Best Bitcoin & Crypto Escrow Services

Key Takeaways

- 🔏 Escrow usually implies a financial arrangement when a third party keeps a payment in custody unless both parties complete their side of the transaction. Crypto escrow is no different, only pertaining to digital currencies like Bitcoin or Ethereum;

- 🔏 Usually, escrow requires a trusted setup but thanks to some features of blockchain, in crypto the degree of trust in a middleman can be reduced. For example, the sender and receiver can use a multi-signature wallet or the escrow can be managed by a smart contract;

- 🔏 Therefore, there are multiple types of crypto escrow services depending on the setup and purposes. There are not a lot of legitimate and proven services or agents active as of 2026, making the process of choosing one more difficult.

Crypto escrow services protect crypto transactions by holding funds in neutral custody until both sides meet the agreed conditions. In 2026, that matters more than ever because crypto deals are no longer limited to “swap token A for token B and hope for the best.” People buy NFTs, pay remote contractors, settle OTC trades, and even close high-value peer-to-peer sales where one wrong click can send funds into the void (and the blockchain will happily confirm your mistake).

Crypto escrow services increasingly act as a bridge between traditional expectations (clear terms, conditional payments, dispute resolution) and digital rails (wallet-to-wallet transfers, smart contracts, stablecoins). For newcomers, it is the tipping point to the realization it can be a normal way to do business, albeit with different tools and a stronger need for basic safety habits. If you’ve ever wished crypto transactions came with training wheels, escrow is pretty close, essential when real money and real trust are on the line.

Crypto Escrow Basics

Definition

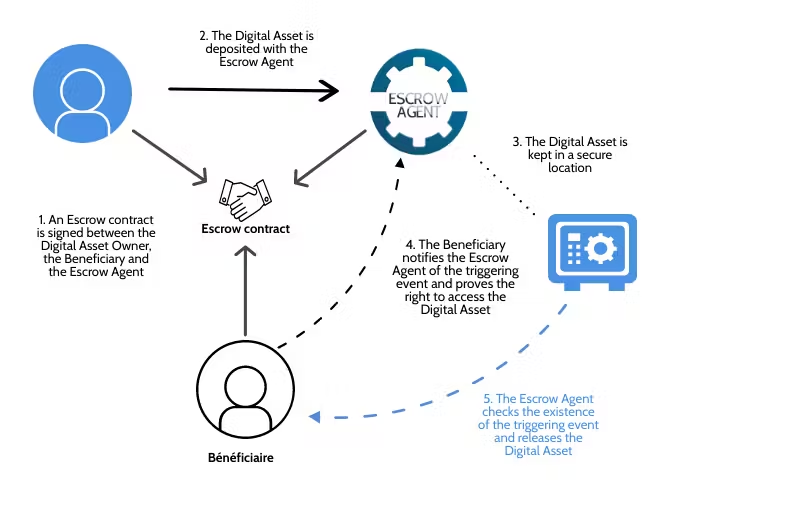

Crypto escrow protects buyers and sellers by holding funds in an escrow account (or an escrow smart contract) until pre-agreed conditions are met. The escrow transaction reduces counterparty risk by making the release of crypto conditional instead of purely trust-based.

This service becomes the “middle layer” both parties agree on rather than have no other choice but to use. Instead of sending crypto directly to a seller and hoping everything goes well, the buyer locks funds into escrow first. That lock can be managed by a human escrow agent (custodial escrow) or by code (non-custodial escrow via an escrow smart contract). Both aim at the same core purpose: enforce the deal rules and prevent the classic crypto nightmare of “sent funds, got nothing.”

Source: Napkin Finance

Because crypto transfers are typically irreversible, escrow becomes a safety rail. If a dispute happens, escrow provides a defined path to resolution. There’s also a practical clarity benefit. A proper escrow transaction forces both sides to define deliverables and timing: what counts as “delivered,” what counts as “accepted,” and what evidence is valid.

How Crypto Escrow Works

A crypto escrow lifecycle usually follows a predictable flow: initiation, execution, and closure. The order matters because each step adds a security checkpoint, and skipping one tends to be where things get messy.

- Initiation (deal setup and funding)

The buyer and seller agree on terms: price, asset, deadlines, acceptance criteria, and what happens if something fails. Then the buyer deposits funds into an escrow account or locks them into an escrow smart contract. This funding step is the first trust signal: the buyer proves they can pay, but the seller still can’t run off with the money. - Execution (delivery and verification)

The seller delivers the agreed item or service. Depending on the deal, “delivery” might be a digital good, access, a physical shipment with tracking, or completion of milestones. Escrow works best when verification is measurable: a clear checklist (tracking marked delivered, files received, milestones signed off) reduces disputes before they start. - Acceptance (release trigger)

Once the buyer confirms the conditions are met, the release is triggered. In a smart-contract setup, this can be an on-chain action. With a human escrow agent, release is an administrative action after reviewing the evidence and approvals. - Closure (payout, refunds, or dispute path)

If everything checks out, escrow releases funds to the seller and the transaction closes. If conditions are not met, escrow can route to a refund, partial refund, or dispute resolution process, depending on the agreed rules. This is why the upfront terms matter: escrow can only enforce what you define.

Key Roles and Responsibilities

Crypto escrow looks simple on the surface—money in, money out—but the roles are what keep it fair. Each participant has a job, and the whole structure collapses if one role is fuzzy or overloaded.

Buyer (payer / depositor)

The buyer funds the escrow account or smart contract and defines what counts as successful delivery. Their responsibility is to be specific and timely: approve release when conditions are met, and raise issues with evidence when they are not.

