Pending Transactions in Payments vs Crypto

Key Takeaways

- ⏳ Pending transactions mean authorization hold that reserves funds or available credit but has not yet settled. In cryptocurrency-related context, this might refer to fiat transactions on hold or unconfirmed transactions on blockchain.

- ⏳ Pending transaction starts with authorization that places the hold, followed by clearing that can see amounts adjusted (tips, partial shipments, incidentals) and finished at posting that updates the current balance. The flow is slightly different in crypto: broadcasting that puts the transaction in a queue, first block inclusion that tentatively confirms it, and a number of consecutive block confirmations that settle the transaction for good.

- ⏳ Unlike traditional payment rails, which often have processor-, merchant- and issuer-side recourse, options for crypto users in the event of an unauthorized or fraudulent pending transaction are limited. In turn, crypto payments have much shorter pending spans and are not affected by business hours.

Contents

When using cashless payments, you might encounter pending transactions, and from experience, it is usually not hard to understand that it is an authorization or temporary hold placed on your account—not yet a final, posted charge. What a lot of people want to know, though, is the mechanics of current balance vs. available balance, clearance times, and implications of these types of transactions.

In crypto, pending transactions can take on a slightly different meaning: ones that have not yet been recorded in a blockchain or not yet validated. However, since crypto on-ramps commonly use cashless payment methods, in this guide, we are going to cover both and highlight their differences.

How Pending Transactions Are Processed

Pending transactions move through three distinct stages—authorization, clearing, and posting—that transform a simple card swipe or ACH initiation into a finalized ledger entry on your bank statement. The “pending” label refers to holds placed on your available balance during authorization, while settlement mechanics in clearing determine the actual amount debited, and posting converts provisional data into permanent transaction history.

When it comes to cryptocurrency transactions, blockchain itself is a distributed ledger. Instead of relying on a bank to process a transfer, you would need validators to approve it before it even gets into a queue.

Authorization

Authorization begins the moment you initiate a purchase or transfer. When you tap your debit card at a coffee shop or enter payment details online, the merchant’s processor sends an authorization request to your card issuer through the payment network. Your bank evaluates the request in real time, checking whether your checking account or credit card has sufficient available balance and whether the transaction triggers any fraud alerts. If approved, the issuer responds with an authorization code and immediately places a temporary hold—commonly called an authorization hold—on your account for the requested amount.

What you see in your app or banking interface at this stage is labeled as a “pending transaction,” though the technical term is an authorization hold. The data displayed is provisional: the merchant name may appear generic, the amount reflects the authorized sum rather than the final charge, and the timestamp marks when the hold was placed—not when funds actually leave your account. This distinction matters because the hold reduces your available balance instantly, even though your current balance remains unchanged until posting occurs later.

Two edge cases tend to surprise people during authorization:

- Partial approvals: Your issuer approves only what’s available, and the merchant decides whether to accept it or decline the sale.

- Reversals and expired authorizations: If the merchant never captures the transaction, the hold times out (often 3–7 days for debit cards, longer for credit cards) and disappears without a posted charge.

Tip-based merchants and pay-at-pump gas stations routinely authorize more than your expected final amount as a protective buffer. Restaurants often add a 20% cushion for tips, while gas pumps may place holds of $75–$125 because the system cannot predict how much fuel you’ll pump. It’s not comfortable to see in your app, but it’s how merchants protect themselves while the final amount is still unknown.

For crypto, this step is broadcasting your transaction. Instead of the merchant issuing the authorization request, your wallet does it on your behalf. The bank is replaced with the consensus layer, where nodes pick your transaction up and check if you can perform it: your balance is sufficient and your digital signature matches the public key. If one of the conditions is not met, the broadcast is discarded and nothing happens.

Clearing

Clearing—often called capture or settlement—bridges the gap between authorization and finalized charges. Merchants typically batch captured transactions at the end of the day and send them to their acquirer, including the authorization codes they received earlier. The payment network routes these batches to issuing banks, which validate each transaction against the original authorization.

This is where the “pending” amount can legitimately change. A restaurant adds the tip you wrote on the receipt. A hotel adds incidentals through incremental authorization. An online retailer ships only part of an order, so the cleared amount comes in lower than expected. The networks and issuers are built to handle these adjustments, which is why the pending amount isn’t always the amount that finally posts.

What can delay clearing?

