Best Crypto On-Ramp: Where to Buy and Sell Directly

Contents

- 1. What a Crypto Onramp Is and How It Works

- 2. Key Features to Compare

- 3. Top Crypto Onramps for 2026

- 4. Fees and Total Cost

- 5. KYC and Identity Verification

- 6. Onramps’ Risks, Legality, and Key Considerations

- 7. How to Choose the Right Crypto Onramp

- 8. Crypto Onramp Selection for Businesses

- 9. Integration Options for Developers

- 10. Future Trends (2026 and Beyond)

- 11. Conclusion

Brief History of Crypto On-Ramps

Crypto on-ramps are the essential bridge between traditional fiat currency and the digital asset ecosystem. They let you convert dollars, euros, or any other government-issued currency into cryptocurrencies like Bitcoin or Ethereum, and that single step changes how you access everything else: wallets, DeFi, NFTs, and on-chain payments. Without an onramp, crypto becomes a closed loop—you can’t join unless you already have crypto.

The story also mirrors crypto’s “growing up” era. In Bitcoin’s early days, getting crypto meant mining it yourself or trading on forums like BitcoinTalk. Then came early exchanges like Mt. Gox in 2010—an important milestone, but one that also highlighted how fragile and underregulated the first fiat-to-crypto attempts were. The real shift happened around 2014–2015, when Coinbase and Binance arrived with institutional-grade infrastructure: eventually, with bank-level security, compliance frameworks, and clearer fee structures. That’s when onramps stopped feeling like an experiment and started looking like a financial product.

Today, onramps aren’t one-size-fits-all. For first-time buyers, a good onramp feels like a normal checkout flow (link a bank account, confirm, done). For active traders, speed and reliability matter as much as price because a delayed deposit can be the difference between catching a move and watching it pass by. Building on that, regulation and technology have pushed onramps into a new phase: faster settlement, more embedded “buy crypto” experiences inside wallets and dApps, and stronger compliance thanks to frameworks like MiCA (Markets in Crypto-Assets). In simple terms, buying crypto has started to feel less like the Wild West and more like modern fintech.

What a Crypto Onramp Is and How It Works

Credit/source: Utorg.pro

In a roundabout way, a crypto onramp connects traditional financial systems to the cryptocurrency ecosystem by converting fiat currency into digital assets. Think of it as the bridge between your bank account and blockchain networks—without onramps, plenty of people would have no practical way to acquire crypto unless someone handed it to them directly.

Here’s the typical flow: you select the cryptocurrency you want, enter your payment details (credit card, bank transfer, or another fiat payment method), verify your identity, and receive crypto in your wallet. The on-ramp service handles the conversion rate, processes the payment through traditional banking rails, and settles the transaction on the blockchain.

That sounds simple. Under the hood, it’s not. Onramps have to integrate with payment processors, comply with financial regulations like KYC (Know Your Customer) and AML (Anti-Money Laundering) requirements, manage liquidity pools, and bridge multiple blockchain networks. They’re essentially operating in two worlds at once: the regulated banking system and the decentralized crypto space.

Most onramps display the exchange rate upfront, including any fees. Some charge a percentage of the transaction (typically 2–5%), while others add a flat fee or mark up the exchange rate slightly. Speed varies too: credit card purchases often complete in minutes, while bank transfers can take several business days depending on your location and the platform’s processing times.

Fiat-to-Crypto Onramps

Fiat-to-crypto onramps dominate the market because they solve the most common entry problem: turning dollars, euros, or other government currencies into Bitcoin, Ethereum, or stablecoins. Platforms like Ramp Network, Transak, and MoonPay lead this space, each bringing different strengths to the table.

For example, Ramp Network specializes in embedded solutions, meaning it powers the buy-crypto buttons you see inside DeFi apps and Web3 wallets. Rather than forcing users to leave the app and visit an exchange, Ramp integrates directly into the user experience. It supports over 150 countries and offers multiple payment methods, from Apple Pay to instant bank transfers in Europe through open banking protocols.

Custodial Onramps

Custodial onramps hold your cryptocurrency on your behalf, similar to how a bank holds your fiat currency. When you buy crypto through Coinbase or Binance, the platform stores those assets in accounts they control, and you access them through your login credentials.

The security model relies on the platform’s infrastructure. Coinbase, for example, stores the majority of customer funds in cold storage (offline) and maintains insurance coverage for digital assets held in their hot wallets. They implement enterprise-grade security protocols—think multi-signature wallets, hardware security modules, and 24/7 monitoring systems that most individual users couldn’t replicate on their own.

This setup has real advantages for beginners. If you forget your password, you can reset it. If you suspect unauthorized access, customer support can freeze your account. You also avoid the responsibility of managing private keys and seed phrases, which removes the risk of permanent loss through user error.

The trade-off is trust. “Not your keys, not your crypto” exists for a reason: custodial platforms can freeze accounts, face regulatory actions, or (in worst-case scenarios) become insolvent.

Credit/source: Coinbase.com

Custodial onramps make the most sense if you prioritize convenience, keep relatively modest amounts on-platform, or plan to actively trade rather than hold long-term.

Non-Custodial Onramps

On the other hand, non-custodial onramps send cryptocurrency directly to a wallet you control, never holding your funds at any point in the process. Services like Bleap and Ramp Network (which offers both custodial and non-custodial options) let you maintain complete ownership of your private keys throughout the entire purchase flow.

Bleap operates as a pure non-custodial onramp, meaning when you buy crypto through their platform, it lands in your self-custody wallet immediately. You provide the wallet address, complete the payment, and receive the funds while Bleap never has access to move those assets. That model appeals to users who take “not your keys, not your crypto” seriously and want to remove third-party custody risk from the equation.

The tradeoff here is that the responsibility shifts to you. If you lose access to your wallet, there’s no password reset. If you send funds to the wrong address, no support team can reverse the transaction. That’s why non-custodial onramps are best once you’re comfortable with self-custody basics and your own security routines.