Seller (provider / recipient)

The seller delivers the product, service, or asset according to the terms and provides proof. That proof can be as simple as a delivery receipt or as structured as milestone documentation.

Escrow agent (trusted third party) — in custodial setups

A human escrow agent holds and administers the escrow account, confirms funding, coordinates the release, and manages disputes by evaluating the provided evidence. The agent’s biggest value is process discipline: they keep both sides within the rule scope when emotions or opportunism kick in. The flip side is trust: you are trusting the escrow agent to act honestly and secure the funds properly.

Source: Vaultinum

Escrow smart contract (automated escrow) — in non-custodial setups

A smart contract can replace the human middle layer with programmable conditions. It can enforce releases, refunds, multi-signature approvals, or timeouts without relying on one person’s judgment. The benefit is transparency and predictability; the risk is that code follows rules exactly, even when real life is messy. That’s why the “write good terms” job still falls on the humans.

Types of Crypto Escrow Services

Custodial Escrow

These services hold crypto funds in a third-party account until an escrow agreement is completed. Think of this as handing the keys to a trusted concierge: the escrow provider takes temporary control of the assets so neither side can “run” with the money mid-negotiation.

If something goes sideways—wrong item, late delivery, mismatched on-chain amount—the custodial agent can pause the release and follow a dispute process. That human-in-the-loop element is the whole point in this arrangement.

The custodial agent’s responsibilities go beyond “just holding coins.” A good escrow provider will confirm deposits on the blockchain, enforce timelines, verify basic evidence (receipts, tracking, signed messages), and maintain clear communication so both parties can move toward a secure deal. For higher stakes, they may also help with identity checks and fraud screening.

Benefits are obvious: less technical work for the user, fewer ways to misconfigure a transaction, and a clear mediator if the escrow agreement gets contested. On the other hand, it introduces custody risk—your funds sit under someone else’s control. If the provider is hacked, mismanages keys, freezes withdrawals, or simply disappears, your “protected” funds become stuck.

Fees are also part of the tradeoff. Custodial escrow commonly charges a service fee, percentage or flat, and you still pay network fees on the blockchain.

Multisig Escrow

This type of escrow uses multisignature wallets to require multiple approvals before funds move. Instead of trusting one middleman, the escrow agreement is enforced by keys—usually a 2-of-3 setup where the buyer, seller, and an escrow provider each hold one key, and any two can authorize the release.

Mechanically, funds are deposited into a multisig address on the blockchain. No single party can unilaterally sweep the balance. If everything is fine, buyer and seller co-sign to release the funds to the seller. If there’s a dispute, the escrow provider reviews evidence and co-signs with the party that matches the terms.

Source: Bitcoin Magazine

Why does this add an extra layer of security? Because it reduces single points of failure. A hacked escrow provider can’t steal funds alone. A scammy buyer can’t claw money back alone. Even the seller can’t “front-run” the release. The trust problem becomes a coordination problem, which is easier to audit.

Multisig escrow shows up a lot in high-value transactions: OTC crypto trades, large P2P crypto transactions, business-to-business settlements, and acquisitions where both sides need time to verify conditions.

Of course, it’s not magic. Multisig still requires operational discipline: safe key storage, clear signing procedures, and a plan for lost keys. Fees can also include setup/service charges, plus standard network fees for creating and spending from multisig. Still, if your top priority is a secure deal without giving one party full control, multisig is one of the cleanest compromises.

Smart Contract Escrow

Smart contract locks funds in a self-executing program on a blockchain and releases them when predefined conditions are met. The escrow agreement becomes code: once the rules are deployed, the contract follows them without needing a human provider to “push the button.”

Conditions such as time locks (release after a deadline), proof-of-payment logic, or oracle-based events to release when an external signal confirms delivery, are predetermined by whoever writes the code. When the conditions are satisfied, the contract automatically transfers the funds. When they aren’t, it can refund, extend, or route the situation into an on-chain dispute flow—depending on how it was designed.

Automation changes who you must trust. Instead of trusting a company to custody funds, you trust the contract logic and the blockchain execution. That can be a big upgrade for transparency, because anyone can verify what the contract will do and when before depositing funds. For many users, that predictability is the real comfort, especially when the goal is a trustless transaction where enforcement comes from the protocol rules rather than someone’s discretion.

Examples of smart-contract-based escrow patterns are common in DeFi and NFT marketplaces: bids held in escrow until acceptance, collateral locked until repayment, or milestone payments released per on-chain confirmations. Some platforms also offer “conditional payment” tools where funds move only if a contract state flips from pending to fulfilled.

There is a serious caveat, though. Smart contracts can have bugs, bad assumptions, or weak oracle dependencies, and code is not forgiving. If the escrow agreement is encoded incorrectly, the contract can lock funds, release them too early, or behave in unexpected ways—and in this arrangement, no “customer support” would be able to reverse it. So the best use case is when the conditions can be clearly defined and verified in a way the blockchain can reliably enforce.

P2P Marketplace Escrow

Source: Accubits

On any P2P marketplace, the escrow service is a valuable feature to facilitate user-to-user trades by holding crypto during the exchange and releasing it when payment is confirmed. The marketplace acts as the escrow provider, but the transaction itself is decentralized in spirit: two users pick terms directly, and the platform provides guardrails so the deal doesn’t turn into a trust fall with no spotter.

