Ultimate Guide to USDT — What Is It & How to Utilize Tether Payments

Key Takeaways

- 💲 USDT (Tether USD / USD₮) is a dollar-pegged stablecoin designed to trade around $1, mainly to move value and trade without crypto-style volatility. USDT is not USD, not legal tender, and not a bank deposit — it’s a token issued by Tether Holdings Ltd, and its “stability” depends on issuer reserves + redemption mechanics, not deposit insurance.

- 💲 The peg is held together by issuance/redemption + arbitrage expectations, not an on-chain algorithm. Reserves are off-chain and verified by reporting, not block explorers: you can see USDT supply and transfers on-chain, but backing is a trust-and-disclosure problem.

- 💲 USDT exists on multiple blockchains as separate token versions (ERC-20 Ethereum, TRC-20 Tron, SPL Solana, etc.) — “USDT supported” is meaningless without the network, and a mismatch is one of the fastest ways to lose funds.

Contents

- 1. Introduction to Tether USD (USDT)

- 2. Tether (Issuer) and USDT Token Overview

- 3. How USDT Works

- 4. USDT Blockchains and Network Versions

- 5. USDT Value and Price Behavior

- 6. USDT Use Cases

- 7. USDT vs Other Stablecoins

- 8. Tether Controversies and Enforcement History

- 9. How to Buy, Store, and Use USDT

- 10. Conclusion

Disclaimer

This article does not constitute financial, legal, or tax advice. Stablecoins, including USDT, carry inherent risks: they can deviate from their $1 peg during periods of market stress or liquidity shortages, and blockchain transactions are irreversible once confirmed. Always conduct your own research and consult qualified professionals before making financial decisions involving cryptocurrency. Moreover, regulatory frameworks for stablecoins remain evolving, and risks related to issuer reserves, redemption policies, and jurisdictional differences exist.

Bitcoin may be the poster child for cryptocurrencies, but another digital asset is increasingly vying for its place as the most ubiquitous and widely adopted crypto. We are not talking about the second cryptocurrency, Ethereum; this status has been taken by Tether USD, the “dollar on crypto rails”. But is it all there is to it? In this guide, we will provide a comprehensive explanation of the largest stablecoin, USDT.

Introduction to Tether USD (USDT)

Let’s jump right into it with a definition. USDT is a dollar-pegged stablecoin issued by Tether Holdings Ltd that maintains a 1:1 value ratio with the U.S. dollar through a reserve-backed mechanism. An asset like USDT enables traders and users to hold digital assets with stable purchasing power across multiple blockchain networks. It works as a practical bridge between fiat currency and crypto markets: you can move value quickly, 24/7, without taking on the day-to-day volatility of assets like Bitcoin or Ethereum.

USDT is not equivalent to holding U.S. dollars in a bank account—its stability depends on Tether’s reserve management and redemption mechanism, and it carries risks traditional bank deposits do not.

As of 2026, USDT processed over $30 trillion in transaction volume, making it the dominant stablecoin by circulation and a cornerstone of global cryptocurrency liquidity. It is not a decentralized stablecoin governed by algorithms or community votes, and it does not generate yield on its own unless you deposit it into a separate lending or staking platform.

Tether (Issuer) and USDT Token Overview

Issuer: Tether Limited

USDT is sometimes defined as a centralized stablecoin, which means it has a single issuer that controls minting and burning. That issuer is Tether, operating through Tether Holdings Ltd and Tether Limited, and tied into the broader iFinex corporate structure which also operates the Bitfinex crypto exchange.

Every USDT token, regardless of whether it lives on Ethereum, Tron, Solana, or another chain, traces back to the same issuer and the same reserve and redemption policies.

The issuer is responsible for:

- Token issuance – Minting new USDT tokens on supported blockchains when customers deposit fiat currency or approved collateral.

- Redemption processing – Converting USDT back to fiat currency for qualified customers who meet verification and minimum threshold requirements.

- Reserve management – Maintaining the backing assets that theoretically support every USDT token in circulation at a 1:1 ratio.

- Attestations and reporting – Publishing periodic reserve reports and third-party attestations to demonstrate backing claim validity and transparency.

- Compliance and terms enforcement – Administering KYC/AML procedures, freezing addresses when legally required, and enforcing the Terms of Service.

