What is a CBDC? A Guide to Central Bank Digital Currencies

Disclaimer:

This page is informational only and does not constitute legal or financial advice. CBDC meaning, designs, legal frameworks, and terminology vary significantly by jurisdiction, and what applies in one country may not apply in another.

What is a CBDC?

CBDC stands for “central bank digital currency” but is more than “state-issued crypto”.

A central bank issues a CBDC as sovereign fiat currency with two defining properties: it is a direct liability of the monetary authority, and it is designed to function as legal tender within its issuing jurisdiction (where the law designates it as such). Unlike commercial bank deposits or private digital assets, a CBDC is the digital form of the nation’s currency issuance itself.

Definition

A CBDC is not the same thing as the digital balances you hold at your bank, nor is it a cryptocurrency or stablecoin like a Paxos (USDP) digital dollar or Tether USD. The exact differences become clear when comparing these digital assets:

| Dimension | CBDC | Commercial Bank Deposit | Stablecoin / Crypto |

|---|---|---|---|

| Claim on | Central bank directly | Commercial bank | Private issuer or protocol |

| Issuer | Monetary authority (central bank) | Licensed commercial bank | Private company or decentralized network |

| Backing | Sovereign fiat currency / central bank balance sheet | Fractional reserves; deposit insurance up to limits | Collateral, algorithm, or market value (varies) |

Legal Tender Status

Legal tender is jurisdiction-specific. It is not even a required feature of every CBDC design; it is a legal designation governments can choose to apply.

What legal tender changes for users:

- (a) Debt payment acceptance: Legal tender status generally means creditors are legally obligated to accept the currency in settlement of debts denominated in the national unit of account.

- (b) Public-sector payment acceptance: A common — but not universal — policy choice is to require acceptance of the CBDC for taxes, fees, and government payments, aligning it with physical cash obligations.

Whether a given CBDC carries these properties depends entirely on the legal framework of the issuing jurisdiction.

Central Bank Liability

“Liability of the central bank” has a precise meaning: the holder has a direct claim on the central bank itself, not on a commercial bank or payment intermediary. Your claim sits on the central bank’s balance sheet, the same as physical banknotes.

The risk implications of this arrangement are:

- Credit risk: Exposure is to the central bank rather than to a commercial intermediary, though “risk-free” is a characterization that requires jurisdiction-specific qualification.

- Liquidity risk: Because the claim is on the monetary authority, the central bank can, in principle, ensure the currency remains liquid within its payment system—though holding limits and access rules can introduce practical constraints.

- Settlement finality: Direct central bank money typically enables immediate, unconditional settlement finality in a way that commercial bank money does not, since no intermediary credit step is required.

Value Parity With Cash

CBDCs are typically denominated in the national unit of account and designed to maintain 1:1 convertibility with physical cash and central bank reserves. One digital unit equals one unit of the national currency—this is the intended parity.

In practice, parity refers to face value equivalence. It does not mean a CBDC is identical to physical cash in every attribute. Similarly, parity says nothing about:

- Privacy characteristics — cash transactions are anonymous in ways a CBDC may not be, depending on design.

- Access requirements — cash requires no account or device; a CBDC may require digital infrastructure.

- Offline availability — cash works without connectivity; offline CBDC functionality is a design choice.

Therefore, it’s worth noting value parity does not imply “same as cash” in every respect.

Why Governments Are Exploring CBDCs

Governments are not evaluating CBDCs for one single reason. Pressures justifying the move tend to come at the same time—and they often pull in opposite directions. For example, inclusion goals can cut against privacy; efficiency can trade off against resilience. Sovereignty concerns can complicate cross-border cooperation. The design choices that follow—retail vs wholesale, account-based vs token-based, intermediated distribution, offline functionality—are essentially engineering responses to these tensions.

As of 2026, over 130 countries are in some stage of CBDC exploration or development, with a significant share in advanced research, pilot, or launch phases. In other words: for many central banks, this is now a practical systems question, not a theoretical one.

Payment Efficiency

The payment-efficiency argument tends to target three concrete frictions.

First, settlement finality time. Many domestic retail payment systems settle in batches, creating intraday credit exposure. A CBDC operating on a real-time gross settlement logic could compress finality to seconds. The non-CBDC comparator is a faster payments rail upgrade (such as the U.S. FedNow or the UK's Faster Payments), which can achieve similar retail outcomes without issuing new central bank money. Where faster payments already exist, the efficiency-only case for CBDC has to clear a higher bar.

Second, cost drivers in the payment system. Merchant fees, card network interchange, reconciliation overhead, and dispute handling are real drag, especially for small merchants. A CBDC payment settled directly in central bank money could bypass some card-network intermediation. Separately, cash management—printing, transport, authentication, and destruction—imposes costs that digitization could reduce. The non-CBDC comparator is account-to-account bank transfer infrastructure, which compresses many of the same costs without creating a new monetary instrument.

