitcoin miners to verify transactions and secure the chain will depend entirely on what the fee market generates.

Fee-Only Miner Revenue

In the post-subsidy era, the miner revenue per block simply becomes the sum of transaction fees of all included transactions.

On a technical level, a Bitcoin transaction fee is the difference between a transaction’s inputs and its outputs. That gap, which users leave unspent (as in “unspent UTXOs”), is claimed by the Bitcoin miner who includes the transaction in a block. Bitcoin miners scan the mempool — the holding area for unconfirmed transactions — and select which transactions to include, typically prioritizing those offering the highest fee per unit of block space, measured in satoshis per virtual byte (sat/vB).

When the block reward is gone, that selection process becomes the entire economic story. Miner income becomes directly variable and demand-driven: a congested network during a high-activity period could yield a lucrative block, while a quiet period with sparse transaction volume could yield something far more modest.

That brings us to the practical question: how does the fee market actually discover prices, and what conditions push fees up or down?

Transaction Fee Market

Transaction fees on the Bitcoin blockchain aren’t flat or percentage-based; neither are they set by any central authority. They emerge from competition: users bidding for limited blockspace, and Bitcoin miners choosing which transactions pay enough to justify inclusion.

The unit you encounter in practice is the fee rate, expressed in sat/vB. This is distinct from the absolute fee paid on a transaction — a larger transaction measured in virtual bytes can pay a higher total fee while targeting the same sat/vB as a smaller one. Suppose Transaction A is 200 vB and Transaction B is 400 vB. If both target 10 sat/vB, Transaction A pays 2,000 satoshis total while Transaction B pays 4,000 satoshis. Both carry the same fee rate, but the Bitcoin miner collecting them earns more from B in absolute terms, even though both transactions are equally “competitive” from a priority standpoint.

Bitcoin block weight is constrained by protocol rules, which caps the amount of data that can be confirmed in any single block. Bitcoin miners therefore sort mempool transactions by fee rate and select those that maximize total fee revenue within that weight limit. Users who want faster confirmation bid higher sat/vB; those who can wait submit lower-rate transactions and may sit in the mempool until congestion clears.

Here is the deal, though: transaction fees currently account for roughly 0.63% of total miner revenue and haven’t exceeded 3% in a year. Moving that figure toward 100% is not a small adjustment.

High-fee conditions, driven by high demand for transaction priority and quicker settlement, can emerge in bull markets or volatile conditions. For more persistent demand for block space that would not rely on harsh market repricing, a possible path is wider adoption of Bitcoin for smaller but more frequent payments.

This scenario is at odds not just with the disinflation by design; scaling through Layer-2 solutions also shifts block space demand from fees directly paid by users to payments settled on their behalf. The fee market is not eliminated by scaling solutions: in a scaled Bitcoin ecosystem, on-chain blockspace becomes premium real estate reserved for settlement actions. Mass settlement events, like many Lightning channels closing simultaneously during a market crisis, can recreate high-fee conditions quickly, as a sudden burst of on-chain settlement transactions competes for the same limited blockspace; this scenario, however, circles back to certain market conditions rather than a consistent revenue stream.

Network Security and Consensus After 2140

That raises the question: won’t miners just stop if they no longer are able to profit from validating Bitcoin? And therefore, what will become of the network’s security?

Incentive Model

Under the incentive model fully dependent on transaction fees, a couple of feasible scenarios emerge. First, sustained low fee demand can push marginal miners offline, stretching confirmation times until cryptocurrency difficulty adjusts downward. This mechanism ensures that blocks still meet the 10-minute target time to be produced, no matter how high or low the hash rate is. Second, fee volatility can create power-cycling behavior, or motivate miners to redirect SHA-256 hardware toward other cryptocurrencies that use the same algorithm.

Hashrate and Attack Costs

Regardless, both scenarios see miners leave the network, which leads to reduced hash rate. This metric, the total computing power doing the “work” (as in Proof-of-Work), is believed to be the most direct measurement of the network’s security against consensus attacks (e.g. a 51% attack).