The process usually looks like this: a seller posts an offer, a buyer accepts, and the marketplace locks the seller’s crypto in escrow for the duration of the trade. The buyer then pays using an agreed payment method, and once the seller confirms receipt, the platform releases the crypto. If there’s a dispute, the marketplace steps in as an arbiter.

Here’s why this model is popular: it bridges real-world payment rails with blockchain settlement. You can pay via bank transfer, e-wallets, or local methods, while the crypto side stays locked until the escrow agreement’s conditions are met. That makes a secure deal much more achievable for everyday users who don’t want to wire money into the void.

P2P escrow still inherits real-world risks: payment reversals, fake confirmations, and region-specific fraud patterns. Following the platform rules to the letter is an insurance: use the correct payment reference, keep communication inside the platform, and don’t release escrow early.

Top Crypto Escrow Services in 2026

Guaranty Escrow

Guaranty Escrow specializes in escrow for real estate and large-asset transactions where the paperwork is as important as the payment. Unlike other popular escrow providers not focused on crypto, they provide Bitcoin escrow services for high-value deals with digital currencies.

Their service is based in California, USA, and offers a fully-compliant and highly-secure Bitcoin escrow service. Both using BTC as payment or by itself in a deal are fair game. Multi-sig escrow is supported, and so is optional conversion to fiat. In addition to Bitcoin, they accept popular altcoins: ETH, SOL, XRP, and Tether USD.

If you’re used to P2P crypto marketplaces, using a more traditional provider can feel slower—and it often is. But for things like real estate, “slow and correct” beats “fast and reversible,” because most mistakes are not easily undone after the transaction closes.

Binance P2P

Binance P2P enables P2P crypto trading with escrow protection that keeps the crypto locked until the payment step is confirmed. Typically, the seller’s crypto is reserved in platform custody while the buyer sends payment using the agreed method. Once the seller confirms receipt, Binance releases the crypto. If something gets weird, the dispute process can kick in with platform mediation.

For 2026 users, the big advantage is speed and liquidity. You can move from “I need USDT” to “I have USDT” quickly, and escrow protection is built into the flow rather than bolted on. It’s particularly useful for smaller-to-mid sized cryptocurrency deal sizes where you care about frictionless execution.

Typical flow of a P2P trade on a centralized exchange (CEX) such as Binance.

The downside is that you’re relying on platform rules and platform judgment. The escrow manager role is effectively the exchange’s support and dispute team, and the final outcome depends on evidence: payment receipts, timestamps, chat logs. That means your best defense is operational: use the exact payment method agreed in the order, avoid off-platform communication, and keep records.

Bitrated

Most crypto escrow services essentially replicate the traditional escrow but not Bitrated. In fact, the platform does not provide escrow services, according to their own words. In turn, Bitrated provides a decentralized alternative built around a multisig wallet structure, which is a very different flavor of escrow service compared to platform custody. Instead of handing funds to a company to hold, you use a multi-signature setup (commonly 2-of-3) where the buyer, seller, and a third party (the arbitrator) each control a key. Funds move only when enough signatures signal approval.

If everything goes smoothly, buyer and seller sign and release without ever involving the third key. If there’s a dispute, the arbitrator becomes the tie-breaker. That role is basically the escrow manager equivalent in a decentralized context—less “company policy,” more “trusted third key-holder,” and effectively a guarantor for the process rather than for either side.

In 2026, this is especially appealing for cryptocurrency deal types where platform risk is a concern. You might not want to rely on a centralized escrow account at all, and you might prefer something closer to an escrow smart contract without needing to deploy custom code. Multisig is a middle ground: transparent rules, no single point of control, and a dispute path that doesn’t require a corporate support ticket.

As is often the case with the initiatives like Bitrated, the user experience is far from their centralized or traditional counterparts; it is not an escrow account since party collusion can happen, and all you have against this is their proprietary trust score; only Bitcoin is supported; and last but not least, you would be lucky to find users still actively using it in 2026.

Propy

Propy is also different from traditional escrow services but in a different way: it targets blockchain real estate transactions by combining property workflows with title-related services. The platform is a partner of Coinbase and has its own native token PRO. In addition to blockchain, they claim to leverage AI in their services, too.

As was the case with Guaranty Escrow, Propy can extend their service only to users in the US. Since their platform uses Ethereum to record deeds and issue the PRO token, using other digital assets may require off-chain methods.