In practice, the market splits like this: custodial services like Coinbase and Binance dominate the beginner and active trader segments, while non-custodial options like Bleap attract users who prioritize sovereignty and accept the added responsibility. Ramp Network’s hybrid model (both custodial accounts and direct-to-wallet purchases) reflects reality: different users have different priorities, and one size doesn’t fit all in crypto access.

For a real example of how onramps work, you can read the guide we wrote for our users that walks you through the process and describes the practical benefits.

Key Features to Compare

Choosing the best crypto onramp is more than considering the headline fee. The important detail is how the whole experience behaves in the real world: what the flow looks like, where it works, what it supports, and what happens when something breaks.

Transaction Flow

This is the number of steps between your fiat money and your crypto wallet. The simpler the flow, the fewer chances users have to drop off, hit errors, or second-guess the process.

Custodial onramps tend to follow a familiar pattern: create an account, verify identity, then buy crypto that lands in the platform’s wallet. If you want self-custody, you add a fourth step—withdraw to your own wallet. That’s extra friction, but it also means compliance checks are handled upfront, and repeat buys can feel faster and more predictable.

Non-custodial onramps compress this. Platforms like Ramp and MoonPay let users buy crypto that goes directly to their Web3 wallet in one transaction. KYC still happens (most of the time), but it’s often inline and automated, so it feels more like a checkout than opening a bank account.

For developers building dApps in particular, flow affects conversion rates dramatically. A custodial flow often means users leave your app, sign up somewhere else, then (hopefully) return. A non-custodial embedded flow keeps users in your interface the whole time, which is why embedded widgets typically see higher completion rates.

Coverage

By AkhilV1998 - Own work, CC BY-SA 4.0, https://commons.wikimedia.org/w/index.php?curid=144443416

Geographical reach isn’t uniform across crypto onramps, and “global” claims can be misleading. A platform might support a country on paper but offer only one payment method there, usually credit cards with restrictive limits.

According to QuickNode’s analysis of leading fiat onramps, the top platforms vary significantly in coverage. Transak operates in 160+ countries with support for 150+ payment methods. Ramp covers 180+ countries with strength in European and North American markets, while MoonPay supports 160+ countries with strong penetration in regions where banking integrations are more developed.

Payment method availability is where the real differences show up:

- Cards offer wide reach, but higher fees and stricter limits.

- Bank transfers (ACH, SEPA, faster payments) tend to be cheaper, but aren’t available everywhere.

- Alternatives like Apple Pay, Google Pay, PIX, or UPI can massively improve conversion in specific regions.

If you’re targeting users in Southeast Asia, Latin America, or Africa, verify the onramp works with the rails people actually use in those regions—not just that the country appears on a supported list.

Asset Support

Asset support defines which use cases an onramp can serve. An onramp that only offers Bitcoin and Ethereum can cover “getting started,” but it won’t help users onboarding into DeFi on Polygon or ecosystems on Avalanche.

Coming back to our example, Ramp demonstrates how broad this can get, supporting digital assets across 90+ blockchain networks. In practical terms, that can let someone buy USDC directly on Polygon instead of buying ETH on Ethereum mainnet, paying high gas fees to bridge, then swapping. That’s not just convenience—it’s fewer failure points and often real savings.

Today, we are way past limiting the crypto experience to BTC and ETH; stablecoin support deserves special attention. Platforms that offer USDC, USDT, or their alternatives across multiple chains give users flexibility for DeFi onboarding without immediate exposure to volatility. For international users, stablecoins can also function as a dollar-denominated “parking spot” when local banking access is limited.

Token diversity impacts developer integration too. If your dApp runs on a smaller chain, you’ll want an onramp that supports it natively or provides a seamless bridge path. Coinbase offers extensive asset support, but it’s largely aligned with what’s available on its exchange. Specialized onramps like Transak and Ramp often move faster on emerging networks.

Integration Tooling

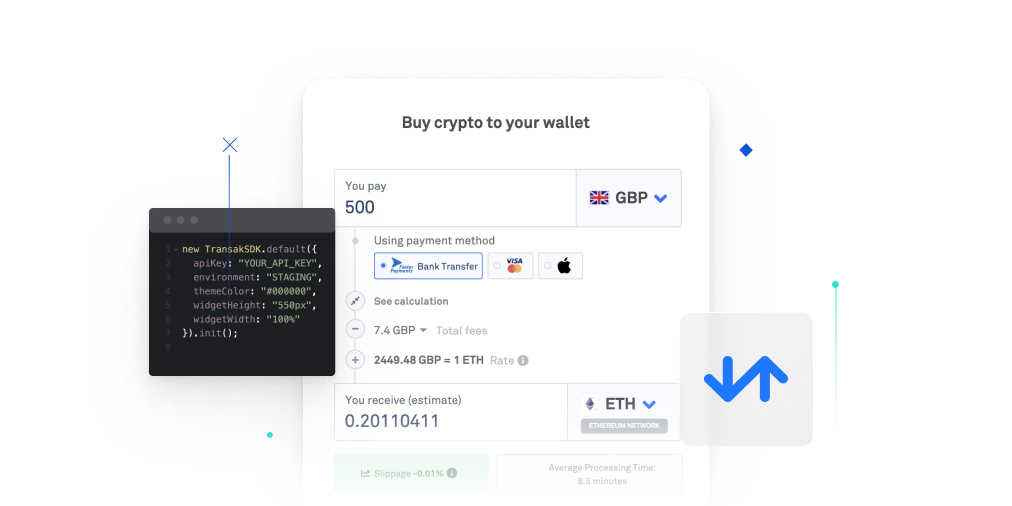

For developers, this is where the differences become obvious. Some solutions are fully API-driven; others are essentially “drop in a widget and configure it.”

API-based integrations (Transak, Wyre) offer maximum control: custom flows, webhooks, and deep UX ownership. The trade-off is complexity—you handle error states, state management, and API version changes. This approach is worth it if you need customization or you’re integrating into an existing fintech stack.

SDK options reduce the workload in comparison. Ramp’s JavaScript SDK, for instance, can embed an overlay inside your application so users never leave your domain. The SDK typically handles compliance, payments, error states, and delivery to the correct address.