- Batch cutoff timing: Submitting after a daily cutoff can push settlement to the next business day

- Weekends and holidays: Processing slows on non-business days while the hold stays in place

- Offline terminals: Some transactions are stored and transmitted later

- Merchant delays: Some merchants batch weekly rather than daily

- Network exceptions: Rare validation problems can suspend clearing until resolved

According to PNC Bank, most pending transactions resolve within 1–5 business days, and the bulk of that window comes from merchant capture and clearing—not the initial authorization. Moreover, weekends and bank holidays extend the timeline because business-day counting excludes them.

On the base level, blockchain transactions in most networks are not as sophisticated as to natively allow for this change in amounts from broadcasting to posting, even though this can be achieved by routing a transaction through smart contracts. In most cases, what you broadcast is what will be included in the block but what can change the total is the network fee. For instance, Bitcoin on the protocol level supports Replace-by-Fee (RBF) and Child-Pays-for-Parent (CPFP), which are both methods to change the network fee of a previous transaction.

And sometimes, this is needed to reduce the time a transaction spends in the “pending” queue, called mempool. Validators are incentivized to prioritize transactions with a higher network fee attached. A low fee is not always the user’s fault, since the fee recommendations can change faster than a block is produced, but even if it was intentional, bumping it up is usually possible, although depends on the software and recipient.

Posting

Posting is the final conversion: a cleared transaction becomes a permanent ledger entry. Once the issuer completes validation, the pending item becomes posted, and three things happen at once:

- The transaction appears in your official history.

- It becomes statement-eligible.

- Your current balance updates to reflect the settled debit or credit.

The transition also resolves the “provisional” nature of the pending record. Your OneKey App or bank portal now shows the finalized merchant name, the exact amount including adjustments, and the posting date that marks the ledger update. For credit cards, posting matters for statement timing and interest if you carry a balance. For debit cards, posting is the moment the funds definitively leave your checking account.

Two most common issues are:

- Clearing never happens: The merchant never captures, so the hold expires and disappears.

- Pending + posted overlap: You see both for a short period. This typically resolves within 24–48 hours, and you’re not charged twice.