A common misconception is that “USDT is a dollar” in the same way physical cash is legal tender. In reality, USDT is a token that represents a claim governed by the issuer’s terms of service — not a direct obligation from a government or central bank.

According to Tether’s official website (tether.to), the company states that “every Tether token is always 100% backed by our reserves, which include traditional currency and cash equivalents, and from time to time, may include other assets and receivables from loans made by Tether to third parties.” This claim is the foundation of USDT’s value proposition, but you should treat it as the issuer’s representation rather than real-time, cryptographically provable backing.

Token Naming

USDT naming looks simple until you interact with multiple exchanges, wallets, and explorers.

- “Tether” is both the brand name and the shorthand for the issuer in everyday conversation.

- “USDT” is the ticker symbol you’ll see on exchanges, in wallets, and on block explorers.

- “Tether USD” and “USD₮” are alternate presentation formats that show up in issuer materials and some apps.

Exchanges almost always display “USDT” in trading pairs (BTC/USDT, ETH/USDT). Wallet apps may show “USDT” or “Tether USD.” Block explorers typically show “USDT” plus a contract address (especially on Ethereum as an ERC-20).

How USDT Works

Issuance and Redemption

USDT operates in two overlapping markets: the primary market is where USDT is minted and redeemed directly with Tether Holdings Ltd. Access is limited to authorized participants (typically institutional clients, exchanges, or OTC desks). The secondary market, however, is where the vast majority of economic activity with USDT occurs: exchanges, on-chain transfers, and peer-to-peer movement of already-circulating USDT.

The primary issuance and redemption sequence follows a gated process:

- Mint Request: An authorized customer submits a request to Tether specifying the desired USDT amount and target blockchain.

- Compliance/KYC Gate: Tether conducts identity verification and anti-money laundering checks on the requesting entity before proceeding.

- Fiat Deposit: The customer transfers USD (or equivalent collateral) to Tether’s banking partners, with the exact amount matching the requested token issuance.

- On-Chain Mint: Tether’s smart contracts create new USDT tokens and assign them to the customer’s specified address on the chosen blockchain (Ethereum, Tron, etc.).

- Distribution: The customer typically deposits these tokens into centralized exchanges or distributes them via OTC desks, where retail users can acquire them.

- Redemption Request: An authorized customer initiates a burn request, signaling intent to convert USDT back to fiat.

- Token Return/Burn: The customer sends USDT to Tether’s burn address, permanently removing those tokens from circulation.

- Fiat Payout: Tether wires USD to the customer’s bank account, completing the cycle.

Most retail users simply buy and trade USDT on an exchange where it’s already circulating and use it like any other transferable token. In even simpler terms, chances are, you won’t even touch the stablecoin at any step beyond 6 (where secondary market activity is) but having it as context will help.

Peg Maintenance

USDT’s peg (link to its monetary value) is held together not just by redemption logic but also by arbitrage expectations; not by an automatic on-chain collateral system, in any case. The market logic is:

- If USDT trades at $0.99, arbitrageurs can buy discounted tokens and redeem them for $1.00 (if authorized), capturing the difference.

- If USDT trades at $1.01, authorized participants can mint new tokens at $1.00 and sell at the premium.

That push-and-pull creates price “gravity” toward $1. Retail users still benefit from this even without direct redemption access, because liquidity and the expectation that someone can redeem helps keep pricing tight.

When USDT trades meaningfully off-peg, it usually signals stress: liquidity constraints, reserve doubts, or friction in the redemption pipeline. Temporary deviations can happen during extreme volatility, especially when moving funds between venues or chains becomes expensive or slow.

