Beginner's Guide to Uniswap Exchange and UNI Token

Key Takeaways

- 🦄 Uniswap is an on-chain DEX, not a company (not to be confused with Uniswap Labs), non-custodial and permissionless by design: you swap from a self-custodied wallet, no accounts/KYC at the protocol layer, and anyone can create pools—which is exactly why scam tokens and low-liquidity pairs also exist.

- 🦄 AMM mechanics drive execution quality: you trade against liquidity pools, not an order book; trade size vs pool depth determines price impact and slippage. Fees are two separate costs: pool fees go to LPs (and vary by pool/version), while gas fees are set by the underlying chain—Layer 2s often matter more than “Uniswap fees” for frequent activity.

- 🦄 Versions change the risk/management profile: V2 is simple and always-on, V3 adds concentrated liquidity (better execution in-range, real out-of-range risk and active management), and V4 adds hooks (programmability plus hook-specific trust/audit risk).

- 🦄 Swapping is typically two transactions: approval (ERC-20 only) + swap; most failures are slippage/allowance/nonce/network mismatches, not “Uniswap being down.”

- 🦄 Your safeguards are mostly on you: verify domain, router/spender addresses, and token contract addresses; treat unlimited approvals, high price impact, and thin liquidity as warning signs—because the protocol won’t stop you from making a bad swap.

Disclaimer

Nothing on this page constitutes financial or legal advice. Uniswap is a protocol, not a fiduciary service. You are responsible for verifying token contract addresses before swapping, confirming transaction details in your wallet before signing, and understanding the tax and regulatory implications of on-chain activity in your jurisdiction.

The protocol does not prevent you from swapping scam tokens, sending funds to the wrong address, or accepting unfavorable slippage. Those safeguards exist at the user and wallet layer, not inside the smart contract. This guide explains mechanics and workflows, with risk notes where they matter, but it does not replace independent verification or professional consultation.

Launched in November 2018, Uniswap operates as an automated market maker on the Ethereum blockchain, enabling non-custodial token swaps through liquidity pools instead of more traditional order books. Along with liquidity mining and yield farming, it hugely contributed to the so-called “DeFi summer” in 2020 and established itself as a key player in the niche.

This guide will cover the protocol’s mechanics in Uniswap Protocol Overview, compare deployments in Uniswap Versions (V2, V3, V4), and then move into real-world usage constraints in Key Considerations, Risks, and Legality.

Uniswap Protocol Overview

Uniswap is a decentralized exchange protocol implemented through smart contracts on Ethereum and other blockchains that lets users swap ERC-20 tokens directly from self-custodied wallets using automated liquidity pools rather than traditional order books or centralized intermediaries. The definition uses quite a few specific terms, which we will now unpack. Unlike a custodial crypto exchange, Uniswap operates on-chain: each swap is a blockchain transaction you sign from your own wallet, and settlement is publicly verifiable.

As of 2026, Uniswap Protocol remains the largest decentralized exchange by trading volume and regularly processes billions of dollars in swaps across multiple networks. According to official reporting, the protocol has facilitated over $2 trillion in total trading volume since its 2018 launch (source).

Decentralized Exchange (DEX)

As opposed to a centralized counterpart, a decentralized exchange or DEX operates without a central authority controlling user funds or trade execution.

Any DEX, Uniswap included, meets three criteria: trading is non-custodial, meaning you keep control of your private keys throughout the swap process, settlement is on-chain (each swap is written to the blockchain as an individual, permanent record), and liquidity pool creation (explained further) is permissionless. All three criteria must be met to define a DEX: for example, ChangeHero is not one because even though the service is non-custodial and deposits/withdrawals are on-chain, liquidity is something the service handles and swaps are also performed with an internal system.

In a Uniswap swap, your operational counterparty is the liquidity pool smart contract itself. This is peer-to-contract execution: you trade against pooled reserves, and the contract calculates the exchange rate based on reserves at execution time.

In addition to leaving custody and key management to users, DEXs also do not do account-based order matching that enable limit orders or stop-losses and most importantly, smart contracts do not request identity verification, though interface providers or jurisdictions may impose requirements separately.

Automated Market Maker (AMM)

An automated market maker quotes prices algorithmically based on the ratio of tokens in a liquidity pool rather than matching discrete buyer and seller orders as an order book does. AMM logic reads reserves, calculates the exchange rate and executes your swap if you proceed; then it updates reserves, and the updated ratio becomes the new price reference.

Assume a pool holds 10 ETH and 20,000 USDC, implying a rate of 2,000 USDC per ETH. You swap 1 ETH for USDC. The contract adds your 1 ETH (now 11 ETH) and releases USDC according to the pricing algorithm (for example, 1,818 USDC), leaving 18,182 USDC. The new ratio implies a lower ETH value in fiat equivalent. Your trade moved the ratio; the next trader inherits that updated state. The larger your trade relative to pool depth, the more you shift the price.