Third, resilience and continuity of payment rails. Concentrated payment infrastructure creates single-point-of-failure risk. A CBDC architecture—if designed with redundancy—could function as a backup rail independent of commercial bank systems. The non-CBDC comparator is regulatory mandates for redundancy and diversification among settlement providers.

With this all in mind, offline payments introduce delayed reconciliation risk and potential double-spend exposure, and scalability and cyber/operational load during peak events could concentrate systemic risk onto CBDC infrastructure. These edge cases pose considerable challenges for any CBDC implementation and set it apart from discussions of “faster payments”.

Financial Inclusion

Onboarding as many residents as possible without creating unnecessary hurdles is another huge factor in the CBDC design. There are quite a few cohorts being borderline marginalized by the current systems in place that CBDC can take into account: unbanked individuals face documentation and KYC barriers. A CBDC with tiered identity requirements—lighter KYC for lower limits—could lower the entry threshold without eliminating compliance obligations. Underbanked individuals often have an account but rely on high-fee services. A CBDC wallet with no minimum balance requirement and near-zero transaction fees could reduce that fee load, even though it does not solve credit access.

Rural and low-connectivity populations face distance and infrastructure limitations. Offline or low-bandwidth CBDC operation could reduce dependence on branches and ATMs, with the caveat that offline functionality is technically and operationally complex. Migrants and cross-border workers face high remittance costs, documentation gaps, and limited access in both jurisdictions. Interoperable CBDC rails could help, but regulatory alignment is substantial.

However, an important caveat is that inclusion-focused designs are not privacy-neutral. Tiered identity still needs enforcement mechanisms for limits and layering prevention. The lighter the identity requirement, the greater the inclusion benefit—but the harder it becomes to satisfy AML/CFT obligations. “Inclusive” is not a solution; it is a design constraint that must be handled explicitly in the identity and compliance stack.

Monetary Sovereignty

Monetary sovereignty in CBDC discussions refers to specific mechanisms governments want to preserve:

- Unit of account dominance (domestic pricing and settlement remain in domestic currency)

- Monetary policy transmission (rates and liquidity conditions still propagate effectively)

- Central bank money as a trust anchor (public access to settlement-final, sovereign money as cash declines)

High stablecoin adoption for domestic payments, foreign currency substitution in emerging markets, and the secular decline of cash are all factors contributing to eroding monetary sovereignty—and a CBDC intends to counteract.

It’s not to say that CBDC is inherently “more money printing.” What changes is the form factor and distribution channel of central bank money. What does not change is denomination, backing, or the monetary policy framework governing issuance.

Cross-Border Settlement

Lane 1: Retail remittances. Persistently high costs (often cited at 6–7% averages in many corridors), slow settlement, and weak transparency are the core pain points. CBDC-based pathways could compress correspondent banking layers and improve speed and auditability—but only with interoperability.