Tether Reserves

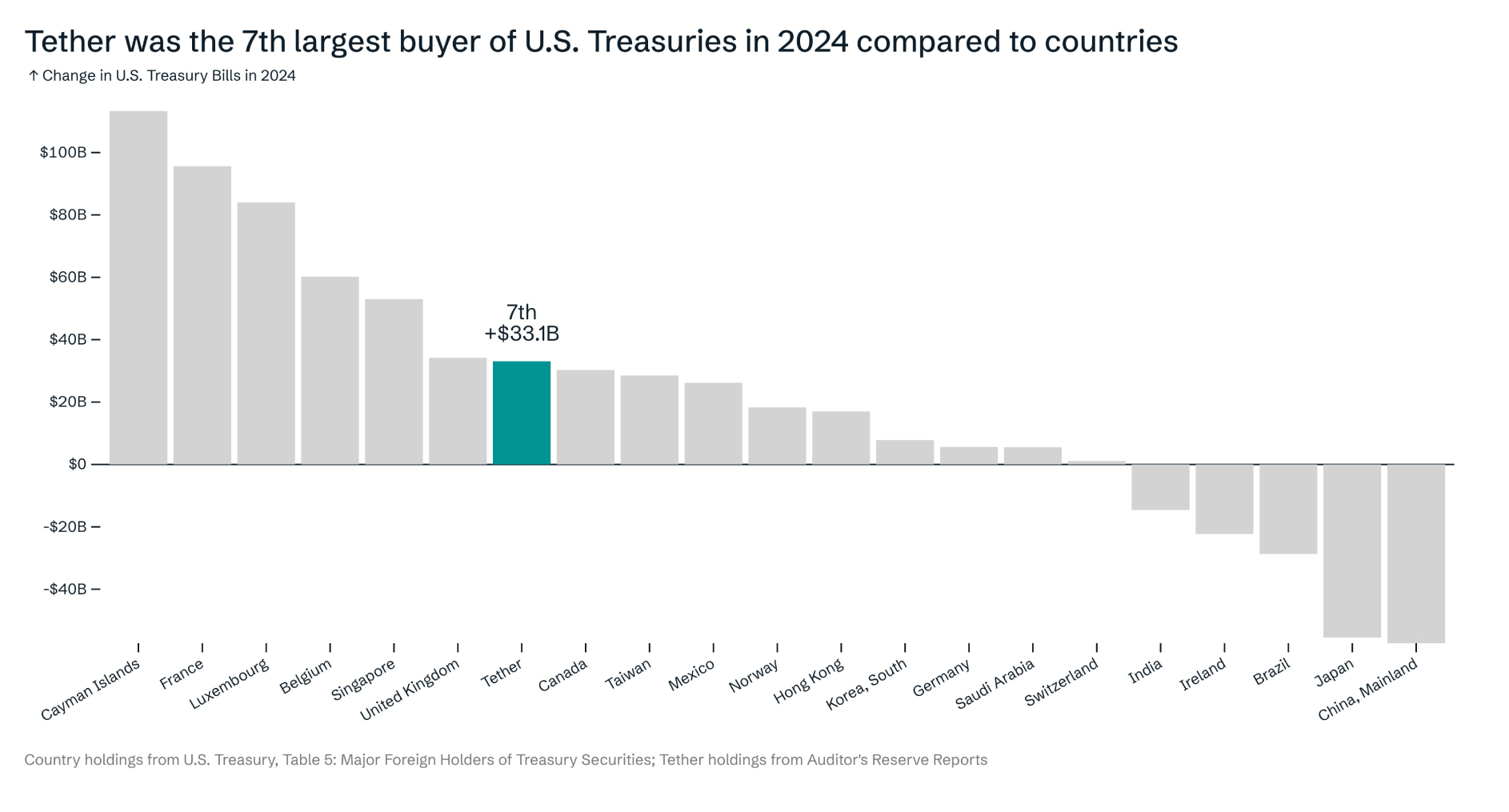

Tether states that every USDT in circulation corresponds to an equivalent value held in dollar reserve backing, claiming full reserve support for the token supply. So, it’s not just stacks of cash: reserves are categorized into cash, cash equivalents, and other assets. For years consistently, Tether reported holdings, with the majority of its reserves in U.S Treasuries, have positioned the company among the largest holders of U.S. government debt globally.

A savvy reader might already infer this: these reserves are off-chain. You can verify USDT supply and transfers on-chain, but you cannot verify the backing assets with a block explorer. On-chain data shows how many tokens exist; off-chain reporting claims what supports them. That’s why reserve verification is ultimately a trust-and-reporting exercise, not a cryptographic one.

Attestations and Audits

And speaking of this verification, to back its claims, Tether publishes attestations from independent accounting firms. An attestation is a point-in-time snapshot: it checks that reserves existed on a specific date and aligns with disclosed categories, but it does not provide the same depth as a full audit.

A full audit generally reviews financial statements, internal controls, and processes over time, offering broader assurance.

