What is Crypto Tokenization? A Beginner’s Guide

Disclaimer

This article is not a piece of financial advice. When dealing with cryptocurrencies, remember that they are extremely volatile and thus, a high-risk investment. Always make sure to stay informed and be aware of those risks. Consider investing in cryptocurrencies only after careful consideration and analysis and at your own risk.

Contents

- 1. What is Crypto Tokenization?

- 2. How Crypto Tokenization Works

- 3. Real World Asset (RWA) Tokenization Deep Dive

- 4. Creating a Tokenized Asset

- 5. Examples and Use Cases of Crypto Tokenization

- 6. Benefits of Crypto and Asset Tokenization

- 7. Infrastructure for Tokenized Assets

- 8. Regulatory Landscape by Jurisdiction

- 9. Integration with Traditional Finance

- 10. Challenges and Risks of Tokenization

- 11. The Future of Crypto Tokenization

Put simply, tokenization in crypto is like turning a deed to a house into a digital certificate you can store in your wallet, trade instantly, or even split with other people. Instead of dealing with paper contracts and middlemen, you get a blockchain-based token that represents your share of something valuable—whether that's real estate, fine art, stocks, or even Treasury bonds.

Tokenization aims to fundamentally change how we own, trade, and access assets and open up markets that were previously locked behind high entry costs or geographic barriers. Real world asset tokenization crypto projects are already turning physical assets into digital tokens that anyone can buy, sell, or hold—often without going through traditional banking channels.

Throughout this guide, you'll learn exactly how crypto tokenization works, what types of assets can be tokenized, how real estate tokenization crypto projects are reshaping property investment, and what makes RWA tokenization crypto different from standard digital assets. You'll also explore the technical infrastructure, regulatory landscape, and real-world use cases driving adoption today.

Definition and Importance

This guide is a deeper dive into the concept or tokenization; for a shorter article with the crypto tokenization definition, see the page in our glossary.