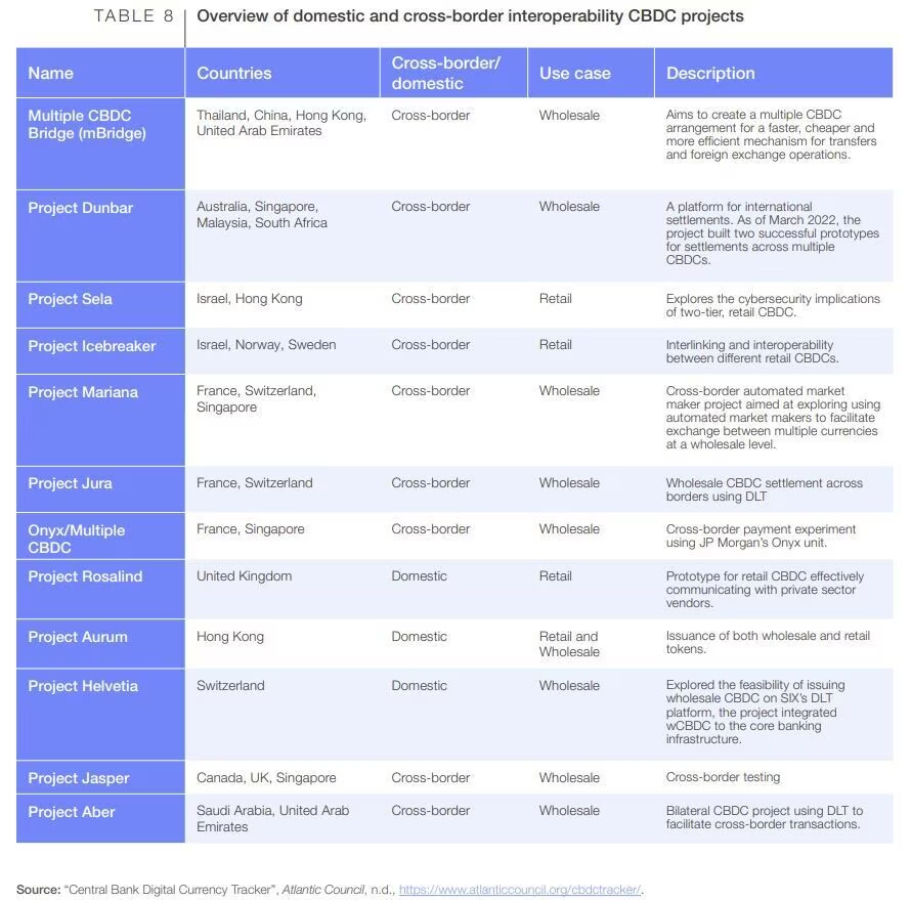

Lane 2: Wholesale interbank settlement. Wholesale cross-border settlement relies on capital-intensive and operationally complex correspondent systems. PvP and DvP settlement in central bank money can eliminate principal risk and compress settlement cycles. The mBridge project is an example of a multi-CBDC wholesale initiative that has processed real transactions across jurisdictions, but it remains early-stage rather than a universal benchmark.

Constraints governments cite as blockers:

- Interoperability standards (no agreed global standard)

- AML/CFT alignment across jurisdictions

- FX conversion, liquidity, and governance of shared platforms

The constraint list is why cross-border CBDC discussion almost always becomes a governance discussion.

Types of CBDCs and Design Models

CBDC design is not a single product but an entire spectrum of solutions. Two dimensions matter, and they are independent:

- Retail vs. wholesale — who is permitted to hold and use the currency.

- Account-based vs. token-based — how value is represented and how access is controlled.

Real-world pilots frequently mix these dimensions, so separating them first makes the implementation choices easier to evaluate.

Retail CBDC

A retail CBDC is a direct liability of the central bank held by the general public—individuals and businesses.

Typical retail design choices that materially affect user experience and policy outcomes: intermediated distribution, balance and transaction limits, tiered KYC; is it interest or non-interest bearing? Does it work for offline payments? Are programmability constraints on the table?

A retail CBDC provides a cash replacement with resilience, enables government-to-person transfers and merchant payments finality; it boosts financial inclusion and even disaster/crisis liquidity. However, it is constrained by bank disintermediation sensitivity and privacy expectations vs. compliance requirements.

Wholesale CBDC

A wholesale CBDC narrows down access to licensed financial institutions and is designed for interbank and financial market settlement. It differs from reserves/RTGS in that it can operate on a shared digital ledger with programmable settlement logic (e.g., DvP) that traditional RTGS systems do not support natively without heavy bilateral scaffolding.

Wholesale-specific design considerations: delivery-versus-payment (DvP) vs. payment-versus-payment (PvP), intraday liquidity management, interoperability with existing RTGS. A wholesale CBDC can be designed for tokenized deposit and asset settlement and even Cross-border corridor design.

According to the Atlantic Council's CBDC Tracker, the majority of cross-border CBDC experiments currently underway are wholesale in nature, reflecting institutional demand for improved settlement mechanics and interoperability.

Account-based Models

In an account-based CBDC model, authorization is tied to identity. The ledger records balances associated with account identifiers. This model closely resembles digital banking in this regard, even though it does not mean the central bank holds customer accounts.

Operational and compliance implications of an account-based CBDC: reversibility and dispute handling (governance-permitting), compliance integration, operational dependency on intermediaries and their role in customer relationships.

In implementation, most often either the Central bank runs the core ledger and intermediaries manage customer accounts, or intermediaries run sub-ledgers with periodic settlement on a central ledger.

Token-based Models

In a token-based CBDC model, authorization is tied to possession via cryptographic proof. Value travels with the token rather than being adjusted purely as a named balance in a register.

Some design tradeoffs unique to token-like systems are offline transfer feasibility, bearer-like loss and theft risk, AML/KYC via tiering, double-spend prevention, and privacy-by-design options (e.g., selective disclosure). Token-based CBDCs can use custodial and self-custodial wallets with hybrid designs, much like cryptocurrencies do. Even so, it does not automatically mean blockchain technology is involved.

Retail/wholesale categorization answers who is this for. Account/token answers how access and value are implemented. Central banks mix and match based on policy constraints and payment infrastructure realities: for example, a CBDC can be retail and account-based, or wholesale and token-based.