Attestations can prove:

- Total reserves equaled or exceeded circulating USDT supply on the measurement date

- Reserve composition matched the categories Tether disclosed in breakdowns

- Banking and custodial records aligned with reported balances at that snapshot

That being said, attestations cannot prove:

- Whether reserves remained adequate between attestation dates (intraperiod fluctuations)

- The quality or liquidity of “other assets” beyond face-value categorization

- Whether Tether followed consistent reserve management policies throughout the reporting period

Don’t get it wrong, attestations are still useful. They give structured checkpoints — just don’t confuse them with continuous, real-time proof.

Market Liquidity

Tether’s transparency is a subject of many criticisms but its role in the crypto market today is undeniable. USDT’s usefulness is inseparable from liquidity, which comes from three main places:

- Centralized exchange order books (Binance, Kraken, Coinbase) where USDT pairs are deep and fast.

- OTC desks and market makers (Cumberland, Genesis, and regional desks) for large trades with controlled slippage.

- Cross-chain bridges and wrapped versions that extend USDT across ecosystems, but can also fragment liquidity.

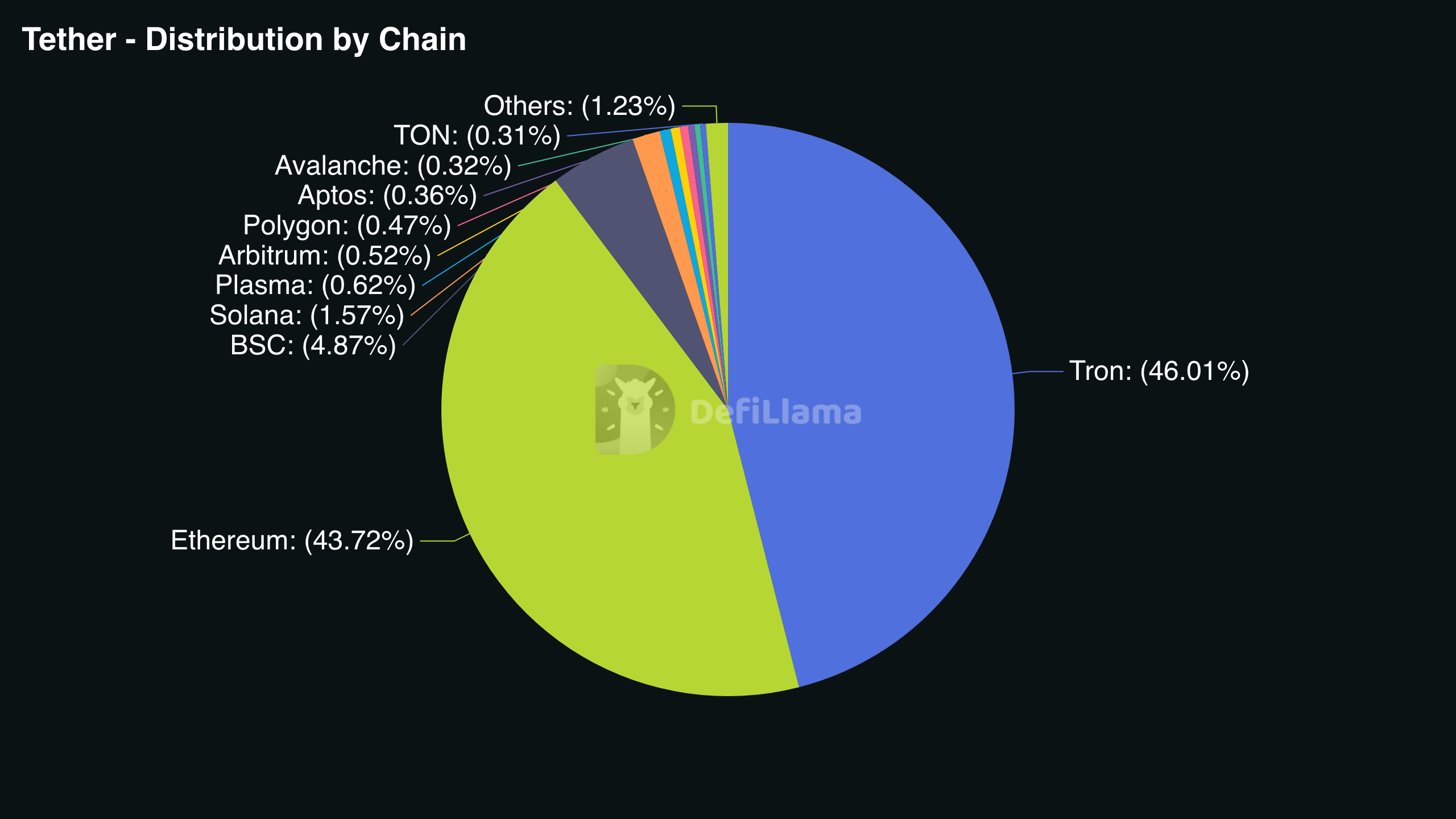

On top of that, USDT’s multi-chain support is a strength and a complication. USDT on Ethereum, Tron, and Solana are separate implementations, and liquidity on one chain does not automatically help another. On a day when Tron liquidity is thin, you can see worse spreads on Tron even if Ethereum looks perfectly stable — unless you bridge or route through an exchange.

Last year, USDT processed an estimated $55 trillion in full-year transaction volume, with USDT and USDC together representing the vast majority of stablecoin activity globally. Transfer counts and transaction patterns reveal substantial retail usage, with a large share of USDT transactions involving amounts under $1,000.

USDT Blockchains and Network Versions

As mentioned before, USDT is not “one universal coin.” It exists as separate tokens across multiple blockchain networks, each with its own token standard, address format, fees, and platform support. Why should you care? Knowing the difference will separate routine troubleshooting from total loss of funds.

Network Versions

The most common versions you’ll see are:

- ERC-20 USDT on Ethereum (addresses start with 0x, fees paid in ETH)

- TRC-20 USDT on Tron (addresses start with T, fees paid in TRX)

- SPL USDT on Solana (base58 addresses, fees paid in SOL)

USDT launched on Tron as a TRC-20 token in July 2019 to meet user demand for an alternative to Ethereum with lower transfer fees. Fast forward a few years, and TRC-20 has become a dominant transfer rail for low-fee USDT movement.