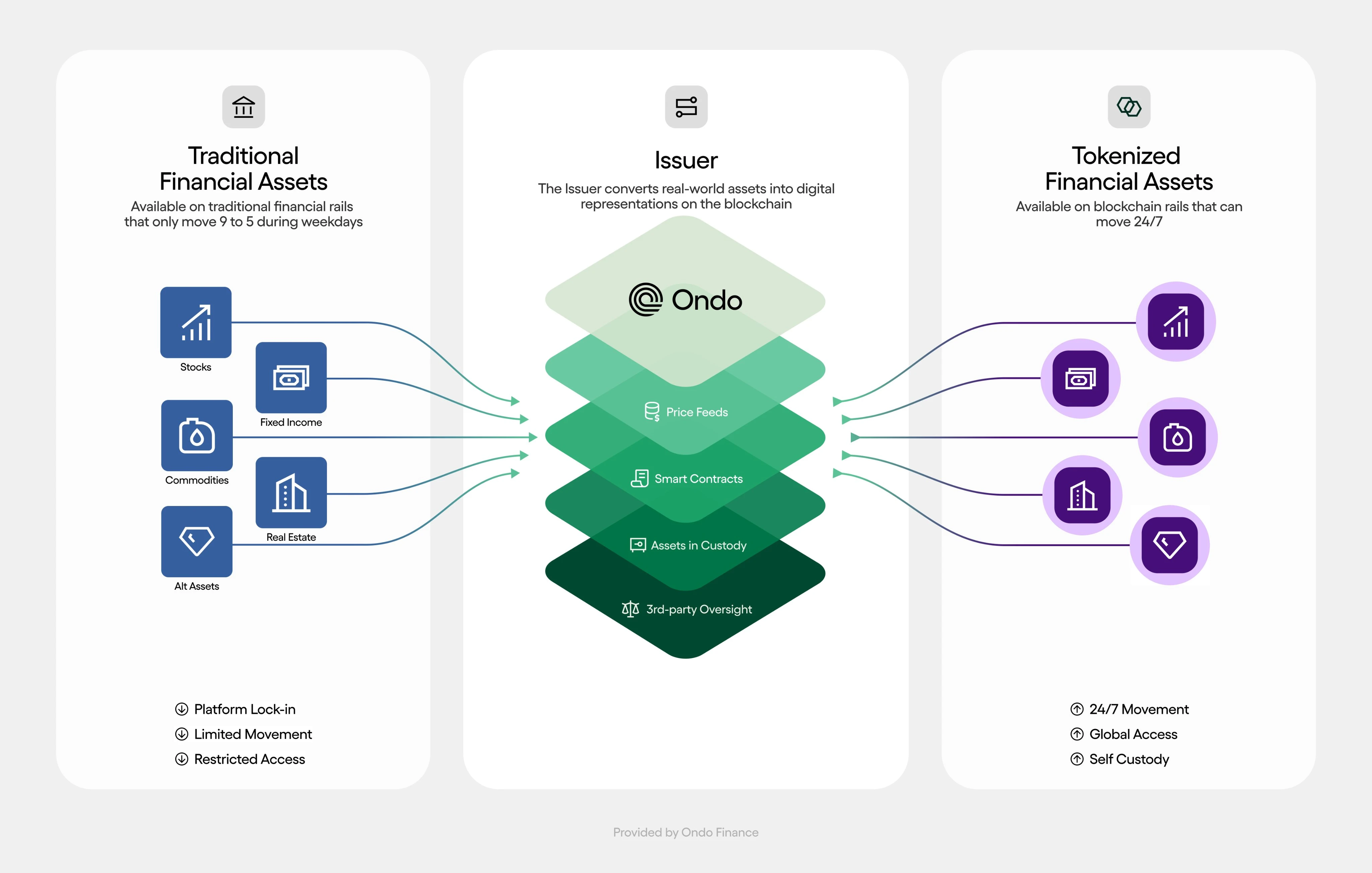

Tokenization is the process of converting rights to an asset—whether physical, digital, or financial—into a digital token that exists on a blockchain. Turning a paper document into this token is like turning a real estate deed or a share certificate into a digital format that's traceable, transferable, and programmable. Each token represents ownership or a specific right tied to the underlying asset, secured by blockchain technology.

In comparison, traditional asset ownership involves intermediaries, paper trails, and slow transfer processes. Tokenization removes these friction points by creating a digital representation that can be transferred instantly, tracked transparently, and verified without a central authority. The blockchain records every transaction in an immutable ledger, meaning the ownership history is permanent and tamper-proof.

So, tokenization turns assets into programmable digital units that can be bought, sold, or traded on blockchain networks. This applies to everything from real estate tokenization crypto projects to tokenized stocks, art, or even intellectual property. The token itself doesn't hold the physical asset but the verifiable rights to that asset.

How Tokenization Works

How is that effect achieved? Tokenization transforms physical or digital assets into blockchain-based tokens through three foundational layers: the blockchain infrastructure itself, smart contracts that define token behavior, and operational processes that bring tokens to life.

At a high level, the process looks like this:

- Identify and legally structure the asset you want to tokenize (for example, a property or a bond).

- Create a legal link between the token and the underlying ownership rights.

- Deploy smart contracts on a chosen blockchain to define token supply, rules, and permissions.

- Mint tokens representing the asset and distribute them to investors or users.

- Manage ongoing operations—transfers, payouts, and compliance—through a mix of smart contracts and off-chain processes.

The impact is straightforward but powerful: assets that once required lawyers, notaries, and weeks of paperwork can now be represented by tokens that move globally in minutes with transparent, verifiable records.

What is Crypto Tokenization?

Although this distinction is often implied in the conversation around tokenized assets in sources like our blog, let’s spell it out anyway. Crypto tokenization is simply tokenization that uses blockchain as its base layer. Instead of updating ownership records in private databases or government ledgers, you record them on a distributed ledger shared across many nodes.

Definition of Tokenization in Blockchain

Each token that represents an asset on a blockchain is:

- Traceable: Every transfer is recorded on-chain.

- Transferable: Tokens move directly between wallets without intermediaries.

- Programmable: Smart contracts can automate behavior like payouts, voting, or transfer restrictions.

This programmable nature is the big difference from a PDF of a share certificate or a scanned deed. With public blockchains as rails, tokens can interact with DeFi protocols, enforce compliance rules automatically, and plug into a broader Web3 ecosystem.

Tokens vs Cryptocurrencies

Here's where beginners might get confused: tokens and cryptocurrencies are not the same thing, even though both exist on blockchains.

Cryptocurrencies like Bitcoin or Ethereum are native to their own blockchains and can also be called coins. Bitcoin operates on the Bitcoin blockchain, Ethereum on the Ethereum blockchain. These are designed primarily as digital currencies or stores of value. They power their respective networks and are used to pay transaction fees (known as gas fees).

Tokens, on the other hand, are built on top of existing blockchains using established standards. For example, a real world asset tokenization crypto project might issue tokens on Ethereum using the ERC-20 standard. These tokens don't have their own blockchain—they borrow Ethereum's infrastructure. Some tokens can act as cryptocurrencies if they have properties of money but these tokens in question do not.

What can tokens represent? Applications are diverse: ownership in a building, voting rights in a DAO, access to a service, or fractional shares of a company.

Security Tokens, Utility Tokens, and Other Types of Tokens

Tokens themselves come in different flavors, each designed for a specific purpose. Before navigating tokenization crypto projects, let’s take a moment to sort these concepts out.

- Security tokens represent ownership in a real-world asset or company. They function like traditional securities—stocks, bonds, or real estate shares—but in digital form. These tokens are often subject to securities regulations, meaning they may require compliance with KYC (Know Your Customer) and AML (Anti-Money Laundering) rules. Security tokens are the main type applied in RWA tokenization crypto, where assets like treasury products or real estate are digitized.

- Utility tokens grant access to a product or service within a blockchain ecosystem. They're not designed primarily as investments but as functional tools. Think of them like digital arcade tokens—you use them to access features, pay for transactions, or unlock platform benefits. Utility tokens don't carry ownership rights in a company or asset, which generally keeps them outside strict securities regulations (though this varies by jurisdiction)—at least, on paper.

- Non-fungible tokens (NFTs) are unique tokens that represent one-of-a-kind digital or physical items. As opposed to fungible tokens where one token equals another, each NFT is distinct. They're commonly used for digital art, collectibles, or proof of authenticity.

- Governance tokens give holders voting power in decentralized protocols. These tokens let communities decide on protocol upgrades, treasury allocations, or strategic decisions. They're a core feature of DeFi (Decentralized Finance) platforms.