Where does the ratio come from and how pools avoid running out of liquidity? Users can take on the role of liquidity providers (LP) to supply the tokens that fill these pools and earn a percentage of swap fees as compensation. Each swap pays a fee (varying by pool and version), and that fee accrues to the liquidity providers whose capital is active in that pool.

Why Uniswap Doesn't Use an Order Book

First, an on-chain order book would require a transaction for every limit order placement, cancellation, and partial fill. At scale, that becomes expensive. During particularly high congestion periods on Ethereum in 2021 and 2022, the simplest swaps could cost $50–$100 in gas; an order book would multiply those writes. AMM pools only update state when swaps execute, compressing pricing logic into fewer transactions.

Secondly, order books need tight spreads and consistent depth, necessitating crypto market makers. Low-volume and newly launched tokens often have thin books and wide spreads. An AMM pool can provide continuous liquidity across a price curve from a single deposit, which is why permissionless listings become usable at all.

Uniswap Versions

Uniswap versions are more than milestones across its history: each iterates on how liquidity works, which in practice means how swaps execute and how liquidity providers manage exposure. Most user-facing interfaces as of 2026 default to V3 for liquid pairs because capital efficiency is materially better. V2 remains active for long-tail tokens and simple LP setups. V4, released in January 2025, adds programmable hooks that enable custom pool behavior; adoption is still rolling out as integrators evaluate hook risk and implementation patterns. For updates, see Uniswap's blog.

Uniswap V2

V2 uses the most well-known constant product invariant: x × y = k. We will explain it later but what you need to know for now is it leaves liquidity spread across all prices, which keeps positions “always on,” but makes capital less efficient for pairs that mostly trade inside a narrow band.

An LP deposits equal values of two tokens, receives LP tokens (such as UNI—more on it later) proportional to their share, and earns a fraction of every swap fee. The position never goes out of range. LPs do not pick tiers or ranges, and capital reposition is likewise not necessary.