Beyond these, USDT also exists on Polygon, Avalanche, Aptos, and other networks — but you must verify support on your wallet and exchange. “USDT supported” is not enough; you need the exact network.

What changes between versions?

- Transaction fee payer and fee dynamics: during high congestion, Ethereum gas can range from $2 to $50+; Tron is often under $1; Solana is typically fractions of a cent. You must hold the network’s native token to pay fees.

- Confirmation and finality expectations: Ethereum deposits may require 12-35 confirmations; Tron often needs 19; Solana reaches practical finality quickly. Always check the receiving platform’s confirmation rules.

- Wallet and exchange support varies: Your wallet may support ERC-20 but not SPL; an exchange may accept TRC-20 deposits but not allow TRC-20 withdrawals.

- Bridging is not the same as sending: Cross-chain movement requires a bridge or an exchange route. You cannot “send ERC-20 to a Tron address” and hope it converts on its own.

Contract Addresses

In addition to wallet addresses, when using stablecoins and tokens in general, you might encounter so-called contract addresses. Contract addresses matter most on account-based chains (Ethereum, Ton, Polygon) and in DeFi.

The contract address is always chain-specific, just like regular addresses. Use an official source to find the contract address (recipient deposit page, CoinGecko, CoinMarketCap) and cross-check on the chain’s canonical explorer (Etherscan, Tronscan, Solscan). Confirm symbol/name/decimals. Legitimate Ethereum USDT shows “Tether USD,” symbol “USDT,” and 6 decimals; watch out for lookalike tokens and airdropped scams.

Wallet address (recipient address) where you send USDT, token contract address that identifies the token implementation on that chain, and transaction hash (TXID) that identifies a specific transfer are three separate things associated with each token transaction, not to be confused.

USDT Value and Price Behavior

Price Behavior

USDT usually trades close to $1, but “the USDT price” depends on where and how you look:

- Spot price on a centralized exchange (USDT/USD, USDT/USDC)

- Implied price via USDT pairs (BTC/USDT vs BTC/USD)

- OTC desk quotes and on/off-ramp pricing (which can include regional premiums)

Small premiums and discounts are often just microstructure: spreads, liquidity depth, local banking constraints, and redemption frictions.

USDT trades at a premium when demand spikes and fiat on-ramps are slow and at discount on a venue experiencing withdrawal fear or solvency rumors. The most practical signals to watch are bid-ask spread, order-book depth, and borrow/funding rates in margin markets.