What’s important for this guide is RWA tokens are typically security tokens that bridge traditional finance with blockchain technology. They allow fractional ownership of high-value assets—like real estate or commodities—making previously illiquid markets accessible to everyday investors.

How Crypto Tokenization Works

Tokenization becomes real when you combine blockchain infrastructure, smart contracts, and operational processes. Let’s break down each layer.

Underlying Blockchain Technology

Unlike traditional databases controlled by a single entity, blockchain operates without a central authority, making it transparent and tamper-resistant. When you tokenize an asset, you're creating a digital representation on one of these blockchain networks.

Ethereum dominates the real world asset tokenization crypto landscape, with the total value locked in RWA protocols surpassing $15 billion as of March 2026. This isn't surprising—Ethereum's mature ecosystem, developer tools, and established security make it the go-to choice for tokenization crypto projects.

But Ethereum isn't alone. Other blockchains like Polygon, Solana, Avalanche, and specialized networks also support tokenization, each offering different trade-offs between speed, cost, and security. The common ground is that all these blockchains provide immutable record-keeping. Once a token is created and transactions are recorded, they cannot be altered or deleted.

Smart Contracts and Token Standards

Smart contracts are self-executing programs stored on the blockchain. They automatically enforce rules without intermediaries—think of them as vending machines for digital assets. You input specific conditions, and the contract executes actions when those conditions are met.

For tokenization, smart contracts define everything about your token: how many exist, who can transfer them, what rights they represent, and how they behave in different scenarios. Token standards ensure these smart contracts follow predictable patterns that wallets and exchanges can recognize.

The most popular standards include:

- ERC-20: The standard for fungible tokens. Each token is identical and divisible.

- ERC-721: The original NFT standard for non-fungible tokens.

- ERC-1155: A hybrid standard that can handle both fungible and non-fungible tokens within the same contract. This flexibility reduces deployment costs and complexity for projects managing multiple asset types.

BlackRock's launch of its first tokenized fund, BUIDL, on the Ethereum network demonstrates how institutional players trust these standardized frameworks for managing real assets.

Real World Asset (RWA) Tokenization Deep Dive

Now that the fundamentals are clear, it’s time to zoom in on real world asset tokenization—the part of the market that’s bringing traditional finance directly onto blockchains.

What is RWA in Crypto?

Real world asset tokenization in crypto refers to the process of converting ownership rights of tangible, physical assets—like real estate, commodities, bonds, or artwork—into digital tokens on a blockchain. In simple terms, RWA tokenization bridges the traditional financial world with the crypto ecosystem by representing real-world value on-chain.

Most crypto assets (like Bitcoin or Ethereum) derive their value from network effects, technology, or speculation. RWA tokens work differently. They're backed by actual, verifiable assets that exist outside the blockchain. A tokenized Treasury bond represents a claim on a real U.S. government security; a tokenized property represents fractional ownership in an actual building.

What Makes RWA Different from Other Crypto Assets

RWA tokens operate fundamentally differently than native cryptocurrencies or purely digital assets since they derive their value from something tangible and legally enforceable outside the blockchain.

While a token like UNI grants governance rights within a protocol, and Bitcoin functions as a decentralized digital currency, an RWA token represents a legal claim on a real asset. This means RWA tokenization crypto projects must navigate regulatory frameworks, custodial requirements, and legal ownership structures that purely digital assets don't face.

Another critical difference: RWAs bring real-world economic activity onto blockchain rails.

RWA tokens also offer relative stability. Because they're backed by real assets with established valuation methods, they tend to be less volatile than purely speculative crypto assets. This makes them attractive to risk-averse investors and institutions looking for blockchain benefits without extreme price swings.

Creating a Tokenized Asset

Creating a tokenized asset involves more than just writing smart contract code—it’s a multi-layered process that requires careful planning, legal groundwork, and technical precision.

Identifying and Structuring the Underlying Asset

The first step is defining exactly what you're tokenizing. Start by evaluating the asset's characteristics: Is it tangible (like real estate) or intangible (like intellectual property)? Is it easily divisible, or does it require a specific ownership structure?

For real estate tokenization crypto projects, this means conducting property appraisals, verifying ownership rights, and determining how fractional shares will work. For tokenized securities, you'll need to structure rights clearly—what do token holders actually own? Equity? Debt? Profit shares? Something else entirely?

The key question is: What rights transfer with the token? That clarity matters, both legally and for market confidence.

Photo by Troy Mortier on Unsplash

Think of this phase as creating a blueprint. It’s not building yet but mapping out exactly what the final product represents and how it connects to the real-world asset is important nonetheless.

Choosing the Blockchain and Token Standard

Once the asset structure is clear, you select the blockchain and token standard. This decision impacts liquidity, compliance capabilities, and long-term interoperability.

When choosing, consider:

- Compliance features: Does the blockchain support KYC/AML enforcement or compliant transfer controls?

- Transaction costs: High gas fees on Ethereum may drive projects to Layer 2 solutions or alternative chains.

- Liquidity: Where will secondary trading happen? Pick the ecosystem with existing RWA liquidity.

- Interoperability: Can the token move across chains if needed?

This decision isn't always permanent—many projects deploy on one chain initially and bridge to others later. But starting with the right foundation saves headaches down the road.

Legal, Regulatory, and Compliance Setup

Things get serious even before deployment. Tokenization projects must navigate a complex regulatory landscape that varies by jurisdiction and asset type.