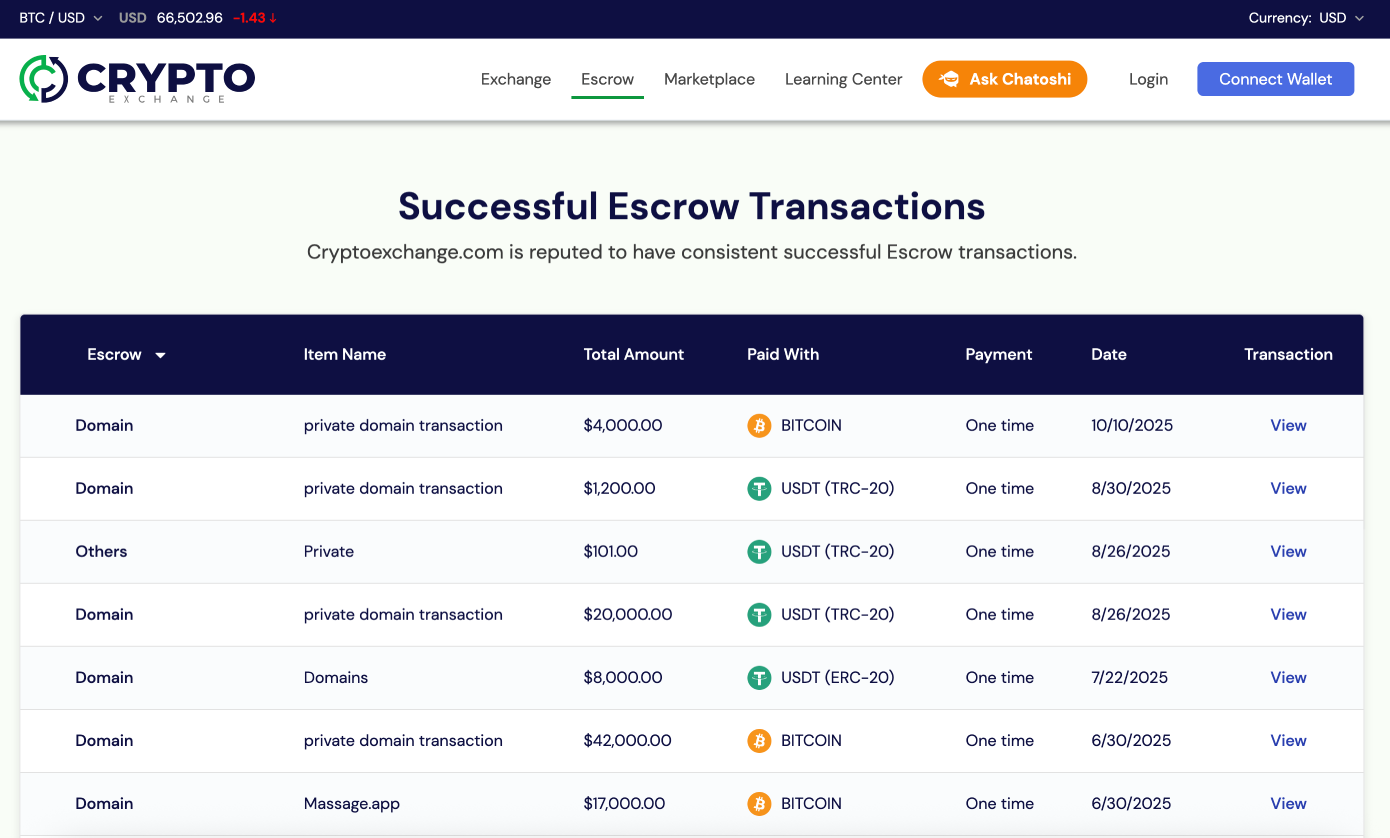

CryptoExchange Escrow

Source: Cryptoexchange.com

If it’s not real estate that you need crypto escrow service for and rather, a more simple deal, such as buying a domain name, consider yourself lucky. CryptoExchange runs a custodial crypto escrow service that can fit any bill, as long as it is only digital assets going into the “account”.

In the world of crypto escrow services increasingly relegated to exchanges (like Binance P2P), CryptoExchange’s escrow platform is one of the few remaining true and blue services like that. The process is exactly as we described prior, with three participants and an agreement process that can take 5 to 20 days. A major drawback is its geographical limitations: sure, it is not US-only, but outside of English-speaking countries and most but not all of Europe, its services may be completely unavailable.

Community Options

Last but not least, an honorary mention to individual escrow service providers that you can find on forums like BitcoinTalk or Reddit. When your options in terms of licensed providers are not as extensive as, for example, for a user in the US or EU, you might want to search community-curated lists of individual users…and hope for the best. Sure, very often people offer to serve as an intermediary for negligible pay or free of charge, and the idea of the third party being your peer instead of a corporate middleman might appeal to some, but the risks are that much higher.

Platforms like Bitrated aimed to reduce misplaced trust assumptions with their original methods; on forums and curated lists and directories, the reputation system is just word of mouth. The final bit of warning is that crypto escrow is a dying art, and just like many, many companies that used to offer the service are no longer functional, individual users may no longer be providing any help with transactions.

How to Choose a Crypto Escrow Platform

Even when your options are limited, in this particular case, there is still a choice. If the providers highlighted above for one reason or another do not fit your needs, let’s recap the criteria we used to help you choose the suitable crypto escrow service.

Security Model

Anyone would want a service so crucial as crypto escrow to be as secure as possible. Security profiles vary between custodial models with agents, P2P escrows run by a centralized exchange, or multisig alternatives.

If a platform uses cold storage for client funds, the chance of an online breach is smaller. However, it protects the funds only from online threats and does not eliminate trust assumptions.

Consider the track record. A provider can market “bank-grade security” all day, but you want to see consistent operational maturity: clean incident history (or at least transparent post-mortems), sensible withdrawal controls, and policies that don’t change overnight. If the escrow is embedded into a cryptocurrency exchange, treat it like exchange risk plus escrow risk.

If there is an escrow smart contract involved, deterministic clear rules are a must. Moreover, smart contracts need audits, and the user needs to understand what the code actually enforces (timeouts, admin keys, upgradeability).

Dispute Resolution and Arbitration

Photo by Cytonn Photography on Unsplash

A good escrow service doesn’t just offer a chat box; it has a defined dispute process, clear evidence standards, and a real arbitration path when the parties disagree.

Success rates are often hard to verify. If a provider publishes dispute statistics, that’s a good sign of process maturity. Another question worth asking is how disputes interact with release controls. With an escrow smart contract, disputes may be handled by predefined time locks and escrow states (release/refund/partial release), but some systems still rely on an admin key or a designated arbitrator address.