It needs to be said that the attack cost against the Bitcoin blockchain has three components: acquiring or leasing sufficient hashpower, paying electricity to sustain it, and the opportunity cost of foregone honest mining revenue. In the fee-only era, that third component is dominated entirely by expected transaction fees rather than subsidy, tying attack economics more directly to network usage. If it gets cheaper to amass 51% of the hash rate than use it to mine blocks honestly and reap the benefits, that’s where issues start.

In a high on-chain demand environment, mempools push fees upward, miner revenue climbs, hashrate stabilizes or grows, and attack costs remain prohibitive. In a low-demand environment, fees compress, marginal miners exit, hashrate declines, and attack costs fall proportionally. These are observable in real time through mempool depth, average fees, and hashrate trends.

One mitigation path belongs specifically here: the settlement layer dynamic. Bitcoin doesn’t need massive transaction count to sustain meaningful fee revenue if each transaction carries high value. Fewer, higher-value settlements can still support a robust security budget.

Difficulty Retargeting

Coming back to difficulty, its retargeting mechanism adjusts approximately every 2,016 blocks based on how long those blocks actually took to mine, targeting an average of roughly 10 minutes per block. It works identically in the fee-only era and acts like an automatic stabilizer when miner behavior shifts.

If many Bitcoin miners exit quickly, block times stretch until the next retarget corrects downward. The network doesn’t break, albeit it is going to run slower for up to two weeks. For users, confirmation counts matter more than time estimates during these windows.

Nevertheless, block difficulty does not compensate for lost hash rate. Although the target times can eventually return to normal, the cost of attack on the network will reduce or increase proportionally to the hash rate, not difficulty.

The good news is, if fee pressure creates incentives for miners to include unusual transaction types or adopt policies that benefit their revenue, full nodes running unmodified consensus rules will reject any invalid block regardless of how much fee revenue it contains. Fee-only incentives increase revenue motive, not protocol authority. Rule enforcement sits with the full node network, not with hashrate.

Economic and Price Implications of a Fixed Supply

Surprise: it’s not only the miners that Bitcoin’s monetary policy affects. The network-level story — fees, hashrate, security budget — is only half the picture. The other half is market structure: how BTC is valued, traded, and held when new supply becomes negligible.

Deflation and Disinflation

The elephant in the room is disinflation. Unlike deflation, which is an overall contraction in the volume of circulating money, this describes a situation when inflation, an increase in the volume of money, contracts. If it was too complicated, disinflation is falling inflation. Some even argue that as more bitcoins become lost coins, the network will even experience deflation in the most literal sense of the word. But isn’t it supposed to be good if the main goal of your asset is store of value?

Clearly, since Bitcoin was designed with disinflation in mind, there is merit to that choice. Demand for Bitcoin becomes the primary driver of its purchasing power when the variance in supply is entirely eliminated if we use the law of supply and demand. But “demand for Bitcoin” is exactly the critical condition.

When holders expect appreciation, BTC velocity tends to fall. Why would I spend Bitcoin if it is going to be worth more in the future? Spending can still happen for BTC-denominated settlement obligations, emergencies, business cash flow, but it remains to be seen whether the rise in purchasing power (simply put, the price tag) can keep up with suppression of velocity caused by hoarding.

Liquidity Constraints

Holders may have no problem with BTC rising in price until they would want to cash out. A fixed and shrinking effective float doesn’t automatically create deep markets, to put it lightly.

Bitcoin’s divisibility into satoshis helps with unit-of-account and small denominations, but it does not create depth: a market can be denominated in satoshis and still have thin order books.

Supply Constraints

Bitcoin’s supply is structurally inelastic. Commodities respond to price via increased production; Bitcoin does not. Whether BTC trades at $10,000 or $1,000,000, the Bitcoin blockchain issues new coins only on schedule; it’s predictable and some may argue that it is already priced in but it does no favors to liquidity, regardless.

In a near-zero-issuance world, secondary supply becomes the only supply-side variable — which is why sentiment can move price even more sharply than when issuance is still in the picture in both directions.