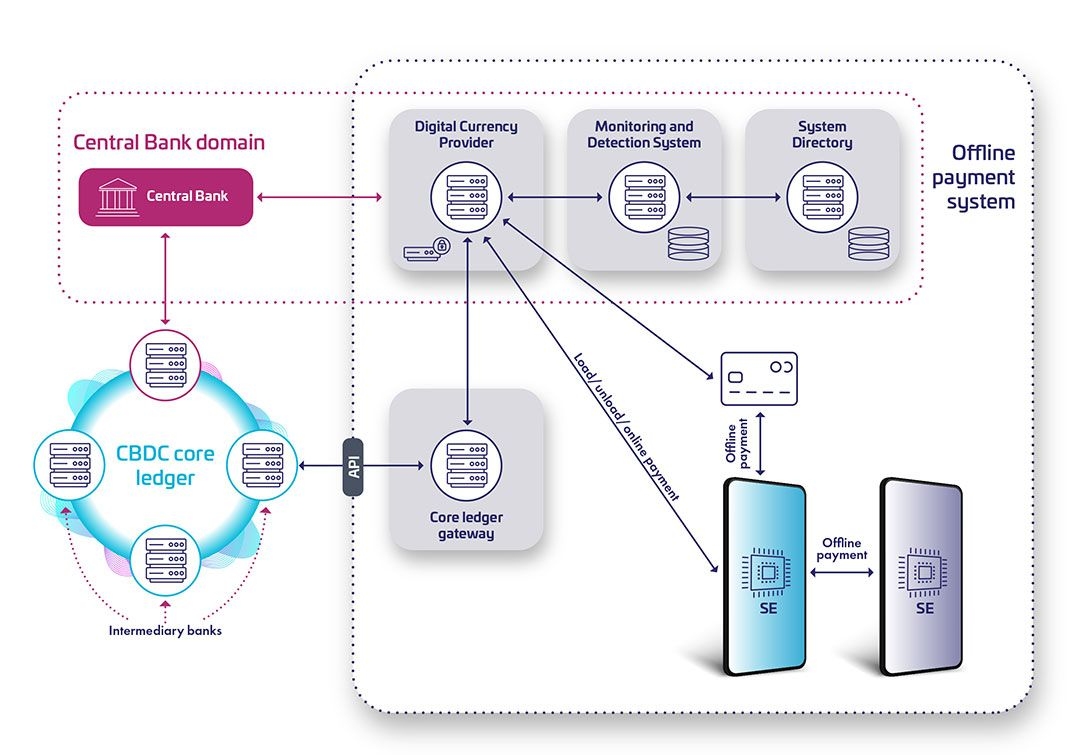

How CBDCs Work

Issuance and Redemption

To nobody’s surprise, a CBDC does not come into existence the way physical cash is printed. Issuance is a balance-sheet operation: when a central bank issues CBDC, its liability increases, and a corresponding claim or asset enters the system (the specific mechanism depends on design). This matters because it clarifies why issuing CBDC is not inherently “printing money” in the inflationary sense; it is a transformation of claims within the payment system.

A CBDC lifecycle goes through these steps: mint or issuance, distribution, circulation and transfer in the system; at the tail end, a CBDC goes through redemption, retirement or burn, and ends with reconciliation / settlement finality. In an account-based model, issuance credits and redemption debits accounts on the central bank ledger. Token-based model mints tokens with cryptographic proof; redemption burns tokens.

In both models, the ledger of record is ultimately controlled by the central bank, and par value is maintained by design.

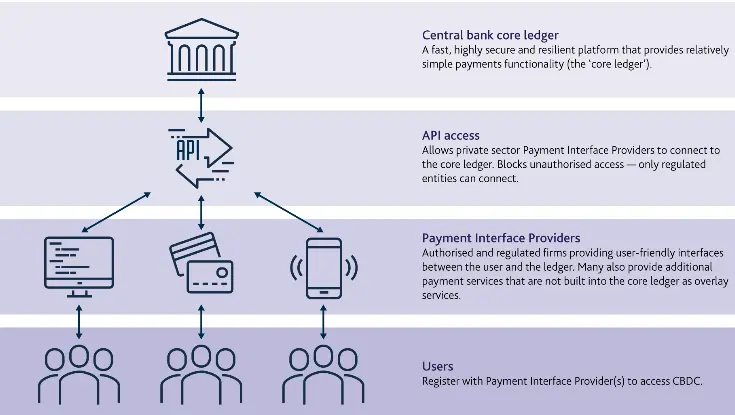

Intermediary Roles

Despite what the name might lead you to believe, a central bank is not the only entity involved in the CDBC’s life cycle. Most CBDC architectures are layered.

Central bank:

- Controls issuance, core ledger, and rulebook.

- Sets AML/CFT parameters and technical standards.

- Typically sees aggregated flows in an intermediated model, not end-user transaction detail by default.

Commercial banks and payment service providers (PSPs):

- Onboard customers (KYC/AML).