Source: Rhino Bitcoin

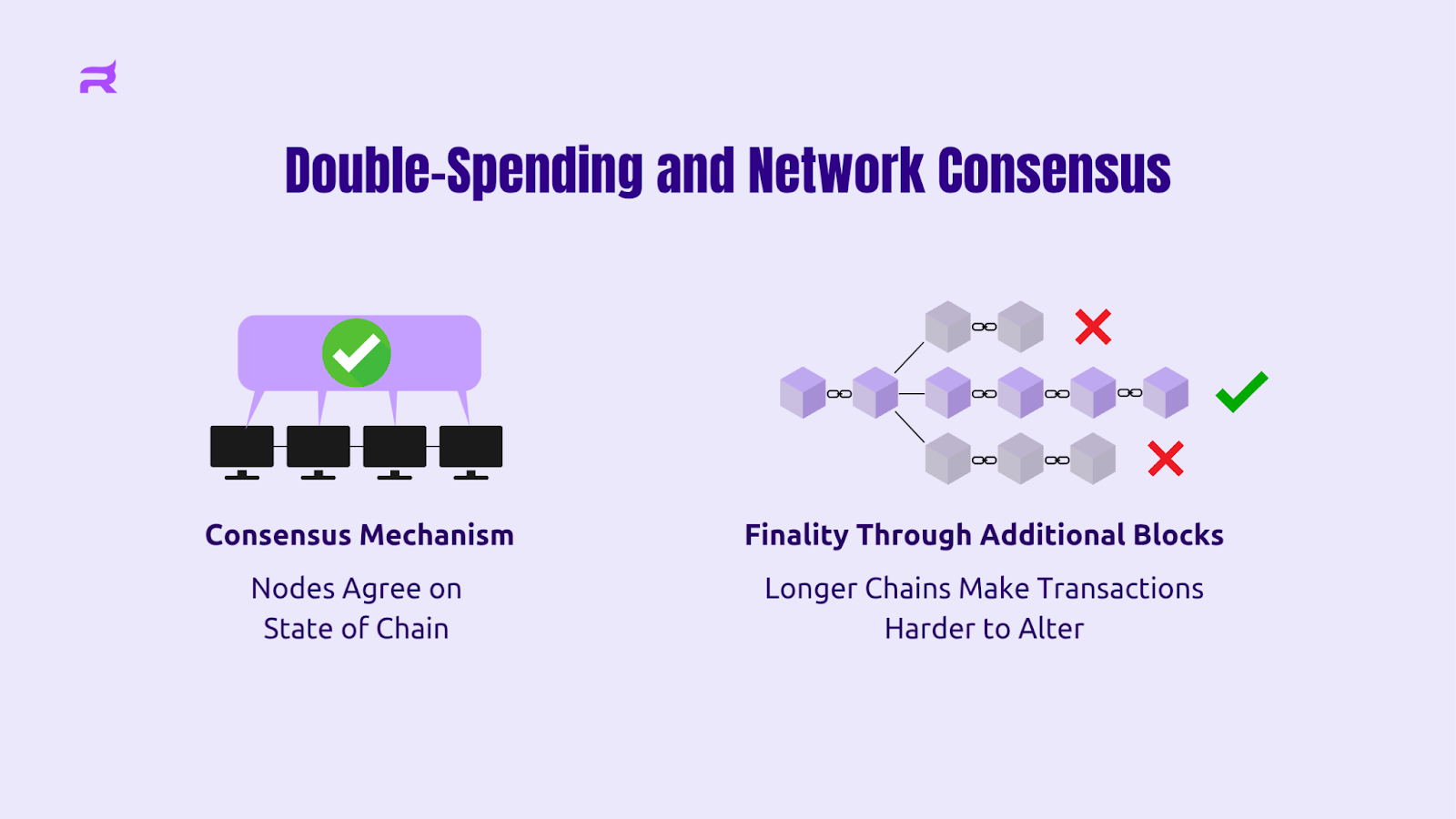

However, in crypto, posting is not always equivalent to your transaction finally included in a block. Rarely, one or more blocks could be produced by a misbehaving validator (not necessarily a bad actor, faults can arise due to poor synchronization etc.), and if the consensus about the validity of that particular block changes, it can get orphaned, discarding all entries that it put on the blockchain. The more blocks follow, the harder it is for records to be changed like that, so waiting for a few network confirmations is considered to be best practice against this risk. For example, even though Bitcoin transactions take about ten minutes to be recorded in the ledger, it is recommended to wait for six blocks to consider a transaction final, which prolongs the process up to a whole hour.

Pending vs Posted: Balance Impact and Account Effects

The real accounting difference is straightforward: pending transactions reduce your available balance through authorization holds, while posted transactions update your current/ledger balance and become part of your permanent record. If you only remember one practical rule, make it this one: your spendable money is governed by available balance, not by what’s already posted.

Available Balance

Your available balance follows a predictable chain:

- You initiate a purchase.

- The issuer approves and places a hold.

- The merchant captures for settlement.

- The hold is replaced by the posted charge.

- If the merchant never captures, the hold expires and your available balance “snaps back.”

Two common confusions explain most “my balance looks wrong” moments. First, available balance drops instantly while current balance stays still, creating a temporary gap. Second, available balance can jump upward when a hold expires, which looks like money reappeared—but it’s simply reserved funds being released. Moreover, this is why checking available balance is central to understanding real-time funds availability.

Current Balance

“Current balance” can mean slightly different things depending on the institution, but the practical mapping is consistent. For checking accounts, current balance typically reflects the ledger: posted activity only, excluding pending holds. For credit cards, current balance usually reflects posted charges since the last statement, again excluding pending authorizations.

If your institution uses labels like “ledger balance,” “book balance,” “available funds,” or “memo balance,” treat it this way: current/ledger is posted activity; available is posted activity minus active holds (or available credit minus posted charges and pending authorizations).

The way it works in crypto is somewhat more definite: your funds are considered unavailable as soon as the transaction is authorized (successfully broadcast). Crypto wallets normally reflect it accordingly. If it is not approved or reverted, your balance goes back to what it was before that transaction. If it is stuck in a mempool, however, neither you nor the recipient get the funds for the time being, which is why it can be a problem.

Ending Balance

Ending balance is the finalized total on your statement cycle or end-of-day record, and it includes only posted transactions up to the cutoff. Pending items are generally excluded until they post, which is why a purchase authorized on the last day of your statement cycle can show up on the next month’s statement.

Reconciliation tip: Use posted transactions and ending balance for statement matching—not the pending list. For account reconciliation, posted history is the clean source of truth.

