USDT vs. USDC: Which of the Two Stablecoins is a Better Choice?

Key Takeaways

- 💵 Prefer USDT when trading access is the priority: its liquidity depth and exchange pair coverage are unmatched across centralized and decentralized venues.

- 💵 Use USDC when compliance and reserve transparency are non-negotiable: monthly attestations and Coinbase's co-founding role give it a clear regulatory profile.

- 💵 Assume both tokens carry freeze and blacklist risk: Tether and Circle can immobilize addresses at will; controllability and custody controls are not optional concerns.

USDT and USDC are both dollar-pegged stablecoins, which begs the question: how are they different? Tether's USDT and Coinbase-backed USDC share the same $1 target price, yet they diverge sharply on transparency, regulatory posture, and how much control their issuers can exercise over your funds. Understanding those differences in practice—not just in theory—is what this guide is built around.

Stablecoin Overview

Definition

Fiat-collateralized stablecoins like USDT and USDC belong to the broadest category of dollar-pegged assets, but that category is not homogeneous. Here is a quick taxonomy to give you a bird’s eye view:

- Fiat-collateralized (USDT, USDC): Tokens issued 1:1 against cash or cash-equivalent reserves held by a centralized company. The peg is sustained through redeemability. Since both USDT and USDC belong to this category, this guide will discuss it.

- Crypto-collateralized (e.g., USDS): Tokens backed by on-chain crypto assets, typically over-collateralized to absorb volatility.

- Algorithmic: Tokens that use supply-adjustment mechanisms or protocol incentives rather than direct collateral to hold the peg. No central reserve exists.

- Hybrid models: Combinations of the above, often blending on-chain collateral with algorithmic stabilizers.

Classification introduces issuer-controlled risks: reserve quality, counterparty exposure, and redemption gating, which simply do not apply to protocol-enforced models in the same way.

Key terms used throughout this article:

- Issuer: The company that creates and manages the stablecoin (Tether for USDT, Circle for USDC).

- Reserve assets: The cash, treasuries, or other instruments held by the issuer as collateral to back outstanding tokens.

- Mint: The act of creating new tokens when a user or partner deposits eligible fiat currency.

- Burn: The destruction of tokens when they are redeemed, removing them from circulation.

- Redemption: The process by which a token holder exchanges stablecoin for the underlying fiat currency directly with the issuer.

Peg Mechanisms

The $1 peg for a fiat-backed stablecoin is not written into a smart contract—it is a balance produced by a specific loop of incentives. Here is how that loop works in practice:

- A customer deposits USD with the issuer or an authorized banking partner.

- The issuer mints an equivalent number of tokens and delivers them to the customer's wallet.

- Those tokens enter circulation: traded on centralized exchanges, decentralized exchanges, and used in DeFi protocols.

- If the token's market price rises above $1, arbitrageurs mint new tokens cheaply and sell at the premium until price falls back. If it drops below $1, they buy discounted tokens and redeem them for full dollar value until the discount closes.

- Redemption burns the tokens, contracting supply and reinforcing the peg from the other direction.

- Reserve composition and settlement latency can introduce short-term pricing friction: if reserves include illiquid instruments or banking delays slow settlement, the arbitrage loop takes longer to close, widening the transient deviation.

Reiterating: the peg is not enforced by protocol code. No on-chain mechanism automatically corrects a deviation. What actually holds the price near $1 is a combination of redemption expectations, active market making, and arbitrage capital. Remove any one of those, and the mechanism weakens.

The primary market is the direct mint/redeem channel between a qualified user and the issuer. Only participants with direct issuer access can interact here, and this is the only venue where the peg is mechanically enforced — you can always receive $1 of fiat for one token, subject to issuer terms. The secondary market covers every exchange, DEX pool, and OTC desk where tokens change hands between third parties. Market participants here cannot compel the issuer to act; they can only buy or sell, which means secondary-market pricing reflects sentiment, liquidity, and access — not an ironclad guarantee. During normal conditions both markets stay tightly aligned but during stress, they can diverge sharply.

Depegging

A deviation from the target peg called depegging occurs when a stablecoin's market price deviates from $1 by more than a narrow band (typically considered meaningful beyond ±0.5%) for a sustained period rather than a fleeting order-book gap.

A micro-depeg lasts minutes to hours and is usually self-correcting through arbitrage. A structural depeg persists for days or longer and signals a breakdown in one or more pillars of the peg mechanism. Triggers here are more serious: credible public doubt about reserve quality or solvency; a banking partner failure that freezes fiat flows entirely; or a regulatory action that blocks redemption activity in key markets.

USDT (Tether) Profile

Issuer: Tether Ltd.

Tether Limited, a company incorporated in the British Virgin Islands and operationally connected to iFinex Inc. (the parent entity also behind Bitfinex), issues and manages USDT. In practice, minting happens when a verified counterparty sends fiat to Tether's bank accounts; Tether then issues an equivalent amount of tokens on the requested network. Burns work in reverse: redeemed tokens are destroyed once fiat is wired back. What the issuer controls, critically, is the entire pipeline from fiat custody to token issuance to on-chain supply management, meaning USDT's peg relies entirely on Tether Limited's operational integrity and solvency at every step.