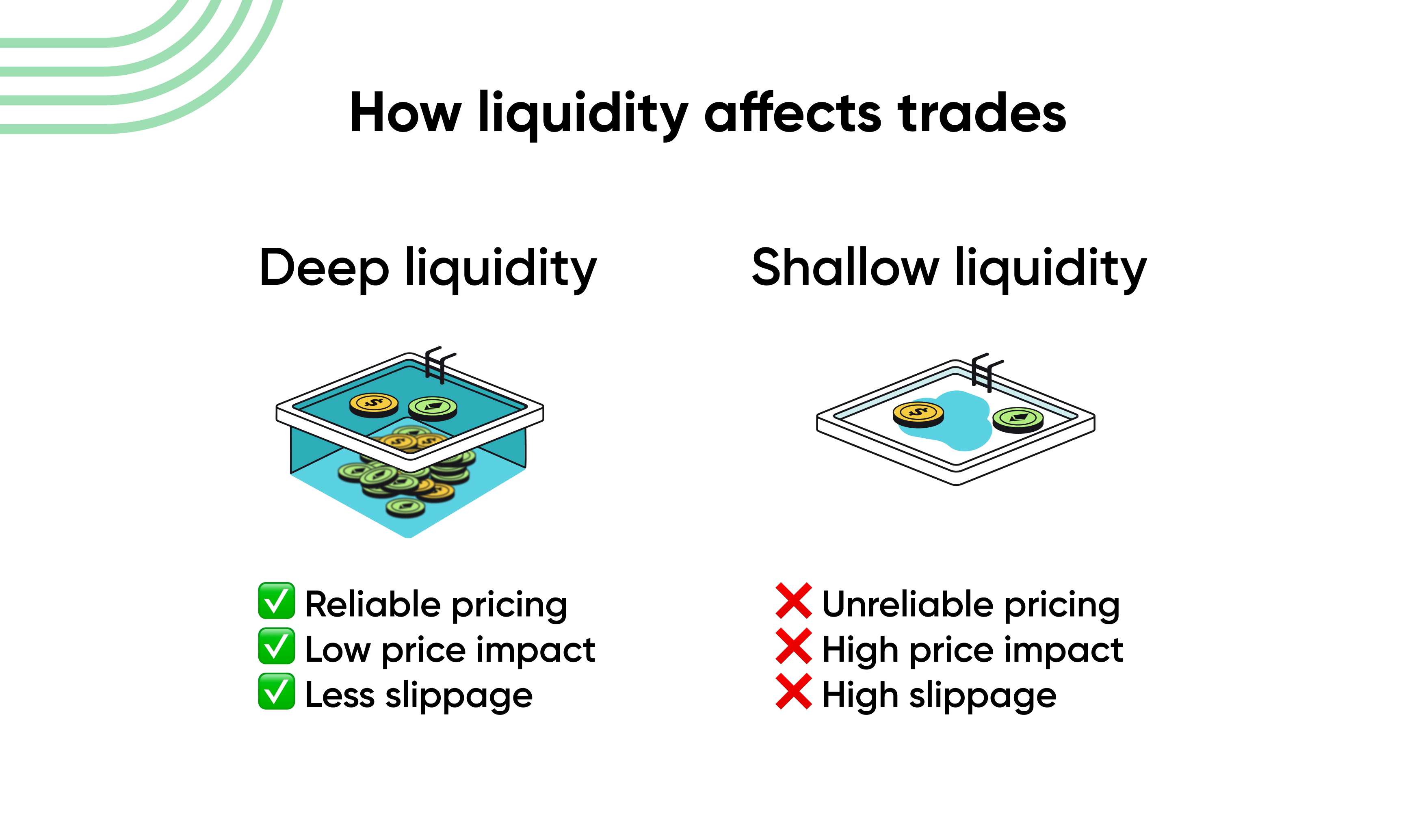

Swap execution quality depends on reserve depth. Deep pools produce low slippage; shallow pools produce sharp price impact. The model is predictable: no dynamic tiers, no range gaps—just reserves versus trade size.

The core limitation of this model that motivated V3 is capital inefficiency. A $1M position spreads from zero to infinity, so if most volume is between $1,800 and $2,200 ETH, most capital sits idle. Nevertheless, V2 is still seeing use in particular cases.

Uniswap V3

V3 introduced concentrated liquidity, letting LPs deploy capital inside a chosen price range rather than across the full curve. Concentrated liquidity increases effective depth at the current price and can reduce slippage for liquid pairs.

It introduced so-called out-of-range risk: if the price leaves LP’s range, they stop earning fees immediately. The deployed capital also converts toward the asset that declined relative to the pair. Example: provide ETH/USDC liquidity between 1,800 and 2,200; if ETH rallies to 2,500, the position becomes 100% USDC and 0% ETH. You earn nothing unless the price returns to the previous levels.

Tight ranges also increase capital efficiency and fee capture when in-range, but go out-of-range faster. Wide ranges reduce management but converge toward V2 behavior. If you trade outside the dominant liquidity cluster (because LPs have not rebalanced), you may face thinner liquidity than a comparable V2 pool with the same TVL.

V3 supports multiple pools per pair with different fee tiers—0.01%, 0.05%, 0.30%, or 1.00%. Routing logic may split trades across pools to minimize total cost, balancing explicit fees and implicit slippage. Swappers typically let the router choose; LPs choose the tier and accept its risk/return profile.

Uniswap V4

V4’s defining feature is hooks: custom smart contract functions that run at specific points in the swap and liquidity lifecycle (before/after swap, before/after liquidity changes). In this iteration pools become programmable primitives without forking core logic, which can enable:

- Dynamic fees based on volatility, time, or oracle data

- On-chain limit orders by gating execution on price thresholds

- Custom rebalancing logic that can automate what V3 made manual

In addition to hooks, V4 introduces a PositionManager using ERC-6909 for internal accounting, reducing gas costs versus ERC-721 NFTs in V3. The user experience remains broadly similar: you still hold a tokenized claim on a position, just under a different standard.

Core Mechanics of Uniswap

In a nutshell, Uniswap executes swaps through on-chain smart contracts that manage token reserves directly: you submit an input token to a liquidity pool, the pool recalculates its reserve ratio according to an invariant, and the output token is transferred. The mechanics that determine output are visible on-chain before you confirm the transaction.

Liquidity Pools

Liquidity pools are smart contracts holding reserves of exactly two tokens—token0 and token1 in internal state—managed by an automated market maker formula. In other words, on Uniswap and other AMM-powered DEXs, you are not trading with another person but against pooled reserves.

Each pool supports one trading pair. A USDC/ETH pool holds USDC and ETH. If you swap DAI for WBTC, the router may chain multiple pools (DAI/ETH, then ETH/WBTC), but each pool still handles exactly one pair.

And as already was explained, liquidity providers fund the reserves by depositing both assets in the pool ratio. Once deposited, liquidity is available to any swap that meets the pool’s constraints—no per-trade approvals from LPs.

Price and Slippage

Uniswap’s constant-product formula requires the product of reserves to remain constant before and after a swap: x × y = k, where x and y are reserves and k is the invariant that must not decrease after the swap completes. Price is derived from the reserve ratio.

Spot price is instantaneous but execution price is the average across your trade size. The gap between them is called price impact, a direct consequence of the invariant.

Speaking of which, slippage is the difference between the expected price at submission and the executed price at block inclusion. It comes from reserve changes before your transaction lands in the blockchain ledger and from your trade size relative to liquidity.