Cash Flow

Pending holds in more traditional payment systems can be long enough to create timing mismatches that can disrupt your plan, especially with debit cards.

- Scenario one: A paycheck posts and boosts both current and available balance. Then a hotel places a large pending hold, reducing available but not current. If checks or bills post while the hold is active, you can trigger overdrafts or an insufficient fund fee even though your current balance looks fine.

- Scenario two: A restaurant authorizes $75, then posts $93 after tip. Your balance can “bounce” as the hold releases and the final amount posts, creating a net drop you didn’t budget for.

The takeaway is consistent: budget a buffer for variable-amount merchants, and track holds as reserved funds until the final post.

Spending Limits

Pending authorizations also consume limits immediately.

- Debit cards: Daily spending limits shrink as soon as holds are placed, even before posting.

- Credit cards: Pending authorizations reduce available credit immediately, which can cause declines even when your statement balance looks unchanged.

Edge case: Incremental authorizations in hospitality and rentals can stack, creating multiple simultaneous holds that eat into spending ability before anything posts.

Credit Utilization

Credit utilization has two “versions” in real life:

- Issuer-reported utilization: Usually based on posted statement balance at cycle close; it generally excludes pending.

- Real-time available credit impact: Pending holds reduce what you can spend right away.

So a large pending hold can limit your purchases without immediately affecting what gets reported—until it posts and hits your statement timing.

Typical Pending Transaction Timelines

| Payment Rail | Typical Duration | Common Delays | What Ends Pending |

|---|---|---|---|

| Debit Card | 1–3 business days | Offline processing, merchant batch timing | Merchant capture/clearing completes |

| Credit Card | 1–5 business days | Merchant settlement lag, tip adjustments | Final posting to statement cycle |

| ACH Transfer | 2–5 business days | Weekend/holiday cutoffs, bank verification batches | ACH settlement through network |

| Merchant Holds | 1–7 business days (varies by industry) | Incremental authorization, hold expiration policy | Final capture or automatic release |

What about pending times for crypto transactions? It all depends on the network: Bitcoin can take over an hour to settle; Ethereum has shorter block times so it takes a few more confirmations but is considered safely settled within 3–4 minutes. More speed-oriented networks (Solana, Monad, L2s) further condense the waiting times up to a couple of seconds—so something has to go wrong if your transaction shows up as pending for longer than even a minute there.

Common Causes of Pending Charges

Pending charges usually come from one of three layers: authorization holds, clearing/settlement delays, or operational decisions by merchants and processors. Moreover, you’ll often see overlap—like a gas station preauthorization plus delayed capture.

Preauthorization

Preauthorization is a temporary hold to confirm funds when the final amount is uncertain.

What you’ll notice:

- Placeholder vs. final amount: A rounded estimate or standard hold amount

- Descriptor differences: The pending descriptor may differ from the posted descriptor

- Immediate appearance: The hold shows up quickly, even though it isn’t posted

What ends it: Merchant capture, authorization expiration, or reversal.

Incremental Authorization

Incremental authorization is common in open-ended services (hotels, rentals) where the merchant adds to the hold as usage continues. Each increment may show as its own pending line item.

Reader check: Same merchant name, clustered timestamps, and multiple pending lines often indicate incremental authorization—not separate purchases.

Merchant Capture

Authorization is approval; capture is the merchant actually requesting payment. Pending persists when capture is delayed due to batching, shipping, backorders, or manual review.

Drop vs. post decision rule: If the authorization expires before capture, the pending item disappears without posting. If capture happens, it converts to posted.

Network, Bank, and Merchant Processing

Firstly, different queues handle authorization messages and settlement instructions, so delays can happen even after the merchant acts.

Edge cases:

- Weekend/holiday batch behavior

- Timeouts leading to duplicate pending authorizations

- Reversal lag (1–3 business days)

Secondly, banks may extend pending through fraud screening, ledger update cycles, nightly posting windows, or exception queues. Some items sit in an internal transaction queue before becoming posted.

What you can and can’t do:

- Customer service can verify while pending: Authorization details, merchant ID, active status

- Cannot be changed until posting: Most disputes require the posted transaction unless fraud is suspected

Thirdly, gateways and acquirers can also delay settlement through risk checks, delayed batch submission, partial captures, or re-authorizations.