Direct redemption with Tether Limited is not available to retail users by default. Verified business customers and institutional counterparties can request redemptions, but Tether imposes a minimum redemption threshold of $100,000 and charges a 0.1% fee. Processing times can span multiple business days. For most retail holders, the practical redemption path runs through exchanges rather than Tether directly — which means peg stability, in practice, depends on secondary market liquidity rather than on-demand issuer redemption. In a stress scenario, that distinction matters enormously.

Tether Limited is not a bank and is not FDIC-insured, which has concrete implications: holders are unsecured creditors of the issuer, not depositors with government-backed protection. If Tether Limited were to face insolvency, token holders would have no priority claim under typical banking resolution frameworks and would depend entirely on whatever assets remain after senior obligations are met. Tether has registered as a money services business with FinCEN and is subject to MiCA considerations in the EU.

Tether’s Reserves

Tether publishes a reserve breakdown across several broad categories, each carrying distinct risk characteristics worth understanding before you treat USDT as "cash equivalent."

- Cash and cash equivalents (including bank deposits): This category provides immediate liquidity but carries counterparty risk — the specific banks holding these deposits matter, and concentration in any single institution creates exposure if that bank faces stress. In a depeg scenario, the ability to liquidate these assets quickly is actually the highest here, but only if the banks themselves remain solvent.

- U.S. Treasuries (T-bills and money market funds holding T-bills): This is typically and currently the largest component of Tether's reserves. T-bills carry minimal credit risk and strong duration stability (short-term instruments), but even here, a rapid liquidation demand — such as a sudden mass redemption — requires an orderly market to realize full value without slippage. A stress test would reveal whether T-bill positions can be unwound fast enough to meet institutional redemption flows.

- Secured loans and receivables: Tether has historically held a portion of reserves in loans collateralized by assets, often Bitcoin. This category carries both credit risk (counterparty default) and collateral risk (Bitcoin's price volatility). A sharp market downturn could simultaneously impair collateral values and trigger redemption demand.

- Other investments (precious metals, Bitcoin, equity stakes): This is the highest-risk bucket. These assets are illiquid relative to T-bills, price-volatile, and difficult to liquidate at scale without moving markets. Their inclusion in reserves adds potential upside for Tether's equity but directly increases reserve volatility from a backing perspective.

Having reserves is not the same as having those reserves clearly segregated and custodied in a holder-protective structure. Tether does not publicly disclose the specific custodians holding its assets or the legal structure governing how reserves are held in the event of insolvency. This means that even if the total reserve value is sufficient, there is no contractual mechanism guaranteeing that USDT holders have a first-priority claim on those assets. In a market stress event, the absence of formal segregation is a meaningful distinction — it separates a fully backed stablecoin from one that is merely asserting backing.

When reviewing Tether's reserve attestation documents, the most decision-relevant line items are: (1) the percentage allocated to T-bills vs. loans vs. other investments — shifts away from T-bills toward secured loans or Bitcoin over time are a signal worth tracking; (2) whether total consolidated assets exceed total liabilities, and by what margin; (3) the identity and independence of the attesting firm. Changes in reserve composition quarter over quarter are more informative than any single snapshot.

Attestations

An attestation is not an audit, and conflating them gives a misleading picture of Tether's disclosure quality and transparency. An attestation is a point-in-time engagement in which an independent accounting firm verifies that stated figures are consistent with records provided by the issuer — as of a specific date, under agreed-upon procedures. It does not assess internal controls, does not verify that reserves are held in perpetuity, and does not provide assurance about what happens between reporting dates. A full audit, by contrast, involves examination over an entire fiscal period, testing of controls, and broader scope. The key point here is Tether has provided attestations, not audits.

Tether publishes quarterly reserve attestations conducted by BDO Italia, one of the major BDO network affiliates. Each report typically discloses total consolidated assets, total liabilities, and a breakdown of reserve composition by category. Quarterly frequency means up to three months of unobserved reserve movement between reports, and the agreed-upon procedures scope means the attester is confirming figures, not independently sourcing or valuing every underlying asset.

Supply

Circulating supply refers to the number of USDT tokens currently issued and accessible in the market, as opposed to authorized supply (which represents the theoretical ceiling on issuance) or tokens that have been minted but are held in reserve or treasury accounts. Circulating supply is the commonly quoted market cap figure because it represents actual tokens competing for demand in the ecosystem, and it's the number most relevant to assessing real-world tokenomics and liquidity depth.

Because USDT supply is the largest of any stablecoin, its depth on exchange order books and DeFi liquidity pools is exceptionally high, making it the default settlement layer for many trading pairs. A rapid contraction in supply — even if driven by legitimate redemptions — can temporarily disrupt those pairs' liquidity and widen spreads.

USDT's circulating supply currently stands at approximately $190 billion. At that scale, USDT commands the deepest market depth of any dollar-denominated stablecoin, which translates to tighter spreads on major pairs and lower slippage on large trades — a practical liquidity advantage independent of any reserve quality comparison.