A feature called slippage tolerance is your guardrail but it requires your knowing what it does. You set a minimum output (or maximum input). If execution would violate it, the transaction reverts. You still need to pay gas for the attempt, but your tokens are not swapped.

Uniswap Fees

Uniswap swap fees and network gas fees are separate costs.

- Swap fee (0.05%, 0.3%, or 1% depending on v3/v4 pool configuration) is taken from the input before output is calculated.

- Network gas fee is paid to validators in the chain’s native token (ETH on Ethereum, POL on Polygon) and fluctuates with the underlying network’s stare, independent of Uniswap.

Swap fees accrue to liquidity providers by being added into pool reserves. LP tokens represent proportional claims on reserves; as reserves increase from fees without issuing new LP tokens, LP positions appreciate mechanically.

How to Swap Tokens on Uniswap

A Uniswap swap is not “one click.” It is a sequence of on-chain actions that often includes two separate transactions: an ERC-20 approval (if needed) and the swap execution. Each consumes gas and requires wallet confirmation.

Transaction Approval

ERC-20 approvals are required only when the token you are swapping from is an ERC-20 contract, not native ETH. Even if you are trading a pair with ETH, normally, Uniswap turns it into Wrapped Ether for you, which is also an ERC-20 token.

Approvals grant an allowance to a spender contract and are necessary for continuous interactions with any smart contract.

Most approval-related losses can be avoided if you:

- Verify the spender address in your wallet before signing. It should match Uniswap’s published router address for your network.

- Choose the allowance amount deliberately: exact amount versus unlimited.

- Approval is separate and must be confirmed first. Until it settles, the swap will fail with “insufficient allowance.”

Token Selection

To make sure the swap goes through at all and does not result in you permanently losing funds, before you swap:

- Confirm the blockchain network matches in both your wallet and the Uniswap interface. If your wallet is on Arbitrum while the interface is on Mainnet, balances and routing will be wrong.

- Verify the token contract address. Name and logo are not security. Cross-reference against official documentation or a trusted token list (including the one maintained by Uniswap Labs).

- Evaluate the routing path. Direct swaps are simpler; multi-hop routes can improve pricing for illiquid pairs but add gas and contract surface area.

- Configure slippage tolerance and transaction deadline. Tight slippage reduces exposure to adverse execution but increases reverts during volatility. Deadlines reduce stale-execution risk but can fail under congestion.

While we are on the topic of security best practices before you actually use Uniswap, here are a few more tips you can follow: cross-reference the token address displayed in Uniswap against the official project source (website, block explorer, CoinGecko, or trusted aggregator) before trading—copycats are a frequent issue—and confirm you are on the right chain while you are at it. Add these to your checklist, too::

- Beware unlimited token approvals — approving the maximum uint256 value (~1.15×10^77) grants permanent spending rights to the Uniswap router; consider exact-amount approvals for unfamiliar tokens despite the higher gas cost of re-approving later.

- Execute a small test swap for unknown tokens — trade $10–$50 first to confirm behavior (transfer fees, blacklist restrictions, decimals).

- Monitor price impact warnings — above 3% deserves scrutiny; above 10% means you are likely moving the market.

- Avoid panic-swapping during extreme volatility — waiting for stabilization often produces better execution.

Transaction Settlement

Next comes the actual swap part: it’s made quite simple with the Uniswap front end. Pick a token pair, input the amounts, review the exchange rate and fees, and confirm—this is it.

The actual finishing line, settlement means inclusion of your swap in a block and subsequent EVM execution. “Submitted” is not “complete.” After settlement, verify outcomes rather than assume or guess:

- On-chain confirmation status — confirm “Success” on a block explorer.

- Final execution price versus quoted price — compare received amount against quote.

- Fees paid — gas (in receipt) plus LP fee (embedded).

- Token receipt in wallet — you may need to import the token manually by contract address.

Providing Liquidity on Uniswap

Providing liquidity turns holders into market participants earning fees from swaps in their pool. The mechanics differ across versions: Uniswap V2 distributes liquidity uniformly across all prices; Uniswap V3 lets you concentrate capital inside chosen ranges.

The return profile combines fee earnings with exposure to impermanent loss. Uniswap does not issue yield farming rewards at the protocol level; returns come from swap fees, not emissions.

How to Create a Position

On V2, the web interface makes it distinct enough despite you similarly choosing a trading pair and supply token ratios matching pool price. Approve ERC-20 spend for each token. Sign the add-liquidity transaction (clear in the front end interface) to deposit and mint LP tokens. Verify the position: V2 LP tokens are ERC-20 and function as a liquidity pool token representing your share.

Uniswap V3 Position Setup:

- Select a trading pair.

- Choose a fee tier (0.01%, 0.05%, 0.3%, or 1%).

- Choose a price range via tick boundaries.

- Supply token ratios based on where price sits inside your range.