- Custody wallets or token holdings, depending on model.

- Conduct transaction monitoring and reporting.

- Provide customer support and dispute handling.

Wallet providers and agents:

- Provide user interface and transaction-time authentication components.

- In some designs, agents handle cash-in/cash-out.

Identity and Compliance

The Federal Reserve has described four operational characteristics that frame how a well-designed CBDC should function: privacy-protected, intermediated, widely transferable, and identity-verified (Source: Congressional Research Service, IF11471). Federal Reserve Chair Jerome H. Powell has reinforced this framing in public remarks on U.S. CBDC prerequisites.

The compliance stack operates in four layers:

- Identity proofing at onboarding

- Authentication at transaction time

- Transaction monitoring

- Reporting and auditability

A “privacy-protected” CBDC is not anonymous where anonymity means no linkage to identity. Privacy when it comes to CBDCs means data exposure is minimized and access is governed, even though identity is known to at least one layer.

Offline Capability

Stable and constant connectivity simply cannot be assumed to be available at all times to anyone, anywhere. Offline design is therefore a first-order requirement in jurisdictions prioritizing resilience and inclusion. Generally, two solutions address this challenge:

Mode 1: Device-to-device value transfer. Provisional finality at transfer; finality after reconciliation. The main risk is double-spend.

Mode 2: Stored-value balance with later synchronization. Local debits, queued uploads, finality at sync. Main risk: synchronization integrity.

Offline capabilities force additional features: a secure element or trusted hardware, time-bounded and amount-bounded limits, defined re-sync rules, dispute handling for reconciliation failures. It requires device loss and recovery protocol to be considered, as well as imposes some audit trail requirements.

CBDC Timeline and Global Status (2026)

Status categories used here follow operational thresholds:

- Pilot: closed user group + caps + time-boxed/sandbox conditions, no general public access.

- Limited launch: production rails + official announcement, but restricted availability.

- Live deployment: public availability on demand + ongoing issuance/redemption.

Pilots

A pilot is not a proof-of-concept (PoC). A PoC tests whether tech can work in a lab but at the pilot stage, what is tested is whether it does work under real but bounded conditions: restricted participation, capped transaction sizes, intermediated distribution, and defined scope with review points.

Limited Launches

“Limited” reflects deliberate constraints: geographic, demographic, transactional, or structural. These constraints exist because payment infrastructure changes are systemic-risk changes, and staged scaling is the risk-managed default.

Live Deployments

Finally, even “live” requires verification: official launch statement on record, production infrastructure, on-demand onboarding (no pilot waiting list), and most importantly, ongoing issuance and redemption.

A system can be live and still have low adoption. Availability is not necessarily equal to real usage.

Global Landscape Overview

As of 2026, according to the Atlantic Council's CBDC Tracker, 146 countries are exploring a CBDC, 77 are in an advanced phase (development, pilot, or launch), 41 are running active pilots, and three have fully launched retail CBDCs: the Bahamas (Sand Dollar), Jamaica (JAM-DEX), and Nigeria (eNaira).

Retail CBDC progress and cross-border/wholesale momentum are different pipelines. The tracker counts over 13 cross-border wholesale CBDC projects underway, focused on interbank settlement and correspondent banking efficiency rather than consumer wallets.

What’s changed the most since 2022–2024? More jurisdictions have moved from research into pilots since 2023, and cross-border wholesale experiments accelerated in both number and institutional participation.

United States Status

As of 2026, the United States does not have a CBDC. The Federal Reserve is conducting research and exploration, but no decision to issue a digital dollar has been made just yet.

The Federal Reserve exploration and research in the January 2022 discussion paper was not a launch or policy commitment. The same report identified four aforementioned design characteristics for a robust CBDC design, not defined it. There is still no authorizing legislation, no implementation plan, no official program launch. The Federal Reserve has stated it would not proceed without clear support from the executive branch and Congress.

Real-World CBDC Implementations

These four implementations represent the only fully live retail deployments and the world’s largest-scale retail CBDC pilot, providing the clearest evidence base for transferable design implications.

Bahamas Sand Dollar

- Launch status & scope: Fully launched nationwide in October 2020, making the Bahamas the first country to issue a live retail CBDC. Scope covers all inhabited islands across the archipelago, with no geographic restriction post-launch.

- Primary distribution model: Intermediated via authorized financial institutions and payment service providers. End users access Sand Dollar through a licensed digital wallet app; onboarding runs through regulated intermediaries rather than directly through the Central Bank of The Bahamas.

- Targeted use cases:

- P2P transfers between individuals across islands

- Merchant payments at local businesses

- Government disbursements and social payments

- Reducing cash logistics costs for remote islands

- Financial inclusion for unbanked residents without traditional bank accounts

- Adoption signals: Public KPI not consistently disclosed at a granular level; the Central Bank of The Bahamas has reported periodic growth in registered wallets, but transaction volumes and value processed have not been released in a consistent public series.