Key compliance steps include:

- Securities classification: Determine if your token qualifies as a security under the Howey Test (U.S.) or equivalent frameworks elsewhere. The U.S. SEC is often described as using a "regulation by enforcement" approach, which creates ongoing uncertainty for tokenization crypto projects.

- Licensing requirements: Security tokens typically require broker-dealer licenses or exemptions (like Reg D, Reg A+, or Reg S in the U.S.).

- KYC/AML implementation: Build identity verification into token issuance and transfers. Most institutional platforms require this.

- Investor accreditation: Verify accredited investor status where required.

- Disclosure documents: Prepare offering memoranda, risk disclosures, and financial statements—just like for traditional securities.

- Custody and transfer restrictions: Implement smart contract rules that enforce regulatory transfer restrictions.

The EU's Markets in Crypto-Assets (MiCA) regulation provides clearer guidelines than the U.S. framework, potentially making Europe an attractive jurisdiction for compliant tokenization. MiCA establishes rules for token issuers and crypto service providers, reducing regulatory ambiguity.

Legal experts who understand both securities law and blockchain are the best choice to plan and implement this step of a project. After all, this intersection is where most projects encounter unexpected issues.

Issuance, Distribution, and Lifecycle Management

The final step is launching your tokenized asset and managing it over time. This breaks down into distinct phases:

- Issuance: Deploy the smart contract, mint tokens according to the predetermined structure, and conduct security audits. Institutional projects almost always undergo third-party smart contract audits before launch to catch vulnerabilities.

- Distribution: Decide how tokens reach investors. Options include:

- Private placements to institutions

- Public token offerings (subject to securities rules)

- Secondary market listings on compliant exchanges

- Over-the-counter (OTC) sales

- Ongoing management: Tokenized assets aren't "set and forget." You'll need to handle:

- Corporate actions (dividends, profit distributions, buybacks)

- Compliance monitoring (ongoing KYC, transaction surveillance)

- Smart contract upgrades (if regulations or business needs change)

- Investor communications and reporting

Naturally, lifecycle management also means maintaining the connection between the token and underlying asset. If you've tokenized real estate, you'll manage property maintenance, rent collection, and potentially property sales—while ensuring token holders receive their proportional share.

The goal is to build a sustainable, transparent process that maintains asset value and regulatory compliance throughout the token’s lifecycle.

Examples and Use Cases of Crypto Tokenization

Asset Tokenization Examples

Real world asset tokenization crypto spans a wide range.

- US Treasury bonds are the largest category. As of Q1 2026, tokenized Treasury products account for 28% of the RWA market value. These tokens let investors buy fractional shares of government bonds on-chain, earning yields without dealing directly with traditional brokers.

- Commodities like gold, oil, and agricultural products can be tokenized to improve liquidity and reduce custody friction. A farmer could tokenize future crop yields to raise capital before harvest—the blockchain version of a forward contract.

- Art and collectibles often use NFTs to represent ownership or fractional stakes in high-value pieces. This opens up investment opportunities that were once limited to auction houses and a small pool of wealthy collectors.

- Equities and corporate bonds are beginning to appear in tokenized form, as institutions look to reduce settlement times and expand investor access.

Real Estate Tokenization

Real estate tokenization crypto is one of the most practical applications of blockchain technology. Property is traditionally illiquid—you can't easily sell half a building. Tokenization attempts to change that.

Here’s the idea: a property owner creates digital tokens representing ownership shares. Investors buy these tokens, which give them fractional ownership and a proportional share of rental income or property appreciation. Smart contracts automate income distributions, significantly reducing administrative overhead.

Several platforms have successfully tokenized commercial properties, allowing retail investors to own fractions of high-value real estate with relatively low minimum investments. While specific performance varies, the general approach shows how tokenization can democratize access to markets that typically require large capital commitments.

The benefits are clear: lower entry barriers, improved liquidity through secondary trading, and transparent, on-chain records of ownership and payouts.

Current Tokenized Asset Landscape

What is RWA in crypto today? The landscape is dominated by fixed-income products, particularly US Treasuries. Ethereum hosts the majority of RWA activity.

Beyond Treasuries, there is growth in:

- Private credit tokens representing loans to businesses

- Carbon credit tokens for emissions trading

- Invoice financing tokens that let companies raise capital against outstanding invoices

- Commodity-backed stablecoins pegged to physical reserves

Most projects still cluster around Ethereum due to its mature tooling and DeFi integrations, but other blockchains are competing on speed and cost.

Future Tokenized Asset Use Cases

The future of real world asset tokenization crypto extends well beyond what exists today.

- Intellectual property: Music royalties, film rights, or patents could be tokenized, letting investors own fractions of future revenue. Imagine collecting a share of your favorite artist’s streaming income via tokens.

- Infrastructure projects: Toll roads, data centers, or renewable energy plants could raise capital through token sales, distributing revenues to token holders instead of relying only on traditional bonds.

- Supply chain tokenization: Goods could be tracked from manufacturer to end customer, with tokens representing ownership and custody changes. This would add transparency and reduce fraud in global trade.

- Personal assets: Cars or luxury goods could be tokenized and used as collateral in peer-to-peer lending markets, letting you borrow against assets without selling them.