Supported Assets and Networks

Cryptocurrency list and the network list are also a major criterion for finding that perfect crypto escrow arrangement. Many services claim to support “USDT,” but what they really support is one chain’s version. The same goes for stablecoins, wrapped assets, and L2 networks. If your counterpart uses a different chain, you might end up doing an extra swap, and every swap can introduce slippage, price movement, and another escrow fee-like cost in the form of conversion spreads.

Payment rails matter too, especially for P2P escrow tied to fiat. Often, it’s settled without the provider's participation in the deal’s conditions but having clear labels for your payment methods streamlines the process and saves every party headaches.

Limits and Deal Size

Crypto escrow limits decide who the service is built for: casual trades, professional OTC, or enterprise-sized transfers. Most platforms enforce minimums to prevent spam and maximums to manage risk, compliance exposure, and operational load, and those caps can change depending on verification level.

The “how” is usually policy-based. A cryptocurrency exchange with escrow may set deal size limits by account tier, trading history, or KYC status. Independent escrow providers may introduce limits by asset volatility, network congestion risk, or liquidity if they’re handling conversions.

Limits affect your leverage during negotiation. If you’re buying something expensive and the platform caps escrow per deal, you might be tempted to split into multiple escrows. That can work, but it also multiplies complexity: more releases, more deadlines, more chances for one side to claim partial non-performance.

Small users should also care. If the minimum escrow is high, you might overfund a deal “just to qualify,” which is the opposite of risk management. Conversely, micro-deals can be eaten alive by fixed charges; what looks like a tiny escrow fee in absolute terms can be huge as a percentage.

Geographic Availability

Crypto escrow geographic availability decides whether you can even open the door. Services restrict countries for regulatory reasons, banking limitations, sanctions compliance, or local licensing requirements—and the rules are rarely uniform across providers.

Start with two questions: can you use the service in your country, and can your counterparty use it in theirs? Escrow is a two-person handshake; if one side is blocked, the deal is dead or forced into risky alternatives. Some platforms allow browsing but restrict deposits, withdrawals, or dispute handling (which is the worst time to discover a limitation).

A cryptocurrency exchange might support trading globally but limit P2P escrow, fiat rails, or specific payment methods by region.

Also consider time zones and language support as “soft geography.” If your escrow provider’s dispute team operates in limited hours, a fast-moving dispute can turn into a 48-hour silence—long enough for a counterparty to panic, accuse, or escalate.

Fees and Total Cost

Crypto escrow fees determine whether the service is just safe or safe and sensible. Pricing often looks simple at first (a flat fee or a percentage), but total cost is usually a bundle: network fees, conversion spreads, withdrawal charges, and sometimes premium fees for faster support or arbitration.

Start by identifying the base escrow fee model:

- Flat fee: predictable for large deals, painful for small ones.

- Percentage-based: scalable for small deals, potentially expensive for large ones.

- Tiered pricing: better alignment, but you must read the thresholds carefully.

Then hunt for hidden costs. If the escrow requires converting assets (say, you deposit BTC but the counterparty wants USDT), the spread can be the real fee. The same goes for forced network choices: using a congested chain can add meaningful transaction costs, especially if multiple on-chain actions are required (deposit, lock, release, refund).

If the escrow is part of a cryptocurrency exchange, remember that your “total cost” may include exchange withdrawal fees and internal transfer policies. And if a dispute escalates to arbitration, check whether arbitration is included, optional, or charged separately—and whether the fee is refundable depending on outcome.

Customer Support and Responsiveness

Crypto escrow customer support determines how survivable your worst-case scenario is. When a deal goes smoothly, you might never speak to a human but when a dispute hits, response time and competence suddenly become part of the product—especially if you need technical support that can interpret transaction hashes, confirmation counts, and escrow states instead of defaulting to generic scripts.

Clear support channels (ticket + live chat, not just email), stated response-time targets, and dedicated dispute teams rather than general “account support” are all winning features. If the platform offers arbitration, ask how support hands off to the arbitrators and how evidence is collected (structured forms beat free-text chaos).

Transparency and Auditability

Crypto escrow transparency and auditability reduce the “trust me” factor. On top of evaluating whether the platform is honest, you’re evaluating whether you can verify what it claims to do when funds are locked and emotions are high.

Start with operational transparency. Does the provider clearly explain how escrow release works, who can trigger releases, what happens during a dispute, and how arbitration decisions are enforced? Vague language like “we may” and “at our discretion” is a red flag, because discretion is exactly what people argue about in escrow disputes.

Auditability matters on two layers. For smart-contract-based escrow, you want code visibility and independent review (audits), plus clarity on upgradeability and admin permissions. For custodial models (often tied to a cryptocurrency exchange), “proof” is operational: security reports, risk controls, and—when applicable—proof-of-reserves style disclosures. Proof-of-reserves doesn’t automatically cover escrow liabilities, but it signals a willingness to be measured rather than simply believed.

In 2026, the safest choice is usually the most inspectable one. If you can’t tell how funds are held, how disputes are decided, and what you’re paying in total, you’re not choosing an escrow service—you’re choosing a leap of faith.

Legality, Compliance, and Key Considerations

Licensing and Registration

Crypto escrow services require licensing because a manager often holds or controls client funds (even briefly) in an escrow account, which regulators treat as a financial services activity.