Credit/source: Coinbase Docs

No-code widgets are the fastest path. Copy an embed snippet, configure wallet address and assets, match your branding, and you’re live. MoonPay and Transak both offer this style, which is ideal for content sites and community projects that don’t want backend complexity.

For any type, documentation quality matters more than teams expect. When you’re troubleshooting a failed transaction at the worst possible time, clean examples and clear error references save hours.

Customer Support

As is the case with many crypto services, support quality varies wildly across crypto onramps, and it affects your users most when things go wrong (pending transactions, rejected documents, missing deposits).

Response times create expectations. Coinbase, as one of the most illustrative examples, offers tiered support with priority access for high-volume partners, but standard response times can stretch to 24–48 hours for individual users. Smaller, focused platforms like Ramp often respond faster because they position support as a differentiator.

Channels matter too. Email-only support can be painful for time-sensitive issues; live chat (even if it starts with a bot) gives users immediate triage. Phone support is rare, though some enterprise tiers include it. Developers should also consider whether they get dedicated integration support or technical account managers.

One often-overlooked point: when you embed an onramp in your product, users will blame you first and the onramp second. Their support quality becomes part of your brand experience.

Top Crypto Onramps for 2026

Without further ado, let’s dive into the list of crypto on-ramps as of 2026 that deserve the most attention. This list is only about what matters: coverage, integration quality, asset support, compliance, and user experience.

MoonPay

MoonPay focuses on global accessibility. Where many onramps struggle with payment methods or regional restrictions, MoonPay supports credit cards, debit cards, bank transfers, Apple Pay, Google Pay, and local payment methods in certain regions.

This flexibility is especially valuable for international users. The flow stays simple: choose your amount, pick a payment method, complete identity verification, and receive assets typically within 10–30 minutes. MoonPay also powers “Buy Crypto” buttons inside many wallets and NFT marketplaces, so you’ve likely used it without noticing.

Ramp Network

Ramp Network is built for deep Web3 integration and strong digital asset coverage. The platform supports transactions across more than 80 blockchains and connects with over 110 digital assets, which matters in a multi-chain world.

If you need tokens on Polygon, Solana, or Layer 2 networks, Ramp’s support can remove extra swaps and bridging steps. The KYC flow is optimized for speed, often completing in minutes. For developers, Ramp offers APIs and SDKs designed for embedded “stay-in-app” purchases, which is why it’s popular with DeFi and GameFi platforms.

Transak

Transak has carved out a niche with one-step transactions inside wallets and dApps. Instead of sending users off to an exchange and asking them to navigate transfers and networks, Transak collapses the journey into a single embedded flow.

Credit/source: Transak.com

That matters because crypto onboarding can be a gauntlet: create an exchange account, verify identity, buy crypto, set up a wallet, learn addresses and networks, then transfer. Transak reduces the number of exits where users abandon the process.

It supports over 160 cryptocurrencies and works with more than 300 wallet and dApp partners. The service handles compliance in over 160 countries, which is a big reason it shows up inside apps like MetaMask, Trust Wallet, and Ledger Live.

Coinify

Coinify is one of the most beginner-friendly entry points into cryptocurrency, built on the infrastructure of one of the oldest and most regulated exchanges in the space. The interface is clean and familiar—more “banking app” than “trading terminal.”

What makes Coinify stand out is regulatory positioning. Operating under stringent E.U. regulations and licensed in multiple jurisdictions, it offers the kind of institutional backing first-time buyers care about. The trade-off is cost: Coinify fees are approximately 1.5% per transaction, which is higher than some competitors, reflecting the security and compliance overhead.

It also plays nicely with self-custody. You can buy crypto and then move it into decentralized applications or cold storage. You’re not locked in, even if many users choose to stay for convenience.

Paybis

Paybis is geared toward broad fiat currency support, including over 180 fiat currencies. That’s valuable for international users and for businesses operating across multiple markets.

It also leans into business features: corporate accounts, higher limits, batch processing, and dedicated account managers for companies regularly converting between fiat and crypto. Paybis offers a white-label solution too, letting businesses provide onramp services under their own brand while Paybis handles the compliance framework.

Mercuryo

Mercuryo blends onramp functionality with exchange-style swaps. You can buy with fiat, then swap between digital assets without leaving the platform—useful if you want to split a purchase between Bitcoin, Ethereum, and stablecoins in one session.

Mercuryo supports over 100 cryptocurrencies and dozens of fiat currencies. It emphasizes speed and fraud detection, including machine learning systems that flag suspicious behavior while letting legitimate transactions clear quickly. For businesses, it also offers API access and widgets.

Stripe Crypto Onramp

Stripe Crypto Onramp brings familiar payment infrastructure into the crypto space. If you already use Stripe, integration can be straightforward, leveraging existing Stripe accounts and APIs.

Stripe’s advantage is customization: businesses can build fully branded crypto purchase experiences rather than dropping in a generic flow. Stripe handles payment processing, compliance, blockchain interactions, custody, and the backend complexity. Global reach and regulatory compliance in over 40 countries make it particularly relevant for international businesses.

Bleap

Bleap leans into a non-custodial model with low fees and instant settlement. Users control their private keys throughout the transaction, which removes counterparty custody risk.

This isn’t just philosophical. Non-custodial architecture removes “platform holds your funds” scenarios, which can reduce certain risks. Bleap’s fees are typically significantly lower than the 1.5–5% range common on traditional onramps, often under 1%. For larger purchases, that difference adds up fast. Instant settlement is also practical—when timing matters (token sales, DeFi moves), hours of delay can be expensive.

FinchPay

Credit/source: FinchPay.io

Last but not least, another provider featured in the ChangeHero platform is FinchPay. The reasons to include it are its EU license, dedication to transparency and commitment to a simple experience; you can see for yourself the simplicity of the process how Finchpay works in our partnership announcement. The rates and fees to purchase and sell cryptocurrencies through FinchPay are consistently competitive, and their selection of available payment options beyond credit and debit cards has extended considerably to include popular local payment rails.