The key enabler behind all these use cases is composability: once assets exist on-chain as tokens, they can plug into lending, trading, and other DeFi protocols in ways that traditional ownership models simply don’t allow.

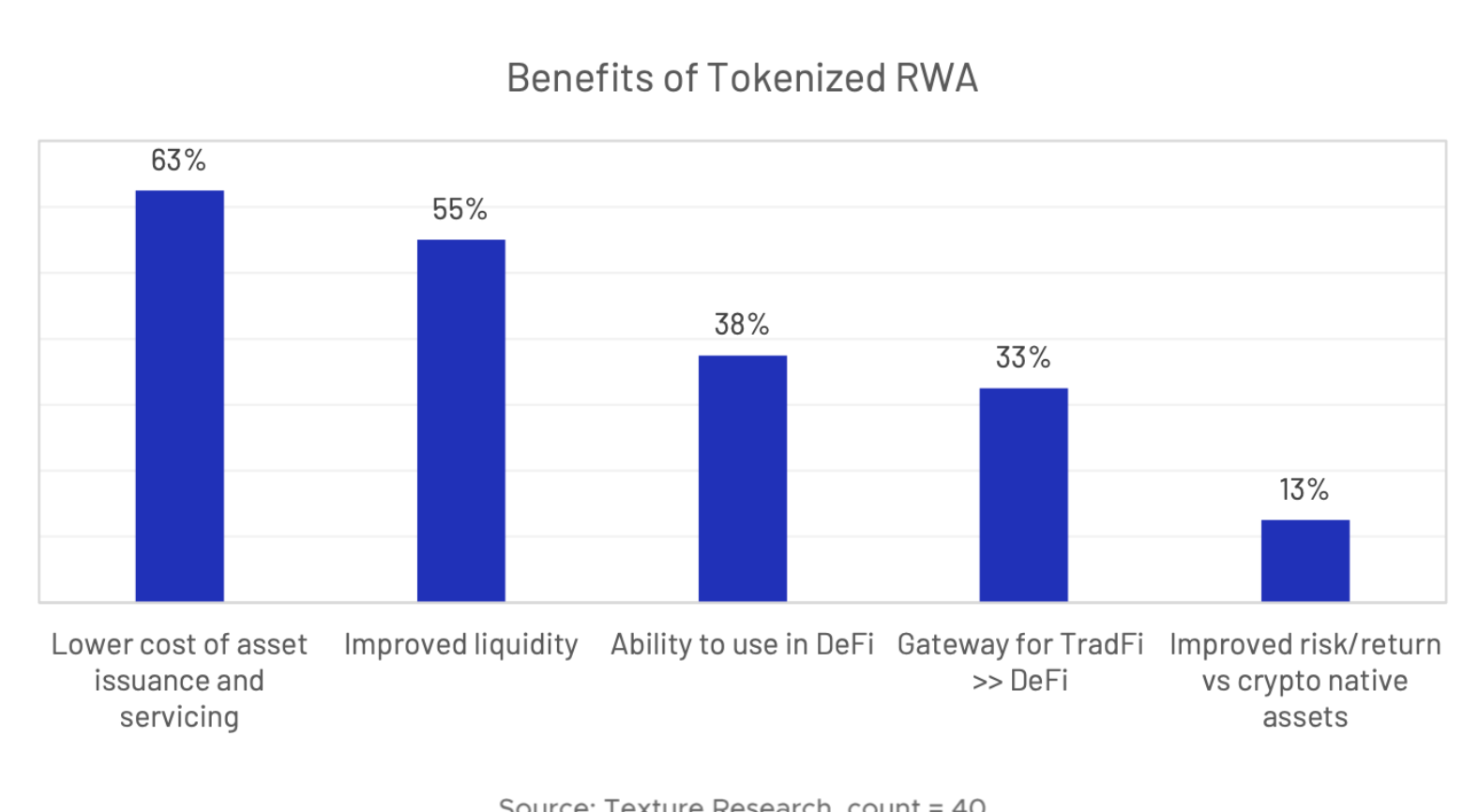

Benefits of Crypto and Asset Tokenization

Tokenization is put forward as an application of technology to address several core limitations of traditional markets. Let’s break down the main benefits for owners, investors, and platforms.

Liquidity Enhancement

Traditional assets like real estate, fine art, or private equity shares are notoriously illiquid. Selling a property can take months, and finding a buyer for a $5 million painting requires specialist intermediaries.

Tokenization changes this by creating digital representations that can trade 24/7 on secondary markets. A $10 million commercial property divided into 10,000 tokens means investors can buy or sell smaller portions whenever they want, instead of waiting for a single buyer for the entire asset.

The key advantage is constant price discovery. Sellers can exit positions more flexibly, and buyers can enter with smaller tickets, improving market efficiency.

Accessibility and Fractional Ownership

Secondly, tokenization democratizes access to high-value investments that were historically limited to wealthy individuals or institutions. Instead of needing $500,000 to enter commercial real estate, you might need $500 for a fractional token representing the same property.

By expanding the investor base, real estate tokenization crypto projects let everyday investors build diversified portfolios across multiple properties, geographies, and asset classes. Someone in Singapore can own a fraction of a Berlin office building and a slice of tokenized US Treasuries in the same portfolio.

More participants mean more capital for asset owners and more options for investors.

Transparency and Immutability

Blockchain creates permanent, transparent records for every tokenized asset. Each transaction, ownership transfer, and contract action gets recorded on-chain where it can be independently verified.