In the United States, the big category to understand is money transmission. If your crypto escrow receives value from one party and passes it to another or can otherwise control that transfer, many states may view it as money transmitter activity. That typically means state-by-state registration and bonding requirements, plus operating as a regulated Money Services Business (MSB) posture in practice (policies, oversight, audits). In many cases, this is effectively a money transmitter license question at the state level, alongside related federal MSB expectations. “We don’t touch fiat” is not a magic shield—control over crypto flows can still trigger licensing analysis.

In the European Union, licensing tends to cluster around whether you are providing regulated crypto-asset services and whether you are safeguarding client assets. If the escrow model looks like custody (holding keys, executing releases, controlling smart-contract admin keys), regulators may expect a formal authorization framework and controls similar to what a financial institution would run: governance, risk management, and documented compliance procedures. Depending on the structure, this can look like needing a financial services license or registration under applicable crypto-asset services rules. The more discretion an escrow manager has, the more you drift from “software tool” into “regulated service.”

In Singapore, the compliance conversation often revolves around whether the service constitutes a regulated payment service or digital payment token-related activity. A crypto escrow that facilitates transfers, holds customer assets, or provides arrangements for settlement may face licensing/registration expectations and ongoing obligations, including financial services license-style oversight and controls when the activity resembles regulated financial services.

KYC and AML Requirements

KYC and AML compliance keeps crypto escrow services from becoming the world’s easiest laundering pipeline, and regulators expect it even when the product feels like a neutral “hold-and-release” tool.

KYC (Know Your Customer) typically starts with identity verification. For individuals, that often means collecting legal name, date of birth, address, and government ID, plus liveness checks or document validation depending on jurisdiction and risk level.

AML (Anti-Money Laundering) is the ongoing part, and it’s where many services stumble. A solid AML program is not just a checkbox policy; it includes risk scoring, transaction monitoring, case management, and clear escalation paths. Transaction monitoring often looks for patterns like rapid in-and-out movements, structuring (splitting a large amount into many smaller transfers), repeated disputes that end in “release anyway,” or activity that doesn’t match the user profile. AML is behavioral: a clean passport photo doesn’t make a suspicious flow suddenly “fine.”

Tax and Recordkeeping Considerations

Photo by Jess Bailey on Unsplash

Escrow activity creates a paper trail of value moving, even when the service isn’t the party “earning” the crypto. Different jurisdictions treat crypto taxes differently, but they tend to agree on one thing: if you can’t prove what happened, you don’t get the benefit of the doubt.

For users, escrow records can be critical for determining acquisition/disposal events, cost basis tracking, and whether an exchange of one asset for another occurred as part of settlement.

A practical tip is to keep records in a format that supports reconciliation. That way, if you ever need to explain why 2.3 ETH moved on a specific date, you can point to one bundle of evidence instead of ten half-matching screenshots.

Regulatory Red Flags and Warning Signs

Non-compliant crypto escrow services tend to broadcast warning signs if you know what to look for, and spotting them early can save you from frozen funds and messy disputes. Escrow is built on trust, but regulators expect trust to be verifiable—through disclosures, controls, and accountability.

A major red flag is lack of transparency about who controls the escrow account and how releases happen. Another warning sign is vague legal language like “not a financial service” paired with features that look exactly like a financial service—holding funds, mediating disputes, and charging a fee for releases.

Pricing can also signal trouble. Unusually high transaction fees, especially fees that change mid-deal or are only revealed at release time, can indicate poor governance or predatory behavior.

Crypto escrow services reduce counterparty risk in one way but introduce custody, technical, and compliance risks that can hit your funds when you least expect it.

Insolvency Risk

Speaking of custody, a custodial escrow account can trap funds when the provider becomes insolvent, and your “protected” money may suddenly become part of a bankruptcy process rather than a simple release button.

Counterparty responsibilities can also get blurry fast. During an insolvency event, the buyer might argue the funds should be returned, while the seller might argue performance already happened and the release is owed. The escrow manager (or their administrator) may freeze everything “until it’s sorted,” and sorting can take months.

Smart Contract Risk (Bugs and Exploits)

Smart contract escrow is not automatically better. It replaces the custody risk with code risk. If the escrow logic lives on-chain, a bug can release funds to the wrong party, lock them permanently, or allow an attacker to drain the escrow account.

Escrow contracts often include time locks, dispute windows, and conditional releases. Each feature increases the attack surface. Add upgradeable contracts (admin keys), and you now have both code risk and key-management risk in the same escrow agreement.

Dispute Resolution Limitations

Crypto escrow can fail at the exact moment you need judgment, because many systems are bad at handling gray areas. Common dispute scenarios are rarely binary. “Item not received” can actually mean “received but damaged”; “digital goods” can mean “the key worked once, then was revoked.”

In traditional escrow, you might rely on contracts, invoices, inspection reports, and a human escrow manager who can ask follow-up questions. In crypto escrow, resolution is often limited to a predefined on-chain condition (which are famously binary), a basic chat log review, or an internal support decision with limited appeal.

If the platform’s “arbitration” is just customer support, the disputer can be stuck in a loop: submit proof, wait, get a template reply, repeat.

Limited resolution mechanisms can escalate losses. While the dispute drags on, the seller may lose inventory value, the buyer may miss deadlines, and both can lose to volatility. Escrow helps with trust, but it doesn’t automatically create a fair court.

Frozen Funds, Holds, and Compliance Lockouts

Compliance controls can freeze escrow funds even when nobody is “scamming.” If a platform runs KYC/AML checks, screens addresses, or responds to law enforcement requests, it can place holds on an escrow account and stop releases mid-deal.