- Key frictions observed:

- Merchant acceptance gap

- Onboarding/KYC friction

- Device dependency

Jamaica JAM-DEX

- Launch status & scope: Fully launched; Jamaica's National Commercial Bank began public rollout in 2022, with the Bank of Jamaica declaring it legal tender. Deployment is nationwide but adoption remains in early growth stages.

- Primary distribution model: Intermediated through commercial banks and authorized payment service providers. End users access JAM-DEX via a digital wallet (the "Lynk" wallet operated by NCB was the initial primary access point), with the central bank issuing to intermediaries who distribute to the public.

- Targeted use cases:

- P2P payments between individuals

- Merchant payments at physical retail points

- Government-to-person disbursements

- Reducing reliance on physical cash and associated handling costs

- Driving financial inclusion for the unbanked and underbanked population

- Adoption signals: Public KPI not consistently disclosed at a system-wide level; the Bank of Jamaica ran incentive programs (cash-back promotions) to drive initial wallet registrations, but comprehensive transaction volume data has not been released in a consistent public series.

- Key frictions observed:

- Trust and familiarity deficit

- Merchant acceptance breadth

- Incentive misalignment with commercial banks

Nigerian eNaira

- Launch status & scope: Fully launched in October 2021, one of the earliest retail CBDCs in a large emerging economy. Available nationwide, with subsequent updates expanding features and targeted user segments including the unbanked.

- Primary distribution model: Intermediated via commercial banks and licensed fintech operators. End users access eNaira through a tiered digital wallet system; Tier 1 wallets require minimal KYC, targeting the unbanked, while higher tiers unlock larger transaction limits with fuller identity verification.

- Targeted use cases:

- P2P transfers

- Merchant payments (including informal-sector vendors)

- Government disbursements and social transfer programs

- Diaspora remittances and cross-border payment corridors

- Financial inclusion for the large unbanked adult population

- Adoption signals: The Central Bank of Nigeria reported approximately 13 million wallets downloaded and over 3 million transactions in the months following launch, though active usage rates lagged behind download figures significantly. Subsequent redesigns were introduced in part to address low activity rates.

- Key frictions observed:

- Low active usage versus downloads

- Bank incentive misalignment

- Trust and privacy concerns

China e-CNY

- Launch status & scope: The largest-scale retail CBDC pilot globally, operating as an ongoing controlled pilot rather than a universal nationwide launch. Pilot cities have expanded significantly since trials began in 2020, covering major urban centers and extending to additional provinces; the People's Bank of China has still not announced a date for unrestricted national rollout.

- Primary distribution model: Two-tier intermediated model: the People's Bank of China issues e-CNY to state-owned commercial banks and licensed payment operators, which in turn distribute wallets and manage customer relationships. End users access e-CNY through bank apps and dedicated e-CNY wallet applications on smartphones, with hardware wallet (NFC card) options for offline and lower-tech access.

- Targeted use cases:

- Retail consumer payments at physical merchants

- E-commerce transactions

- Government salary and subsidy disbursements

- Transit and public-service payments

- Large-event distribution (red-envelope lottery programs at major events)

- Adoption signals: According to the Atlantic Council CBDC Tracker, retail e-CNY surpassed 3.4 billion transactions worth approximately 16.7 trillion RMB by December 2025, representing the most substantial volume evidence of retail CBDC usage anywhere globally.

- Scale & ecosystem integration: e-CNY achieves a distribution and usage scale qualitatively different from the three fully launched smaller-economy CBDCs (Sand Dollar, JAM-DEX, eNaira) by embedding itself across a vast merchant network that includes both major e-commerce platforms and physical point-of-sale infrastructure in hundreds of cities. Public-service touchpoints — including transit systems, government benefit disbursements, and tax payment channels — create mandatory or highly convenient on-ramps. The combination of state-directed commercial bank participation, integration with dominant super-apps, and government subsidy programs (lottery red envelopes) generates use-case density that sustains transaction volumes.

- Key frictions observed:

- Privacy and surveillance concerns

- Coexistence with dominant private payment systems

- Merchant and platform integration complexity

Risks, Drawbacks, and Key Considerations

Privacy

Privacy in the framework of a central-bank issued digital currency is layered:

- Identity privacy (tier structure is the main lever)

- Transaction privacy (selective disclosure credentials)

- Metadata privacy (encryption, key management, and query controls)

No currently available configuration of these products optimizes all three layers simultaneously. They can even be thought of as a trilemma, requiring a compromise. Strong compliance visibility tends to weaken privacy layers, and stronger encryption can complicate lawful access workflows.