- Approve ERC-20 spend for the NonfungiblePositionManager.

- Sign the mint transaction to create the position.

- Verify the position — V3 positions are ERC-721 NFTs with range parameters and fee accrual.

Approvals, mint/add, fee collection, and removal each cost gas; treat gas as part of strategy, not as an afterthought.

Impermanent Loss

The first risk that is usually mentioned in relation to liquidity provision is impermanent loss. It refers to the opportunity cost of providing liquidity versus holding the same tokens. The AMM rebalances as price changes: it sells the appreciating asset and buys the depreciating one to maintain the invariant. Your position can still be profitable in absolute terms if fees exceed the loss, but impermanent loss is structural exposure.

Watch it on numbers: an LP deposits 1 ETH and 2,000 USDC at ETH = $2,000 (the position’s value is, therefore, $4,000). ETH then doubles to $4,000. The AMM rebalances your position to ~0.707 ETH and 2,828 USDC, worth $5,656 but holding would have been $6,000. Impermanent loss is $344, ~5.7%. If the pool was active enough to earn the LP this much from fees, the perceived loss would have been offset, and since these rewards are claimed upon withdrawal and the loss is not realized until then either, the term is “impermanent loss”.

On V3 onwards, if price moves outside your range, your liquidity stops earning fees and becomes effectively single-asset. Rebalancing back in-range requires withdrawing, swapping, and redeploying, costing gas and crystallizing outcomes.

Fee Earnings

Fee earnings accrue pro-rata to liquidity that is active at the time of the swap. In V2, all liquidity is active, and in V3, only in-range liquidity earns. Remember that this does not automatically mean V3 LPs have fewer opportunities.

Furthermore, V3 introduces fee competition inside bands: if many LPs concentrate in the same range, each gets a smaller share of fees. Less crowded ranges can earn more per unit liquidity if volume passes through, but you take a positioning risk: the opposite is likely as well.

APR/APY figures should be viewed as backward-looking projections. Real outcomes depend on trading volume, volatility (both a volume driver and an impermanent loss amplifier), and time-in-range for V3.

If you only look at fee APR without tracking position value versus hold value, you are measuring half the problem.

Liquidity Removal

Removing liquidity reverses the deposit process but can include multiple transactions, especially in V3.

Withdrawal Sequence:

- Choose partial or full withdrawal.

- Confirm interface settings if presented.

- Sign remove-liquidity transaction.

- Collect accrued fees separately (V3 only).

- Verify token receipt; small dust can remain due to rounding.

Verify token contract addresses, confirm the correct network, and read wallet prompts carefully. Phishing front-ends often rely on users approving a spend when they have intended to withdraw.

UNI Token and Governance

Using the Uniswap Protocol does not require UNI. You can swap and provide liquidity without holding it. So what is the purpose of the UNI token?

UNI is a governance token: it grants voting rights over protocol decisions, not transactional access. UNI holders vote on parameter adjustments, treasury allocations, and upgrades. Governance cannot access user funds, reverse transactions, or override immutable execution rules. This boundary matters: governance shapes policy and incentives, not who owns what.

UNI is not a claim on pool reserves like an LP token would be. It’s not required for gas or staking either: neither execution nor consensus need it, because Uniswap lets underlying blockchains take care of those. Its economic security, value capture, and utility all lie in the rights to influence the development trajectory and day-to-day operations of the Uniswap platform.

Token Distribution

What we have just described was UNI’s tokenomics (economic design that informs user behavior) but its distribution and issuance schedule often get referred to by the same term, so let’s review them, too.

UNI launched in September 2020 via a retroactive airdrop that distributed 400 UNI tokens to eligible addresses that had interacted with the Uniswap Protocol, spanning over 250,000 addresses. The airdrop broadened governance participation without KYC or registration.

Initial allocation vested over four years: community (60%), team and future employees (21.51%), investors (17.80%), advisors (0.69%). The community share included the airdrop, liquidity mining rewards, and a treasury for grants and initiatives.

Starting from 2024, the UNI token supply has a 2% annual inflation rate, to allow new users to join, incentivize activity within the protocol and disincentivize passive holding. Unlike Bitcoin’s deflationary design, where “buy and hold” is all but intended strategy, UNI users get the most bang for their buck by actually putting it to use, even at the cost of its monetary value over time.

Governance Scope and Limits

(a) What governance can change at protocol level:

- Fee tier structures across liquidity pool types

- Protocol fee switch activation

- Treasury allocation

- Smart contract upgrades via new deployments

- Parameter adjustments (thresholds, voting periods, oracle integrations)

(b) What governance cannot do (due to hard protocol and cryptographic constraints):

- Reverse completed transactions or rewrite history

- Access private keys or withdraw from user wallets

- Bypass immutable contract logic without deploying new contracts

- Freeze user positions or restrict withdrawals

- Impose identity requirements or censorship at protocol level

Key Considerations, Risks, and Legality

Uniswap usage exposes you to technical, financial, and regulatory risk categories that scale with size and frequency. A non-custodial model shifts responsibility onto you: no one reverses transactions, no one recovers keys, and the protocol does not police token quality. The practical approach is to know failure modes and build verification habits.