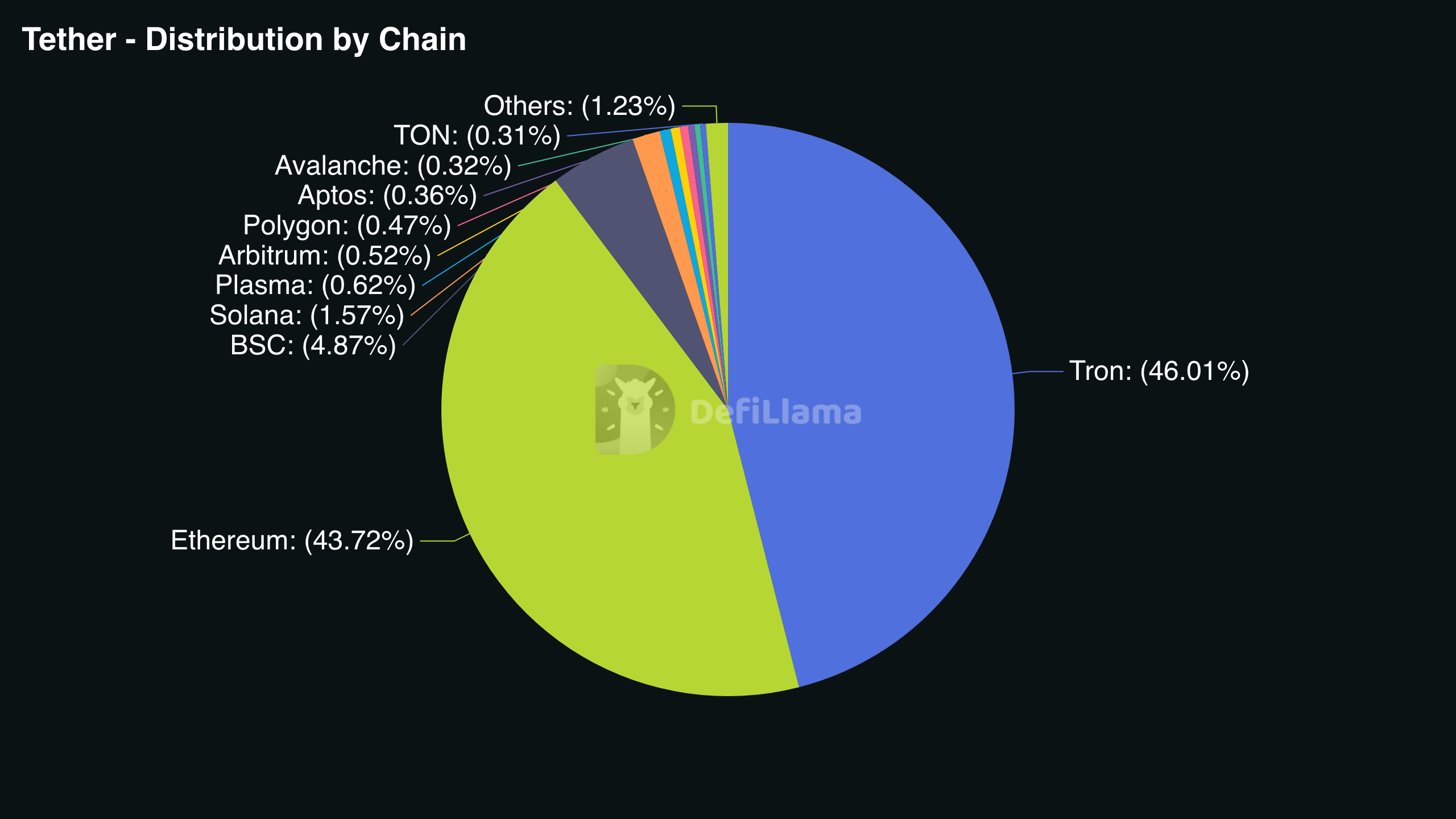

Blockchain Networks

USDT operates natively (i.e. without bridging) across more than a dozen blockchain networks. TRON remains the dominant choice for low-cost, high-throughput transfers — particularly for exchange-to-exchange or OTC settlement — because transaction fees on TRON typically run under $1 and confirmation times are fast. At the same time, Ethereum mainnet USDT provides the deepest DeFi integration and the broadest institutional recognition, but gas costs during congestion can make small transfers economically irrational. Ethereum Layer 2 networks (like Arbitrum and Optimism) offer a middle path: EVM compatibility with significantly lower fees, though liquidity depth varies. Other networks — Solana, BNB Chain, Avalanche — offer speed and low cost but with varying degrees of exchange support and DeFi integration maturity.

Each network has a distinct smart contract address: USDT on TRON (TRC-20) and USDT on Ethereum (ERC-20) are separate token deployments, each backed by Tether's reserves independently. Cross-chain transfers typically require bridges, which introduce their own smart contract risk and latency. A user holding TRC-20 USDT who sends it to an ERC-20 address without bridging will lose funds.