Building on that, compliance lockouts can also happen from simple operational triggers: logging in from a new country, using a flagged bank card for on-ramp/off-ramp, receiving funds from a wallet that previously interacted with a sanctioned address, or a court order or regulator notice requiring a temporary freeze.

Privacy Tradeoffs and Data Retention

In a custodial setup, the escrow manager may collect KYC documents, store chat logs, retain device/IP history, and keep transaction metadata tied to your identity. That retention can help if a disputer files a chargeback-style complaint or if the provider needs to justify a freeze. On the other hand, it creates a data footprint that can be breached, requested by authorities, or shared with vendors; this is a common posture for large custodial escrow-style marketplaces and exchange-run escrow services where compliance programs drive recordkeeping.

In “decentralized” variations and smart contract escrow, the opposite happens: you may avoid handing over identity documents, but the escrow agreement itself can be transparent on-chain. Amounts, timestamps, counterparties, and dispute events can be visible, linkable, and analyzable; this is more common in DeFi-style escrow tooling where the escrow account is a contract address and transparency is the default.

Common Issues and How to Handle Them

Deal Cancellation

Escrow cancellation protects funds by freezing the transaction state and forcing a clean, documented exit from the escrow process. The goal is simple: stop delivery, stop payment, and stop misunderstandings, all in a way the platform can verify later if a dispute appears.

Start with communication: send a written cancellation request inside the escrow chat/thread, reference the transaction ID, and state exactly what you want: “Cancel and revert to original funding wallets/accounts.” Avoid side DMs, because support teams typically treat the on-platform log as the source of truth.

Photo by Markus Winkler on Unsplash

Then follow these steps for a safe cancellation:

- Confirm current status: funded but not released, released, in delivery, or in dispute. Cancellation is usually only straightforward before release.

- Request explicit acknowledgement: ask the other party to reply “I agree to cancel” in the same thread. Screenshots help, but native chat logs help more.

- Pause real-world actions: if any delivery is involved, halt shipment or schedule a carrier intercept (if possible) before you hit cancel.

- Ask about fees and timeframes: some services charge cancellation fees or apply time windows (for example, “cancellation only within X hours of funding”). If the platform doesn’t show it clearly, get the policy in writing from support.

Never “cancel” by moving the conversation off-platform and doing a separate refund manually. That’s how people accidentally create two parallel transactions (one in escrow, one outside) and end up paying twice. If you need to unwind the deal, unwind it inside the escrow process, with a single timeline and a single record.

If the other party refuses to cancel, don’t negotiate in circles: this is what the third party is there for. Trigger the dispute flow with a calm summary: what was agreed, what changed, and what outcome you’re requesting. The earlier you formalize the cancellation, the less likely you’ll get hit with last-minute delivery claims or partial-performance arguments.

Counterparty Disappearance

If your counterparty stops returning the calls, it breaks the escrow process by removing the one thing you can’t automate: cooperation. People ghost for all kinds of reasons—time zones, buyer’s remorse, KYC fear, or plain bad behavior—so your response should assume nothing and document everything.

First, try reconnection in a structured way:

- Send a reminder (ping) inside the transaction thread with a clear ask and a deadline (e.g., “Please confirm shipment details within 24 hours or I’ll open a dispute”).

- Use the platform’s notification tools if they exist.

- Keep messages factual and short: what step is pending, what proof you need, what happens next.

On the other hand, don’t spam across five channels. Too many messages can look like harassment and can complicate moderation decisions later. One on-platform message + one follow-up is usually enough before escalation.

If there’s no response, escalate fast and clean:

- Open a dispute (or a “non-responsive counterparty” ticket) and include the transaction timeline in bullet points.

- Attach evidence that you performed your side of the deal (payment receipt, address confirmation, delivery booking, or whatever applies).

- Ask support to enforce time-based rules: many escrow systems have auto-cancel or auto-refund logic when a party doesn’t act within a defined window. If it’s not automatic, request it explicitly.

Wrong Delivery or Non-Delivery

Handling these issues starts with verification because most shipping chaos is really data chaos. A missed digit in an address can look like fraud, and fraud can hide behind “carrier issues,” so you want a repeatable investigation flow that the escrow process can audit.

Image by freepik

Before you report anything, double-check the basics:

- Re-check the delivery details recorded in the deal: recipient name, full address, postal code, phone number (if used), and any special instructions.

- Validate the tracking link (carrier domain, tracking number length/format, latest scan events).

- Compare timestamps: when the sender claims it shipped vs when the carrier first scanned it.

If delivery is marked “delivered” but you didn’t receive it, treat it like a three-branch problem:

- Wrong address / reroute (often shows as “delivered to mailbox” or “left with neighbor”),

- Carrier mis-scan (status says delivered, but the GPS scan doesn’t match),

- Fraudulent tracking (tracking exists, but for a different parcel/region).

Report discrepancies inside the platform immediately, with a tight evidence bundle:

- screenshots of the tracking page,

- any carrier confirmation emails,

- photos of your mailbox/door area (time-stamped if possible),

- and a short written statement of non-receipt.

Then initiate a real investigation, not just a complaint. Contact the carrier and request a proof-of-delivery record (often includes a scan location or signature). If the sender is legitimate, they should also be able to file a sender-side claim; ask them to do it and to share the claim reference number in the transaction thread.

Do not approve the release “to be nice” while the package status is unclear! Escrow exists to keep leverage balanced. Once funds are released, your dispute usually changes from “hold and investigate” to “try to recover,” and that’s a much less fun game.