Surveillance Concerns

A huge counterargument against any CBDC from privacy activists is the sheer scope of transaction monitoring a system like CBDC can enable. The concern is not only capability—it is expansion of and pathways to misuse: lawful access, administrative overreach, function creep, and third-party surveillance by intermediaries or analytics firms. Each pathway has a different mitigation profile: statutory purpose limitation, judicial oversight, immutable access logs, transparency reporting, data minimization, and restrictions on secondary commercial use.

Cybersecurity

CBDC systems concentrate systemic value and attract high-grade adversaries. Threat surface spans wallets, intermediaries, and ledger integrity.

| Threat | Prevention Control | Recovery Control |

|---|---|---|

| Wallet compromise / account takeover | Multi-factor authentication, hardware-bound keys, anomaly detection on login and signing events | Wallet freezing + re-issuance protocol; user-initiated recovery via identity re-verification |

| Endpoint malware (user devices) | Secure enclave / trusted execution environment for key storage; app attestation | Transaction reversal windows with defined eligibility criteria; forensic audit trail |

| Insider threats at intermediaries | Role-based access controls, four-eyes authorization for privileged operations, audit logging | Incident response playbook with mandatory regulator notification; reconciliation against central ledger records |

| API and ledger integrity attacks | Input validation, rate limiting, cryptographic signing of all ledger state transitions, immutable audit logs | Ledger rollback to last verified checkpoint; out-of-band reconciliation with intermediary records |

| Denial-of-service (network or application layer) | Traffic filtering, redundant routing, capacity headroom above peak demand | Graceful degradation to offline/queued mode; published SLA commitments and public status transparency |

Ledger security is necessary, but endpoint compromise and insider threats often dominate in real-world financial breaches.

Bank Disintermediation

Retail CBDC creates a direct alternative to commercial bank deposits. Moreover, its risk magnitude is design-dependent.

At normal times, the balance sees gradual shifts in transaction balances. Holding caps can keep outflows modest. However, the crisis dynamics can look intimidating: without caps and with high transferability, a CBDC can become a rapid safe-haven instrument, accelerating deposit flight compared to physical cash withdrawals.

This is where design dependency enters the picture. To prevent the worst-case scenario, a CBDC can include levers that introduce hindrance in other aspects of user experience: caps on holding, tiered remuneration / interest, and intermediated distribution (favored in the Federal Reserve framing).

Environmental Considerations

Aside from operational and policy risks, CBDCs also warrant a look from the sustainability angle. Generic “blockchain uses energy” claims are not the relevant comparison for CBDC. Most serious CBDC designs use centralized or permissioned architectures, not proof-of-work.

Dominant drivers of energy use would be transaction volume and peak load, redundancy and geographic replication, cryptographic operations, and offline hardware endpoints (which inevitably leave a manufacturing and lifecycle footprint). A common point of rebuttal against criticism of crypto’s energy use is its comparatively smaller size to traditional finance’s: now imagine how much a crypto-like network would be using if it were to serve large nations.

CBDCs vs Cryptocurrencies and Stablecoins

Now, why would a crypto-focused blog go to such lengths to talk about central-bank-developed projects? The days when CBDCs were thought of as direct competitors to cryptocurrencies are long gone; likewise, the idea that currently existing crypto projects like XRP would be able to enter this space are not often put forward seriously. If anything, projects like CBDCs highlight cryptocurrencies and even stablecoins as open, decentralized, permissionless and censorship-resistant alternatives to fiat money.

| Attribute | CBDC | Cryptocurrency (BTC/ETH class) | Stablecoin (fiat-backed / crypto-backed / algorithmic) |

|---|---|---|---|

| Ledger topology | Centralized or permissioned distributed ledger technology | Permissionless, decentralized | Varies: centralized (fiat-backed) to permissionless (crypto-backed/algo) |

| Issuer / liability | Central bank (sovereign liability) | No issuer; protocol-governed | Private issuer or protocol; claim on reserves or smart contract |

| Identity layer | KYC/AML embedded by design | Pseudonymous / optional KYC | Issuer-driven compliance; varies widely |

| Monetary rule changes | Statutory mandate (legislature + central bank) | Protocol consensus (miners/validators) | Issuer terms or governance token vote |

| Redemption claim | Direct claim on central bank money | No redemption guarantee | Claim on issuer reserves or algorithmic mechanism |

| Price stability | Stable by design (unit of account) | Market-determined; high volatility | Peg-dependent; failure modes vary by type |

| Primary credit risk bearer | Sovereign/central bank absorbs | User bears full market risk | User + issuer (fiat); user + protocol (crypto/algo) |

| Privacy/surveillance exposure | High (state-level visibility possible) | Moderate (pseudonymous on-chain) | Moderate to high depending on issuer |