Moreover, multi-network issuance creates liquidity fragmentation across chains, which affects arbitrage efficiency and price consistency. When USDT briefly depegs on one network, arbitrageurs must bridge tokens across networks to correct the spread, and bridging latency slows that correction. For users, fragmentation also increases the risk of wrong-network deposits: sending TRC-20 USDT to an exchange address expecting ERC-20, for instance, is one of the most common and costly user errors in stablecoin transfers and typically results in irrecoverable funds unless the exchange specifically supports recovery workflows.

Token Controls

Tether's USDT smart contracts across supported networks include several issuer-level control functions that every holder should understand as a practical risk factor tied to the centralization of this instrument:

- Freeze/blacklist: Tether can flag specific wallet addresses, rendering any USDT held in those wallets immobile. The typical trigger is a sanctions compliance obligation (OFAC-listed addresses) or a law enforcement request following theft or fraud. These funds become completely inaccessible until the freeze is lifted or legally resolved.

- Seize/transfer (on some deployments): On certain network deployments, Tether retains the ability to move tokens from a blacklisted address to another wallet without the original holder's consent. This has been exercised in specific theft recovery cases, in cooperation with law enforcement.

- Mint/burn authority: Tether's contracts grant exclusive minting and burning rights to designated issuer addresses. No third party can create or destroy USDT outside Tether's authorization. The implication of this function is that supply is entirely centralized, which eliminates unauthorized inflation risk but concentrates all control with the issuer.

- Pause (network-level, on some contracts): Certain contract implementations include the ability to pause all transfers across the network deployment. This has not been regularly exercised publicly, but the capability exists.

USDC (USD Coin) Profile

What is USDC? If you are completely new to it, catch up with our glossary before continuing with this guide!

Issuer: Circle

USDC, previously called USD Coin, is a U.S. dollar-pegged stablecoin issued and operated by Circle Internet Financial. Circle is responsible for minting new USDC when users deposit dollars, burning USDC when users redeem it, managing the underlying reserves, and enforcing the policies that govern the token's operation.

Coinbase, as a co-founder of the Centre Consortium that originally governed USDC, played a key distribution and governance role but Circle assumed full operational control of USDC following the dissolution of Centre in 2023.

Reserves

Circle backs every USDC in circulation with a 1:1 reserve of U.S. dollar-denominated assets. In practical terms, directly redeeming one USDC delivers one U.S. dollar. The reserve composition holds predominantly short-duration U.S. Treasury securities alongside cash held at regulated U.S. financial institutions — no commercial paper, no crypto collateral, no exotic instruments.

That said, no reserve is without a risk surface. Three areas matter most to readers assessing USDC's backing:

- Interest-rate risk: Minimal, given the short-duration nature of the Treasury holdings. Prices do not swing significantly on small rate moves.

- Banking and custody concentration: Cash reserves sit with a limited number of partner banks, introducing counterparty exposure if any one institution faces stress (as briefly demonstrated during the March 2023 Silicon Valley Bank event, when USDC temporarily de-pegged).

- Redemption settlement timing: Large redemptions are not always instant. Settlement windows and banking hours can create short-term liquidity gaps between a redemption request and the actual delivery of dollars.

Audits

USDC provides financial verification on one of the levels, not all three that are relevant: audit, attestation, and ongoing internal controls.

USDC provides monthly reserve attestations conducted by Deloitte, a Big Four accounting firm. These are not full audits in the regulatory sense, only point-in-time attestations confirming that Circle's reported reserves match or exceed the outstanding USDC supply.

These snapshots track total reserve assets, total USDC in circulation, and the reserve breakdown by category (cash equivalents vs. Treasury holdings). If the as-of date is more than six weeks old, the report predates the current month's cycle, and a newer one should be available shortly.

Supply

USDC's circulating supply refers to the total amount of USDC that have been minted and not yet redeemed, and total minted is a cumulative figure that includes tokens since burned on redemption. For liquidity and redemption purposes, circulating supply is the number that matters.

Likewise, supply changes in USDC are not algorithmic or driven by a protocol mechanism. They reflect direct mint/redemption demand: more dollars deposited means more USDC minted; more redemptions means more USDC burned. There is no expansion rule, no rebase, and no automatic issuance.

As of mid-2026, USDC's circulating supply stands at approximately $76.5 billion, reflecting renewed institutional appetite and growing on-chain settlement usage. USDC accounts for a meaningful share of on-chain stablecoin activity, with its volume reflecting genuine settlement usage rather than speculative trading flows.