Fees and Total Cost

Pricing Models

Crypto onramps generally use two pricing models: variable percentage-based pricing and fixed-rate transactions. Variable pricing changes based on payment method, purchase amount, and sometimes network conditions. Fixed-rate models quote an all-in price upfront, bundling exchange rates and processing into one figure.

The trade-off is transparency versus simplicity. Variable models reflect real costs (like card processing fees), but they can be hard to predict. Fixed models feel clean, but spreads can be baked into the rate.

For regular buyers, variable models can be cheaper if you stick to ACH or SEPA. For one-time buyers who want certainty, fixed pricing can be worth the premium—just confirm whether the quote is truly all-in or whether network fees appear at the last step.

Spreads

Spreads are the difference between the market rate and the rate you actually get. It’s the “airport exchange booth” problem: even when there’s no obvious fee, the rate itself can be worse.

Coinbase charges approximately 1.5% per transaction, and that doesn’t include spread markup. Binance operates with stated fees between 0.1%–0.5% plus spreads that fluctuate with market conditions. Spreads often widen during volatility, because onramps protect themselves when prices move fast.

To spot spread issues, compare the quoted rate at checkout against real-time prices on CoinGecko or CoinMarketCap. If the gap is larger than the stated fee by more than 0.5%, you’re likely paying a spread premium.

Network Fees

Network fees pay miners or validators to process transactions, and they’re outside the onramp’s control. Ethereum gas can swing from a few dollars to $50+ during congestion. Bitcoin fees usually range from $1–$5 but can spike higher during heavy demand.

What matters is who pays the network fee and when. Some onramps include it in pricing, others pass it through. Some batch withdrawals to reduce per-user costs (often with slower delivery). Sophisticated platforms may optimize timing based on mempool activity or offer fee tiers for faster confirmation.

For planning, check current fees on Etherscan (for Ethereum) or Mempool.space (Bitcoin). If fees are high, waiting—or choosing a Layer 2, if available—can make a meaningful difference.

Chargebacks and Disputes

Chargebacks are a unique headache because crypto transactions are irreversible but card payments aren’t. If someone buys crypto with a credit card and files a chargeback, the onramp can lose both the fiat and the crypto (already delivered). That’s why card purchases have higher fees, lower limits, and sometimes withdrawal holds.

Credit/source: Stripe.com

Providers defend themselves with extensive logs: blockchain receipts, KYC records, IP data. Initiating chargebacks can also have consequences for users—platforms track dispute patterns, and some pursue collections or legal action for fraud. For one, Coinbase’s user agreement explicitly states they’ll report fraudulent chargebacks to credit bureaus and collections agencies.

In simple terms: reversible payment methods (cards, PayPal) usually cost 3–4%, while irreversible ones (bank transfers) can be 0.5–1.5%. That price gap is basically chargeback insurance.

How to Calculate Total Cost (Cheapest Onramp Evaluation)

To evaluate real cost, you need to add the pieces most people ignore: base fees, spreads, payment method charges, network fees, and opportunity costs (price movement during processing).

You can use this formula:

Effective Cost = (Stated Fee % + Hidden Spread %) + Payment Method Fee + Network Fee + (Market Movement During Processing)

Example: You want $1,000 of Bitcoin. Platform A charges 1% fees ($10), but has a 1.5% spread ($15) and $3 network fees, totaling $28 (2.8%). Platform B charges 2% flat ($20) with zero spread markup and absorbed network fees, totaling 2%. Platform B is cheaper even with a higher advertised fee.

The payment method matters a lot. That same $1,000 purchase might cost $35–40 via credit card on Coinbase (1.49% fee + 2% spread + card processing), $15–20 via ACH bank transfer, or potentially just $5–10 through Bleap’s non-custodial option with zero spreads and instant settlement.

Opportunity cost is real too. If a platform takes five business days and the market moves 3%, the “cheap fee” may not matter in the end. Conversely, paying 2% for instant access during a dip can outperform waiting. If you want a systematic view, build a spreadsheet, compare 3–5 platforms on your typical purchase size, and test with small transactions first.

KYC and Identity Verification

Truthfully, KYC can feel annoying but only until you understand why it exists—and what it protects (and doesn’t protect).

KYC Requirements

KYC (Know Your Customer) requires platforms to collect documents and data before allowing transactions. Typically that includes government-issued photo identification, proof of address, and sometimes a selfie for biometric checks.

These requirements come from AML (Anti-Money Laundering) rules. On-ramps that want to operate legally must implement these controls to reduce money laundering and terrorist financing risk. The exact documents vary by jurisdiction and by platform policy.

Most providers use tiered verification. Small limits might be available with minimal info, while higher limits require full documentation. Larger transactions can trigger extra checks like proof of income or source of funds. Institutional accounts face stricter scrutiny still (company registration documents, beneficial ownership disclosures).

The important detail is data handling. Legitimate platforms claim encryption and secure storage, and they also have legal obligations under privacy frameworks like GDPR. But KYC data is still a valuable target for attackers, so you’d be right to treat it as a serious factor when choosing an onramp.