Depegging Events

But what happens if the price discrepancy is significant or persists? This deviation, called depeg is about magnitude and duration, and it can be venue-specific. A $0.98 print on one exchange doesn’t automatically mean a system-wide issue.

- IF USDT trades below $1 on one exchange THEN compare against at least two other major venues and USDT/USDC pricing.

- IF withdrawal fees spike or networks clog THEN expect venue-specific distortions.

- IF discounts persist across multiple venues for hours THEN consider reducing concentration or diversifying into other stablecoins.

- IF USDT trades above $1.01 THEN check whether fiat access is constrained; premiums often resolve faster than discounts.

Secondary-market price is not the same thing as direct redemption value. It reflects immediate liquidity needs, perceived risk, and transaction friction.

USDT Use Cases

USDT is seeing such trading and transaction volumes because it solves practical problems: moving value quickly, avoiding volatility between trades, and operating in regions where banking access is limited. Here are the workflows that matter most.

Trading

Best for: Keeping funds liquid on-exchange while preserving value between trades.

- Typical workflow: Sell a volatile asset into USDT, wait, then buy back into the market.

- Why USDT is chosen: Fast redeployment and deep liquidity across pairs.

- Main constraint: Network support and withdrawal fees vary by platform.

Avoid network mismatches between platforms.

Hedging

Best for: Reducing volatility exposure without leaving crypto rails.

- Typical workflow: Convert volatile holdings to USDT to “park” value.

- Why USDT is chosen: No banking delay, broad exchange support.

- Decision cue: Prefer banks for long-term storage; prefer USDT for short-term liquidity.

Keep counterparty risk (no deposit insurance, issuer dependency) in mind when using USDT.

Exchange Transfers

Best for: Moving value between platforms quickly.

- Typical workflow: Withdraw USDT from Exchange A → wallet → deposit to Exchange B.

- Why USDT is chosen: Less volatility risk in transit vs BTC/ETH.

- Network checklist: Same network on both sides, correct address format, memo/tag if required.

Watch out for: Unsupported network deposits and recovery uncertainty.

Remittances

Best for: Cross-border transfers where banks are slow or expensive.

- Typical workflow: Acquire USDT → send on-chain → recipient cashes out locally.

- Why USDT is chosen: Low fees (especially on Tron) and fast settlement.

- Constraints: Local cash-out liquidity and KYC friction at on/off-ramps.

Mind the phrasing: “instant” often refers only to the blockchain step, not the full end-to-end process.

Decentralized Finance

Best for: Lending, borrowing, liquidity provision, and on-chain collateral flows.

- Examples: Aave/Compound deposits, AMM liquidity pools, DEX trading.

- Why USDT is chosen: Deep liquidity and multi-chain availability.

- Two DeFi risks: Smart contract risk and liquidation/impermanent loss mechanics.

USDT vs Other Stablecoins

| Attribute | USDT | USDC | USDS (DAI) | Why it matters |

|---|---|---|---|---|

| Issuer/Custody Model | Centralized (Tether Limited) | Centralized (Circle) | Decentralized (MakerDAO protocol) | Determines who controls reserves and can halt operations |

| Backing/Collateral Type | Cash equivalents, short-term deposits, commercial paper | Cash and short-term U.S. Treasuries | Over-collateralized crypto assets (ETH, WBTC, stablecoins) | Affects stability during market stress and liquidity events |

| Redemption Access | Limited to verified institutional partners | Direct redemption available to Circle account holders | Permissionless via smart contracts (burn DAI, unlock collateral) | Controls how quickly you can exit to fiat |

| Transparency Reporting | Quarterly attestations by third-party firms | Monthly attestations + audited reserves | On-chain collateralization visible 24/7 | Influences trust level and ability to verify backing in real-time |

| Censorship/Blacklisting | Can freeze addresses on supported chains | Can freeze addresses on supported chains | No blacklist capability (immutable smart contracts) | Critical for users in jurisdictions with capital controls or regulatory uncertainty |

| Typical Venues/Usage | Dominant on centralized exchanges, high cross-exchange liquidity | Institutional DeFi, regulated platforms, payment rails | DeFi collateral, lending protocols, decentralized exchanges | Dictates where you can use the stablecoin efficiently |

| Multi-Chain Footprint | 15+ blockchains (Ethereum, Tron, Solana, Avalanche, Polygon, etc.) | 10+ blockchains (Ethereum, Solana, Avalanche, Polygon, Base, etc.) | Primarily Ethereum mainnet and Layer 2s (Arbitrum, Optimism) | Determines cross-chain transfer options and gas cost flexibility |

| Primary Risk Exposure | Counterparty risk (issuer solvency, reserve composition) | Counterparty risk (issuer operations, regulatory compliance) | Smart-contract risk, collateral volatility, governance attack risk | Defines what could cause a depeg event |

USDT tends to win versus USDC on raw exchange availability and liquidity depth, while USDC tends to win on reporting cadence and issuer-facing redemption accessibility for those who qualify.