Traditional records live in siloed databases: property registries, broker systems, and internal ledgers. Verification is slow and error-prone. With tokenization, the blockchain becomes the single source of truth. Smart contracts automatically enforce rules around ownership transfers, distributions, and compliance.

For investors, this means clearer provenance, fewer disputes, and less reliance on opaque intermediaries.

Composability and Interoperability

Source: STRENGTHENING AMERICAN LEADERSHIP IN DIGITAL FINANCIAL TECHNOLOGY, Executive Order 14178 of January 23, 2025

Here is when it keeps getting even more interesting. Tokenized assets integrate naturally with DeFi protocols and Web3 applications. A tokenized real estate share can be:

- Used as collateral in lending protocols

- Added to liquidity pools

- Wrapped and bridged to other chains

- Combined with other tokens in structured products

This composability is unique to blockchain. RWA tokenization crypto projects are already experimenting with these integrations, effectively merging traditional asset value with DeFi innovation.

Ethereum’s dominance in this space is no accident: its ecosystem of protocols and standards makes these cross-protocol interactions practical today.

Infrastructure for Tokenized Assets

Under the hood, successful tokenization relies on the right blockchains, data connections, and interoperability tools.

Popular Blockchains for Tokenized Assets

Not all blockchains are equally suited for tokenization.

- Ethereum is the current heavyweight, hosting the majority of RWA tokenization crypto projects. It offers strong security, established token standards, and deep DeFi integrations.

- Polygon provides lower transaction costs while maintaining compatibility with Ethereum, making it attractive for high-frequency or smaller-value token trades.

- Avalanche and Solana compete on speed and scalability, appealing to use cases that demand fast finality and high throughput.

- Hyperledger Fabric and Corda serve permissioned or enterprise contexts where controlled access, privacy, and consortium governance are more important than public composability.

Choosing a chain is largely about balancing transaction costs, speed, decentralization, regulatory concerns, and ecosystem maturity.

Oracles in Asset Tokenization

Blockchains can’t access real-world data on their own. When you tokenize a commercial property or a Treasury bond, the blockchain needs external information—like current valuations, interest rates, or legal status—to function correctly.

Oracles solve this. They are services that securely feed off-chain data into on-chain smart contracts. For RWA tokenization crypto, oracles can provide price feeds for underlying assets, confirm events like interest payments or bond maturity, reflect updated appraisals or credit ratings and trigger contract actions based on real-world events.

Projects often use decentralized oracle networks to reduce reliance on a single data source. Multiple data providers and consensus mechanisms help mitigate manipulation risks. Without reliable oracles, tokenized assets risk drifting away from their real-world reference point.

Cross-Chain Interoperability

Ideally, tokenized assets shouldn't be locked to a single blockchain. Cross-chain interoperability allows tokens to move or be represented across different networks, unlocking broader liquidity and functionality.

This matters because:

- Investors might prefer one chain’s DeFi protocols but another chain’s custody solutions.

- Institutions may want to operate on permissioned chains while tapping public-chain liquidity.

- Users shouldn’t have to think about which chain an asset “lives” on.

Current solutions include:

- Bridge protocols that lock tokens on one chain and issue wrapped versions on another.

- Cross-chain messaging that lets smart contracts on different networks coordinate actions.

- Multi-chain deployments where the same token logic exists natively on several blockchains.

Security is the main challenge here. Some historic bridge exploits highlight why robust validation and conservative design are essential. For RWA tokenization to scale safely, interoperability must be secure, audited, and as seamless as possible for end users.

Regulatory Landscape by Jurisdiction

Regulation makes or breaks projects, which is especially relevant in tokenization. Two jurisdictions to pay particular attention to are the U.S. and the European Union.

US Tokenization Regulations and SEC Guidelines

In the U.S., the Securities and Exchange Commission (SEC) relies heavily on the Howey Test to determine whether a token is a security. This test asks whether there is:

- An investment of money

- In a common enterprise

- With a reasonable expectation of profits

- From the efforts of others

If all criteria are met, the token is likely treated as a security.

For tokenization crypto projects—especially those involving real world asset tokenization crypto like real estate or bonds—this creates significant uncertainty. The SEC hasn't released a comprehensive, tokenization-specific set of rules. Instead, it often acts through enforcement cases, which many describe as “regulation by enforcement”.

Compliance typically requires:

- Registering offerings or using exemptions (Reg D, Reg A+, Reg S).

- Implementing full KYC/AML for participants.

- Verifying investor accreditation where required.

- Maintaining detailed records and possibly restricting transfers via smart contracts.

Smaller projects can find the legal costs and operational complexity daunting, but they’re necessary if you’re targeting U.S. investors.

European MiCA Framework Impact on Tokenization

Europe has taken a more structured approach. The Markets in Crypto-Assets (MiCA) regulation, which received final approval in 2023, lays out clear rules for many types of crypto assets across EU member states.

MiCA categorizes tokens (for example, asset-referenced tokens, e-money tokens, utility tokens); requires white papers and disclosures for public offerings.; sets conduct and capital rules for service providers; and provides passporting within the EU, so one license can cover all member states.

For RWA tokenization crypto projects, this framework offers valuable certainty. A tokenized real estate project in one EU country operates under a harmonized set of rules, making cross-border scaling easier than in a fragmented regime.