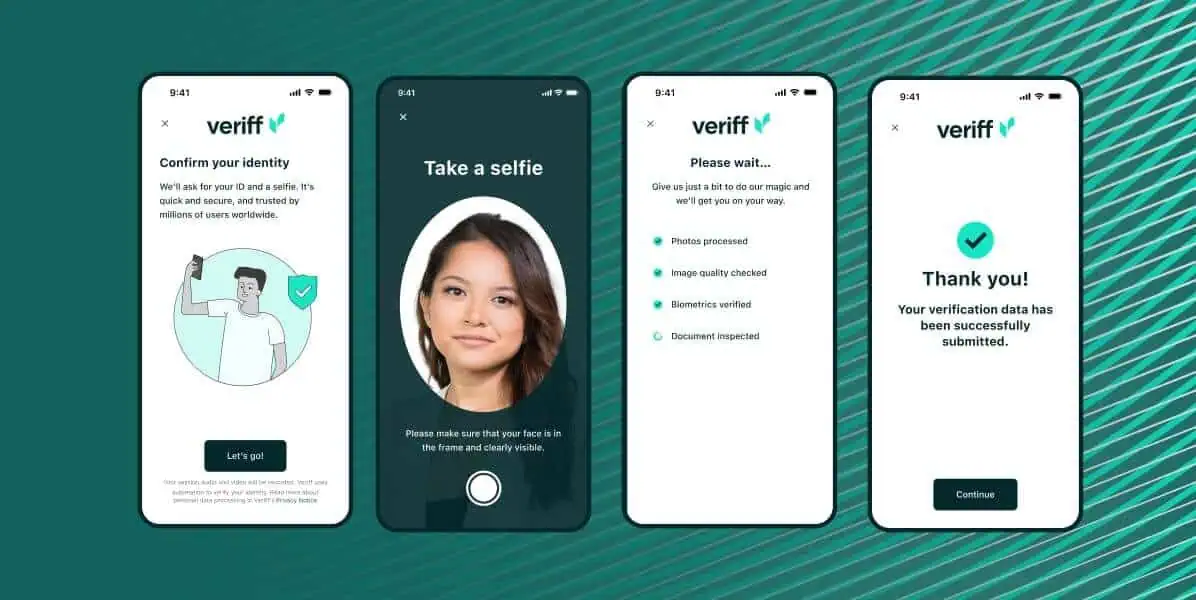

Identity Verification Steps

Credit/source: Veriff.com

Verification usually follows a predictable pattern:

- Upload documents (photos or scans) through web or mobile.

- Automated checks via OCR extract ID data.

- Biometric liveness checks (selfie + movement prompts) help prevent static-photo fraud.

- Third-party verification services like Jumio, Onfido, or Sumsub may run additional authenticity and watchlist checks.

Approval can take minutes for clean submissions, or 24–72 hours when manual review is triggered. Good lighting and clear images make a bigger difference than most users expect.

No-KYC Tradeoffs

Then, there are No-KYC options that can protect privacy and reduce data exposure, on paper. For some users, especially in unstable or restrictive environments, that privacy is more than a preference.

But no-KYC comes with real trade-offs:

- Often strict limits (commonly under $1,000 per day).

- Higher fraud risk (scammers prefer low-friction venues).

- Less predictable platform stability (regulatory pressure can force sudden policy changes or shutdowns).

- Weak dispute resolution (when something goes wrong, recourse is limited).

Some no-KYC activity happens via DEXs, where trades occur on-chain. Others rely on jurisdictions with lighter oversight, or offer optional KYC tiers. For small experimental amounts, no-KYC can be a reasonable choice; but for meaningful sums, regulated onramps usually offer better protections and reliability.

Onramps’ Risks, Legality, and Key Considerations

Crypto onramps touch money, identity, and regulation all at once. That means the risks aren’t just “price goes up and down.”

Regulatory Differences by Country and State

Onramps operate in a fragmented legal landscape. A platform which is compliant in Portugal might be blocked in the U.S. This comes down to classification: some governments treat crypto as commodities, others as securities, and some ban it.

Speaking of the United States, it adds complexity at the state level. New York’s BitLicense (2015) imposes heavy requirements, which is why many onramps block New York residents rather than comply. The EU leans on MiCA for standardization, but member states still add requirements (BaFin licensing in Germany, AMF registration in France).

If you travel or relocate, your usual onramp might become inaccessible. Regulations can also force delistings and new verification requirements seemingly overnight.

Fraud, Scams, and Chargeback Risk

Blockchain irreversibility makes onramps a target for fraud, as covered prior. Once crypto leaves the platform, it can’t be recalled like a bank transfer might be.

The providers are not the only targets. User-facing scams include phishing sites and fake customer support accounts on social media. The precautions against these are the same as across the board: verify information in the official sources, do not share sensitive information like private keys and seed phrases with anyone, and try avoiding search results in favor of visiting the website from your bookmarks.

Provider-facing risks explain common “friction” like withdrawal holds after card purchases. It’s not always great UX, but it’s often risk control. If you’re disputing a legitimate issue (like not receiving crypto), document everything first: screenshots, transaction IDs, and support tickets.

Custody, Counterparty, and Solvency Risk

Depositing funds into an onramp means trusting the platform. Custodial onramps control the private keys, and at a point, you’re holding an IOU.

Credit/source: AwesomeFinTech.com

If the company becomes insolvent, gets hacked, or faces regulatory action, access to funds can vanish. The FTX collapse in 2022 made that painfully clear. Counterparty risk also exists during settlement windows—when fiat has moved but crypto hasn’t yet arrived (or vice versa).

A safer habit is to treat onramps as waypoints, not storage. Buy, then withdraw to a self-custody wallet if you’re holding long-term.

Data Privacy and KYC Data Handling

By its nature, KYC means handing over sensitive information: IDs, proof of address, selfies, and sometimes financial statements. Data breaches can lead to identity fraud, targeted scams, and worse—because unlike a credit card, you can’t “replace” your biometric data.

Platforms in the EU must comply with GDPR, but AML rules also require long retention windows (often five to seven years). Data handling varies widely: encryption standards, audit practices, segmentation, and incident response maturity are not uniform across the space.

Cross-border processing, which is not rare, adds another layer. Data might be collected in one jurisdiction, processed in another, and stored in a third. That can obviously complicate legal recourse if misuse occurs.

Tax Reporting Considerations

On-ramps create a paper trail that tax authorities increasingly use. In many jurisdictions, converting fiat to crypto or crypto to fiat can trigger reporting obligations.

In the US, crypto is treated as property. Capital gains apply when you dispose of assets (selling, trading, converting). Reporting requirements have expanded, and many platforms report activity above thresholds (Form 1099-K and broader broker-style reporting). Europe’s DAC8, put into effect this year, has similar intentions across EU member states.