Chargeback Risk

Chargeback risk grows when a fiat transaction can be reversed after crypto is released, and that mismatch can wreck an otherwise clean transaction. Cards and some bank transfer rails can be recalled or disputed, while crypto transfers are typically final—so you need to design the deal to avoid “reversible-in, irreversible-out.”

Pre-deal precautions do most of the heavy lifting:

- Prefer irreversible fiat methods when possible (or at least methods with clearer settlement finality).

- Match identities: payer name should match the escrow user name where feasible, and any mismatch should be explained in writing before funds move.

- Define a settlement buffer: don’t release crypto the moment the fiat shows “pending.” Wait for the status that indicates funds are actually settled, not just authorized.

- Require proof that survives a dispute: invoice, written agreement, delivery confirmation for goods/services, and a clear description of what the fiat payment is for.

Avoid “friends and family” style payments or vague memos. A clean paper trail (even a simple invoice + acceptance message in the platform thread) makes it much harder for someone to claim unauthorized or “item not received.”

If a chargeback threat appears mid-transaction, pause and document:

- freeze release inside the escrow process,

- ask the payer to confirm (in writing) that they will not dispute,

- and move the conversation to support immediately with the timeline and payment proofs.

Post-issue remedies depend on where you are in the transaction. If crypto hasn’t been released, your best remedy is to keep escrow locked until fiat settlement is confirmed or the deal is canceled. If crypto has been released and a chargeback hits, your priority becomes evidence compilation for the payment provider’s dispute flow (invoice, delivery proof, chat logs) and platform support escalation to flag the counterparty for abuse.

Frozen Accounts and Compliance Reviews

Compliance reviews freeze accounts to verify identity, source of funds, or transaction patterns that look risky, and that can stall an escrow process even when you did nothing “wrong.” The good news is that most freezes are paperwork problems, not permanent losses.

Common triggers are predictable from general experience:

- large or unusual transaction size compared to your history,

- rapid in/out movement (especially through multiple wallets),

- mismatched names between funding source and account,

- or counterparties flagged for suspicious behavior.

When a freeze happens, your first move is to stop making it worse. Don’t open new accounts to “work around it,” don’t spam support, and don’t attempt to reroute funds mid-review. Instead, ask support for the exact scope: what is frozen (withdrawals, deposits, trading), what documents are required, and what the review timeline looks like.

Prepare a clean documentation package (and keep it consistent):

- Identity documents requested by the platform (and make sure they’re current).

- Proof of address if needed, recent and readable.

- Source of funds / source of wealth explanations: bank statements, payslips, invoices, tax documents, or sale agreements—whatever truthfully matches your situation.

- Transaction context: a short written note explaining what the transaction is for and how it fits the escrow process (who you’re paying, why, and what you’re receiving).

Building on that, organize your evidence so a reviewer can approve it fast: label files clearly, match names across documents, and avoid edited screenshots. If you used a third party’s payment method, expect extra scrutiny.

Compliance isn’t personal, but it is procedural—and the fastest way out is giving reviewers exactly what they need, in a format they can approve without guesswork.

Conclusion

In 2026, legitimate dedicated crypto escrow platforms are getting rare but this is competition working as intended, not an extinction event. It quietly moved from a separate service towards a built-in feature of digital commerce and P2P marketplaces. Nevertheless, you should not unconditionally trust a centralized exchange’s escrow nor should you settle for whatever platform an internet search shows you the first. With the tips from our guide, you can now find the best option for a crypto escrow service that fits all your needs.

For even more useful guides like this one, browse the ChangeHero blog to get to know the crypto world better. Subscribe to us on social media to stay tuned to the updates: we’re on Twitter, Facebook, and Telegram.

Frequently Asked Questions

How long do withdrawals from crypto escrow take?

Crypto escrow withdrawals usually take minutes to hours, but the exact withdrawal time depends on two separate clocks: the platform’s internal processing and the blockchain network’s confirmation speed. For reference, CryptoExchange Escrow, where an escrow agent is involved, estimates their processing times to be 5 to 20 days long. People often blame “the network” when the real delay is actually account checks.

What happens to crypto funds in escrow if the deal deadline passes?

Escrow platforms usually freeze the release step when a deal deadline passes, and that’s intentional. A deadline is there to prevent one side from stalling forever while funds sit in limbo, but it also creates a clear moment when the platform’s rules kick in.

What happens next depends on the escrow model:

- Centralized escrow (platform-managed): the platform typically pauses the transaction and prompts actions like “mark as paid,” “confirm receipt,” or “open a dispute.” The escrowed crypto stays locked until the system sees a valid next step.

- escrow smart contract: the contract may enforce time-based conditions (for example, allowing a refund path after a timeout) or require an arbitrator/multisig action if the logic is more advanced.

When are escrow fees charged and what triggers them?

Escrow fees are usually charged at specific lifecycle points of a transaction, and the trigger is almost always an action that creates cost or risk for the platform. Fees usually kick in at the very beginning, upon completing a transaction, on conversion, or upon withdrawal.

Can crypto escrow payments be reversed?

Centralized escrow payments are sometimes reversible in a narrow, rules-based way, but escrow is designed to make casual reversals difficult. That’s not a bug. It’s the entire point of reducing counterparty risk.

How long do crypto escrow disputes typically take?

Escrow disputes typically take anywhere from a few hours to several days, and complicated cases can stretch to 1–2 weeks if evidence is unclear or third-party verification is needed. The range is wide because “dispute” can mean anything from a simple receipt mismatch to a full-on argument about whether services were delivered.