Governance differences

CBDC governance stack:

- Rule-maker: legislature + central bank statutory mandate

- Operator: central bank / designated agent

- Intermediaries: regulated PSPs/banks, no unilateral protocol rule changes

Cryptocurrency governance stack:

- Rule-maker: distributed consensus; hard forks possible

- Operator: validator nodes

- Intermediaries: exchanges/custodians apply external compliance

Stablecoin governance stack:

- Rule-maker: issuer or DAO token governance

- Operator: issuer mint/burn/reserve management or protocol logic

- Intermediaries: issuer blacklisting/freezing or coded mechanisms

Key operational distinction: A central bank can modify CBDC rules through a legally authorized process with democratic accountability. A cryptocurrency changes through distributed consensus. A stablecoin issuer can change terms, pause redemptions, or blacklist addresses subject to its contractual and regulatory constraints.

Risk Profile Differences

| Risk Type | CBDC | Cryptocurrency | Stablecoin | Primary Risk Bearer |

|---|---|---|---|---|

| Credit risk | Negligible (sovereign liability of central bank money) | High (no issuer guarantee) | Moderate–High (depends on reserve quality and issuer solvency) | User (crypto); User + Issuer (stablecoin); Central bank absorbs (CBDC) |

| Bank run risk | Low (central bank as lender of last resort) | Moderate (thin order books in stress) | High (fiat-backed: reserve mismatches; algo: death spiral risk) | Intermediary (CBDC); Validator set (crypto); Issuer + User (stablecoin) |

| Price volatility | None (stable unit of account) | Very high (no price floor) | Low under normal conditions; severe during peg breaks | User bears fully (crypto); User + market (stablecoin) |

| Operational risk | High-value central target; mitigated by sovereign-grade security | Distributed; consensus attacks possible at low hash rate | Smart contract bugs, oracle failures, custodian hacks | Central bank + intermediaries (CBDC); Validator set (crypto); Issuer/protocol (stablecoin) |

| Surveillance exposure | Highest; state-level transaction visibility possible | Moderate; pseudonymous on digital ledger, analytics possible | Moderate; issuer can monitor and freeze | User (all three); state amplification risk highest in CBDC |

| Regulatory risk | Low for user (issuer is sovereign); high political risk | High and evolving; assets can be delisted or restricted | High; issuers face growing regulatory framework scrutiny globally | User + Issuer (stablecoin); User (crypto); Central bank manages (CBDC) |

Conclusion

A common confusion is worth stating plainly: CBDC adoption does not automatically imply a cashless society. Cash coexistence is a policy choice and a behavioral outcome, not a technical inevitability.

Most CBDCs will roll out incrementally through intermediated models and structured pilots. The governance choices embedded at the design stage—privacy protections, identity verification, and transferability limits—will determine public acceptance more than the ledger technology.

For analytical guides and industry news, check out ChangeHero blog. Feel free to subscribe to our Twitter, Facebook, and Telegram for updates and quick content in social media!

Frequently Asked Questions

Is a CBDC the same as money in a bank account?

A CBDC represents a direct liability of the central bank, not a commercial bank. That distinction changes who controls the balance, what protections apply, and how reversals or freezes are executed. Most proposed CBDCs are intermediated—meaning commercial banks or licensed wallet providers handle the user interface—even though the underlying liability remains with the central bank.

The key distinction is counterparty risk: a bank account balance is only as safe as the bank holding it (hence insurance schemes), while a CBDC claim sits with the central bank. The caveat is that intermediated CBDC designs reintroduce a commercial bank or payment institution into the chain, which can blur the distinction at the user experience level.Can a CBDC be anonymous?

A CBDC does not have a single privacy setting. Privacy architecture is a design choice, and proposed systems range from fully anonymous to fully account-linked. Anti-Money Laundering/Counter-Financing of Terrorism (AML/CFT) and fraud controls typically require some form of identity verification at onboarding or at defined transaction thresholds, making complete anonymity the least likely design outcome.

Will CBDCs replace cash?

A CBDC is not designed to eliminate cash in most published policy frameworks. Whether cash is displaced depends on stated policy intent, actual adoption, and infrastructure resilience. Cash was used in 52% of transactions in Europe in 2024 (Mastercard, 2025), which anchors any claim about cash’s persistence against a concrete baseline.

Can CBDCs be used without the internet?

Some CBDC designs include offline functionality, but offline use is not universal, not unlimited, and introduces risks requiring mitigation.

Can foreigners hold a CBDC?

Whether a non-resident can hold or use a CBDC depends on legal eligibility, access channels, and what “cross-border use” means in that design.

“Cross-border use” may mean only that a foreign counterparty can receive value via an FX or bridge mechanism—not that foreigners can hold the CBDC directly.