Compared to a decentralized stablecoin like USDS, USDT concentrates risk in the issuer. DAI concentrates risk in smart contracts, governance, and crypto collateral volatility. In DeFi, that difference is not theoretical — it shows up in liquidation mechanics and in how censorship-resistant (or not) your “dollars” are.

Tether Controversies and Enforcement History

Tether’s enforcement history is part of the risk landscape, not trivia. It shapes how exchanges list USDT, how institutions cap exposure, and how users think about reserves and redemption confidence.

The New York Attorney General (NYAG) investigation began in 2018, focusing on whether Tether and iFinex (Bitfinex) misrepresented USDT backing and concealed an $850 million loss tied to a payment processor. The settlement in February 2021 required $18.5 million in penalties, with no admission of wrongdoing, plus enhanced reporting and restrictions. After that, Tether began publishing quarterly attestations with reserve breakdowns. That improved visibility compared to earlier years, although critics continue to point out that attestations are not full audits.

Enforcement Actions

- Commodity Futures Trading Commission (CFTC) – United States → October 2021 → Allegation: Misrepresentation of USDT backing between 2016 and 2018 → Resolution: Settled without admission of guilt → Penalty: $41 million → Practical implications: Reinforced that “1:1 backing” claims must match reserve realities, not marketing language.

- Financial Services Authority (FSA) – British Virgin Islands → 2022-2023 → Allegation: Potential violations related to reserve management/reporting → Resolution: Ongoing regulatory review; no formal charges filed as of 2023 → Penalty: None publicly disclosed → Practical implications: Highlights jurisdictional oversight limits given the British Virgin Islands incorporation.

- Department of Justice (DOJ) – United States → Investigation opened 2018, no formal charges → Allegation: Potential financial crime violations → Resolution: No public resolution → Penalty: None → Practical implications: Residual uncertainty for exchanges and institutions.

Market Manipulation Allegations

Moreover, there are numerous allegations Tether used USDT to inflate Bitcoin’s price on Bitfinex with wash trading, but it’s essential to separate correlation claims from adjudicated findings. The NYAG and CFTC actions addressed reserve misrepresentation, not proven manipulation.

If you hold or use USDT, treat enforcement history as a reason to stay alert, not a reason to panic on every headline. Monitor quarterly attestations, pay attention to reserve composition shifts, avoid single-platform concentration, and keep at least one alternative stablecoin route ready.

How to Buy, Store, and Use USDT

USDT is popular because it’s easy to move — but that ease only holds if you handle networks, fees, and custody cleanly. Luckily, by now the choice of options is far from limited.

USDT Wallets

Self-custody users who want control over private keys and multi-chain access need a wallet that supports a specific USDT network (ERC-20, TRC-20, SPL, etc.). “Supports USDT” is not precise enough.

The usual wallet security best practices apply: install from official sources, create a new seed phrase, back it up offline, and confirm the wallet clearly labels USDT network variants (for example, “USDT (ERC-20)”). USDT is not interchangeable across networks by default (i.e. without swapping or bridging first).

Safety check:

- Confirm the network name matches on both the sending platform and your wallet.

- Copy the receiving address; never type it.

- Check memo/tag requirements where applicable.

- Send a small test amount first (10-20 USDT).

- Ensure fees make sense for your transfer size.

Moreover, if you ever add USDT manually, for example, in Metamask, get the contract address from authoritative sources — not from random posts, AI responses, or DMs.

USDT on Exchanges

For fiat purchases, trading, and bank cash-outs, centralized crypto exchanges remain the most competitive choice. Exchanges separate three actions that beginners often mix up: spot buy, convert, and withdraw.

What you will need to verify is which USDT network the exchange supports for withdrawals — not just deposits.