Integration with Traditional Finance

Turning assets into digital tokens is not for the sake of doing so. Tokenization really starts to scale when it plugs into banks, custodians, and institutional workflows.

Banking and Custody Solutions

Bridging tokenized assets with traditional banking systems requires solving two fundamental problems: secure asset storage and compliant fiat on- and off-ramps.

On the custody side (who holds and manages the assets), traditional banks operate under strict regulatory requirements. When they handle tokenized assets, they need solutions that combine:

- Secure private key management (often via hardware security modules or institutional custodians).

- Clear segregation of client assets.

- Insurance coverage and robust internal controls.

Many banks partner with specialized digital asset custodians or build their own infrastructure to offer segregated wallets, where clients retain beneficial ownership while the bank handles safekeeping, compliance, and reporting.

On the banking side, conventional rails like SWIFT and ACH don’t run 24/7 like blockchain networks do. Banks involved with tokenization crypto projects often create dedicated digital asset teams that facilitate fiat-to-token conversions, provide AML/KYC checks, and reconcile on-chain and off-chain records.

For end investors, this means you can access certain tokenized assets through familiar banking channels, though typically with higher fees and slower settlement than purely on-chain operations.

Institutional Adoption Strategies

Institutional adoption of RWA tokenization crypto has followed a gradual, risk-aware pattern.

When BlackRock launched its first tokenized fund, BUIDL, on the Ethereum network, it illustrated how large asset managers approach this space: start with familiar, highly regulated instruments and leverage battle-tested blockchains.

The typical institutional playbook:

- Pilot phase: Launch proof-of-concept products using low-risk assets (often Treasury products) on established networks like Ethereum.

- Infrastructure build-out: Develop internal expertise, risk management procedures, and compliance workflows. Form partnerships with tokenization platforms, custodians, and legal advisors.

- Expansion: Gradually add more complex asset classes—commercial real estate, private credit, or structured products—once the initial stack is proven.

Forward-looking institutions design with interoperability in mind, ensuring systems can interact with multiple chains and integrate with legacy core banking technology. They see tokenization not as a side project, but as part of a long-term infrastructure upgrade.

Challenges and Risks of Tokenization

Tokenization brings a lot of promise, but it’s not free real estate. To approach projects and investments with realistic expectations, you need to not just be aware of the risks but be rather familiar with what they are.

Regulatory and Legal Uncertainty

The biggest challenge of crypto RWA tokenization is regulatory ambiguity. Different countries classify tokens differently, and rules are evolving.

In the U.S., reliance on the Howey Test and case-by-case enforcement leaves many tokenization crypto projects uncertain about their status. Projects dealing in RWA tokenization crypto must invest heavily in legal advice to avoid missteps when dealing with this jurisdiction and massive market.

In contrast, the EU’s MiCA framework offers clearer guidance, but it’s still being rolled out in practice. Asia and other regions each have their own approaches, leading to a patchwork of global rules.

For cross-border projects, this means an asset tokenized in one jurisdiction may be treated very differently in another, complicating both marketing and secondary trading.

Technology and Security Risks

Smart contracts are powerful but unforgiving. Bugs, misconfigurations, or overlooked edge cases can lead to theft, frozen funds, or incorrect behavior.

Examples of risk include:

- Poorly set access controls that allow unauthorized minting (creation of tokens).

- Logical errors in distribution mechanisms.

- Inadequate testing around edge cases like defaults, redemptions, or liquidations.

Real estate tokenization crypto projects, for instance, must ensure that contract logic accurately reflects legal ownership and that all unusual scenarios (like foreclosure) are accounted for.

Underlying blockchain infrastructure also matters. Congestion, downtime, or attacks on the network can affect token transfers, cost, and reliability. Mitigation strategies include:

- Choosing mature networks.

- Conducting thorough audits.

- Using multisig or hardware-secured key management.

- Having incident response plans in place.

Tax and Accounting Complexity

Tax and accounting standards were not built with tokenized assets in mind. Nevertheless, for now, investors and traders have no choice but to figure it out before the tax agency starts asking the uncomfortable questions.

Questions you quickly run into:

- Does holding a token equate to direct ownership of the asset for tax purposes, or is it treated differently?

- When you trade tokenized fractions, what events are taxable and how are they reported?

- How do you handle cross-border investors with different tax regimes?

The answers vary by jurisdiction and asset type. For now, many projects work with specialized tax advisors to build guidance and reporting into their platforms, but there’s still a fair amount of gray area.

Cybersecurity and Jurisdictional Issues

Tokenized assets face the same cybersecurity issues as other digital assets:

- Phishing attacks aimed at stealing private keys.

- Compromised wallets or exchange accounts.

- Social engineering targeting project admins.

Because blockchain transactions are irreversible, recovery options are limited compared to traditional banking. Insurance solutions exist but are still developing.

Jurisdictional complexity adds another wrinkle. A tokenization platform might operate under one legal regime, run on a blockchain governed elsewhere, and serve users globally. In a dispute, which court has authority? These legal questions are still being tested, especially for cross-border tokenization of real-world assets.

The Future of Crypto Tokenization

Looking ahead, tokenization is less about speculative coins and more about transforming the plumbing of global finance and business operations.