Smart Contract Risk

Uniswap runs through immutable smart contracts deployed on Ethereum and other EVM-compatible chains. Immutable code eliminates admin-key modification risk for deployed core contracts, but means vulnerabilities cannot be patched in-place; fixes can only arrive via new versions in a separate implementation.

What Can Go Wrong:

Contract bugs or exploits — Quality audits can reduce potential risk but not eliminate it.

- Mitigation: Use official interfaces whenever possible and verify contract addresses before approvals/swaps.

Oracle dependencies and price manipulation — Thin pools used as oracles elsewhere can be manipulated.

- Mitigation: For large sizes, check the pool’s total value locked (TVL) depth. A basic guardrail is TVL ≥ 50× trade size for material trades.

Approval surface and unlimited allowances — Unlimited approvals persist until revoked. It exposes you to unauthorized access later down the line in case a smart contract is compromised and your approvals are still active.

To reduce exposure:

- If your wallet app has a “Token Approvals” view feature, use it, or check it with Etherscan’s approval checker.

- Regularly revoke allowances you do not need.

- Use exact-amount approvals for unfamiliar tokens.

The least you can do to mitigate possible risk is to verify the router contract address against official documentation, then review allowances within 24 hours of your first swap.

Token Risk

Even so, protocol correctness does not protect you from a fraudulent token or a toxic pool. Remember that anyone can set up a liquidity pool on Uniswap, and it is a feature, not a bug. Nevertheless, token risk is independent from Uniswap’s contract security.

Core failure patterns:

(a) Fake token / wrong contract address risk

- Observable sign: Address mismatch versus official sources; wildly inconsistent pricing.

(b) Low-liquidity / high slippage risk

- Observable sign: Price impact warnings >5%; low 24h volume relative to your size.

(c) Tax/fee-on-transfer or rebase token behavior risk

- Observable sign: Explorer warnings or documentation mentioning burn rates, redistribution, elastic supply.

(d) Honeypot / sell restriction risk

- Observable sign: No sell transactions; blacklist/pause logic; transfers revert on sell.

Verifying token contracts without repeating earlier swapping steps:

- Cross-reference contract address from an official project source and a reputable explorer.

- Confirm pool pairing and liquidity depth; verify reserves via explorer links.

Additional verification checkpoints:

- Verified source code on Etherscan

- Decimals consistency

- Supply sanity checks against reputable indexes

Be aware that token metadata (name, ticker, icon etc.) is cosmetic. A contract named “Tether USD” is not necessarily the canonical USDT contract (0xdac17f958d2ee523a2206206994597c13d831ec7 on Ethereum). For any token outside of the Uniswap default list, at the very least verify the contract address on Etherscan against an official source and check for at least $100,000 liquidity.

Self-Custody Responsibilities

Non-custodial nature of Uniswap and other similar DEXs means you own every operational failure mode: cryptographic keys, device hygiene, approvals, gas settings, and the irreversibility of transactions.

What responsibilities you should expect:

Private key / seed phrase custody: the first rule is to write it on a physical backup; never digitize it.

Wallet security hygiene: install from official sources; review dApp connections; revoke unused sessions.

Device and browser risks: avoid shared devices; for meaningful size, use a hardware wallet (Ledger, Trezor).

Transaction finality: test transfers for high-value actions; double-check addresses. As is almost always the case, transactions are irreversible.

Gas management: use suggested settings and check trackers during congestion.

Regulation and Compliance Considerations

Decentralized finance exists in a fragmented regulatory landscape. The practical approach is to separate protocol-level, interface-level, and user-level obligations.

(a) Protocol (smart contracts) — autonomous, no custodian, no centralized gatekeeping.

(b) Interface / operator (app providers) — entities operating frontends are subject to regulation. One particularly telling case is when Uniswap Labs received a Wells notice from the U.S. Securities and Exchange Commission in April 2024; in February 2025 the SEC closed its investigation without filing charges.

(c) User obligations — taxation and compliance apply regardless of decentralization.

If you only do one thing: Confirm whether crypto-to-crypto swaps are taxable in your jurisdiction and set up a logging workflow before your first trade.