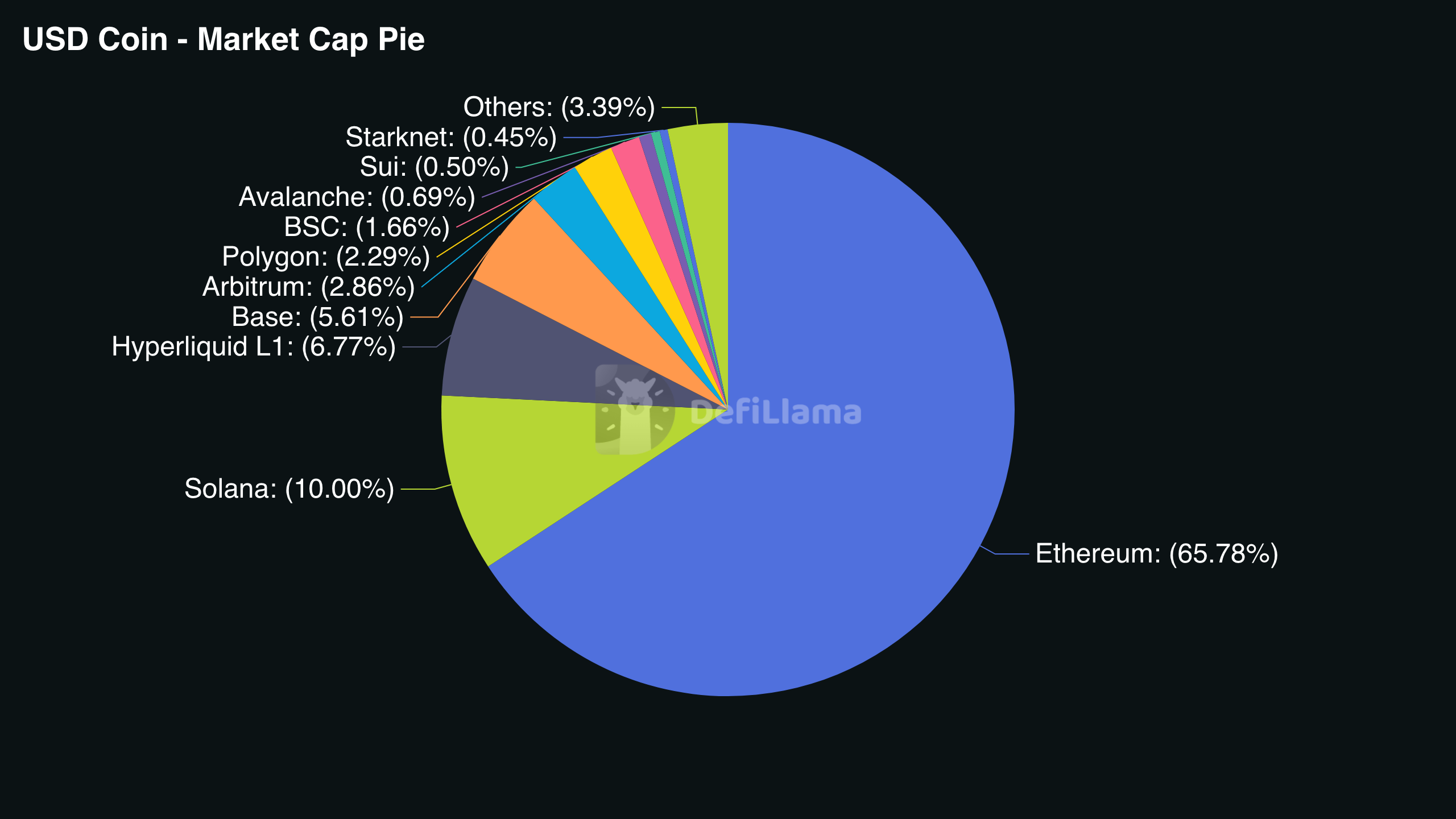

Blockchain Networks

USDC operates across a wide range of blockchain networks, but the distinction between native issuance and bridged representations is critical — and often overlooked.

Native USDC is supported on the most popular Layer-1 (L1) networks:

- Ethereum — the original deployment; highest liquidity depth, broadest DeFi and exchange support, but gas fees can be significant during congestion.

- Solana — native issuance via Circle's Cross-Chain Transfer Protocol (CCTP); fast finality and low fees, popular for high-frequency settlement.

- Avalanche, Base, Arbitrum, Optimism — native issuance on these networks, supported via CCTP.

Some chains display tokens labeled "USDC" that are actually bridged representations — tokens wrapped from another chain, not minted by Circle directly. Bridged USDC carries the additional risk of the bridge protocol itself, not just Circle's backing. Always verify whether the USDC on a given chain is labeled "USDC" (native) or "USDC.e" or similar (bridged) in your wallet or explorer.

Ethereum mainnet suits large, infrequent settlements; L2s like Arbitrum or Base suit frequent, smaller transactions. Ethereum L1 offers the strongest finality guarantees; L2 finality depends on the rollup's proof mechanism. Not all networks are equally supported for withdrawals and deposits across major platforms, mind you.

Token Controls

The original USDC deployment is an upgradeable ERC-20-style contract with several on-chain control primitives built directly into the token design.

- Blacklisting/Freeze: Circle can freeze any USDC address at the contract level, blocking all outbound transfers from that address. The frozen address cannot send USDC, but incoming transfers may still arrive.

- Mint/Burn authority: Only Circle's authorized minter addresses can create or destroy USDC. This is enforced at the smart contract level, not just at the policy level.

- Upgradeability and admin keys: The USDC contract includes an admin key structure that allows Circle to upgrade the contract logic. This introduces a governance dependency — contract behavior can change — though Circle has not historically used this to alter core token mechanics arbitrarily.