Tokenization in Business Operations

Tokenization can fundamentally reshape how businesses manage, finance, and monetize assets. Just a few examples:

- Balance sheet flexibility: Companies can tokenize high-value assets like machinery or real estate to raise capital without traditional loans or full asset sales. This can make capital structures more flexible and efficient.

- Supply chain optimization: Tokenizing inventory or individual items enables real-time tracking, automated payments upon delivery, and stronger anti-counterfeiting measures. Each token acts as a verifiable digital twin.

- Administrative automation: Smart contracts can handle tasks like dividend payouts, interest distributions, compliance checks, and even some reporting functions. This significantly reduces manual workload, especially in real estate tokenization crypto where many small investors are involved.

- New revenue channels: Tokenized assets can plug into DeFi ecosystems to generate yield or serve as collateral, creating additional income streams from assets that were previously just sitting on balance sheets.

The common theme is turning static assets into programmable, dynamic tools that fit into 24/7 global markets.

What Financial Institutions and Regulators Think

Institutional and regulatory perspectives have also shifted from skepticism to cautious engagement. Institutions see and appreciate:

- Faster settlement and reduced counterparty risk.

- Access to new client segments via fractionalized, low-minimum products.

- Operational efficiencies in issuance, management, and reporting.

Others focus on risks around cybersecurity, systemic dependencies on oracles and key infrastructure, and unresolved questions about cross-border supervision.

One point of broad agreement: tokenization is unlikely to disappear. The policy debate now is about how to implement it safely.

Tokenization and Innovation in Financial Markets

Tokenization is already reshaping how markets operate.

- Secondary market evolution: Tokenized private assets can trade more fluidly than their traditional counterparts, shortening lock-up periods and improving investor flexibility.

- New pricing infrastructure: Automated market makers (AMMs), decentralized exchanges, and oracles introduce new ways to discover prices, especially for assets that previously traded infrequently.

- Capital efficiency via composability: Tokenized assets can be reused across different protocols—pledged as collateral, pooled for liquidity, or wrapped into structured products.

The rise of asset-backed tokens—like those representing Treasuries—blurs the line between stablecoins, money-market instruments, and traditional securities. Tokenized US Treasury products are the most prominent example of hybrid instruments that combine old-world stability with new-world rails.

Cross-chain innovations further push markets toward global, 24/7 environments where assets move and interact across multiple infrastructures.

More crypto projects and categories are covered in detail in ChangeHero blog. For bite-sized content and updates, feel free to follow our pages on social media: X, Facebook, and Telegram.

Frequently Asked Questions

What is the Purpose of Tokenized Assets?

Tokenized assets aim to make ownership more liquid, accessible, and transparent. By converting immaterial things like ownership rights into blockchain-based tokens, they turn illiquid assets into tradable units, lower investment minimums so more people can participate, and reduce reliance on slow, paper-based processes and intermediaries.

In practical terms, tokenization can turn an asset that previously required months to sell into something you can trade within hours. For asset owners, that means faster access to capital. For investors, it means more choices and clearer records of who owns what.

What Types of Assets Can Be Tokenized?

Almost any asset with clear ownership and a verifiable value can, in theory, be tokenized.

Common categories include physical assets: real estate (commercial buildings, rentals, single units), art, collectibles, precious metals, and commodities; financial instruments:

equities, bonds, private credit, investment funds, and money market products like tokenized Treasury bills; revenue streams: royalties, licensing agreements, subscription-based revenues, carbon credits, and renewable energy certificates; and even intangible assets such as intellectual property rights, patents, and brand-related assets.The key prerequisites are clear legal ownership and a defendable valuation method.

How Does Tokenization Improve Liquidity in Asset Trading?

Tokenization improves liquidity through:

- Fractionalization: Breaking assets into smaller units so more buyers can afford them.

- 24/7 markets: Allowing tokens to trade around the clock on blockchain-based platforms.

- Global reach: Letting investors participate from different countries without complex intermediaries (subject to local regulations).

Instead of needing one buyer able to purchase an entire asset, you can match many smaller buyers and sellers continuously. This dramatically increases the odds that someone is willing to take the other side of your trade at any given time.

How Can Tokenization Influence Investment Strategies?

Tokenization changes how individuals and firms can build portfolios and provide a few considerable benefits.

Access to asset classes like commercial real estate, art, or private credit that previously required large minimums (broader diversification). Investors can fine-tune exposure by buying small fractions of many different tokenized assets (granular allocation). Greater liquidity means portfolios can be adjusted more frequently in response to market changes (agile rebalancing). Smart contract features—like automated reinvestment or distribution—support more sophisticated, yet user-friendly, yield tactics (programmability).

In short, tokenization turns alternative investments into something closer to mainstream, with lower entry barriers and more flexibility.

What are the Benefits of Using Tokenization for Asset Management?

For asset managers, tokenization offers several advantages:

- Operational efficiency: Automated distributions, built-in compliance checks, and on-chain records significantly cut administrative overhead.

- Expanded investor base: Fractional ownership and digital onboarding open products to smaller and more global investors without proportionally increasing complexity.

- Real-time transparency: Clients can view holdings and transaction histories on-chain, improving trust and reducing reconciliation work.

- Enhanced product design: Managers can create new structures with flexible lock-up terms, dynamic fee models, and integrated secondary markets.

When implemented thoughtfully, tokenization can help managers lower costs, improve service quality, and innovate faster—all while operating within existing regulatory constraints.