Common confusion: If the delay is merchant-side, the merchant can act (void, cancel, expedite). If it’s bank-side, you’re often waiting for posting windows. In addition, if you want a hold released quickly, the merchant is usually the fastest route—your bank typically can’t cancel a valid authorization on your behalf.

Errors and Disputes: What to Do If a Pending Charge Looks Wrong

Image by DC Studio on Freepik

Crypto transfers are notoriously practically irreversible, and there is no customer support or even any single entity to resolve your issues to boot. The most frequent reason for loss of funds is user error, followed by scams that bank on this feature of the blockchain. To avoid mistakes, learn well how crypto transactions work in advance. If you are dealing with fiat payments, though, you have a lot of recourse.

Before disputing anything, make four checks: (1) pending vs posted, (2) descriptor mismatch, (3) duplicate entries that typically self-resolve within 24–48 hours, and (4) documentation—timestamp, amount, and descriptor screenshots.

Incorrect Amount

Many “incorrect” pending amounts are normal: tips, gas holds, hotel incidentals. If the pending amount is higher than your receipt by a predictable buffer, the excess typically releases when posting happens.

That being said, true mismatches deserve quick action. Collect your receipt, the transaction timestamp, and screenshots. Contact the merchant within 24–48 hours and ask for a corrected capture or a void of the authorization. If the merchant cannot confirm within 72 hours, prepare to escalate after posting (unless fraud is involved).

Next best action: If the merchant is unresponsive or the amount can’t be explained, proceed to Eligibility.

Unrecognized Merchant

Unrecognized descriptors are often parent companies or processors (“SQ”, “PAYPAL”), or delayed presentment from a purchase you made days ago. Check email receipts, shared account users, and the descriptor phone number.

If you see fraud indicators (unrecognized location, rapid-fire charges), lock your card, request a replacement, and enable alerts. Then follow the Bank Disputes path.

Next best action: Once identified or confirmed as fraud, proceed to Eligibility.

Reversed Authorization

A reversal might show as the pending item disappearing or as an offsetting negative entry. In most cases, no action is needed—holds release within standard windows.

Act only if the hold persists beyond typical timelines (often 5–7 business days for debit, up to 30 days for credit cards). Provide your bank with the original date, merchant, and amount and ask about manual release.

Next best action: If it doesn’t clear, proceed to Bank Disputes.

Failed Transaction

A decline can still leave a brief hold because funds were reserved before the failure completed. Check your bank’s status label, your merchant confirmation (or lack of one), and your receipt screen.

Avoid retrying repeatedly—each attempt can create a new hold. Ask the merchant to confirm whether they captured anything.

Next best action: If it posts despite failure, proceed to Merchant Disputes.

Eligibility

While pending, banks typically only intervene immediately for fraud, stolen card use, or identity theft. Most other disputes require the charge to post first. Standard timelines still apply: pending items often resolve in 1–5 business days.

Next best action: Based on eligibility, proceed to Merchant Disputes or Bank Disputes.

Merchant Disputes

Photo by LumenSoft Technologies on Unsplash

Use structured communication:

“On [date and time], I was charged [authorization amount] by [merchant descriptor]. Last four digits [XXXX]. Transaction ID/authorization number [if available]. The issue is [reason]. I’m requesting [remedy].”

Ask for the right fix: void the authorization (pending, no goods/services), issue a reversal (captured but needs undoing), or refund after posting (already finalized). Always request written confirmation.

Next best action: If unresolved, proceed to Bank Disputes.

Bank Disputes

Debit disputes on pending items rarely get provisional credit unless fraud is confirmed. After posting, formal dispute rights apply and investigations begin.

Credit card disputes are stronger once posted (Fair Credit Billing Act). While pending, issuers usually advise waiting unless fraud is suspected.

ACH disputes have their own timelines: incorrect authorized debits can often be disputed within 60 days; unauthorized ACH debits should be reported within 60 days for protection.

Only escalate when the merchant refuses, is unreachable beyond 72 hours, or fraud is confirmed.

Next best action: After filing, keep documentation and monitor for updates.

Documentation

Match evidence to your scenario: screenshots of pending details, receipts/invoices, cancellation confirmations, shipping proof, merchant correspondence, and a timeline log. Save everything until the transaction posts and the case is fully resolved—complex investigations can take 45–90 days.

Next best action: With your documentation organized, you’re ready for either merchant escalation or a bank dispute.