Uniswap vs Alternatives

| Criterion | Uniswap | Centralized Exchanges (CEXs) | PancakeSwap | Other AMMs (e.g., SushiSwap) |

|---|---|---|---|---|

| Custody model | Self-custody; user holds private keys | Custodial; exchange controls funds | Self-custody; user holds private keys | Self-custody; user holds private keys |

| KYC/identity | No KYC required for swaps | KYC typically required | No KYC required for swaps | No KYC required for swaps |

| Market structure | AMM (Automated Market Maker) | Order book (limit/market orders) | AMM (Automated Market Maker) | AMM (various formulas) |

| Typical fee components | Protocol fee (variable, currently 0% to 0.05%) + network gas fee | Trading fee (0.1%–0.5%) + withdrawal fee | Protocol fee (0.01%–1%) + BNB Chain gas fee | Protocol fee (0.25%–0.3%) + network gas fee |

| Price execution drivers | Liquidity depth in pools, MEV exposure, slippage from large trades | Order book depth, maker-taker spread, latency | Liquidity depth in pools, lower gas costs on BNB Chain | Liquidity depth, routing efficiency, AMM formula type |

| Asset availability | Permissionless listings; anyone can create a pool | Curated listings; exchange decides which tokens to list | Permissionless listings; anyone can create a pool | Permissionless listings; anyone can create a pool |

| Chain/ecosystem focus | Ethereum mainnet, Arbitrum, Optimism, Polygon, Base, and others | Multi-chain via centralized infrastructure | BNB Chain (BSC) primarily | Ethereum mainnet and various L2s/sidechains |

| Composability (DeFi integrations) | High; integrates with lending, yield aggregators, derivatives | Low; siloed platform with limited external composability | Moderate; integrates with BSC DeFi ecosystem | High; varies by chain and protocol design |

| Support/recourse | No customer support; code is law, community forums only | Customer support available; dispute resolution process | No customer support; code is law, community forums only | No customer support; code is law, community forums only |

| Primary risks | Smart contract risk, impermanent loss, MEV, liquidity fragmentation | Platform insolvency, withdrawal freeze, regulatory seizure, counterparty risk | Smart contract risk, impermanent loss, bridge risk when moving assets | Smart contract risk, impermanent loss, protocol-specific governance risks |

Uniswap vs Centralized Exchanges

The core difference is custody and counterparty exposure. Uniswap is self-custodial with on-chain execution, which exposes users to smart contract risk and token risk. Centralized exchanges (CEXs) essentially hold custodial IOUs on users’ behalf, use internal matching, and carry platform and withdrawal risk.

Cost diverges for the same reason. On Uniswap you pay LP fee + gas + any interface fee, and you experience price impact. On a CEX you pay trading fees and later withdrawal fees, but you do not pay gas directly at trade time.

Compliance and access are equally structural: CEXs tend to require KYC/AML and can restrict accounts; Uniswap protocol swaps do not require identity verification, but fiat rails generally live in KYC environments.

Choose Uniswap (and DEXs generally) if:

- You prioritize self-custody and want to eliminate counterparty risk

- You trade long-tail tokens not listed on CEXs

- You need access without KYC gatekeeping

- You value censorship resistance

- You trade on Layer 2 where gas is low

Think twice or avoid Uniswap if:

- You need direct fiat on-ramps/off-ramps in the same trading venue

- You execute very large orders and require deep order book liquidity

- You prefer customer support and recourse

- Self-custody risk is operationally unacceptable

- You trade small sizes on mainnet where gas dominates

Uniswap vs PancakeSwap

The difference here is ecosystem gravity. Uniswap is Ethereum-native and deeply integrated with Ethereum L2s. PancakeSwap is the strongest on the BNB Chain.

BNB Chain is cheaper per transaction, which matters for small frequent trades. The trade-off is decentralization and validator-set concentration. If you bridge to BNB Chain to access PancakeSwap liquidity, you inherit bridge risk—one of the most exploited surfaces in crypto.

Choose PancakeSwap if:

- You already hold assets on BNB Chain

- You trade BNB-ecosystem tokens with deeper BNB Chain liquidity

- You make frequent small trades and want low fees

- You prefer simpler LP flows and accept the decentralization trade-off

Think twice or avoid PancakeSwap if:

- You prioritize decentralization and Ethereum security assumptions

- You trade Ethereum-native tokens with deeper Uniswap liquidity

- You want Ethereum DeFi composability

- You want to minimize bridging risk

Uniswap vs Other Automated Market Makers

Uniswap V3’s concentrated liquidity is efficient for volatile pairs when LPs manage ranges. Constant-product pools (Uniswap V2 but also SushiSwap) are simpler but less efficient. Curve is optimized for near-parity assets (i.e. stablecoins).

Other DEXs also tend to rely more on incentives and liquidity mining than Uniswap presently. SushiSwap, for example, uses incentives and protocol emissions to attract liquidity, which can be powerful short-term but less reliable if emissions decline. Uniswap’s liquidity is often more fee-driven than subsidy-driven, opting for organic value capture rather than printing rewards and inflating supply along with it.