Tax rules vary dramatically by country: take Germany’s one-year holding exemption, Portugal’s approach to certain trades, Singapore’s lack of capital gains tax for long-term investors, India’s 30% tax plus 1% TDS. Using multiple onramps across multiple jurisdictions can become a serious accounting project.

Limits, Holds, and Settlement Delays

As “instant” the services might be advertised as, it rarely means instant across the whole process.

New accounts often start with low limits that increase after KYC and history, not unlike on centralized exchanges in general. Bank transfers tend to be cheaper but slower, and platforms may hold withdrawals until payments are fully cleared (especially ACH). Cards are faster but pricier and often come with lower limits.

Security holds can also trigger after account changes (email, payment methods, security settings). Compliance holds can freeze activity if monitoring systems flag suspicious patterns, sometimes for days or weeks.

Settlement time also varies by asset and network, and not only because of the technical parameters. Bitcoin and Ethereum are usually quick once cleared, while certain tokens might require extra confirmations or internal treasury approvals.

How to Choose the Right Crypto Onramp

Our list of the best on-ramp options for crypto is not exhaustive, obviously. We highly encourage you to continue doing your homework to see if a product we failed to mention suits your needs the most! Should you go looking further, the best crypto onramp depends on what you’re optimizing for: cost, speed, safety, or simplicity. Most people need a mix.

Credit/source: Swapped.com

Security Controls

Security should be high on the priority list, if not the first point. Check for multi-factor authentication (MFA), encryption, and clear security workflows (login alerts, withdrawal confirmations, device verification). Strong security creates friction you can notice—but that’s not a bad thing.

One of Coinbase’s strengths is that it stores 98% of customer funds in offline cold storage and maintains insurance coverage for digital assets held online. Many on-ramps use fraud detection algorithms that flag unusual activity. Those controls can feel inconvenient in the moment, but they’re often the reason you still have clean funds later.

Compliance Coverage

Strong compliance coverage matters because it reduces the risk of sudden shutdowns, frozen rails, or lost banking partners. Platforms operating in regulatory gray zones can work… until they don’t.

EU requirements (like 5AMLD) and US oversight (FinCEN MSB status and state licensing) shape user experience in very real ways: verification depth, limits, and transaction monitoring. On the other hand, compliant platforms typically have better relationships with banks and payment processors, which can reduce failed transactions and unexplained holds.

Geographic Availability

Before you ask, availability isn’t just “is my country supported?” It’s also: does the onramp support my local currency and my local payment rails? Spreading the transaction across several jurisdictions can also stretch its security, as briefly mentioned above.

Ramp Network does this right by supporting transactions across more than 80 blockchains and connects users with over 110 digital assets in numerous countries, and that kind of reach can reduce the need for expensive international workarounds. If you can deposit in your own currency instead of routing through USD, you may avoid 2–4% FX fees on every purchase.

Also worth checking: is support available in your time zone, and does the onramp have real local integration versus nominal availability?

Payment Acceptance

Payment methods directly shape cost and speed:

- Bank transfers: lowest fees, slower settlement (1–5 business days).

- Cards: instant, higher fees (3–5%).

- Digital wallets (Apple Pay, Google Pay): convenience, often priced similarly to cards, with tokenization benefits.

If you’re buying regularly, low-friction recurring bank transfers can support a dollar-cost averaging strategy without turning fees into a constant drag.

Liquidity and Limits

Liquidity affects execution quality. High liquidity helps large buys clear at expected rates without slippage. Low liquidity can mean you effectively “pay” an extra 2–3% through worse fills.

Limits also matter more than people think. If you want to deploy $50,000 during a dip but your onramp caps you at $5,000 daily, you’ve turned a market plan into a ten-day waiting game. Binance tends to offer higher liquidity and higher limits for verified accounts. Compare limits based on what you’ll actually do, not what sounds nice.

Settlement and Payouts

Settlement time is how quickly crypto hits your wallet (or how soon you can withdraw). Bleap emphasizes instant settlement, with tokens arriving in your wallet within seconds of payment confirmation.

Traditional platforms often impose ACH holds (3–5 days) before allowing withdrawals. You may “see” the crypto but can’t move it. That’s chargeback defense, not random punishment.

Credit/source: PayPal.com

Also check sell-side settlement: fiat withdrawals can take 1–2 business days on some platforms, a full week on others. If fast cash-out matters, this is a deal-breaker feature, not a footnote.

Custody Model

Custody decides who controls the private keys. Custodial platforms (Coinbase) manage keys, backups, and recovery, but introduce counterparty risk. Non-custodial platforms (Bleap) deliver directly to your wallet, removing custody risk but putting full responsibility on you.

A hybrid approach is common: use custodial accounts for active trading, and self-custody for long-term holding.

Crypto Onramp Selection for Businesses

For businesses, an onramp isn’t just a checkout feature. It affects their own compliance posture, reporting, uptime, customer support, and operational risk.

Use-Case Fitness

High-frequency, low-value transactions (gaming, subscriptions) can fit non-custodial solutions that reduce regulatory overhead by not holding customer funds; they are only one option for a specific use, though. Businesses onboarding newcomers often need custodial solutions that guide users through the full journey.

Transaction size also changes requirements. Stripe may suit retail-scale transactions under $10,000. On the other hand, large transfers (over $100,000) often require enhanced due diligence, custom settlement schedules, and dedicated support.

Geographic coverage is another key layer. Businesses serving Europe, Asia, and North America typically need multiple fiat rails (SEPA, FPS, ACH, plus local methods). Ramp Network supports over 150 countries with localized payment methods, which can simplify global operations. According to industry analysis, Ramp Network and Coinbase dominate the market due to their robust capabilities, extensive geographic coverage, and reliable infrastructure.

Risk Management

More so than retail users, businesses need rate locks to protect both the buyer and themselves from slippage. Many enterprise onramps offer 30–90 second rate locks, but this often needs to be negotiated.

Compliance risk changes quickly as regulations evolve and disproportionately affects businesses. Redundancy matters here—keeping a secondary onramp provider can be a practical hedge (even if it’s not your main route).