Conclusion

A moment of the last satoshi halving away is going to be long, long after the effects of the fee market will have reshaped Bitcoin mining. Instead of asking “what happens after the last Bitcoin is mined”, your question should be “how would mining be sustained with most revenue coming from fees, not block subsidy” because while the former is still more than a century away, it will take us a couple of decades to arrive in the second reality.

Frequently Asked Questions

When will all bitcoins be mined?

All bitcoins are projected to be fully mined around the year 2140, though that date is an approximation, not a fixed deadline. Bitcoin’s issuance schedule is governed by halvings — roughly every four years, the block subsidy (block reward) paid to Bitcoin miners is cut in half, creating a long tail of diminishing new BTC entering circulation. The final satoshis will be issued only after approximately 33 more halving events.

Will Bitcoin stop working after the last bitcoin is mined?

Bitcoin is not supposed to stop working after the last bitcoin is mined: the Bitcoin blockchain continues operating indefinitely through transaction fees alone. Bitcoin miners post-subsidy still assemble blocks, order and include transactions, and earn transaction fees from users. Block production does not stop; the incentive structure shifts.

Will transaction fees replace block rewards?

Transaction fees are intended to replace the block subsidy as the primary revenue source for Bitcoin miners, though whether they will be sufficient as a security budget is a separate question. Each time a user sends BTC, they attach a fee to incentivize miners to include their transaction. As block subsidies shrink with each halving, fees make up a larger share of miner revenue. Fees can replace block subsidies as a revenue source in accounting terms. Whether that fee revenue is large enough to sustain current levels of network security is a distinct question that depends on blockspace demand over time.

Will transaction fees increase after the last bitcoin is mined?

Transaction fees are likely to increase under certain conditions, but multiple forces push in both directions, making a single forecast unreliable. Spikes in blockspace demand (more users competing for limited block space) can push the fee higher and migration to L2s, transaction batching, and improved fee estimation tools reducing overpayment and bidding wars can reduce the fees for users and revenue for miners.

“Fees increasing” can mean two different things — absolute fee in satoshis per transaction, or fee rate measured in sats per virtual byte (sats/vB). These can move in opposite directions depending on transaction complexity and network conditions. Fee market outcomes depend heavily on continued Bitcoin adoption growth and Layer 2 maturity. Neither is guaranteed on any particular timeline.

Will Bitcoin be more deflationary after 2140?

After 2140, Bitcoin’s protocol issuance rate will reach exactly zero, meaning no new BTC will enter circulation — but that is a supply schedule fact, not a guarantee of price deflation or appreciation. “Deflationary” in this context means the issuance inflation rate drops to 0% — the protocol stops creating new BTC entirely. This is distinct from purchasing power or price deflation, which depends on demand, adoption, and macroeconomic conditions outside the protocol.

Scarcity is a necessary but not sufficient condition for value. The Bitcoin supply schedule guarantees scarcity but not any particular market outcome.

What happens if too many bitcoins are lost?

If too many bitcoins are permanently lost, the accessible circulating supply shrinks. BTC is locked to a specific address controlled by a private key. If that key is destroyed, lost, or never recorded, the coins at that address become permanently inaccessible; current estimates suggest somewhere between 3 million and 4 million BTC may already be permanently lost. Bitcoin has no recovery function — there is no central authority or protocol mechanism to reassign lost funds, at least yet.

Can the 21 million cap on Bitcoin supply be changed?

The 21 million BTC cap can technically be changed, but doing so would require a consensus rule change of extraordinary difficulty and would face near-universal resistance.

Raising the cap would necessitate a hard fork: a change to Bitcoin’s consensus mechanism that is not backward compatible. It would need to be adopted by the economic majority: Bitcoin miners, node operators, exchanges, businesses, and individual users. Without that broad adoption, the fork produces a competing chain, not a replacement.

Bitcoin’s scarcity is foundational to its store-of-value narrative. Holders, miners, and businesses have made financial decisions premised on a fixed supply. Diluting that supply undermines the expectation anchoring that gives BTC a large part of its perceived value — a strong incentive for stakeholders to reject any such proposal.

The 21 million cap is not enforced by a single entity but by every node running the current consensus rules. Changing it requires convincing the entire network simultaneously, which is an extraordinary coordination challenge with no realistic path in current conditions.