Similarly to USDT, if your address is blacklisted, you cannot transfer USDC out. The funds are not destroyed, but they are functionally inaccessible. Frozen addresses can be re-enabled if the circumstances that triggered the freeze are resolved, though at Circle's discretion.

These controls are a direct consequence of USDC's regulated, compliance-first architecture. Transparency about them is part of what makes USDC useful to institutions that require audit trails and enforcement mechanisms — and a consideration for users who prioritize censorship resistance above all else.

USDT vs USDC at a Glance

USDT and USDC serve the stablecoin market from two distinct angles: one built for raw liquidity and trading scale, the other engineered for compliance and institutional confidence.

Key Differences Between USDT and USDC

It’s about time to get to the point of the guide: you probably do not need us to tell you that USDT and USDC are two different dollar stablecoins with differences in reputation and structure. A guide might be of use when choosing one or the other, so let’s move right on to it.

Transparency

Transparency in the context of stablecoins can manifest in three ways: how frequently the issuer reports on reserves, how rigorous the assurance is, and how granular the backing asset breakdown is. These differences directly affect how much you can verify before trusting the peg.

As described above, USDC, issued by Circle, publishes monthly attestations conducted by Deloitte, with reserves held in cash and short-duration US Treasuries. USDT, issued by Tether, has historically reported quarterly and uses attestations rather than full audits, with a reserve composition that has included a broader range of assets beyond cash equivalents.

For institutional treasury teams and finance departments, reserve transparency is often a hard requirement before any stablecoin can be approved for corporate use. A monthly attestation by a named Big Four firm typically satisfies more compliance checklists than a quarterly self-reported summary. During periods of market stress, if a stablecoin's reserves include less liquid instruments, redemption pressure could theoretically stress the peg before holders can exit. Transparent, granular reporting reduces the guesswork and, consequently, the tail-risk premium investors mentally assign to a given stablecoin.

Regulatory Compliance

At the issuer level, Circle operates under US state money transmission licenses and has proactively engaged with regulators, while Tether is incorporated in the British Virgin Islands and operates under a different supervisory framework.

In the EU, MiCA (Markets in Crypto-Assets Regulation) rules on fiat-backed stablecoins began applying on June 30, 2024. By 2026, exchanges and payment platforms operating in the EU may treat USDT and USDC differently based on each issuer's compliance posture under MiCA. This could affect which stablecoin remains readily available for trading or spending within European platforms — worth monitoring if the EU is your primary operating jurisdiction.

Higher regulatory compliance at the issuer level generally reduces the risk of a stablecoin being delisted by regulated exchanges or cut off by banking partners. However, compliance also introduces censorship exposure: both Tether and Circle have the technical capability to freeze addresses or blacklist tokens at the issuer's discretion.

For most users whose priority is access continuity on mainstream platforms, USDC's compliance posture currently represents lower delisting risk. For users operating in jurisdictions with uncertain regulatory treatment, issuer-level compliance standing may itself become a platform availability signal worth tracking.

Liquidity

Liquidity is not a single number but a sum of a few parts. Order book depth and spread on top centralized exchanges determines the slippage cost of any individual trade. Breadth of trading pairs, particularly how often a stablecoin serves as the quote currency against altcoins, determines whether you can execute directly or need to route through an extra conversion step. Cross-chain availability affects bridging cost and slippage when moving between Ethereum, L2s, and alternative chains. And redemption and creation pathways determine how quickly large authorized holders can convert back to USD through institutional channels during periods of stress.

USDT currently leads on all four dimensions at most CEXs. It is the dominant quote currency across the widest range of spot and derivative pairs globally, which translates to fewer routing hops and generally better execution quality on long-tail assets.

DeFi Usage

On Ethereum mainnet and many L2s, USDC has a strong presence in lending protocols and stablecoin swap pools, partly due to its regulatory profile making it more acceptable to protocol governance communities. On other chains or in specific cross-border corridors, USDT remains dominant. The practical implication: before committing to a specific protocol or pool, verify which stablecoin has the deepest liquidity there and the lowest swap slippage.

On the institutional side, a SWIFT and Chainlink cross-ledger settlement demo involving USDC illustrated that institutional settlement experimentation is actively exploring USDC as the onchain settlement leg.

Payment Activity

Payments activity refers specifically to non-trading transfer usage: money moving between counterparties for goods, services, salaries, remittances, or invoices. Think merchant and payment rail integrations, remittance and peer-to-peer transfer patterns, and onchain settlement.

Last year, USDC processed higher adjusted transaction volume than USDT. The adjusted methodology attempts to strip out bot-driven and exchange-internal movements, leaving a cleaner signal of real economic transfers. This suggests greater non-trading usage for USDC relative to USDT.

On the institutional experimentation front, a SWIFT and Chainlink cross-ledger settlement demo involving USDC signals that enterprise-grade payment rails are actively piloting USDC for settlement — labeled explicitly as a demo rather than a live deployment.

Market Metrics and Liquidity

Liquidity separates a stablecoin that works in theory from one that works under pressure. The key is staying honest about what each metric actually measures: size, activity, or real execution quality.