Integration risk is real too. APIs change. Webhooks fail. Staging environments and ongoing integration tests are not optional at scale.

Liquidity risk becomes material with volume. A major provider may fill a $500,000 order cleanly, while a smaller provider might create 2–3% slippage. Businesses should request evidence of liquidity depth and historical fill rates.

Compliance Operations

Compliance structures differ by region (US MSB registration + state licensing versus EU EMI licensing and passporting). Those differences affect verification flows, limits, and customer experience.

KYC thresholds create product constraints: enhanced due diligence triggers above certain amounts ($3,000 in the EU under 5AMLD, $10,000 in the US under Bank Secrecy Act provisions). Businesses must choose whether to apply checks earlier (lower conversion, simpler compliance) or closer to thresholds (higher conversion, surprise friction at checkout).

AML monitoring can also surprise merchants, especially with non-custodial flows. Even if a third party handles much of the screening, merchants still need documented policies for frozen funds, appeals, and law enforcement requests.

Sector-specific rules matter too. Gaming can overlap with gambling regulation. Healthcare intersects with HIPAA concerns. Financial services face extra scrutiny. Vendor selection should account for these realities upfront.

Vendor Due Diligence

Photo by Sasun Bughdaryan on Unsplash

Don’t just evaluate uptime and UI. With enterprise-level integration, you should get to ask about reserves, banking relationships, and insurance. Major providers like Coinbase publish balance sheets and compliance disclosures. Smaller providers may not, so you need direct questions: segregation of funds, insurance coverage scope, and treatment of in-flight transactions during outages or shutdowns.

Check regulatory history: enforcement actions, restrictions, or fines. Also negotiate SLAs with crypto-specific clauses: performance during volatility, rate accuracy, maximum slippage, settlement timeframes, and contingency plans if banking partners terminate relationships.

Technical diligence should include staging access, load testing, webhook reliability, and incident response transparency. Security certifications (SOC 2 Type II, ISO 27001, PCI DSS), for instance, are strong signals of maturity.

Integration Options for Developers

Developers and builders are the ones that make these checkouts work; it makes sense that they would need a deeper look into the products. Here are a few features that they should also keep in mind when choosing the best on-ramp to integrate.

SDKs and APIs

SDKs and APIs provide granular control. You can shape the flow, handle webhooks, and align UX with your product’s logic. Stripe’s Fiat-to-Crypto toolkit follows familiar endpoints and documentation patterns. Coinbase Commerce focuses on merchant integrations with wallet detection, price conversion, and settlement options.

The upside is scalability and customization; conversely, the downside is ongoing maintenance as APIs evolve and regulations shift.

Widget Embeds

On the opposite side are widget embeds, the fastest “ship it” option. Drop in a snippet, configure branding and asset options, and the provider handles KYC, payments, and execution.

Providers like Onramper offer additional customization via URL parameters, but you’re still bound by the provider’s interface decisions, as a tradeoff. If their widget slows down, your onboarding slows down too.

Wallet Integration

Wallet integration reduces mistakes by detecting existing wallets like MetaMask or Trust Wallet and pre-filling destination addresses. That removes a major friction point and reduces “wrong address” disasters.

Implementation typically uses Web3.js or Ethers.js for browser wallets and deep linking (WalletConnect) for mobile. The key safety rule: never request or store private keys—only public addresses. Also make sure you correctly handle network selection for multi-chain wallets.

No-Code Options

Being the easiest ones, these let even non-technical teams deploy crypto buying flows quickly. MoonPay’s Widget Builder and Transak’s Dashboard provide visual configuration and either widgets or hosted pages.

The trade-offs in this case are flexibility and data ownership. You often get limited analytics, minimal customization, and an external-domain experience that some users distrust.

Webhook and Event Handling

Webhooks turn an onramp into a real system component: transaction initiated, KYC completed, payment confirmed, tokens delivered. Your backend can trigger emails, update balances, fulfill products, and log accounting events.

Always verify webhook signatures, implement idempotency checks, and design state handling for incomplete KYC, declined payments, confirmation delays, and refund flows. A simple state machine prevents users from getting stuck in limbo.

AI-Based Onramp Routing

Credit/source: “AI-enabled routing in next generation networks: A survey” by Fatma Aktas, Ibraheem Shayea, Mustafa Ergen, Bilal Saoud, Abdulsamad Ebrahim Yahya, Aldasheva Laura in Alexandria Engineering Journal, Volume 120, 2025, ISSN 1110-0168, https://doi.org/10.1016/j.aej.2025.01.095.

Onramper’s AI routing dynamically selects the best provider based on location, payment method, crypto asset, and success probability. Instead of maintaining multiple direct integrations, developers integrate Onramper once, and the routing happens behind the scenes.

This helps solve regional availability issues. A single provider rarely covers all countries and rails well. AI routing can surface different optimal options for users in Brazil versus Germany, while keeping your UI consistent.

Integration Examples

Summing up, different product types tend to gravitate toward different approaches:

- A DeFi platform might use the Stripe SDK to create a custom flow where users buy stablecoins and deposit into smart contracts automatically.

- A game might embed an Onramper widget inside an item shop for quick token purchases.

- An education site might link to a MoonPay hosted page after a tutorial (“Buy Your First Bitcoin” with $50 pre-set).

- An NFT marketplace might detect MetaMask, pre-fill addresses, and streamline purchase-to-delivery in a few clicks.

Future Trends (2026 and Beyond)

Having looked at the current state of these services, we can turn to anticipated developments before concluding. All in all, onramps are getting smoother but not because crypto got simpler, because the “plumbing” is improving.

Account Abstraction

This novel feature changes how users interact with wallets. Instead of forcing people to manage private keys and seed phrases from day one, wallets can behave more like fintech apps: social recovery, gas-less transactions, and biometric-style authentication.

Account Abstraction separates signing from execution, enabling smart contract wallets that can batch transactions and reduce costs. For onramps, that means fewer “crypto-specific” hurdles before a first purchase. New users can onboard without learning key management immediately, and providers can aggregate transactions to make micro-purchases viable.