DEX aggregators like 1inch, Matcha (previously 0x), and CowSwap can search multiple venues for best execution, especially for large trades. Uniswap routes across its own pools, which also finds the optimal rate but is inherently limited by comparison. For small trades on mainnet, aggregator overhead can offset gains.

Choose Uniswap over other AMMs if:

- You want concentrated liquidity efficiency on v3

- You prioritize liquidity depth and routing quality on Ethereum/L2s

- You prefer minimal incentive dependency and clearer mechanics

- You want to minimize contract surface area versus aggregators (when quotes are similar)

Choose SushiSwap or other AMMs if:

- Incentives materially improve your net outcome on specific pairs

- Another venue has clearly deeper liquidity for your pair

- You are trading stablecoins where Curve is structurally superior

Conclusion

Uniswap consolidates four mechanisms into one protocol stack: AMM pricing through liquidity pools, self-custody swaps executed on-chain, liquidity provision with fee revenue and impermanent loss exposure. In a non-custodial environment, gas costs, slippage discipline, and verification habits are not optional—they are the cost of admission. UNI-fuelled governance routes protocol policy decisions through token-holder votes rather than centralized operators, justifying the token.

To stay in the loop of the latest crypto news and projects, subscribe to ChangeHero blog and follow us on Twitter, Facebook, and Telegram.

Frequently Asked Questions

Is Uniswap Safe?

Uniswap protocol smart contracts present a distinct risk profile from the interface you use to access them and the security posture of your own wallet or device. The protocol’s non-custodial design means Uniswap Labs cannot reverse transactions, freeze assets, or recover funds sent to incorrect addresses. Responsibility is yours.

Is Uniswap Legal?

Legality depends on the jurisdiction in which you reside, the specific tokens you trade, and how you use the decentralized exchange—Uniswap protocol itself is open-source software deployed on public blockchains, but access restrictions and regulatory interpretations vary by region. Permissionless access does not remove compliance duties.

Does Uniswap Require KYC?

The Uniswap protocol does not collect or verify user identity—KYC obligations arise from wallet providers, fiat on-ramps, or third-party services linked from the application interface, not from interacting with the smart contracts themselves.

Uniswap is a decentralized application built on top of a broader blockchain protocol stack (Ethereum and compatible networks), and it is commonly used as infrastructure in the wider cryptocurrency market for swapping, hedging, and portfolio rebalancing. When you swap on Uniswap, you are converting one crypto asset into another, and your transaction history is publicly visible on-chain—so while the protocol does not ask for your identity, users should not assume strong financial privacy by default.

What Wallets Work With Uniswap?

Uniswap supports any Ethereum Virtual Machine-compatible wallet that implements WalletConnect protocol or browser extension standards and allows you to manually select the correct blockchain network for your intended trade. You connect a crypto wallet and sign locally; keys do not leave your device.

What Fees Does Uniswap Charge?

Uniswap swaps incur three distinct fee categories: network gas fees paid to validators, liquidity provider fees embedded in the pool's exchange rate, and optional interface or routing fees that may be applied by Uniswap Labs or third-party frontends.

What Is Slippage?

Slippage is the difference between the exchange rate you expect when you submit a swap and the actual execution rate you receive, caused by pool price movement between submission and confirmation or by your trade size relative to available liquidity. Manage it by calibrating tolerance to token type and liquidity conditions, while remembering the trade-off: low tolerance increases reverts; high tolerance increases vulnerability to MEV and adverse execution.

What Is Impermanent Loss?

Impermanent loss is a liquidity-provider-specific phenomenon describing the opportunity cost of providing liquidity to an automated market maker pool compared to simply holding the same two tokens in your wallet, caused by the pool's constant-product rebalancing mechanism responding to external price changes. It applies to LPs, not swappers. In V3, narrow ranges amplify both fee potential and out-of-range risk.

How Do I Avoid Fake Tokens on Uniswap?

Fake tokens exploit Uniswap's permissionless architecture by creating malicious contracts with names and symbols that mimic legitimate projects, relying on user error during token approval and swap confirmation to drain funds. If a token requires >5% slippage for a small trade, shows abnormal behavior, or lacks credible documentation, treat it as high-risk.

Why Did My Transaction on Uniswap Fail?

Transaction failures occur when the Ethereum Virtual Machine reverts your submitted transaction due to unmet execution conditions, insufficient gas, restrictive token contract logic, or stale pricing assumptions embedded in your signed transaction data.

Do not spam retries with identical parameters. Replace-by-nonce is the correct “speed up” path; a self-send with the same nonce is the standard cancel path.

What is the Uniswap (UNI) price prediction?

For forecasting scenarios and market-cycle framing, see Uniswap (UNI) price prediction, keeping in mind that execution mechanics, liquidity conditions, and regulatory headlines can materially affect outcomes.

What is the live Uniswap (UNI) price?

For a live reference of the current token quote, see Uniswap (UNI) price.