Things to Know about Pending Transactions

That gap between available balance and finalized charge is the source of most overdrafts, “duplicate charge” scares, and reconciliation headaches—especially when multiple holds stack at once.

Overdraft Risk

When it happens: Pending authorizations reduce spendable cash instantly on a checking account, even though your bank statement and posted history haven’t updated.

During the pending window:

- Maintain a buffer equal to 20–30% of your average daily balance

- Delay non-essential payments if large holds are active

- Confirm hold behavior for high-hold merchants (gas stations, hotels)

- Use available balance for decisions, not ledger balance

- Set reminders 3–5 days after large authorizations to confirm posting

Debit vs credit card risk contrast: Debit holds can trigger overdraft fees; credit holds reduce available credit but don’t drain your bank account cash pool.

Temporary Disappearance

A pending item can vanish because it expired, your app refreshed, or the merchant is between batches. Disappearance isn’t proof of a refund.

Reconciliation protocol:

- Check whether your available balance increased by the hold amount

- Wait 24–48 hours and refresh—many items reappear as posted

- Compare the original authorized amount to current balances

- Set a follow-up date 5 business days from the original pending date

- Screenshot details before the entry disappears

If your blockchain transaction was in the mempool while it was still pending, check your transaction history again—it could have expired and reverted.

Duplicate Pending Entries

Image by redgreystock on Freepik

What to do if you have two or more similar entries that are still pending?

- Same merchant + same amount + same timestamp: Likely a display duplicate; wait 24 hours

- Same merchant + different amounts: Possible incremental authorization or tip adjustment

- Two different merchant descriptors: Could be wallet/processor labeling; verify IDs and totals

Escalation (starting with support service) is only worth it if duplicates post separately as completed charges.

If your crypto wallet is displaying duplicate transactions, a check in the blockchain explorer is worth a peek. Most likely, this is a wallet's display glitch, but if it was double you will know it immediately.

Conclusion

In crypto, there are fewer reasons for why your transaction might be pending than in cashless payments. However, it does not make it less annoying, nor it somehow safeguards you against these when you are paying with fiat. Most often, in both cases, waiting for a while longer resolves this. What makes these scenarios different is that to confirm this, crypto users can use open-source public tools instead of trusting a bank or merchant.

Frequently Asked Questions

Is a pending transaction approved or not?

Authorization creates a temporary hold against your available balance. Check for “authorization” or “hold” labels; pending vs posted sections, if you are using an app or user dashboard. Monitor it for 3–7 business days and avoid repeat attempts. Keep in mind that authorization can expire without capture.

How does a pending transaction affect my balance?

Pending transactions immediately reduce your available balance while your current balance remains unchanged until the transaction posts. Your available balance reflects real-time spending power after subtracting pending holds, whereas your current balance shows only completed posted transactions.

Can a pending transaction be declined?

Transaction declines occur when your bank or card issuer rejects an authorization request due to insufficient available funds, risk controls, or processing mismatches. Existing pending holds can trigger declines even when your current balance appears adequate.

Can I cancel a pending transaction?

You cannot directly cancel a pending authorization through your bank because the hold represents the merchant’s request, not a completed charge you control. You cannot reverse a blockchain transaction either; your options are to wait for it to expire if the network fee is too low, or contact the recipient should you be able to. The second path rarely succeeds, especially if you do not know the recipient or they do not have your interests in mind.

How long until a pending transaction clears?

Most pending transactions clear within 3–7 business days, though the exact timeline depends on merchant category, payment rail, and processing queue factors. Business days exclude weekends and bank holidays.

What if a pending transaction fails?

Pending transactions that don’t complete follow one of three paths: expiration without posting, merchant void/reversal, or posting with a different final charge amount.

Can a pending transaction charge twice?

Duplicate pending authorizations often self-resolve during clearing, while duplicate posted charges require immediate action. Escalate if your funds moved twice in two cleared entries or persist beyond 7 business days.

Why is my pending transaction taking so long?

Extended authorization holds lasting 10–30 days occur with specific merchant categories where final charges remain uncertain until service completion.

- Why long holds happen: Hotels, rentals, fuel, cruises/resorts

- Exposure reduction strategies: Prefer credit for large holds; request itemized bills; ask for release after completion

- Documentation to request: Release confirmation, itemized final bill, timestamps

- Bank vs. merchant responsibility: Merchant controls release; bank usually can’t expedite valid holds