Market Capitalization

Market capitalization in this context is simply circulating supply multiplied by approximately $1 — it is not equity value or a measure of profitability. USDT holds a commanding lead in this aspect. A larger float generally means deeper order books and lower slippage on large trades, since more supply is available across venues. That said, market cap alone does not guarantee redeemability at par or regulatory compliance.

Supply growth itself carries a dual reading. When Tether issues billions at a time, that signals strong exchange demand — essentially, markets need more liquidity rails. But rapid issuance can also flag concentration risk if supply growth is outpacing audited reserve verification.

Trading Volume

Trading volume in CEX spot and perpetual turnover — the raw exchange activity that determines bid-ask spreads and fill quality for active traders. If we understand volume as on-chain transaction volume, the utility metric that reflects payments, DeFi settlements, and real transfers between wallets, then the picture would be different.

Raw trading volume figures, especially on CEXs, can include bot-driven or wash-like activity that inflates turnover without reflecting genuine market depth. For this reason, adjusted transaction volume — transfers representing real economic activity — serves as a complementary and often more honest lens when evaluating utility for payments or DeFi protocols.

Exchange Coverage

Is a stablecoin actually usable for the specific pairs, networks, and jurisdictions you operate in or just exists on a given platform and that’s it?

Here is a practical checklist to run before committing to one stablecoin for trading or custody:

- Default quote currency: Check whether your target trading pairs (e.g., BTC/USDT vs BTC/USDC) are liquid on the exchanges you use. USDT remains the default quote on most major global CEXs, while Coinbase defaults to USDC and privileges it across its product suite.

- Network support for deposits and withdrawals: Verify which blockchains the exchange supports for each stablecoin. USDT is available on more chains in aggregate, but USDC's native issuance on Ethereum, Solana, Base, and other networks often means cleaner redemption paths versus bridged representations.

- Regulatory geography: EUR-region venues and MiCA-compliant exchanges have restricted or delisted USDT in certain contexts. If you operate across European venues, USDC's Circle issuer structure offers more regulatory predictability.

- Native vs bridged USDC: Some exchanges credit "USDC" that is actually a bridged or wrapped version rather than natively issued Circle USDC.

Price Stability

For stablecoins, it’s two distinct questions. How closely does the traded price track $1 across venues, under normal conditions and during stress? Can and will the issuer honor a $1 redemption at par, regardless of secondary market conditions?

To assess market price stability rigorously, look at four data points: (1) the average deviation from $1 over a rolling 30 or 90-day window, (2) the maximum intraday drawdown during documented stress events such as exchange collapses or broad market liquidations, (3) the time-to-repeg after a deviation — how quickly the arbitrage mechanism restores the peg, and (4) spread widening on major venues during volatile periods, since a coin can technically trade "near $1" while bid-ask spreads blow out enough to make execution costly.

Both USDT and USDC maintain tight pegs under normal conditions. Historical stress events, however, have shown USDC can temporarily depeg in correlation with issues at partner banks — as observed during early 2023 — while USDT has shown larger drawdowns during broader crypto market crises. The key distinction is that USDC's redemption mechanism through Circle is well-documented and has been exercised at scale, which supports redemption stability even when market price briefly diverges.

Key Considerations, Risks, and Drawbacks

Both USDT and USDC carry risks that most holders never think about until something goes wrong.

Reserve Risk

Reserve risk is the probability that the assets backing a stablecoin at a 1:1 ratio are insufficient, illiquid, or inaccessible at the moment you need to redeem. It breaks into four distinct sub-risks, each with its own failure mode.

- Asset quality. Reserves held in cash and short-duration US Treasury bills are the most liquid and lowest-risk collateral category. Reserves that include commercial paper, secured loans, corporate bonds, or other assets introduce credit and default exposure.

- Maturity and liquidity mismatch. Even high-quality assets create risk if they cannot be liquidated fast enough to meet simultaneous redemption demand.

- Concentration risk. If reserves are held at a single custodial bank or with one prime broker, that institution's disruption can lock reserves entirely.

- Disclosure cadence. There is a meaningful difference between a real-time reserve dashboard, a monthly attestation, and a full audit.

Rapid risk-off moves can trigger simultaneous redemption demand from large holders. If a banking partner is caught in a regulatory action, reserve access can be disrupted even when assets are nominally intact, causing a temporary gap between the secondary market price and the redemption price.

Counterparty Risk

Delivery or counterparty risk in stablecoins operates across three distinct layers.

- Layer 1: The issuer (legal entity). The failure mode is insolvency, regulatory shutdown, or a legal challenge that freezes operations entirely. Mitigation: diversify across at least two issuers.

- Layer 2: Banking and custody partners holding the reserves. The failure mode is a banking partner freeze or failure that prevents redemptions. Mitigation: monitor disclosed banking partners and concentration.

- Layer 3: Access rails (exchanges, payment processors, on/off-ramps). The failure mode is platform-level withdrawal halts or account restrictions. Mitigation: keep a portion on-chain in a wallet you control.