Stablecoin Rails

A highly-anticipated feature, these are becoming the “middle layer” between banking and crypto. Instead of multiple conversions (and multiple points where fees and slippage appear), users can convert fiat once into a stablecoin and use that stablecoin as the base asset for everything else.

Because stablecoin transactions settle continuously on-chain, they can reduce settlement time from days to minutes. Compliance also becomes more auditable when stablecoins are backed by transparent reserves and clear issuance structures. For users, the experience is straightforward: deposit fiat, receive USDC or USDT, then move through the ecosystem with fewer delays.

Fraud Prevention

Fraud evolves fast, and so must safety: biometric liveness checks that detect deepfakes, behavioral analytics that flag anomalies in real time, and blockchain screening that checks whether destination addresses are linked to scams or sanctioned entities.

Data tokenization reduces stolen-card risk by replacing card numbers with merchant-specific tokens. 3D Secure 2.0 adds banking-app confirmations. Better fraud controls reduce chargebacks, which improves relationships with banks and payment processors—a practical win that can translate into better user pricing over time.

Regional Payment Networks

Regional payment rails are shaping adoption by meeting users where they already are, and the expansion can be expected to continue. PIX in Brazil, UPI in India, and regional e-wallets across Southeast Asia can enable instant settlement with minimal fees, far outperforming international wires.

Credit/source: Payment Industry Intelligence Integrating these rails takes real effort (unique APIs, compliance standards, settlement mechanics). But the efficiency gains are huge: near-zero processing costs, instant funding, and a familiar payment experience. When buying crypto feels as normal as paying for groceries in the same app, adoption becomes much easier.

Conclusion

Picking the best crypto onramp is really about balancing four things: total cost, ease of use, security, and geographic coverage. Every platform makes trade-offs, and the “right” answer depends on your situation.

Custodial platforms (centralized exchanges) like Coinbase and Binance still dominate for a reason: they’re straightforward, familiar, and fast once you’re set up. Non-custodial options like Bleap flip the model—more control and fewer custody risks, but also more responsibility on you. Many users end up with a hybrid approach: use custodial rails for convenience and liquidity, then move long-term holdings into self-custody.

Looking forward, the trend is clear: tighter compliance, smoother UX (especially via Account Abstraction), faster settlement through stablecoin rails, and smarter routing across providers. The onramps that win in 2026 will be the ones that make crypto feel normal—without cutting corners on safety.

One last practical rule: compare at least three options, test with small amounts first, and don’t just chase the lowest stated fee. In crypto, the real cost is always the full path—from fiat to wallet, with every spread, hold, and delay included.

Sources Used:

- https://www.alchemy.com/dapps/best/fiat-onramps

- https://www.quicknode.com/builders-guide/best/top-9-fiat-onramps

- https://koinly.io/blog/best-crypto-exchanges-new-york/

- https://coinbureau.com/review/best-crypto-exchanges/

- https://www.bleap.finance/blog/best-crypto-on-ramps

- https://coincub.com/review-of-the-best-crypto-on-and-off-ramp-solutions-in-2025/

Frequently Asked Questions

Which crypto onramp has the lowest total cost?

There isn’t a universal cheapest option because total cost depends on payment method, purchase size, and asset choice. Bleap stands out for transparency, with zero-fee non-custodial purchases and instant settlement, and it’s often competitive when you factor in spreads and delivery time.

The catch is that “zero fees” elsewhere can still mean spreads. Compare the quoted rate against live market pricing (for example, on CoinGecko or CoinMarketCap) at checkout to see what you’re really paying.

Which crypto onramp is best for beginners?

Coinbase remains the default beginner choice because it prioritizes clarity, guided onboarding, and a familiar app experience. Fees are higher, but that premium often buys a smoother learning curve and more predictable support.

If you want similar simplicity with potentially better rates, Ramp Network can be a strong alternative once you’re comfortable with the basics.

Which crypto onramp is best for dApps?

Ramp Network is a common choice for dApps because of its wide blockchain support and strong embedded integration options. It can deliver crypto directly to self-custody wallets, removing extra steps and fees.

MoonPay and Transak are also solid, but Ramp’s breadth across networks often gives it an edge for newer ecosystems—just confirm your target chain is supported before you commit.

Which payment method is cheapest?

Bank transfers (ACH in the US, SEPA in Europe) are typically the cheapest (often 0%–1%), but they’re slower (1–5 business days). Cards are fast but expensive (3%–5%). E-wallets sit in the middle.

If you’re buying regularly, recurring bank transfers can reduce your average cost substantially over time.

What is the difference between custodial and non-custodial onramps?

Custodial onramps hold your crypto in accounts they control until you withdraw. This is convenient (recovery options, support, quick trades) but introduces counterparty risk.

Non-custodial onramps deliver crypto directly to your wallet, where you control the private keys from the moment of purchase. Bleap is an example. You get sovereignty, but you also carry the responsibility—lose your seed phrase, and there’s no recovery line.

Can you buy crypto without KYC?

Yes, but options are limited and usually capped at small amounts. No-KYC routes often come with higher fees, lower reliability, and higher fraud exposure. Most onramps serving US or EU customers require KYC for anything above nominal thresholds due to AML obligations.

If privacy is essential, use extra caution: reputation checks, small test transactions, and a clear understanding of the platform’s legal and operational risk.

How do you verify an onramp’s reputation?

Look for incident history (security breaches, regulatory actions) and consistent user reports about support quality during failures (stuck transactions, verification issues, withdrawal delays). Check regulatory status where possible, and treat “too perfect” review patterns as suspicious.

A platform’s credibility shows up in how it handles problems, not how it markets itself.

Are “free” crypto onramps real?

They can be “fee-free” on paper, but rarely free in practice. Many earn through spreads (a worse effective exchange rate). Promotions may also be time-limited or restricted by asset and payment method.

Bleap’s zero-fee approach for non-custodial transactions is positioned as a transparent alternative. Either way, the best test is simple: compare the checkout quote against a live market rate to see your real cost.