Overlooking KYC tiers and withdrawal holds is a common mistake for first-time exchange users. You can often buy USDT instantly, but withdrawing it may be locked until the fiat payment clears. What’s more, withdrawal fees can vary dramatically: ERC-20 commonly costs much more than TRC-20. Always check minimums and fees before you commit funds.

Onramps

However, there is a solid alternative to an exchange for first-time conversion from fiat to USDT: crypto onramps. They are gateways that let you buy crypto assets with delivery directly into your self-custody wallet. You can buy USDT directly, buy BTC/ETH first and convert, or use P2P with escrow.

Even then, “instant” does not always equal “instantly withdrawable.” Holds or KYC checks are common, especially with reversible payment methods.

USDT Transfers

Wallet-to-wallet sends and exchange deposits are only possible when the sender's network matches the receiver's supported network. Use test transfers, confirm memos/tags, and remember that bridged variants (like USDT.e) are not always treated as the same asset by every platform.

For more on how to send USDT, you can check out our dedicated guide!

How to choose the network? Is speed your priority? Choose Solana or Tron. Need the lowest cost? Tron or Polygon. Looking for DeFi ecosystem access? Ethereum. Want to try balanced efficiency? BNB Chain or Polygon.

If you sent USDT on the wrong network or missed a memo/tag, contact the receiving platform with TxID and details immediately. Do not expect refunds; reversals aren’t part of how blockchains work.

Cash-Out Methods

To convert USDT to fiat in a bank account, assess these methods based on your priority:

- Speed: Cards or P2P (often higher fees, lower limits)

- Lowest fees: Exchange sell + bank transfer (slower)

- Largest limits: Higher-tier exchange accounts or OTC

P2P cash-outs have distinct scam patterns. For one, fraudulent buyers send fake bank notifications or edited “proof” of funds being sent: always verify these things on your end and do not hesitate to reach out for arbitration in case of such dispute.

Conclusion

USDT is, in practice, a blockchain-native “digital dollar rail”: stable enough for everyday use, liquid enough for global trading, and flexible enough to move across multiple chains. That combination is exactly why it dominates stablecoin activity — and also why you should treat it as a tool, not a substitute for insured banking.

Browse the ChangeHero blog to learn more about the latest crypto news, projects, and platforms. And for quick bite-sized updates, follow us on social media: Twitter, Facebook, and Telegram.

Frequently Asked Questions

Is USDT backed by dollars?

USDT is backed by dollar reserve holdings managed by Tether Holdings Ltd, supporting redemption primarily through eligible exchanges and the issuer’s own channels, not direct holder-to-issuer conversions for all users. Reserves reportedly include cash and cash equivalents, U.S. Treasuries, and other assets managed by the issuer. Tether claims that every USDT token is backed 100% by these reserves, ensuring theoretical 1:1 redemption value and convertibility, though most holders access this value through market liquidity rather than direct redemption.

Why is USDT not always worth $1?

USDT temporarily deviates from $1 when liquidity imbalances, exchange-specific problems, network congestion, or broader market volatility disrupt normal trading conditions. Withdrawal halts on a major exchange, FUD about Tether’s reserves, or sudden large redemption requests create selling pressure that pushes price below the pegged target on specific venues. Moreover, network congestion (e.g., Ethereum gas spikes blocking arbitrage), regional demand surges (Asia premium vs Western markets), or risk-off sentiment across all stablecoins can cause fleeting discounts or premiums.

Is USDT safe for beginners?

“Safe” for USDT means price stability around $1, but it does not eliminate counterparty risk (Tether’s solvency), self-custody errors, or scam exposure—stable price ≠ zero loss risk.

The #1 beginner failure mode: Copying the wrong address or selecting the wrong network during withdrawal. To prevent it, double-check both the destination address format and the network dropdown before confirming, because no customer support can reverse a misdirected blockchain transaction.

Which blockchains USDT is on?

USDT exists as separate token contracts on different blockchains (Ethereum, Tron, Solana, etc.), meaning tokens on one network cannot directly move to another without using a bridge service or centralized exchange conversion.

Is USDT the same as USD?

USD is sovereign fiat currency issued by the U.S. government, while USDT is a cryptocurrency token issued by Tether Holdings Ltd that targets a 1:1 market value with the dollar through reserves and issuer redemption mechanisms—“1 USDT ≈ $1” reflects this peg, not legal tender status.