Redemption vs. secondary market liquidity is a critical distinction. "Being able to redeem with the issuer" and "being able to sell on a market" are not the same thing. If you do not qualify for direct issuer redemption, you are entirely dependent on secondary market depth during stress.

Smart Contract Risk

Smart contract risk changes materially depending on which network you are using to hold or transact USDT or USDC. It includes and is not limited to contract upgradeability and proxy patterns, admin key, mixing up canonical vs. bridged representations, and dependency risk (RPC, oracles, third-party infrastructure).

What to verify on a block explorer before engaging with any stablecoin:

- Whether the contract source code is verified and publicly readable

- Whether it is a proxy contract, and if so, what the linked implementation contract is

- Whether there are any token symbol collisions

- Recent mint and burn events

- The presence of privileged function signatures (pause, blacklist, freeze, upgradeTo)

Custody Risk

How and where you hold USDT or USDC shapes the nature of the risk you are actually taking. Self-custody risks: seed phrase loss, phishing, malicious approvals. Losses are often permanent. Custodial platforms risks: insolvency, withdrawal freezes, rehypothecation, account-level KYC/AML holds.

| Use Case | Recommended Custody Pattern | Operational Control |

|---|---|---|

| Long-term holding | Hardware wallet + minimal hot wallet exposure | Withdrawal allowlisting on any exchange account that holds residual balance |

| Active trading | Exchange custody only for active order balances | Transaction limits and withdrawal address whitelists |

| DeFi user | Self-custody with hardware wallet for signing | Revoke token approvals after each protocol interaction; use multisig for large holdings |

| Business treasury | Institutional or qualified custodian, or on-chain multisig | Multisig with geographically distributed signers, transaction limits, and regular approval audits |

Freezes, Blacklists, and Token Controls

Both USDT and USDC include on-chain control mechanisms that are written directly into their smart contracts. Issuer-level token controls operate at the smart contract layer and affect the token itself regardless of where it is held — on an exchange, in a DeFi protocol, or in a hardware wallet. An exchange freezing a user account is a platform-level action that restricts access through their interface but does not alter the on-chain token.

Common triggers for freeze or blacklist actions:

- Suspected fraud or theft

- Sanctions exposure or OFAC compliance obligations

- Law enforcement or court orders requesting asset preservation

- Regulatory investigations

- Platform-level policy violations (exchange-level account freezes)

- AML/KYC reviews that cannot be completed or have failed

Holding only one stablecoin on a single network through a single platform creates a concentration of operational risk. Splitting holdings between USDT and USDC, distributing them across two networks, and maintaining at least two independent withdrawal or liquidation routes means that no single failure point locks your entire stablecoin position.

Conclusion

Choosing between USDT and USDC ultimately comes down to what you need the stablecoin to do for you. If your priority is trading access and liquidity, the decision axis shifts toward USDT. If transparency, regulatory compliance, or institutional-grade payments matter more, USDC earns the edge. For those navigating DeFi or cross-border payments, usage patterns and counterparty risk both factor in before you move funds.

If you found this article helpful, the rest of ChangeHero blog is equally full of insights and knowledge about the crypto industry. To be updated daily on the state of crypto, follow us on Telegram, X (Twitter), and Facebook.

Frequently Asked Questions

Which Is Safer, USDT or USDC?

USDC and USDT carry different risk profiles depending on how you define "safer" — and that definition matters more than market cap alone; higher market cap does not equal safer.

- Reserve/issuer risk: USDC publishes monthly third-party attestations and holds reserves in cash and short-duration U.S. Treasuries. USDT relies on attestations rather than full independent audits, and its reserve mix has historically included assets beyond cash equivalents.

- Regulatory/operational risk: USDC is issued by a U.S.-regulated entity and is more likely to remain accessible on compliant, licensed platforms. USDT faces heavier scrutiny and has been delisted or restricted on some EU-regulated venues.

- Market/liquidity risk: USDT commands higher global liquidity and deeper order books on many major CEXes.

Can USDT Be Swapped for USDC?

Yes — via CEX, DEX, OTC, or wallet aggregator routes. Confirm both assets are on the same blockchain, and receiving address format matches the destination network. Verify whether the asset being received is native or bridged/wrapped. It wouldn’t hurt to check the pool depth or order book spread beforehand and record the transaction details for tax and accounting purposes.

Can Stablecoins Depeg From $1?

Yes — micro-depegs are often liquidity-driven and short-lived, while structural depegs are about reserves, banking access, or regulatory blocks.

Can USDT or USDC Be Frozen?

Both can be frozen at the smart contract level.

Practical implications:

- Self-custody: a freeze locks tokens in your wallet.

- DeFi: frozen collateral can break normal withdrawals and liquidations.

- Receiving funds: funds from high-risk sources can create secondary risk.

How Does MiCA Affect USDT and USDC in 2026?

MiCA’s stablecoin provisions became applicable on June 30, 2024, and by 2026 their effects show up mostly as platform-level availability changes and product restrictions.

Which Networks Support USDT and USDC?

Both are multi-chain, but always verify network support at the destination, fee levels, finality expectations, and whether you are using a native or bridged representation.